Much can be accomplished in any life pursuit with a few simple ingredients.

Take investing, for example.

Simply mixing frugality, compounding, and time can yield tremendous results.

If one can live below their means, consistently invest their spare capital, and take advantage of the power of compounding over a long period of time, they almost can’t help but to become decently wealthy.

And this simple set of ingredients can even be supercharged when the right investment strategy is followed.

In my view, the best strategy of all is dividend growth investing.

This is a long-term investment strategy whereby one buys and holds shares in world-class businesses that pay safe, growing dividends to shareholders.

As you might imagine, it requires steadily rising profit in order to pay out steadily rising cash dividends.

And it takes a special kind of business to manage all of this.

The Dividend Champions, Contenders, and Challengers list – a compilation of US-listed stocks that have raised dividends each year for at least the last five consecutive years – shows you what it takes, as it lists one special, world-class business after another.

As large as this list may initially seem to be, it’s whittled down from thousands of public equities.

As large as this list may initially seem to be, it’s whittled down from thousands of public equities.

So that just goes to show how rare but powerful truly great businesses are.

Because I recognized the importance of investing in great businesses early on in my investing journey, and because I wanted to one day generate enough passive investment income to live off of, I started using this strategy for myself almost 15 years ago.

It guided me as I’ve gone about building the FIRE Fund.

That’s my real-money portfolio, and it now throws off enough five-figure passive dividend income for me to live off of.

The strategy has been so effective, it even put me in a position to retire in my early 30s.

If you’re curious about how that played out, my Early Retirement Blueprint has the details.

As important as it is to invest in great businesses, it’s also important to consider valuation at the time of investment.

Price is simply what you pay, but value is what you actually get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying and holding undervalued high-quality dividend growth stocks might sound too simple to be effective, but a few key ingredients can make all the difference over a lifetime of investing.

Of course, recognizing undervaluation means one already has some kind of familiarity with how to go about valuing a business.

If you don’t yet have this in place, Lesson 11: Valuation, penned by fellow contributor Dave Van Knapp, is worth a read.

It discusses the basic ins and outs of business valuation, and it includes a template that can be used to estimate the fair value of almost any dividend growth stock out there

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Essex Property Trust Inc. (ESS)

Essex Property Trust Inc. (ESS)

Essex Property Trust Inc. (ESS) is a real estate investment trust that owns and operates a portfolio of US West Coast multifamily properties.

Founded in 1971, the company is now an $18 billion (by market cap) real estate giant that employs roughly 1,700 people.

Essex Property Trust focuses on three different supply-constrained markets across the US West Coast: Southern California, 42% of NOI; Northern California, 40%; and Seattle, 18%.

The company’s property portfolio consists of approximately 62,000 apartment homes across more than 250 apartment communities.

Commercial real estate can be super tough.

Lots of debt, plenty of exposure to economic cycles, and even risk of obsolescence across various forms of commercial real estate (such as office buildings).

This is why, even though I have a deep endearment for dividends, I’m not a huge fan of most REITs (in spite of the outsized yields that many REITs offer).

However, REITs that focus on housing, such as Essex Property Trust, earn my trust (and, sometimes, my capital).

Shelter is a non-discretionary need in life.

Essentially, we cannot live without it.

As such, shelter has a built-in demand that many other forms of CRE lack, and the runway for that demand extends out for as far as humans will need somewhere to live (i.e., forever).

Shelter also has no risk of obsolescence.

Our world is constantly changing, and technology is accelerating change, but it’s hard to imagine technology or anything else fundamentally changing shelter.

This is why I believe multifamily housing is a more “investable” form of CRE for the long term in comparison to many other types.

There’s just much more long-term visibility here.

One thing that makes Essex Property Trust unique, relative to every other publicly-traded multifamily housing REIT, is this company’s property portfolio footprint.

Essex Property Trust has concentrated its footprint exclusively along the US West Coast.

This creates the most unique supply-demand setup in the space.

A combination of unique geography and heavy-handed regulation across West Coast jurisdictions conspire to limit supply.

The West Coast is filled with natural areas that are prohibitive to building much of anything, limiting the supply of usable land for construction and acting as a natural barrier to entry.

Regulatory red tape only adds to supply woes.

It should go without saying that existing supply is that much more valuable when it’s so difficult to bring new supply to market.

By the way, these same supply issues plague single-family houses in these markets, making apartments more affordable by comparison.

On the demand side, the West Coast is highly desirable: It has a captivating combination of high-paying jobs, temperate climates, and beautiful nature.

It’s no surprise that California is the most populous state in the US (by far).

If California were its own country, it’d have the fifth-highest GDP in the world.

So it’s both enduring demand and limited supply which is working in Essex Property Trust’s favor.

The company almost can’t lose over the long run, and that’s why its revenue, profit, and dividend should continue to grow for many years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

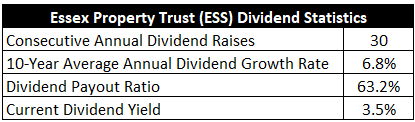

Already, Essex Property Trust has increased its dividend for 30 consecutive years.

That easily qualifies the company for its vaunted status as a Dividend Aristocrat – one of only three REITs that can claim such a thing.

In addition, just to show how relentless and consistent Essex Property Trust has been, this 30-year track record dates all the way back to the REIT’s initial IPO.

So this company has been reliably paying a growing dividend right out of the gate.

The 10-year dividend growth rate of 6.8% is actually quite strong for a REIT (most REITs are slow-growth income vehicles).

On the other hand, the stock’s 3.5% yield is on the low side for a REIT.

On the other hand, the stock’s 3.5% yield is on the low side for a REIT.

In my view, the higher growth rate more than makes up for the relatively lowish yield, but income-oriented investors who crave yield, even at the cost of total return, may find other, higher-yielding REITs more interesting.

That said, it’s worth pointing out that this yield easily beats the market and is 30 basis points higher than its own five-year average.

Plus, the payout ratio is only 63.2%, based on midpoint guidance for this year’s Core FFO/share.

That’s one of the lowest payout ratios I know of in this space, indicating a much safer dividend than what you’d find with most other REITs.

If you’re okay with sacrificing a bit of yield, Essex Property Trust has one of the very best dividend profiles in all of REITdom.

Revenue and Earnings Growth

As much as that may be true, though, many of the dividend metrics are backward looking.

However, investors must always be looking forward, as today’s capital gets risked for tomorrow’s rewards.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will come in handy when the time comes later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past against a future forecast in this manner should give us enough information to form an idea on where the business could be going from here.

Essex Property Trust moved its revenue from $971 million in FY 2014 to $1.7 billion in FY 2023.

That’s a compound annual growth rate of 6.4%.

Very solid top-line growth here, but it’s not super insightful.

When it comes to REITs, it’s imperative to look at profit growth on a per-share basis.

That’s because REITs use debt and equity to fund growth, as they’re legally required to distribute at least 90% of their taxable earnings to shareholders.

This circles back around to the point I made on REITs being income plays, and the limitations around internal funding for growth means tapping equity (by issuing shares) results in dilution.

That tends to create distortion between absolute revenue growth and profit growth relative to shares outstanding.

Also, when assessing profit for a REIT, we want to use funds from operations instead of normal earnings.

FFO (or adjusted FFO) is a measure of cash generated by a REIT, which adds depreciation and amortization expenses back to earnings.

Essex Property Trust grew its FFO/share from $7.89 to $15.24 over this period, which is a CAGR of 7.6%.

Similar to top-line growth, actually.

This is a pretty accurate reflection of Essex Property Trust’s growth rate.

It lines up pretty well with the rate of dividend growth over the last decade, too, indicating prudent stewardship on the part of management.

It’s certainly no growth monster, but this is very respectable for a REIT.

Looking forward, CFRA currently has no three-year FFO/share CAGR projection.

Unfortunate, as I do like to compare the proven past to a future forecast, but CFRA commonly omits this from their REIT research.

If we zoom in on the company’s most recent quarterly report, Core FFO/share increased by 4.5% YOY.

And that’s in a somewhat challenging near-term environment, seeing as how rents spiked during the pandemic, California instituted some eviction restrictions, and then rents recently moderated.

Occupancy is currently hovering around 96%, showing resilient demand for properties and the sturdiness of the basic thesis around enduring need for shelter.

I’d also note that median household income across its entire portfolio is $124,000 – well in excess of the US.

So these are well-to-do renters apparently quite content to pay a premium to live where those higher wages are accessible.

Also, the company has numerous growth drivers, including development (i.e., new supply), redevelopment (i.e., improving currently properties and thereby powering higher rents), and acquisitions, and natural rent growth.

It’s not hard to slowly but consistently move the needle.

Overall, I’m prone to give Essex Property Trust the benefit of the doubt and assign a future growth rate that looks a lot like the past.

Keep in mind, this has been one of the market’s best REITs for decades.

Since its 1994 IPO, the stock has delivered a total return of 4,719% – far outpacing its peer average and the S&P 500 as a whole.

Because of distinct advantages around both supply and demand, this Dividend Aristocrat almost can’t help but to do well.

It’s hard to imagine how the REIT doesn’t continue to grow at the kind of high-single-digit rate management and shareholders are accustomed to.

That lines up the dividend for similar growth (somewhere in that 6%-7% area).

And you’re getting a 3.5% yield to start off with.

Essex Property Trust has torched most REITs for years, and these numbers indicate it has what it takes to continue blowing away the competition.

For dividend growth investors who don’t mind a touch less yield today, it’s hard to dislike the long-term total return story.

Financial Position

Moving over to the balance sheet, Essex Property Trust has a good financial position.

The REIT had just over $6 billion in long-term debt as of the end of last fiscal year, which isn’t overly concerning relative to the market cap of $18 billion.

A common measure for a REIT’s financial position is the debt/EBITDA ratio.

Essex Property Trust’s net debt/EBITDA ratio is 5.4.

I usually see REITs range from 3 to 7 on this ratio, so Essex Property Trust is basically right in the middle of that range.

The company’s weighted average interest rate on its total debt is 3.5%, and there are no major maturities over the next five years.

In addition, the REIT has investment-grade credit ratings for its senior unsecured debt: BBB+, S&P; Baa1, Moody’s.

It’s not the best balance sheet out there, but it’s one of the better ones among the REITs that I follow.

This has been an excellent investment for three decades.

I think the next three decades could be more of the same.

And with economies of scale, luxury properties, regulatory know-how in difficult markets, and an entrenched footprint in supply-constrained and desirable locations, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

California’s infamous red tape is a double-edged sword – constraints on bringing new inventory to market assist existing properties, but it’s also difficult to grow the portfolio.

Real estate is cyclical, although the basic need of shelter does mitigate some of that cyclicality.

Essex Property Trust has indirect exposure to the technology industry, as a lot of tech companies (and the jobs they offer to workers/renters) are based on the West Coast.

The capital structure of a REIT relies on external funding for growth, and rising interest rates can create harm in two ways: Debt becomes more expensive when rates are higher, and competitive yields elsewhere reduces demand for equity.

Essex Property Trust lacks geographic diversification.

The West Coast exposure introduces risks of natural disasters, such as earthquakes.

As work becomes more flexible, more remote workers could choose to leave the West Coast for cheaper locations inland.

A homelessness crisis, rising crime along the I-5 corridor, and an extremely high local cost of living combine to mitigate demand for West Coast living.

There are certainly some risks to seriously consider here.

But the enduring demand for this company’s core offering needs to also be considered, as well as the valuation of the stock at this time…

Valuation

The stock is trading hands for a forward P/FFO ratio of 17.9.

That’s based on midpoint guidance for this year’s Core FFO/share.

This is somewhat analogous to a P/E ratio on a regular stock, so you can see how undemanding the multiple is.

The P/CF ratio of 17.4, the other common way to look at a REIT’s valuation, is also clearly reasonable, and it’s decently lower than its own five-year average of 18.6.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 6.5%.

In my view, this 6.5% number is the correct one to use.

It’s almost right on the nose with the 10-year dividend growth rate, and it only slightly trails the 10-year FFO/share CAGR.

Furthermore, it’s very close to the most recent dividend raise of 6.1%.

From all I can see, Essex Property Trust is consistently growing the business and dividend at somewhere between 6% and 7%.

I’m splitting the difference here.

This has been one of the market’s best and most reliable REITs for decades, and I have no reason to start doubting it now.

The DDM analysis gives me a fair value of $298.20.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I see some modest undervaluation here, which jibes with the small disconnect between current and historical multiples.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates ESS as a 3-star stock, with a fair value estimate of $306.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates ESS as a 3-star “HOLD”, with a 12 month target price of $305.00.

I came out a touch low, but we’re all in a very tight range. Averaging the three numbers out gives us a final valuation of $303.06, which would indicate the stock is possibly 8% undervalued.

Bottom line: Essex Property Trust Inc. (ESS) is a high-quality REIT with a core product that features enduring demand. And a footprint favorably spread out across supply-constrained markets means it almost can’t lose over the long run. With a market-beating yield, inflation-beating dividend growth, a reasonable payout ratio, 30 consecutive years of dividend increases, and the potential that shares are 8% undervalued, this Dividend Aristocrat may just be one of the very best REIT choices for long-term dividend growth investors.

Bottom line: Essex Property Trust Inc. (ESS) is a high-quality REIT with a core product that features enduring demand. And a footprint favorably spread out across supply-constrained markets means it almost can’t lose over the long run. With a market-beating yield, inflation-beating dividend growth, a reasonable payout ratio, 30 consecutive years of dividend increases, and the potential that shares are 8% undervalued, this Dividend Aristocrat may just be one of the very best REIT choices for long-term dividend growth investors.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is ESS’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 93. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, ESS’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long ESS.