Let’s talk about a “rich guy loophole” that you and I can take advantage of—and bank dividends up to 12.5%.

And no, I’m not going to ask for your most recent tax return or W2. These are perfectly legal “backdoor” divvies trading between $10 and $20 per share. A sweet setup by Congress has these payers yielding between 10.5% and 12.5%.

The secret is the business development company. BDCs provide capital to small and midsized businesses. These firms often invest alongside or after venture capital. They are “kinda sorta” like private equity firms, but available to everybody (as in, we don’t need a half million in liquid assets to invest).

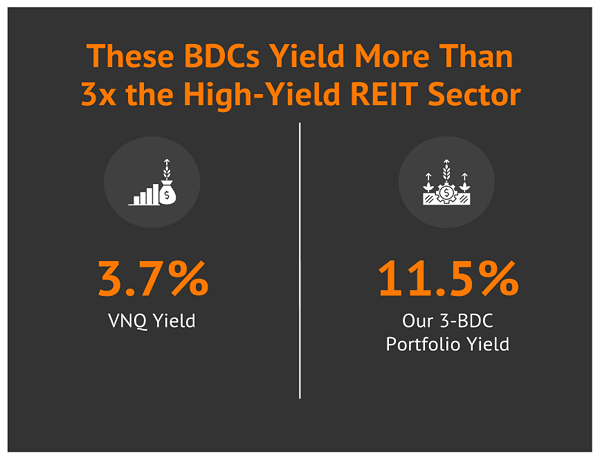

BDCs have structures similar to real estate investment trusts (REITs). Both were created by Congress. Both were designed to spur investment in part of the economy. And both have a mandate to pay out at least 90% of their taxable income in the form of dividends.

You already know REITs offer generous yields. Well, if you like REIT divvies, you will love BDCs:

Of course these double-digit yields aren’t “gimmes.” Big yields often bring big risks. Let’s evaluate each company carefully.

Of course these double-digit yields aren’t “gimmes.” Big yields often bring big risks. Let’s evaluate each company carefully.

SLR Investment (SLRC)

Dividend Yield: 10.5%

SLR Investment (SLRC) is a self-described “yield-oriented” BDC (but, hey, aren’t they all?) that invests predominantly in senior secured loans of private U.S. middle market companies.

That’s a normal-sounding description of just about any BDC. And it is. But SLRC has leaned heavily into specialty niches.

The portfolio is divided into four parts: The traditional “sponsor finance” business, which is cash-flow loans, is only 24% of the portfolio at fair value. Equipment financing (33%) and asset-based loans (31%) are both bigger slices of the pie; the remaining 12% or so comes from life science loans. And SLRC’s assets are spread across a wild 800 unique issuers across 110 industries, resulting in an average exposure of just 0.1% per issuer.

SLRC trades at a 14% discount to NAV. That’s not the lowest price you’ll find in BDC-land, but it’s about as inexpensive as you can find without wandering into a field of red flags. Of course, I looked at SLRC earlier this year when it traded at a slightly higher discount, and I wondered aloud then “whether it’s a bargain—or merely cheap.”

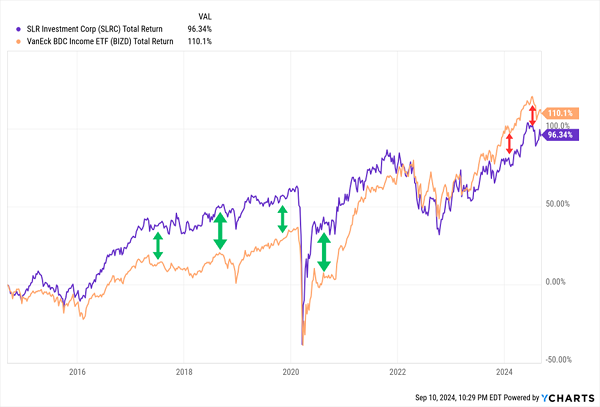

My concerns? SLR Investment is externally managed, which typically means higher management and incentive fees that hold back investor returns. That’s fine when management earns its keep. But SLR is trailing the industry ETF VanEck BDC Income ETF (BIZD), which begs the question, are these external managers bringing any value?

But When It Doesn’t Anymore, Watch Out

On the bright side, a large portion of SLR’s portfolio is fixed-rate in nature, which means these loans will gain in value as rates fall. This “fixed-rate feather” stands in stark contrast to many of its competitors, whose investments are almost completely variable-rate.

On the bright side, a large portion of SLR’s portfolio is fixed-rate in nature, which means these loans will gain in value as rates fall. This “fixed-rate feather” stands in stark contrast to many of its competitors, whose investments are almost completely variable-rate.

From an income perspective, SLRC’s 10.5% yield is—believe it or not—in the bottom third of publicly traded BDCs. However, SLRC is putting even more distance between it and a prior period of under-covered dividends; payout coverage remains tight but increasingly manageable. (Regrettably, though, the company’s brief dalliance with monthly payouts ended last year.)

Nuveen Churchill Direct Lending Corp. (NCDL)

Dividend Yield: 12.5%*

Next up is a fresh-faced BDC that has only been in existence since 2018 and just went public earlier this year.

Nuveen Churchill Direct Lending Corp. (NCDL) is one of a handful of business development companies with some serious name recognition. Much like Goldman Sachs BDC (GSBD) and Carlyle Secured Lending (CGBD), NCDL benefits from its connection to a giant financial name. Two, in fact: Nuveen, as well as its parent TIAA.

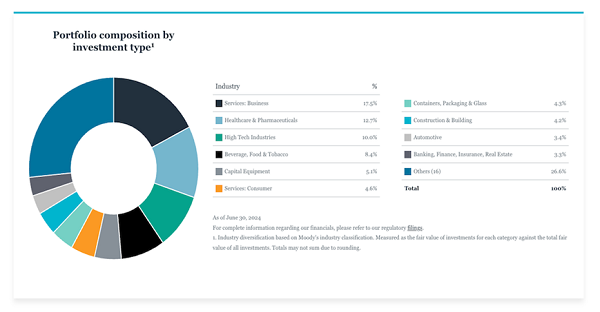

NCDL is a straightforward play on private credit. The fund’s external manager—Churchill, a Nuveen affiliate—invests the BDC in senior secured loans to private equity-owned middle market companies in the U.S. The roughly $2 billion portfolio is 198 companies strong right now. The vast majority of holdings (91%) are first lien loans, though Nuveen Churchill Direct Lending also deals in second lien debt, subordinated loans and equity co-investment.

Source: Nuveen Churchill Direct Lending Corp.

Source: Nuveen Churchill Direct Lending Corp.

We obviously don’t have much price action to study, so instead, here are a few fundamentals and business elements I’m interested in watching as this newish BDC develops a track record:

- NCDL’s involvement with Nuveen and TIAA should provide it with more access to deal flow than some independent BDCs have.

- This is a healthy portfolio at present, with just three companies on non-accrual representing less than a half a percent of total investments at fair value. Its positioning in the debt stack isn’t overly aggressive, either.

- NCDL targets a conservative 1.0x-1.25x in debt leverage, and it sat around 1.04x as of midyear. But CEO Ken Kencel says he expects deal activity to ramp up during the second half of 2024.

- Fees are currently being waived for the first five quarters following the company’s January 2024 IPO. In other words, shareholders are paying zero incentive fees through the second quarter of 2025. That’s a nice benefit in the short term, but we’ll want to see how the eventual introduction of fees will weigh on performance.

- Nuveen Churchill Direct Lending has started publicly traded life with two sets of dividends—quarterly regular and special dividends. The former is set at 45 cents per share, while the latter is cemented at 10 cents per share throughout 2024. That comes out to 10.3% from the regulars, and 12.5% from the specials. So management has established a strong income base with the potential for meaningful sweeteners.

- While NCDL is an extremely new issue with little coverage, the market doesn’t seem to be guessing at its value. Shares currently trade at a mere 3% discount to NAV—a figure we’d ideally like to widen before even jumping in.

Crescent Capital BDC (CCAP)

Dividend Yield: 11.5%*

Crescent Capital BDC (CCAP) is another debt-focused BDC with a penchant for special dividends. However, it was founded in 2015 and has traded since 2020, giving it a little more of a track record. Crescent enjoys the resources of Crescent Capital Group, a global credit investment firm that specializes in below-investment-grade credit strategies.

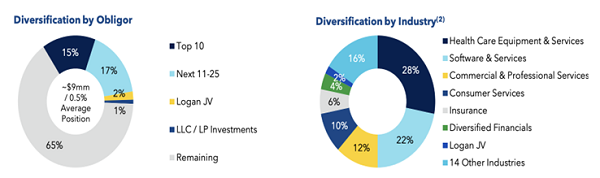

CCAP also invests in private middle market companies, predominantly in the U.S., though it does have roughly 10% international exposure spread across Europe, Canada, Australia, and New Zealand. It favors first lien debt deals (90) with companies in non-cyclical industries (85%), so it’s quite defensive in nature.

Source: Crescent Capital BDC Q2 Earnings Presentation

Source: Crescent Capital BDC Q2 Earnings Presentation

Worth noting: In March 2023, the company closed on its acquisition of First Eagle Alternative Capital (FCRD) at a hefty 66% premium that was split across CCAP shares, cash from Crescent Capital and cash from CCAP’s advisor, Crescent Cap Advisors. That helped further propel a seven-quarter streak of earnings growth.

The Stock Has Done Pretty Well, Too

Admittedly, the deal forced CCAP to halt a run of 5-cent special dividends. Fortunately, not only have specials come back—they’ve gotten bigger. And perhaps even more telling—the company raised its regular dividend, albeit by a penny per share, for the first time in years. (It’s an odd special, too. Crescent Capital announces its special dividends after the fact; for instance, in August, it declared a Q3 base dividend of 42 cents per share, but also a 9-cent-per-share supplemental for the second quarter.) Regardless, CCAP now yields 9.3% on regulars, and 11.5% once specials are factored in.

Admittedly, the deal forced CCAP to halt a run of 5-cent special dividends. Fortunately, not only have specials come back—they’ve gotten bigger. And perhaps even more telling—the company raised its regular dividend, albeit by a penny per share, for the first time in years. (It’s an odd special, too. Crescent Capital announces its special dividends after the fact; for instance, in August, it declared a Q3 base dividend of 42 cents per share, but also a 9-cent-per-share supplemental for the second quarter.) Regardless, CCAP now yields 9.3% on regulars, and 11.5% once specials are factored in.

On top of all that, this BDC trades at an 11% discount to NAV. Though in this case, the market might be pricing in some amount of volatility ahead. Virtually all of CCAP’s debt investments (97%) are floating-rate in nature, which could be problematic once the Fed officially pivots to rate cuts. And that seven-quarter earnings-growth streak? Analysts are modeling an equally long set of quarterly earnings declines over the next two years.

— Brett Owens

An 10.5% dividend… paid monthly? Yes, but you’ll want to move quickly. [sponsor]

One of my top buy-and-hold income plays for this market is the brainchild of one of the smartest investment minds on the planet… It dishes an incredible 10.5% yield… paid like clockwork every single month! And my research suggests that it’s poised for big price gains in the months ahead… no matter which way the broader market swings. I’m so excited about this fund that I’ve made it a core holding in my “Monthly Payer Portfolio” – an easy-to-buy collection of stocks and funds that could hand you $3,300+ in payouts every single month! Don’t delay! Details are ready for you HERE.

Source: Contrarian Outlook