I’ve been investing for nearly 15 years now.

And guess what?

I’ve made so many mistakes.

While it would theoretically be awesome to be able to go back in time and avoid the mistakes before I made them, these mistakes were part of the learning process that helped me to grow and become better.

One of the biggest mistakes I’ve made, which has also allowed me to learn so much, is not focusing enough on the quality of a business before I invested.

Sacrificing quality in the name of anything else is almost always a bad idea.

And this is why I’m such a fan of dividend growth investing, a long-term investment strategy that prizes buying and holding shares in very high-quality businesses that pay safe, growing dividends to their shareholders.

By the very nature of this strategy, you’re almost automatically limited to some of the best businesses in the world.

To see what I mean, check out the Dividend Champions, Contenders, and Challengers list, which has compiled invaluable information on the US-listed stocks that have raised dividends each year for at least the last five consecutive years.

If you look at that list, you’ll find one household name after another (along with some hidden gems).

If you look at that list, you’ll find one household name after another (along with some hidden gems).

Boiling it down, it takes a great business to be able to generate the ever-larger profit necessary to afford ever-rising dividend payments.

And this is why I’ve been such an ardent follower of the strategy over the years, letting it guide me as I’ve gone about building my FIRE Fund.

That’s my real-money portfolio that produces enough five-figure passive dividend income for me to live off of.

In fact, I’ve been blessed enough to live off of dividend income since I quit my job and retired in my early 30s, and my Early Retirement Blueprint describes how that was made possible.

Now, as much as I’m a quality-first kind of investor these days, it should be said that valuation at the time of investment is also a crucial aspect of sound capital allocation.

Price only represents what you pay, but it’s value that represents what you get.

Price only represents what you pay, but it’s value that represents what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Leaning into quality by building a portfolio of world-class businesses that pay safe, growing dividends is something that’s tough to go wrong with over time, especially if you insist on attractive valuations at the time of investment.

This may all be easier said than done in real life, particularly if one doesn’t fully understand the intricacies of how valuation works.

Well, that’s where Lesson 11: Valuation comes in.

Written by fellow contributor Dave Van Knapp, it expressly lays out the whole concept of valuation and even shares an easy-to-apply template which can be used to estimate the fair value of just about any dividend growth stock you’ll run across.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Eversource Energy (ES)

Eversource Energy (ES)

Eversource Energy (ES) is an American utility holding company.

Founded in 1927, Eversource Energy is now a $24 billion (by market cap) major utility player that employs over 10,000 people.

Eversource Energy operates regulated electric, gas, and water distribution utilities in the states of Connecticut, Massachusetts, and New Hampshire.

The Electric Distribution segment accounted for 62% of FY 2023 revenue (prior to eliminations); Natural Gas Distribution, 15%; Electric Transmission, 12%; and Water Distribution, 1.5%. Other accounted for the remainder.

The company serves approximately 4.4 million customers, with the vast majority of them (~3.3 million) being electric utility customers.

Regulated utilities can be really good long-term investments.

We cannot function in a modern-day society without the services (such as electricity) certain utilities provide.

Furthermore, power utilities operate through local monopolies, as there is usually only one provider in any one geographic area.

Combining this basic need with a localized monopoly creates a captive and beholden customer base which will automatically seek these services and pay for them.

It’s as close to “guaranteed” revenue as it gets.

On the flip side, because it’s easy to take advantage of this position of power, these utilities are heavily regulated by local governments and limited on just how much they can charge.

In exchange for investing in infrastructure and providing necessary services, utilities are allowed a reasonable rate of return on its investments.

There’s a “floor” underneath the business model that supports recurring revenue, but there’s also a regulation-induced “ceiling” on how much money can be made.

A bit of a double-edged sword.

But it’s a sensible trade-off, in my view.

Otherwise, we might have a world in which only a wealthy subset of society could afford to keep the lights on.

With that out of the way, Eversource Energy took what was “easy money” and made things more difficult by by pursuing offshore wind energy projects.

Investing outside of its core competency… didn’t pan out.

After completing the exit of its offshore wind business in Q3 2024, Eversource Energy is now a pure-play regulated utility (and the largest of its kind in the New England region).

This is an important distinction, as the misstep regarding offshore wind investments was an overhang on the business and stock that had really limited investor/market enthusiasm around this idea.

The stock has been mercilessly punished over the last several years.

Well, the offshore wind exposure is now gone, freeing up management to focus solely on its capital investment plan to fuel growth.

To this point, the company’s current plan calls for investing slightly more than $23 billion between 2024 and 2028 in order to upgrade core infrastructure, ensure dependable service to customers, and drive returns on these investments under its regulatory framework.

In particular, because its region is expecting electric demand to more than double by 2050, management is aggressively pursuing an electrification strategy.

The shift back toward its core competency, creating a clearer path toward acceptable returns on investment under its regulatory framework, should help the company to produce more reliable revenue, profit, and dividend growth over the coming years – something that Eversource Energy has historically been very good at for decades.

Dividend Growth, Growth Rate, Payout Ratio and Yield

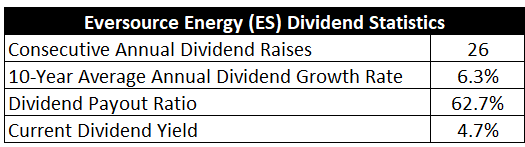

In point of fact, this company has increased its dividend for 26 consecutive years.

The 10-year dividend growth rate is 6.3%.

That’s very respectable for a utility.

You won’t find many power utilities out there that are growing their dividends materially faster than this.

It’s right about in line with what I’d expect.

It’s right about in line with what I’d expect.

But there’s something about this stock that definitely isn’t in line with what I’d expect.

And that’s its yield.

This stock yields a market-smashing 4.7%.

That is well ahead of what a lot of other utility stocks are offering right now.

Moreover, this is 170 basis points higher than the stock’s own five-year average, giving us an early indication that there’s some kind of disconnect here.

When the yield is near 5%, a mid-single-digit dividend growth rate is enough to get the job done.

A payout ratio of 62.7%, based on midpoint adjusted EPS guidance for this year, is a pretty commonplace level for this kind of business and shows a sustainable dividend.

Other than the yield, a lot of these dividend metrics are fairly “standard” for a power utility.

But that yield, which is unusually high and really pops out, is what makes this idea so uniquely interesting right now.

Revenue and Earnings Growth

As interesting as it may be, though, a lot of the dividend numbers I just went over are based on what’s already happened in the past.

However, investors must always be thinking about what’s likely to happen in the future, as today’s capital ultimately gets risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will come in handy when the time comes to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should give us enough information to make an educated judgment call on where the business could be going from here.

Eversource Energy moved its revenue from $7.7 billion in FY 2014 to $11.9 billion in FY 2023.

That’s a compound annual growth rate of 5%.

For a power utility, that’s solid.

Meanwhile, earnings per share grew from $2.58 to $4.34 (adjusted) over this period, which is a CAGR of 6%.

Again, right down the middle of the plate for a power utility.

The EPS growth lines up nicely with dividend growth over the last decade, showing prudence and awareness around capital management.

Now, I’ll quickly note that I did use adjusted EPS for FY 2023.

That’s because Eversource Energy took a massive $5.58 impairment charge related to the aforementioned offshore wind investments in FY 2023.

The ill-fated move into offshore wind is an ugly chapter for the business which showed poor judgment and execution on the part of management.

Fortunately, that chapter is now over.

However, the stock is still scarred and suffering (helping to explain the higher-than-usual yield) from this episode, which could be an exciting opportunity on a go-forward basis for new investors (albeit not so exciting for older investors who got in years ago).

Looking forward, CFRA believes that Eversource Energy will compound its EPS at an annual rate of 6% over the next three years.

Obviously, this is not a big leap at all.

It’s exactly in line with what Eversource Energy did over the prior decade.

I think the assumption of a continuation of the status quo is a reasonable one.

Management has continued to reiterate its long-term projection for 5% to 7% EPS and dividend growth, so 6% splits the middle and agrees with the proven past.

Midpoint adjusted EPS guidance for this year portends 5%+ YOY EPS growth, so I see nothing to indicate that CFRA is way out of line here.

With the offshore wind debacle behind the firm, and with an expected upcoming sale of its very small water utility business (freeing up capital for debt service and capital expenditures), Eversource Energy has a cleaner story based on being a pure-play regulated utility completely focused on electricity and natural gas.

With inherent population growth, the near-$25 billion capital spending plan that has implicit returns on investment, and natural increase in base rates, it’ll be difficult for Eversource Energy to not grow at a mid-single-digit rate over the coming years.

This is not a high hurdle to clear, yet the stock is still in the penalty box.

I think CFRA sums it up best here: “We view [Eversource Energy’s stock] as overly discounted vs. peers, as the shares recently traded at a ~26% discount to the peer median despite only modestly lower earnings growth expectations.”

The market’s pendulum on any individual name can wildly swing from optimism to pessimism, and it does seem way too far in pessimism’s direction right now.

Even absent a rerating higher, the near-5% yield paired with ~6% dividend growth easily sets one up for a ~10% annualized total return, with about half of it coming from the outsized dividend.

If one is okay with a slower-growing power utility business, that’s about as good as it gets.

Financial Position

Moving over to the balance sheet, Eversource Energy has a weak financial position.

The long-term debt/equity ratio is 1.7, while the interest coverage ratio is under 1.

Its should be said this is a business model that carries lots of debt by design.

Growth plans are usually funded through equity and debt, as there is an implicit ROI guarantee from regulators.

However, even by the low standards of a power utility, these are poor numbers.

Eversource Energy has basically tripled its long-term debt load over the last decade, indicating that it’s better at compounding debt than anything else across the business.

Long-term debt now exceeds the total market cap of the company.

Getting sidetracked by the wind project harmed the business and its balance sheet, and it’ll take time to right this wrong.

That said, the interest coverage ratio looks even worse than it really is because of the large impairment charges.

As we move into FY 2025, the interest coverage ratio should improve and normalize into a low-single-digit range.

I’d also note the credit ratings for the parent company’s senior unsecured debt are squarely in investment-grade territory: BBB+, S&P; Baa2, Moody’s; BBB, Fitch.

Profitability is okay.

Return on equity has averaged 6.3% over the last five years, while net margin has averaged 8.9%.

Now, the averages were harmed by FY 2023 and the large impacts to GAAP results.

In normal years, Eversource Energy is seemingly producing ROE of around 9%, which is quite solid for a power utility (a business model that has a regulation-induced ceiling on returns on capital).

Utilities simply aren’t allowed to produce high returns on capital, which is something that does limit my enthusiasm when it comes to this business model.

Other than the balance sheet, which is scarred, Eversource Energy is running a really good utility business, and the growth plan revolving around electrification offers a lot to like.

And with economies of scale, along with monopolistic control over its service territories, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Competition, regulation, and litigation are omnipresent risks in every industry.

While competition is effectively eliminated through local service territory monopolies, regulation is magnified for this business model and purposely limits growth through a government-enforced regulatory framework.

Connecticut, which represents about 25% of the company’s earnings, has been a particularly challenging regulatory district.

The offshore wind debacle introduces many questions around execution and management’s ability to make intelligent decisions regarding sound capital allocation.

The company’s balance sheet is one of the worst I’ve seen in this space, heavily weighed down by debt and limiting the company’s financial flexibility.

Its territories have a “progressive” stance, which could see an increasing shift away from natural gas (impacting ~15% of revenue), and the further push into electrification heads this off, but the cold climates will likely require the usage of natural gas for heating for the indefinite future.

Natural disasters, especially fires, are always a possible hazard for utilities.

Power utilities are characterized by low risk profiles, and I don’t see anything different in this case.

But this stock is uncharacteristically cheap, with the stock still down more than 35% from pre-pandemic highs…

Valuation

The forward P/E ratio is now only 13.6.

That’s based on midpoint guidance for this year’s adjusted EPS.

Even for a utility, and even for one hobbled by debt, that is shockingly low.

Its five-year average P/E ratio is 22.6, and we are well off of that.

All other basic multiples are also far lower than their respective five-year averages.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 6%.

If you’ve been following along, you’d see how 6% is a “no-brainer” number.

It’s very close to the demonstrated 10-year dividend growth rate, it precisely lines up with the demonstrated 10-year EPS CAGR, and it’s dead on with the near-term forecast for EPS growth.

Furthermore, it’s right in the middle of Eversource Energy’s own long-term EPS and dividend growth guidance.

No need to complicate anything here.

The DDM analysis gives me a fair value of $75.79.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

While this is far from the highest-quality idea out there, the valuation seems to price in more than enough negativity.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates ES as a 4-star stock, with a fair value estimate of $73.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates ES as a 4-star “BUY”, with a 12-month target price of $72.00.

We have a pretty tight consensus. Averaging the three numbers out gives us a final valuation of $73.60, which would indicate the stock is possibly 16% undervalued.

Bottom line: Eversource Energy (ES) is running a solid power utility. Continued investments in electrification should help to fuel its growth agenda. Other than the balance sheet, it has very respectable metrics. With a market-smashing yield, mid-single-digit dividend growth, a reasonable payout ratio, more than 25 consecutive years of dividend increases, and the potential that shares are 16% undervalued, value-seeking dividend growth investors willing to take a swing on a beaten-up stock have a fat pitch coming right down the plate here.

Bottom line: Eversource Energy (ES) is running a solid power utility. Continued investments in electrification should help to fuel its growth agenda. Other than the balance sheet, it has very respectable metrics. With a market-smashing yield, mid-single-digit dividend growth, a reasonable payout ratio, more than 25 consecutive years of dividend increases, and the potential that shares are 16% undervalued, value-seeking dividend growth investors willing to take a swing on a beaten-up stock have a fat pitch coming right down the plate here.

-Jason Fieber

Note from D&I: How safe is ES’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 80. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, ES’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: Dividends & Income

Disclosure: I have no position in ES.