I’ve been investing for nearly 15 years now.

A lot of investors, companies, and strategies have come and gone over the years.

But you know what’s fairly consistent?

But you know what’s fairly consistent?

Great businesses.

Yes, great businesses tend to continue being great.

Winners tend to keep winning.

This is why I’m such an ardent fan of dividend growth investing.

This is a long-term investment strategy whereby one buys and holds shares in high-quality businesses that pay reliable, rising dividends to shareholders.

You can find many examples of these by perusing the Dividend Champions, Contenders, and Challengers list – a compilation of hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

As you can see, this strategy creates a gravitational pull toward great businesses.

After all, it takes a special kind of business to be able to pay reliable, rising dividends, because it takes reliable, rising profit to afford that.

And reliable, rising profit usually emanates from great businesses.

I’ve been using this strategy almost since the very beginning.

It’s changed my life, helping me to build the FIRE Fund – my real-money portfolio which generates enough five-figure passive dividend income for me to live off of.

It even allowed me to retire in my early 30s.

My Early Retirement Blueprint details exactly how I was able to do that.

Now, as great as dividend growth investing is, there’s more to it than simply selecting great businesses to invest in.

Valuation is also a critical component.

Valuation is also a critical component.

Whereas price is what you pay, value is what you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Investing in great businesses at attractive valuations via the dividend growth investing strategy is nearly a foolproof way to build substantial wealth and passive income over time.

That all said, this assumes one already comprehends the basic ins and outs of valuation.

If you don’t already have that comprehension in place, I’d definitely recommend to check out Lesson 11: Valuation.

Penned by fellow contributor Dave Van Knapp, it lays out valuation in very simple terms and makes estimating the fair value of almost any dividend growth stock out there pretty straightforward.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Comcast Corp. (CMCSA)

Comcast Corp. (CMCSA)

Comcast Corp. (CMCSA) is a media and entertainment conglomerate with interests in cable, broadcasting, film, streaming, live entertainment, and theme parks.

Founded in 1963, Comcast is now a $150 billion (by market cap) media might that employs over 180,000 people.

Comcast classifies itself as operating two primary businesses: Connectivity & Platforms and Content & Experiences.

Connectivity & Platforms is reported across the following two segments: Residential Connectivity, 57% of FY 2023 revenue; and Business Services Connectivity, 7%.

Content & Experiences is reported across the following three segments: Media, 20%; Studios, 9%; and Theme Parks, 7%.

Connectivity & Platforms is largely comprised of Comcast’s broadband and video distribution assets, including more than 30 million high-speed broadband subscribers and more than 14 million video subscribers.

The other half of the business, which is Content & Experiences, is largely comprised of NBCUniversal broadcast TV and film studio assets, Peacock streaming, cable television networks (including Sky), and global Universal theme parks.

In addition, through Comcast Spectacor, Comcast owns the NHL’s Philadelphia Flyers, as well as the Wells Fargo Center arena in Philadelphia, Pennsylvania.

While the uninformed might think of Comcast as a dying cable company, the truth is, as you can clearly see, Comcast is actually a diversified media and entertainment empire with exciting assets that extend far beyond cable television.

Yes, cable television is suffering from “cord cutting” and is in secular decline.

Despite this, and because of the other assets across the sprawling empire, Comcast continues to prosper.

Actually, outside of video connections, almost every other business under the Comcast umbrella is growing.

For instance, thanks to the ever-growing thirst for data consumption, high-speed internet connections are in secular growth mode.

A good example of this can be found in the company’s most recent quarter – Q1 FY 2024 – which showed a 12.3% YOY decline in total domestic video customers and yet flat YOY revenue across Connectivity & Platforms revenue (thanks to rising prices and strong broadband demand).

Moreover, Comcast has heavily invested in Peacock, its streaming television offering, to counter the secular decline in cable video connections.

In the same Q1 quarter, Peacock’s paid subscribers grew 55% YOY, resulting in 54% YOY revenue growth from Peacock alone.

With broadband, theme parks, streaming, sports, one of the US’s largest movie studios (Universal), and broadcast TV, Comcast has the kind of diversified media and entertainment company that can not just survive but thrive in the face of cable TV’s demise.

And that bodes well for Comcast’s ability to continue growing its revenue, profit, and dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

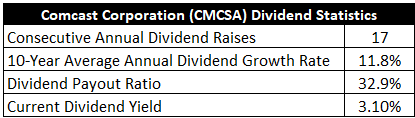

To date, Comcast has increased its dividend for 17 consecutive years.

I’ll note that “cord cutting” has been occurring during this entire time frame, and yet Comcast has been growing its dividend straight through anyway.

If that doesn’t speak volumes, I’m not sure what will.

If that doesn’t speak volumes, I’m not sure what will.

Also, Comcast hasn’t been just growing its dividend but aggressively so.

The 10-year dividend growth rate is 11.8%, which is incredibly strong, although more recent dividend raises have been in a high-single-digit range (7% or so).

Still, high-single-digit dividend growth is more than enough to get the job done when you see the stock yields 3.1%.

A 3%+ yield and 7%+ dividend growth can pretty easily get you to a 10%+ annualized total return, assuming a static valuation (but there could be multiple expansion upside here, too, which is why I’m covering it today).

By the way, this yield is 90 basis points higher than its own five-year average.

The yield is unusually high for this stock, which is where part of the opportunity could be.

Seeing as how the payout ratio is only 32.9%, Comcast has plenty of headroom here for future dividend raises.

If this were any other business model (one without Comcast’s stigma), these dividend metrics would jump off the page.

Really great numbers right across the board.

Revenue and Earnings Growth

As great as these numbers are, though, many of them are based on what’s happened in the past.

However, investors must always be looking toward the future, as today’s capital gets risked for tomorrow’s rewards.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will come into use when the time comest later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should give us the information necessary to make an educated call on where the business could be going from here.

Comcast grew its revenue from $68.8 billion in FY 2014 to $121.6 billion in FY 2023.

That’s a compound annual growth rate of 6.5%.

For the size of Comcast, that’s pretty impressive.

However, it wasn’t all organic, as Comcast did make some strategic acquisitions over this period.

The $39 billion deal for Sky in 2018 is a prime example.

That said, the needle has been steadily moving both before and after 2018.

Meantime, earnings per share increased from $1.60 to $3.71 over this 10-year stretch, which is a CAGR of 9.8%.

Strong.

Again, if you close your eyes and imagine this is any other business, you’d have a hard time not liking what you’re seeing.

Excess bottom-line growth was driven by prolific share buybacks, with the outstanding share count down by approximately 21% over the last decade.

Looking forward, CFRA is calling for an 8% CAGR in Comcast’s EPS over the next three years.

That’s not terribly far off from what transpired above, and I think that’d be a very respectable outcome for Comcast and its shareholders.

CFRA sees “…a firming recovery path for TV/film content, and theme parks businesses— benefiting from pent-up demand.”

CFRA then highlights a very important point: “Meanwhile, with the cable broadband business recently riding some demand tailwinds, the company has increasingly pivoted to a broadband-led connectivity strategy and gained significant traction in its nascent wireless offering.”

These two points are at the crux of the matter: Comcast has long been adapting to the secular decline in cable TV by pivoting toward a broadband-led connectivity strategy which is bolstered by a diversified set of global entertainment assets.

It’s difficult to imagine Comcast managing through the situation much better than it has been, given the business model and some of the challenges around legacy cable TV.

Speaking on this, it’s worth noting this is a family-run business.

Brian Roberts (part of the founding Roberts family) runs Comcast as CEO and owns all of the company’s B shares (giving Roberts about 1/3 of all voting control).

It’s rare to see so much “skin in the game” in a US company (I usually see this much more often in foreign companies).

Brian Roberts has done an admirable job, and it’s great to see so much alignment between management and shareholders.

I’m willing to take this 8% number as the base case on a go-forward basis.

This would also be enough to drive like (or better) dividend growth, keeping that high-single-digit dividend growth train chugging along nicely.

Financial Position

Moving over to the balance sheet, Comcast has a somewhat weak financial position.

The long-term debt/equity ratio is 1.1, while the interest coverage ratio is 6.

I start to get concerned when I see an interest coverage ratio below 5, and we’re close to that level now.

Comcast ended last fiscal year with about $95 billion in long-term debt, which is an eye-popping number – even for a company of this size.

That kind of debt makes me squeamish, although I’d note that Comcast has been slowly deleveraging in recent years.

After topping out at ~$105 billion in FY 2020, long-term debt has been coming down since then.

I view the balance sheet as easily the least desirable aspect of Comcast.

Profitability, on the other hand, is quite decent.

Return on equity has averaged 13.7% over the last five years, while net margin has averaged 10.2%.

ROE has been juiced by the balance sheet, but ROIC is typically coming in at over 10%.

Certainly not the highest returns on capital out there, but I see nothing to be terribly disappointed by.

Overall, Comcast’s management has done a great job of pivoting away from cable TV and using the cash flow from that dying cash cow to lean into better businesses.

And with economies of scale, high barriers to entry, and the ability to operate as a local monopoly in many markets, the business does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

While the broader media industry is fiercely competitive, Comcast benefits from often being the only major cable player in any given market.

Streaming TV is an existential threat to the cable bundle, but Comcast counters this with Peacock and broadband (because one cannot stream television without internet access).

Cable television usage is in secular decline, and this disproportionately harms the company: It hurts both the distribution (i.e., cable video) side of the business and production (i.e., networks) side.

Comcast faces technological obsolescence risk, with competitors constantly trying to bring better, cheaper, and/or faster internet access options to market (e.g., 5G wireless, LEO satellites).

The high debt load limits the company’s future flexibility in terms of M&A and network buildouts.

Comcast also has a poor reputation for customer service.

There are some serious risks to consider, but a lot of risk appears to be priced in already.

I say that because of how cheap the stock looks right now…

Valuation

The P/E ratio is only 10.8.

That’s less than half that of the broader market’s earnings multiple.

It’s also well below the stock’s own five-year average P/E ratio of 16.9.

The sales multiple of 1.4 is also lower than its own five-year average of 1.7.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

I’m very comfortable with this kind of expectation from Comcast.

You can see a thread of high-single-digit dividend growth running throughout today’s writeup, and I’m sticking with it here.

If you look at the last few years, Comcast has been reliably growing its dividend at a similar rate.

And the near-term forecast for EPS growth is barely higher than this, giving some margin of safety and flexibility around the dividend growth.

I actually think Comcast could surprise to the upside on this, but I’d rather err on the side of caution.

The DDM analysis gives me a fair value of $44.23.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I believe there’s modest undervaluation present, if not more than modest.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates CMCSA as a 5-star stock, with a fair value estimate of $56.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates CMCSA as a 4-star “BUY”, with a 12-month target price of $50.00.

I came out surprisingly low this time around. Averaging the three numbers out gives us a final valuation of $50.08, which would indicate the stock is possibly 19% undervalued.

Bottom line: Comcast Corp. (CMCSA) controls an enviable media empire that is slowly but surely moving away from its legacy cable TV business with every passing quarter. After executing several large moves, Comcast is becoming more reliant on exciting businesses across growing areas of entertainment, including broadband and theme parks. With a market-beating yield, double-digit dividend growth, a low payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 19% undervalued, bargain-hunting dividend growth investors looking for a dirt-cheap idea should be keeping this one in mind.

Bottom line: Comcast Corp. (CMCSA) controls an enviable media empire that is slowly but surely moving away from its legacy cable TV business with every passing quarter. After executing several large moves, Comcast is becoming more reliant on exciting businesses across growing areas of entertainment, including broadband and theme parks. With a market-beating yield, double-digit dividend growth, a low payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 19% undervalued, bargain-hunting dividend growth investors looking for a dirt-cheap idea should be keeping this one in mind.

-Jason Fieber

Note from D&I: How safe is CMCSA’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 89. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, CMCSA’s dividend appears Very Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: Dividends & Income

Disclosure: I have no position in CMCSA.