Inflation marches on, national debt is rising, and costs continue to go up.

Is life getting more difficult?

Maybe.

But there’s one way – a way that’s totally in your control – to mitigate these issues and make life easier.

I’m talking about investing.

Investing lets your money work for you, so you don’t always have to.

Investing taps into the exponential power of compounding.

Investing taps into the exponential power of compounding.

When you start to grow your wealth and passive income, life becomes a lot easier.

Now, there are a lot of different investment strategies out there.

But I think dividend growth investing is the best.

This is a long-term investment strategy that’s all about buying and holding shares in great businesses paying shareholders safe, growing dividends.

You can find hundreds of examples by perusing the Dividend Champions, Contenders, and Challengers list.

That list contains invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

This strategy has aided and guided me as I’ve gone about building my own wealth and passive income via the FIRE Fund – my real-money portfolio which generates enough five-figure passive dividend income for me to live off.

Dividend income has covered my bills for a number of years.

Dividend income has covered my bills for a number of years.

I was even able to live without a job after I retired in my early 30s.

By the way, my Early Retirement Blueprint explains how I was able to quit my job and retire at such a young age.

Using the right strategy to make the right investments can go a long way.

However, investing at the right valuations is also key.

Whereas price tells you what you pay, it’s value that tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying high-quality dividend growth stocks at attractive valuations can help you to fight off many of life’s ills, such as inflation and economic uncertainty, and this repeated behavior can even eventually unlock financial freedom.

That said, knowing when a stock is undervalued requires some basic knowledge.

This is where Lesson 11: Valuation comes in.

Put together by fellow contributor Dave Van Knapp, it lays out the whole valuation concept in simple-to-understand terms and even offers an easy-to-use valuation template.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Mondelez International Inc. (MDLZ)

Mondelez International Inc. (MDLZ)

Mondelez International Inc. (MDLZ) is an American multinational confectionery, snack food, and beverage company.

Founded in 2012, but with certain roots dating back to 1923, Mondelez is now an $88 billion (by market cap) confectionary and snack giant that employs approximately 90,000 people.

The company reports results across four geographic segments: Europe, 35% of FY 2023 revenue; America, 31%; Asia, Middle East & Africa, 20%; and Latin America, 14%.

Developed markets account for 61% of sales, while the remainder comes from developing markets.

FY 2023 revenue can also be broken down by product category: Biscuits and Baked Snacks, 49%; Chocolate, 30%; Gum and Candy, 12%; Beverages, 3%; and Cheese and Grocery, 6%.

Mondelez runs a powerful but simple business model based on providing consumers all over the world with enjoyable snacks via high-quality branded products.

Some of these branded products include: Cadbury, Oreo, and Ritz (all of which are brands doing more than $1 billion in sales per year.

People love snacking.

Per the 2023 State of Snacking report, 88% of consumers snack daily, and 76% report longtime loyalty to specific brands.

Well, that consistent, repeated consumer behavior, along with product loyalty, bodes well for Mondelez and its bevy of market-leading brands: Mondelez holds the #1 global position in biscuit, and #2 global position in chocolate.

This is why Mondelez continues to report higher revenue and profit, year after year, and it’s why this should continue to occur indefinitely.

And that leads to the growing dividends that shareholders have come to enjoy and expect.

Dividend Growth, Growth Rate, Payout Ratio and Yield

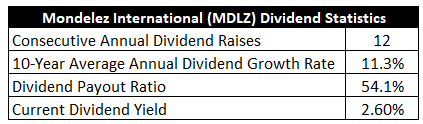

Indeed, Mondelez has increased its dividend for 12 consecutive years.

This is as long as the track record could possibly be, dating back to the 2012 spin-off of Mondelez from its former parent company Kraft Foods Inc.

So Mondelez has been a dividend grower right out of the gate (although it was technically already a very old and mature business in 2012).

The 10-year dividend growth rate of 11.3% is very solid.

The 10-year dividend growth rate of 11.3% is very solid.

Moreover, Mondelez has been very consistent with the dividend growth, handing out 10%+ dividend raises, year in and year out, like clockwork.

And you get to pair that HSD-LDD dividend growth with the stock’s 2.6% starting yield.

Worth noting is the fact that this market-beating yield is 50 basis points higher than its own five-year average.

And this is a healthy dividend, as the payout ratio is only 54.1%.

This moderate payout ratio strikes a nice balance between retaining earnings for growth and rewarding shareholders with cash.

Mondelez has a fantastic dividend profile.

You get plenty of growth on top of the appealing yield, and there are no questions around the sustainability of it.

Something to like for just about every investor.

Revenue and Earnings Growth

As fantastic as these numbers are, though, some of them are backward looking.

However, investors must always be looking forward, as today’s capital is risked for tomorrow’s rewards.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast like this should give us what we need to make an informed judgment call on where the business could be going from here.

Mondelez raised its revenue from $34.2 billion in FY 2014 to $36 billion in FY 2023.

That’s a compound annual growth rate of 0.6%.

Rather poor top-line growth, so what gives?

Well, it’s misleading.

Mondelez has shifted its portfolio quite a bit over this period in order to better concentrate the company’s portfolio around faster-growing, more profitable snack foods.

This included divestitures, including the recent sale of its developed market gum business to Perfetti Van Melle Group for $1.4 billion.

At the same time, Mondelez has made a number of strategic acquisitions, including the purchase of Clif Bar & Company in 2022 for approximately $2.9 billion.

Revenue dropped materially after FY 2014, and stayed there for a time, but it has since increased by 39.2% since FY 2019 alone.

Meanwhile, earnings per share grew from $1.28 to $3.62 over this 10-year period, which is a CAGR of 12.2%.

See, that’s more like it.

Net margin has basically doubled since FY 2014, so the portfolio moves have turned out well.

In addition, the company has been a buyback machine; the outstanding share count has been reduced by nearly 20% over the last decade.

I think it’s fair to say that Mondelez’s management has done a great job with its portfolio, driving more growth and better profitability with in-demand products.

We can also see how that low-double-digit dividend growth has been fueled by similar EPS growth, further proving just how sustainable the dividend growth has been.

Looking forward, CFRA sees Mondelez compounding its EPS at an annual rate of 9% over the next three years.

While that would represent a modest slowdown in growth relative to what’s transpired over the last decade, it would still be a very respectable bottom-line growth rate that could allow for similar dividend growth (thanks to the balanced payout ratio).

CFRA calls out the big challenges around higher input costs (especially in regard to cocoa), which has forced Mondelez to pass on higher prices and, possibly, sacrifice some volume.

On the other hand, CFRA notes Mondelez’s exposure to fast-growing products and emerging geographic markets.

When both your products and markets are growing quickly, that’s a powerful one-two punch.

I think CFRA’s number is a good base case to work with.

And I imagine most shareholders would find it hard to be disappointed with ~9% EPS and dividend growth over the coming years, particularly when starting out with a pretty decent yield.

Assuming no major changes to valuation, that sets the stock up for a 11%+ annualized total return profile.

It’s not explosive AI growth or anything, but that’s not bad at all.

Financial Position

Moving over to the balance sheet, Mondelez has a solid financial position.

The long-term debt/equity ratio is 0.6, while the interest coverage ratio is over 13.

These are pretty good numbers.

I see no major issues with the company’s leverage.

The company’s profitability is satisfactory, and it’s been generally improving (although there’s room for even more improvement).

Return on equity has averaged 14.4% over the last five years, while net margin has averaged 13.3%.

As I pointed out earlier, net margin was about half of this level back in FY 2014.

I’d like to see Mondelez put up higher returns on capital, but this is all quite adequate.

Overall, Mondelez is one of the very best snack food businesses in the world.

And with economies of scale, a global distribution network, brand recognition, and pricing power, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Competition, in particular is a key risk, as this space is notoriously competitive.

Input costs, such as raw materials, are volatile and have recently been a lot higher.

Being a global enterprise, Mondelez has exposure to geopolitics and currency exchange rates.

There’s some exposure to macroeconomics, and a recession could cause consumers to pull back on discretionary snack food purchases.

The rise of GLP-1 drugs are a new risk and pose a threat to demand for snack foods.

While every business has risks, these risks strike me as very reasonable and not nearly as high as what you’d find among other business models out there.

And with the valuation being as reasonable as it is, the risks that are present seem quite acceptable to me…

Valuation

The stock is trading hands for a P/E ratio of 21.

That’s lower than its own five-year average of 22.5, and it’s also lower than the broader market’s earnings multiple.

The P/CF ratio of 16.5 is also below its own five-year average of 19.4.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

I think that’s a pretty fair expectation for long-term dividend growth when looking at Mondelez’s capabilities over time.

This mark is lower than the demonstrated 10-year dividend growth rate, which itself is lower than the 10-year EPS CAGR.

However, there’s been a lot of portfolio shuffling, cost inflation is biting, and the near-term forecast for EPS growth isn’t as high as it’s been in the past.

Mondelez could certainly surprise to the upside.

But it’s hard to see a scenario in which it materially disappoints.

Either way, it’s prudent to err on the side of caution.

The DDM analysis gives me a fair value of $73.96.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Nothing overly aggressive about this valuation model, yet there’s still attractiveness here.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates MDLZ as a 4-star stock, with a fair value estimate of $75.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates MDLZ as a 3-star “HOLD”, with a 12-month target price of $72.00.

I came out somewhere in the middle, but there’s a tight consensus. Averaging the three numbers out gives us a final valuation of $73.65, which would indicate the stock is possibly 10% undervalued.

Bottom line: Mondelez International Inc. (MDLZ) is a high-quality snack food business with multiple billion-dollar brands beloved by consumers all over the world. After years of portfolio shuffling, the company has a fantastic roster of thriving products. With a market-beating yield, double-digit dividend growth, a balanced payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 10% undervalued, this is an easy idea for long-term dividend growth investors.

Bottom line: Mondelez International Inc. (MDLZ) is a high-quality snack food business with multiple billion-dollar brands beloved by consumers all over the world. After years of portfolio shuffling, the company has a fantastic roster of thriving products. With a market-beating yield, double-digit dividend growth, a balanced payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 10% undervalued, this is an easy idea for long-term dividend growth investors.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is MDLZ’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 66. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, MDLZ’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long MDLZ.