Becoming a successful investor over the course of one’s lifetime can be as easy or as hard as one wants to make it.

There are countless wildly complex strategies out there that one could delve into.

On the other hand, some of the very best and most timeless ideas in all of investing are extremely simple.

One example is sticking to quality.

There’s almost nothing in life where low-quality options are the best options.

Be it the car you drive, the place you live in, or the food you eat, nobody willingly chooses junk.

Well, the same goes for the businesses you invest in.

Well, the same goes for the businesses you invest in.

This is why I’m such a fan of dividend growth investing.

This is a long-term investing strategy that prioritizes high-quality businesses that pay safe, growing dividends to shareholders.

Because growing cash dividend payments basically require growing profits in order to sustain that economic behavior, the strategy almost automatically filters one right into the great businesses out there which are able to routinely grow their profits.

You can see what I mean by checking out the Dividend Champions, Contenders, and Challengers list, which has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

It’s hard not to notice how many great businesses are on this list.

By following this strategy for more than 10 years myself, I’ve been able to build the FIRE Fund.

This is my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

I’ve been fortunate enough to experience a lot of success with the strategy, as the wealth and passive dividend income that emanates from the Fund allowed me to quit my job and retire in my early 30s.

How was I able to do that?

How was I able to do that?

My Early Retirement Blueprint lays it all out.

So I mentioned quality earlier.

Another timeless and yet simple idea in investing is to pay very close attention to valuation and make sure that you invest when it’s sensible to do so.

See, price is only what you pay, but it’s ultimately value that you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Simple ideas are often the best ideas, and buying high-quality dividend growth stocks when they’re undervalued is a simple and yet highly effective way to invest over the long term.

Of course, undervaluation is a lot easier to spot when you already understand how valuation works.

And that’s where Lesson 11: Valuation comes in.

Written by fellow contributor Dave Van Knapp, it describes valuation in basic terminology and even provides a valuation template that can be used to quickly estimate the fair value of just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Huntington Ingalls Industries Inc. (HII)

Huntington Ingalls Industries Inc. (HII)

Huntington Ingalls Industries Inc. (HII) is a major American defense company, operating as the largest independent military shipbuilder.

Founded in 1886, Huntington Ingalls is now a $7.5 billion (by market cap) military mammoth that employs more than 40,000 people.

Huntington Ingalls primarily designs, constructs, maintains, and repairs a range of nuclear and non-nuclear ships. These ships include aircraft carriers, submarines, and amphibious assault ships.

The United States Navy is by far the company’s largest single customer, representing approximately 80% of total annual revenue.

The company operates across three segments: Newport News (primarily nuclear ship design and construction), 55% of FY 2023 revenue; Ingalls (primarily non-nuclear ship design and construction), 24%; and Mission Technologies (primarily fleet services and support), 21%.

There are a lot of things to like about this business.

First, there’s just the general, long-term tailwinds for defense contractors, in general, due to human nature and the omnipresent need for sovereign defense.

Sovereign nations cannot exist without defense products.

Humans have been fighting with each other since the dawn of time.

We used to fight with rocks.

And now we use advanced machinery like nuclear-powered aircraft carriers.

That leads me to the second point, which is the fact that Huntington Ingalls is the only company that manufactures certain products for the US military.

That includes nuclear-powered aircraft carriers, which circles back around to what I just mentioned.

If the US military orders a nuclear-powered aircraft carrier, Huntington Ingalls will be the company to build it.

It has a monopoly over its domain, which is incredibly attractive – and that’s within a broader industry that operates oligopolistically (i.e., there are only a handful of prime US defense contractors).

This leads me to another reason to like Huntington Ingalls.

Simply put, defense products are becoming increasingly complex and expensive.

Rocks are cheap and simple; nuclear-powered aircraft carriers are extremely expensive and complex.

This technological evolution in defense products builds growth – via ever-more expensive machinery brought to market – right into the business model.

Furthermore, this further entrenches the established companies that command the scale and know-how necessary to manufacture the appropriate products for modern warfare.

This combination of inherent necessity, ever-increasing complexity/cost, and monopoly over certain products all position Huntington Ingalls and its shareholders for rising revenue, profit, and dividends for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

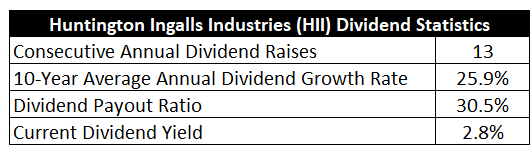

Already, the company has increased its dividend for 13 consecutive years.

The 10-year dividend growth rate is 25.9%, which is astounding, but there’s been a marked deceleration in dividend growth of late.

The five-year dividend growth rate is 10.7%, and the three-year dividend growth rate is 5.9%.

This slowing in dividend growth isn’t due to lack of a book of business but rather that the cost of projects has risen and labor has become more difficult to source.

In some ways, this company has become a victim of its own success.

In some ways, this company has become a victim of its own success.

But Huntington Ingalls doesn’t need to reinvent the wheel here.

Getting back on track requires some simple fixes to identified problems, and it’s hard to see how or why those fixes can’t or won’t be implemented.

While dividend growth has recently slowed, the stock’s yield has risen to 2.8%.

That easily beats what the broader market offers.

And this yield is also 70 basis points higher than its own five-year average.

So those buying shares today are getting paid quite a bit more income on the same invested dollar while they wait for Huntington Ingalls to clean things up and work through its massive book of business.

This higher yield makes the idea more alluring than it was before.

And with a payout ratio of just 30.5%, the company’s dividend is easily covered and has headroom for more growth.

Revenue and Earnings Growth

As alluring as the fresh setup may be, though, many of the dividend metrics are looking backward.

However, investors must always be looking forward, as today’s capital is being risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be useful when later attempting to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this way should allow us to build a reasonable model of where the business might be going from here.

Huntington Ingalls increased its revenue from $7 billion in FY 2014 to $11.5 billion in FY 2023.

That’s a compound annual growth rate of 5.7%.

Not bad.

I like to see a mid-single-digit (or better) top-line growth rate from a fairly mature business like this, and it delivered.

Meanwhile, earnings per share grew from $6.86 to $17.07 over this period, which is a CAGR of 10.7%.

Very solid.

Tough to dislike a double-digit bottom-line growth rate.

Excess bottom-line growth was fueled by margin expansion and share buybacks.

For perspective on the latter, the outstanding share count has been reduced by approximately 18% over this period.

Looking forward, CFRA believes that Huntington Ingalls will compound its EPS at an annual rate of 5% over the next three years.

This forecast, if it were to materialize, would represent EPS growth getting cut in half relative to what the business produced over the last decade.

I think CFRA is right to be cautious regarding the near-term growth potential for Huntington Ingalls.

As I said earlier, this company has, arguably, been a victim of its own success.

On one had, Huntington Ingalls finished its most recent quarter with a backlog of $49.4 billion.

That’s more than six times the size of the company’s entire market cap, and it amounts to several years of revenue all on its own.

Moreover, the company has been in the midst of a negotiation with the US Navy over the construction of Virginia-class Block V and Block VI and Columbia-class submarines, which will only add to the massive backlog.

But an agreement on the subs had been expected to be reached by now, and the delay introduces uncertainty and anxiety.

I’d just point out that a delay is not a cancelation.

And the backlog is undoubtedly keeping the business more than busy enough already.

However, this is one more piece of a puzzle that’s starting to reveal issues around execution.

CFRA highlights this: “…[Huntington Ingalls] has high exposure to long-term fixed-price contracts, which can suffer during periods of high inflation. Given cost overruns and uncertain timing of Navy contracts, the 2024 guidance for free cash flow was slashed to $0-$100M (from $600M- $700M) and the long-term free cash flow guidance was removed.”

The business is bumping up against older and now disadvantageous contracts in a new era of costs (almost all of the ships currently under construction were negotiated prior to the pandemic), compounded by cost overruns, supply chain kinks, and labor shortages.

It’s that last point that might be the biggest longer-term challenge the company faces.

While new contracts can catch up to new costs, and while execution on projects can be tuned, the company has faced retirements from experienced workers and had difficulties sourcing new labor to make up for the losses.

Huntington Ingalls noted this again when it reported Q3 results for FY 2024: “Second, our assumptions of performance improvement and risk reduction have not been achieved, due to late critical material deliveries from the supply chain and reduced experience levels within our teams, both in production touch labor and supervision. This leads to labor inefficiency, and in some cases to rework, which can affect program schedules.”

This is why I say the company is a victim of its own success.

There are no issues whatsoever with demand.

To the contrary, it has more work than it knows what to do with or can competently complete in a timely fashion.

It’s a good problem to have, no doubt.

Nonetheless, it is a problem.

CFRA sums it up well here: “The bigger risks to [Huntington Ingalls] are in execution, not demand, in our view, as the firm must estimate costs and time for shipbuilding, which is increasingly difficult as modern warships grow more complex in an environment of high inflation and skilled labor shortages.”

This is really the crux of the matter.

That said, I see this as a short-term problem against a long-term book of business that has, in some cases, no alternative options for completion.

Honestly, if Huntington Ingalls faced more competition for some of its work, I might be more concerned.

As it stands, though, they’re often the only game in town.

And so the company does have time to build and upskill its workforce while it simultaneously improves execution and new contracts.

Again, I don’t see anything unsolvable here.

Management knows its pain points (labor, cost overruns on existing projects, getting new contracts right-sized, etc.).

While it works through the challenges, it stands to reason that bottom-line growth will be slower than what it historically has been.

That would mean CFRA’s bottom-line growth rate forecast is a reasonable assumption, and that should translate to similar dividend growth.

That’s over the near term.

Over the long term, however, I see a quasi-monopolistic business with multiple tailwinds at its back, and geographic trends in the Pacific (such as what’s happening with China and Taiwan) augurs for a strong US Navy (and, thus, continued work for Huntington Ingalls).

The mid-single-digit dividend growth of recent times appears likely to continue over the next few years.

From there, problems that must be solved will almost certainly be solved, and that would put the business back on track for the double-digit bottom-line and dividend growth longer-term shareholders have become accustomed to.

And one starts off with a near-3% yield, getting paid handsomely to wait for all of that to play out.

Financial Position

Moving over to the balance sheet, Huntington Ingalls has a good financial position.

The long-term debt/equity ratio is 0.5, while the interest coverage ratio is approximately 10.

These are fine – certainly not outstanding – numbers.

In this case, though, I don’t think an outstanding balance sheet is all that necessary.

The company has incredible long-term revenue visibility (via the large backlog).

With multiple years of revenue already baked in, the balance sheet is stronger than it looks (because of reduced apparent need to lean on it any time soon).

Profitability is strong, although recent results (harmed by challenges noted earlier) have weighed on the firm.

Return on equity has averaged 26% over the last five years, while net margin has averaged 6.1%.

In better years, before the pandemic, the company was routinely printing ROE that was well north of 30% and ROIC that was well over 20%.

Huntington Ingalls is still producing high returns on capital, even if the numbers aren’t as impressive as they were a few years ago, and it wouldn’t be some kind of insurmountable challenge to get back to prior excellence.

Overall, while the business isn’t running at 100% right now, it’s still a world-class defense firm with a quasi-monopoly over its domain.

And with high barriers to entry, large economies of scale, technological know-how, R&D, IP, long-term contracts, switching costs, and a unique and entrenched government relationship, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Huntington Ingalls is somewhat insulated from competition due to its domination of shipbuilding within a broader industry that is oligopolistic; however, regulation is intense because of the direct government oversight.

The very business model has geopolitical risk, which can cut both ways.

US debt and overall spending is facing scrutiny, which may pressure US DoD budgets and what can be allocated to the US Navy (and, thus, Huntington Ingalls) in the future.

The company’s overwhelming dependence on the US Navy introduces customer concentration risk, although the US Navy has been a reliable partner/customer for many years.

While the large backlog greatly helps with revenue visibility, Huntington Ingalls faces significant execution risks around its ability to manage the workload and maintain its reputation as a reliable, timely deliverer of high-quality products.

Related to that prior risk, Huntington Ingalls must source and skill labor, which is proving to be difficult and adds risk around its ability to execute.

There are certainly some risks here to seriously mull over.

But the valuation, after the stock’s recent 35% drop, seems to be pricing in an exaggerated amount of risk already…

Valuation

The P/E ratio is now sitting at just 10.7.

We’re at nearly a single-digit earnings multiple, which is kind of crazy.

This is less than half that of the broader market’s earnings multiple.

It’s also well off of the stock’s own five-year average P/E ratio of 13.9 (which itself is not demanding).

And the yield, as noted earlier, is substantially higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 4% dividend growth rate for the next five years, and a long-term dividend growth rate of 7.5%.

I usually reserve a two-stage model for high-growth businesses which are unlikely to sustain such high growth rates for decades on end, and a slowing is usually modeled in after a short-term burst.

This case is the opposite of that, and it’s kind of unique in this sense.

As I already showed, an anticipation for mid-single-digit dividend growth – at best – over the next few years or so is reasonable.

More of the recent same is exactly what I’m modeling in over the next five years.

Moreover, I’ve also reduced my expectations for long-term dividend growth out of Huntington Ingalls compared to previous analyses, as the business is mired in an execution fog that will likely limit dividend growth over an extended period of time.

While I fully expect the business to get back to its prior ways once it passes through this near-term bog, the near-term issues do weigh on the long-term outlook.

Still, I’m not modeling in any kind of unattainable growth here.

These are very achievable numbers, and the business would have to be struggling for many years in order to not clear these hurdles.

The DDM analysis gives me a fair value of $198.30.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I came out with a cheaper fair value than before, and yet the stock still comes out looking cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates HII as a 5-star stock, with a fair value estimate of $326.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates HII as a 3-star “HOLD”, with a 12-month target price of $200.00.

I’m very close to where CFRA is at on this one. Averaging the three numbers out gives us a final valuation of $241.43, which would indicate the stock is possibly 21% undervalued.

Bottom line: Huntington Ingalls Industries Inc. (HII) is a high-quality defense prime that dominates its domain in a monopoly-like fashion, within the favorable confines of an oligopolistic industry. It has some short-term challenges to overcome, but its massive backlog shows no demand slowdown whatsoever. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, 13 consecutive years of dividend increases, and the potential that shares are 21% undervalued, this appears to be the cheapest way to play US defense in a world where geopolitical tensions are showing no signs of abating.

Bottom line: Huntington Ingalls Industries Inc. (HII) is a high-quality defense prime that dominates its domain in a monopoly-like fashion, within the favorable confines of an oligopolistic industry. It has some short-term challenges to overcome, but its massive backlog shows no demand slowdown whatsoever. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, 13 consecutive years of dividend increases, and the potential that shares are 21% undervalued, this appears to be the cheapest way to play US defense in a world where geopolitical tensions are showing no signs of abating.

-Jason Fieber

Note from D&I: How safe is HII’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 68. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, HII’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: Dividends & Income

Disclosure: I’m long HII.