When it comes to money, there are many different things we can do with it.

We can save it, spend it, invest it, give it away, etc.

For obvious reasons, spending it is a very popular choice.

And, I must say, back when I was younger, that was always my go-to option.

But once you start to prioritize the investing choice, your entire life starts to change.

Once money is spent, it’s gone forever.

But when it’s invested, that money can make more money for you… all by itself.

This happens through the magical process of compounding – interest earned on interest, causing exponential growth of money.

One of the most powerful investment strategies to capture the best of compounding is dividend growth investing.

This long-term strategy is all about buying and holding shares in high-quality businesses that pay reliable, rising dividends to shareholders.

You can find many examples of what I’m referring to by looking over the Dividend Champions, Contenders, and Challengers list.

This list has compiled in-depth information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

As you might imagine, it takes a special kind of business to be able to steadily pay out ever-higher cash dividends to shareholders, since it takes ever-more profit to afford such behavior.

It should go without saying, you can’t run some terrible business while also doing all of that.

It should go without saying, you can’t run some terrible business while also doing all of that.

As such, this strategy tends to funnel an investor right into some of the best businesses and investments – thereby capturing the best of compounding.

I started employing this strategy for myself nearly 15 years ago, allowing it to steer me as I’ve gone about building my FIRE Fund.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

I’ve actually been in the extremely fortunate position of being able to live off of dividend income since I quit my day job and retired in my early 30s.

For the ins and outs of how that played out, check out my Early Retirement Blueprint.

Now, as powerful as the dividend growth investing strategy is, there’s more to it than simply selecting the right businesses for long-term investment.

Valuation at the time of investment is also of prime consideration.

Valuation at the time of investment is also of prime consideration.

Price only tells you what you pay, but it’s value that tells you what you actually get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Finding undervalued high-quality dividend growth stocks and then buying them with capital not spent can lead to exponential growth in your wealth and passive income over time, unlike the immediate loss that occurs when simply spending money.

This does, of course, require some basic understanding of how valuation works.

Well, that’s where Lesson 11: Valuation comes in.

Written by fellow contributor Dave Van Knapp, it lays out valuation in easy-to-understand terms and even provides a valuation template that can be applied to almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

McDonald’s Corp. (MCD)

McDonald’s Corp. (MCD)

McDonald’s Corp. (MCD) is an American multinational fast-food restaurant chain.

Founded in 1940, McDonald’s is now a $193 billion (by market cap) QSR monster that employs 100,000 people.

McDonald’s has more than 40,000 restaurants located across over 100 countries.

Approximately 95% of restaurants are franchised, operated by independent local business owners.

The company reports results across three segments: International Operated Markets, 48% of FY 2023 revenue; United States, 41%; and International Developmental Licensed Markets & Corporate, 10%.

This is a brilliant business model.

Actually, it’s multiple brilliant business models… all in one.

Before I begin, nobody reading this article isn’t already familiar with McDonald’s and its famous golden arches.

But I’ll break it down very quickly.

At its core, McDonald’s sells a variety of basic burger, sandwich, and related food products (which are locally relevant, depending on the market) across its 40,000+ restaurants worldwide.

If that’s all there was to McDonald’s, it’s be one of the world’s best and most successful businesses.

But McDonald’s kicks it up two notches, and this is where things get really interesting.

First, there’s the fact that the vast majority (95%) of its restaurants are franchised, creating a steady stream of royalties back to McDonald’s.

Second, McDonald’s owns most of the actual buildings that house its restaurants, allowing it collect rent (in addition to royalties) from its franchisees.

By locking its franchisees into long-term contracts and allowing them to locally run these restaurants, McDonald’s is able to collect extremely reliable and consistent royalties and rents that are based on steady global consumer demand for a variety of food staples.

This is a restaurant, royalty, and real estate business… all in one.

Because of this multi-pronged approach, McDonald’s has numerous growth levers.

Plus, there’s the natural growth in the company’s global restaurant footprint (with each restaurant becoming a royalty and rent machine for McDonald’s).

This is why McDonald’s has been able to build up an incredible track record when it comes to revenue, profit, and dividend growth, as well as why all of this should continue for many years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

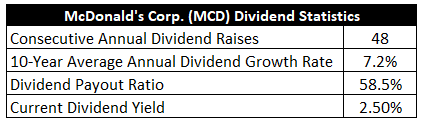

To date, McDonald’s has increased its dividend for 48 consecutive years.

This easily entitles McDonald’s to claim its elite Dividend Aristocrat status, and it’s only two years away from becoming an even rarer Dividend King.

Its 10-year dividend growth rate is 7.2%, which is certainly solid, but there’s been a nice acceleration in dividend growth over the last several years.

For instance, the five-year dividend growth rate is 8.3%, and the most recent dividend raise came in at nearly 10%.

It’s clear that McDonald’s is committed to high-single-digit dividend growth.

Along with that, the stock yields 2.5%.

Along with that, the stock yields 2.5%.

This easily beats what the broader market gives you, and this yield is also 30 basis points higher than its own five-year average.

And with a reasonable payout ratio of 58.5%, the dividend is currently about as healthy as it’s ever been.

Hard to overstate the impressiveness of this company’s dividend growth profile.

Even after nearly 50 straight years of ever-larger dividends, growth has actually been quickening.

It’s really quite incredible.

Revenue and Earnings Growth

As incredible as the profile is, though, many of these metrics are looking in the rearview mirror.

However, investors must always be looking through the windshield, as the capital of today is ultimately risked for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be instrumental when later attempting to estimate the intrinsic value of the business.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this way should give us what we need to roughly gauge where the business may be going from here.

McDonald’s revenue has actually slightly decreased from $27.4 billion in FY 2014 to $25.5 billion in FY 2023.

A negative top-line growth rate is obviously not what we want to see.

However, this is misleading and not indicative of issues with the core business.

The reason for the decline in revenue is due to the company’s decision to extensively refranchise its restaurants between 2015 and 2018.

McDonald’s has gone from ~80% franchised restaurants to ~95% franchised restaurants, temporarily impacting revenue (because stores were no longer owned by the company) in order to create a steadier and more reliable cash flow machine for the long run.

Meanwhile, earnings per share grew from $4.82 to $11.56 over this 10-year period, which is a CAGR of 10.2%.

That’s a more accurate reflection of what’s really happening at McDonald’s, lining up pretty well with recent dividend growth trends.

It also goes to show how successful the company’s overall efforts have been, since driving double-digit bottom-line growth out of a large, mature business like McDonald’s is not easy.

It’s hard to argue with the decision to refranchise stores, which lightened up capital intensity, smoothed out cash flow, and greatly improved margins.

Speaking on that last point, net margin has nearly doubled over the last decade.

In addition, regular buybacks, which reduced the outstanding share count by more than 25% over the last decade, helped to drive excess bottom-line growth.

Looking forward, CFRA forecasts that McDonald’s will compound its EPS at an annual rate of 9% over the next three years.

CFRA states: “…the broader QSR sub-industry has seen weaker customer traffic due to broad-based consumer pressures. We also note that [McDonald’s], which over-indexes with lower income consumers, struggled with the execution of its national value platform in Q2.”

On the other hand, CFRA notes: “Nonetheless, we still expect [McDonald’s] to benefit from some consumer trade-down, along with its ability to leverage its scale.”

I think that last part highlights the crux of the matter.

McDonald’s has unrivaled scale in its space.

No QSR competitor can touch what McDonald’s brings to the marketplace in terms of scale and brand recognition.

And that scale is set to become even more formidable, as the company has plans to open 10,000 new stores globally by 2027 (marking its fastest period of store growth ever).

I’d also argue the value proposition of McDonald’s is one of the strongest out there, if not the strongest.

And because of that value proposition, McDonald’s stands to disproportionately benefit from any kind of trade-down that may occur in an economic weakening.

Indeed, with inflation taking a bite out of the average consumer’s purchasing power, trading down to McDonald’s is easier and more alluring than ever before.

There’s also the ~$9 billion that has been spent on restaurant renovations over the last several years, putting the company ahead of many competitors (who are just now starting similar efforts).

No consumer wants a dingy restaurant environment.

Furthermore, McDonald’s has been aggressively building out its digital capabilities, giving consumers easier and more plentiful ordering choices through in-store kiosks, drive-through menus, and its app (which has a built-in rewards program that builds stickier relationships).

I’m willing to take the 9% number as the base case.

CFRA isn’t assuming anything heroic here.

This is basically guiding for what McDonald’s has done over the last decade, more or less.

If the company can continue to meet that type of bottom-line growth hurdle, that sets up the dividend for a similar track.

Said another way, shareholders should be able to count on more high-single-digit dividend growth from McDonald’s for years to come, just as they’ve been able to count on that for many years already.

When starting off with a 2.5% yield, that paints a nice total return picture (one of 10%+ annualized).

And that’s out of an easy-to-understand business model that has fashioned itself into a rent and royalty castle.

In my view, this is low-hanging fruit.

As Warren Buffett might put it, it’s a one-foot bar to step over.

Financial Position

Moving over to the balance sheet, McDonald’s has a good financial position.

Due to negative common equity, there’s no usable debt/equity ratio.

However, the interest coverage ratio is slightly over 8, which is okay.

The company ended last fiscal year with about $37 billion in long-term debt (against about $4 billion in cash).

That’s not overly concerning for a company with a market cap of nearly $200 billion, but it must be said that this balance sheet is far from spectacular.

Profitability, on the other hand, is pretty spectacular.

Because of the common equity situation, ROE is N/A.

But net margin has averaged 29.3% over the last five years, which is a world-class number.

Circling back around to the margin expansion story I touched on earlier, net margin was bumping along at ~17% a decade ago.

It’s nearly doubled, which just speaks on how powerful the refranchising effort has been and how much that’s lightened up on the company’s capital needs.

Other than the iffy balance sheet, which can be forgiven in light of the reduced capital intensity, McDonald’s is operating a terrific business at a high level.

This is a rent-and-royalty scheme with locked-in franchisees who do most of the heavy lifting, making it one of the most alluring business models I know of.

And with economies of scale, unrivaled brand recognition, pricing power, IP, R&D, and the largest global QSR footprint in the world, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Competition, in particular, is extremely fierce in the QSR industry, but regulation and litigation are relatively muted concerns.

There are no switching costs present for customers.

Barriers to entry in the industry aren’t very high.

The company is highly exposed to the global economy, but the low-cost nature and value proposition of the company’s core products insulate it somewhat from a recession.

A global footprint introduces geopolitical risks and exposure to currency exchange rates.

The company’s large size may open up concerns over the law of large numbers, but the fact that it’s currently embarking upon its fastest period of store growth ever should qualm some of those concerns.

Overall, the risks around a long-term investment in McDonald’s seem very acceptable to me.

And with the stock recently correcting in price, the valuation also strikes me as very acceptable…

Valuation

The P/E ratio is 23.7.

That compares favorably to its own five-year average of 27.7.

The cash flow multiple of 20.7 is also lower than its own five-year average of 22.2.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

This number is just barely higher than the 10-year dividend growth rate, but recent dividend raises have been markedly higher than 7%.

Moreover, the company has compounded EPS at ~10% over the last decade.

The payout ratio remains moderate.

Taking that 9% near-term EPS growth projection as the base case, McDonald’s should easily be able to grow its dividend at a high-single-digit rate over the foreseeable future.

If anything, I’m being conservative here, but I’d rather err on the side of caution.

The DDM analysis gives me a fair value of $287.24.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I see a stock that appears to be modestly undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates MCD as a 4-star stock, with a fair value estimate of $292.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates MCD as a 3-star “HOLD”, with a 12-month target price of $275.00.

Super tight range this time around. Averaging the three numbers out gives us a final valuation of $284.75, which would indicate the stock is possibly 5% undervalued.

Bottom line: McDonald’s Corp. (MCD) has a brilliant business model, leveraging rents and royalties into a reliable cash flow machine. It sells timeless food staples at low costs, heavily insulating it from economic cycles. The scale is unrivaled. And the brand recognition is unlike any other. With a market-beating yield, high-single-digit dividend growth, a reasonable payout ratio, nearly 50 consecutive years of dividend increases, and the potential that shares are 5% undervalued, this Dividend Aristocrat is a high-quality idea for long-term dividend growth investors.

Bottom line: McDonald’s Corp. (MCD) has a brilliant business model, leveraging rents and royalties into a reliable cash flow machine. It sells timeless food staples at low costs, heavily insulating it from economic cycles. The scale is unrivaled. And the brand recognition is unlike any other. With a market-beating yield, high-single-digit dividend growth, a reasonable payout ratio, nearly 50 consecutive years of dividend increases, and the potential that shares are 5% undervalued, this Dividend Aristocrat is a high-quality idea for long-term dividend growth investors.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is MCD’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 77. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, MCD’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long MCD.