We have so many choices when it comes to what to do with our money.

A lot of people give these choices very little thought and spend with reckless abandon.

While we all require our necessities, plenty of spending is discretionary.

But what if we just direct a small portion of our money toward investing?

Well, the results can be dramatic.

Investing just $500 per month (not a herculean feat) for 30 years and compounding that money at a 10% annualized rate results in more than $1 million at the end.

It’s not that hard to become a millionaire.

It’s not that hard to become a millionaire.

And the crazy thing is, you could do a lot better.

You could save more, or you could get an annualized return that exceeds 10%.

That latter part is where really intelligent investing comes in.

And I’d argue that one approach toward that end is the dividend growth investing strategy.

This is a long-term investment strategy whereby one buys and holds shares in high-quality businesses that pay safe, growing dividends to shareholders.

You can find hundreds of examples by taking a look at the Dividend Champions, Contenders, and Challengers list – a compilation of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

This strategy can yield terrific results over the long run, because one is tending toward terrific businesses by the very nature of sticking to those businesses that can produce the ever-larger profit necessary to fund ever-larger dividends.

I’ve personally used this strategy for more than a decade now, allowing it to guide me as I’ve gone about assembling the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

In fact, I’ve been able to live off of dividend income ever since I quit my day job and retired in my early 30s.

By the way, my Early Retirement Blueprint explains how I was able to do that.

By the way, my Early Retirement Blueprint explains how I was able to do that.

Now, as powerful as this strategy can be, it’s about more than just investing in terrific businesses.

Investing at the right valuations is also very important.

That’s because price is only what you pay, but it’s value that you actually get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Even just saving a few hundred dollars per month and investing that into undervalued high-quality dividend growth stocks can unlock financial independence and turn you into a millionaire over time.

All that said, being able to spot undervaluation first requires one to understand the ins and outs of valuation.

That’s where Lesson 11: Valuation enters the picture.

Written by Dave Van Knapp, a fellow contributor, it provides an easy-to-follow valuation template that can be applied to almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Air Products & Chemicals (APD)

Air Products & Chemicals (APD)

Air Products & Chemicals (APD) is a major global producer and supplier of industrial gases, now the largest supplier of hydrogen and helium in the world.

Founded in 1940, Air Products & Chemicals is now a $59 billion (by market cap) industrial gases giant that employs over 20,000 people.

The company’s FY 2023 sales were reported through four Industrial Gases business segments organized by geography: Americas, 43%; Asia, 26%; Europe, 24%; and the Middle East and India, 1%. Corporate and other accounted for the remainder.

There are three key reasons why Air Products & Chemicals is such a fantastic business and long-term investment.

First up, industrial gases are critical input for the manufacturing processes of many different end products ranging from electronics to vehicles.

These products literally cannot be produced without industrial gases.

Second, because of the critical nature of these industrial gases, and because constant and reliable access to these gases is an absolute must, a manufacturer will set up a long-term contract with a dependable provider of said gases (such as Air Products & Chemicals).

Complex infrastructure is then installed at a manufacturing site to ensure reliability, which makes it extremely costly and difficult to switch providers later.

The third reason is, Air Products & Chemicals is part of a global oligopoly: There are only three major companies in this space that control the vast majority of the available global market share.

Let’s just break that down real quick.

Air Products & Chemicals combinesnecessary inputwith long-term contracts reinforced by at-site infrastructure, and the companies does this within the favorable confines of a global oligopoly.

Did you catch that?

Customers can’t do without the industrial gases, there are only a few players to choose from, and contracts and infrastructure lock the customers in.

It’s a business model with built-in favorable conditions for success.

It almost cannot lose over the long run.

This is precisely why Air Products & Chemicals should be able to continue increasing its revenue, profit, and dividend for many years to come (just as it has for many years already).

Dividend Growth, Growth Rate, Payout Ratio and Yield

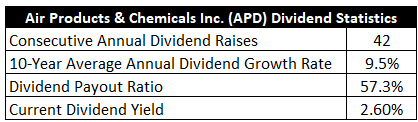

Indeed, this is a company that has increased its dividend for 42 consecutive years.

That easily qualifies it for its status as a vaunted Dividend Aristocrat.

The 10-year dividend growth rate of 9.5% is very solid and quite impressive when considering the size of the company and the fact that we’re already decades into the dividend growth story.

That said, the most recent dividend raise was only 1.1%, as the company is busy investing in a number of growth projects around the world (which I’ll touch on later).

However, once we’re on the other side of this heavy CapEx cycle, I’m confident that Air Products & Chemicals will return to its high-single-digit dividend growth ways.

And you get to pair that with the stock’s healthy 2.6% yield.

And you get to pair that with the stock’s healthy 2.6% yield.

This yield, by the way, is 40 basis points higher than its own five-year average, so the market has adjusted the yield higher in order to compensate for the near-term compression in dividend growth.

A payout ratio of 57.3%, based on midpoint guidance for FY 2024 adjusted EPS, indicates a well-covered dividend, although the FCF coverage looks temporarily poor (due to higher-than-average CapEx, as I just mentioned).

This Dividend Aristocrat has one of the best dividend growth track records out there, both in terms of length and rate, but the short-term dividend growth story will probably have limited excitement.

Investing in the business by funding growth projects is precisely what long-term investors should want this management team to do – businesses that sit on their laurels and fail to invest and keep up with competition eventually run into major problems – so being able to overlook the short-term shortcomings on dividend growth may be the most rewarding thing to do over time.

It’s short-term pain for long-term gain.

In spite of the CapEx, Air Products & Chemicals still has a beautiful dividend growth profile.

Revenue and Earnings Growth

As beautiful as these numbers are, though, many of them are looking backward.

However, investors must always be looking forward, as today’s capital is being risked for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be of great use when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this manner should give us the information we need to determine where the business could be going from here.

Air Products & Chemicals moved its revenue from $10.4 billion in FY 2014 to $12.6 billion in FY 2013.

That’s a compound annual growth rate of 2.2%.

Not exactly inspiring top-line growth.

But there’s a huge caveat to this.

The company’s management had decided to intentionally make the business smaller and more efficient through what was called the “Five-Point Plan”, which was introduced in 2014.

This plan was designed to focus the business on industrial gases by jettisoning non-core operations.

Executing this plan led to spinning off the electronics material division in 2016, and the performance materials division was then sold in 2017 for $3.8 billion in cash.

All of this worked out fantastically well.

Earnings per share grew from $4.61 to $10.33 over this period, which is a CAGR of 9.4%.

That’s more like it.

We can see not only how much more efficient and profitable the business is but also how closely EPS and dividend growth have matched up over the last decade.

There hasn’t been much of a change in the outstanding share count, so all of this excess bottom-line growth was driven by improved profitability.

And if recent investments pan out, shareholders could be looking at even faster growth over the next decade.

Looking forward, CFRA is forecasting that Air Products & Chemicals will compound its EPS at an annual rate of 12% over the next three years.

See, there it is.

That’s the bottom-line growth acceleration that’s been playing out and appears to be gaining steam.

CFRA highlights the “…clear visibility for double-digit EPS growth over the next several years (although FY 2024 is likely only high-single digits) due to [Air Products & Chemicals]’s on-site (take-or-pay) business combined with a record backlog.”

Indeed, to that last point, Air Products & Chemicals recently reported its backlog as being near $20 billion.

This is why CapEx is so high right now (management is targeting $5 billion to $5.5 billion in capital expenditures for FY 2024 – about twice as high as only a few years ago).

Put simply, Air Products & Chemicals is building out the projects that customers are demanding.

CFRA also states that it is “…bullish on [Air Products & Chemicals]’s backlog of growth projects with a focus on expanding the scope of syngas supply agreements, acquiring air separation units, and new agreements in large industrial gas projects. [Air Products & Chemicals] is well positioned to capitalize on gasification related to carbon capture and hydrogen mobility, which are long-term secular tailwinds.”

That last point is really important, as the company is just now starting to benefit from these two new growth areas.

Previously, it was a big manufacturing story.

We can now add cleaner energy and mobility to the mix – only adding to the appeal.

An example of this would be the company’s Alberta, Canada net-zero hydrogen energy complex that takes Alberta natural gas and then uses processes to capture/sequester 90% of carbon dioxide and produce net-zero hydrogen (among other products).

I don’t think CFRA’s projection is unreasonable, although I wouldn’t necessarily expect like dividend growth to play out over the next few years.

However, again, once the company is past this big investment phase, I fully believe that Air Products & Chemicals will get back to at least high-single-digit dividend growth.

And there’s room for upside surprise to that (perhaps somewhere in the low-teens area).

Meantime, investors are starting out with a pretty nice yield.

There’s not much to complain about.

Financial Position

Moving over to the balance sheet, Air Products & Chemicals has a really good financial position.

The long-term debt/equity ratio is 0.6, while the interest coverage ratio is over 15.

The company finished last fiscal year with $9.4 billion in L-T debt, and I consider that to be relatively benign for a company sporting a market cap near $60 billion.

Air Products & Chemicals has engaged in a number of joint ventures in order to fund growth projects without overly stressing cash flow and the balance sheet, and that’s helped to maintain balance sheet strength alongside spending and investments.

Profitability is decently robust.

Return on equity has averaged 16.4% over the last five years, while net margin has averaged 19.6%.

The returns on capital certainly aren’t the highest I’ve seen, but they are more than respectable and enough to keep the compounding machine going.

Overall, Air Products & Chemicals is a great business.

And the company does benefit from durable competitive advantages, including global economies of scale, large barriers to entry, high switching costs, a global oligopoly, and long-term contracts with fixed infrastructure.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Demand for industrial gases is correlated with manufacturing activity, and so any kind of broad economic contraction would impact the company.

Since the company is heavily involved in a variety of major energy projects around the world, ongoing changes within the global energy complex adds uncertainty and long-tail risks.

The current heavy CapEx cycle is weighing on cash flow.

Massive projects being undertaken around the world introduces execution risks.

Input costs can be volatile.

More than half of the company’s sales come from outside the Americas, exposing the company to currency exchange rates and geopolitics.

Joint ventures are employed in order to help fund growth projects, but the financial health/commitment of partners may vary over time.

There are some risks to consider, but the quality of the business is also worth considering.

And with the valuation looking so reasonable, the risks could be worth the stretch…

Valuation

The P/E ratio is 24.5.

That’s well below its own five-year average of 28.4.

And using midpoint guidance for this year’s adjusted EPS, the forward P/E ratio drops to 21.9.

The P/CF ratio of 16.7 is not egregious at all, and that’s also below its own five-year average of 17.4.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

That growth rate is at the higher end of what I’ll allow for, but I think it makes sense here.

The company has grown its EPS and dividend at a rate well in excess of this mark over the last decade, and the near-term forecast for EPS growth is also far ahead of this number.

Assuming that CFRA is somewhere in the ballpark, my model builds in a large margin of safety (between go-forward EPS growth and dividend growth), which is likely the correct thing to do – the CapEx will limit dividend growth relative to EPS growth.

Still, a lot of wiggle room here.

And seeing as how this is a long-term model, I do think dividend growth will pick up nicely once we’re past the the heavy investment cycle.

The DDM analysis gives me a fair value of $304.44.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Even after a sensible look at the value of the business, the stock looks appealing.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates APD as a 4-star stock, with a fair value estimate of $303.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates APD as a 5-star “STRONG BUY”, with a 12-month target price of $297.00.

We have a tight consensus here. Averaging the three numbers out gives us a final valuation of $301.48, which would indicate the stock is possibly 10% undervalued.

Bottom line: Air Products & Chemicals (APD) is running a powerful business model which is exposed to numerous secular growth areas of the global economy. It’s backed by a huge backlog, contracts, fixed infrastructure, and an oligopolistic industry. With a market-beating yield, a healthy payout ratio, high-single-digit dividend growth, more than 40 consecutive years of dividend increases, and the potential that shares are 10% undervalued, this Dividend Aristocrat is a viable alternative to hyped-up and expensive options elsewhere in the market.

Bottom line: Air Products & Chemicals (APD) is running a powerful business model which is exposed to numerous secular growth areas of the global economy. It’s backed by a huge backlog, contracts, fixed infrastructure, and an oligopolistic industry. With a market-beating yield, a healthy payout ratio, high-single-digit dividend growth, more than 40 consecutive years of dividend increases, and the potential that shares are 10% undervalued, this Dividend Aristocrat is a viable alternative to hyped-up and expensive options elsewhere in the market.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is APD’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 95. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, APD’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Disclosure: I’m long APD.

Source: Dividends & Income