Investing can be as easy or as hard as you want to make it.

But why make it hard?

Why add undue difficulty and risk?

I think investing should be as easy and straightforward as possible, which sets one up for durable, reliable, and repeatable success over the long run.

That’s why I’ve adhered to the dividend growth investing strategy for more than a decade now.

This strategy is one that advocates buying and holding shares in world-class businesses that pay safe, growing dividends to shareholders.

You can find hundreds of these businesses on the Dividend Champions, Contenders, and Challengers list.

That list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

To be able to afford to pay steadily rising dividends requires a business to steadily increase profit and cash flow.

To be able to afford to pay steadily rising dividends requires a business to steadily increase profit and cash flow.

And it takes a special kind of business to do that.

This is why the strategy tends to funnel an investor right into some of the world’s best businesses.

Like I said, I’ve adhered to the strategy for more than a decade.

It’s guided me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

In fact, because my dividend income is enough to cover my bills, I was even able to retire in my early 30s.

My Early Retirement Blueprint explains how I did that.

My Early Retirement Blueprint explains how I did that.

Now, the strategy is about more than just investing in high-quality businesses that pay safe, growing dividends.

Valuation at the time of investment is also a major consideration.

See, price is only what you pay, but it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying high-quality dividend growth stocks at appealing valuations might just be the best way to keep investing simple, do extraordinarily well with your money, and even become financially independent over time.

Of course, knowing when a valuation is appealing means one already understands the ins and outs of valuation.

Well, that’s where Lesson 11: Valuation comes in handy.

Written by fellow contributor Dave Van Knapp, it provides a handy valuation guide that can help one to estimate the fair value of almost any dividend growth stock.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Philip Morris International Inc. (PM)

Philip Morris International Inc. (PM)

Philip Morris International Inc. (PM) is the world’s largest publicly traded tobacco company, engaged in the manufacture and marketing of tobacco and related nicotine products.

Originally founded in 1847, Philip Morris International (hereafter referred to as PMI) is now a $155 billion (by market cap) global tobacco and nicotine behemoth that employs more than 80,000 people.

FY 2023 revenue can be broken down mainly geographically: Europe, 38%; South and Southeast Asia, Commonwealth of Independent States, Middle East, and Africa, 30%; East Asia, Australia, and PMI Duty Free Region, 18%; Swedish Match, 7%; Americas, 6%; and Wellness and Healthcare, 1%.

PMI sold approximately 613 billion cigarettes in 2022, down slightly from approximately 622 billion in 2022.

The company’s global market share of cigarettes and heated tobacco is an estimated 28%, excluding China and the US (a state-owned monopoly controls the China market, and PMI sells no cigarettes in the US market).

This incredible global market share is due largely to the strength and ubiquity of Philip Morris’s Marlboro brand, the #1 cigarette brand in the world.

This one brand alone comprised more than 39% of the company’s total cigarette sales volume for last year.

It is one of the most dominant consumer brands in the world.

And as long as a brand is properly managed and continues to deliver on expectations, dominant brands tend to stay dominant.

This puts a company with dominant brands in a powerful spot.

What makes PMI especially powerful in this respect is the fact that the company combines a dominant brand with the addictive nature of its product.

Brand loyalty alone can carry a company far.

But PMI takes that idea to the next level by adding addictive properties to the equation.

That equation spits out an end product (the Marlboro cigarette) that is highly price inelastic – i.e., an increase in price doesn’t significantly reduce demand.

This kind of pricing power is very uncommon in the world, and it’s a potent counter to unfavorable industry dynamics stemming from the secular decline in smoking (which is leading to steadily decreasing cigarette volumes).

The secular decline of smoking isn’t news, of course, and PMI’s management figured out quite a while ago that the cigarette industry is a “melting ice cube”.

In response, a transformation began in earnest a number of years ago, pivoting the entire business model toward cigarette alternatives.

This has led to something that might be quite surprising to casual observers.

PMI actually has growth engines – two of them!

Because of prescient investments in non-cigarette products, PMI now has two key product offerings which are growing.

First, it has its IQOS HTUs (heated tobacco units).

These RRPs (reduced-risk products) use a heat-not-burn technology, and sales have been brisk.

IQOS has the #1 position in 11 markets, and HTUS showed 14.7% YOY growth in FY 2023.

This quote from the Q4 FY 2023 earnings release says it all: “This was led by the continued growth of IQOS, which has now surpassed Marlboro in terms of net revenues, confirming its position as the leading premium nicotine brand less than 10 years from launch.”

That is remarkable.

Second, PMI has ZYN, which is a nicotine pouch product that is proving to be a wildly popular alternative to smoking (allowing consumers to consume nicotine without harmful combustion).

ZYN showed 62% YOY growth in FY 2023, which is an eye-popping number for any business (but especially for this business).

I have another quote, from Q1 FY 2024, which nicely sums up where we’re now at with PMI: “The smoke-free business accounted for 39% of our total net revenues.”

PMI is quickly headed toward getting the majority of its revenue from non-cigarette, smoke-free products.

It’s not hard to imagine a future in which the company basically sells no cigarettes at all.

Management has executed an incredible pivot, which is positioning the business to not just survive but thrive over the coming decades.

And that’s what should lead to continued revenue, profit, and dividend growth for years to come, even with shrinking cigarette volumes.

Dividend Growth, Growth Rate, Payout Ratio and Yield

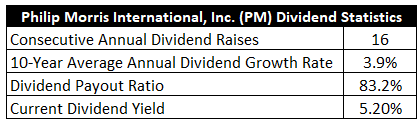

Already, PMI has increased its dividend for 16 consecutive years.

That’s actually as long as the track record could possibly be, as it dates back to the company’s initial spin-off from former parent company Altria Group Inc. (MO) in 2008.

The 10-year dividend growth rate of 3.9% is modest, but there are two things to keep in mind.

First, this is an income play, not some high-quality compounder with lots of growth.

The stock yields a market-smashing 5.2%.

The stock yields a market-smashing 5.2%.

Is the low growth rate worth that 5%+ yield?

For those who prioritize income over growth, perhaps so.

This yield is pretty close to its own five-year average, and that’s because the market tends to expect a higher yield and uses that to compensate for the lower growth rate.

The second thing is, I think this dividend growth rate will pick up over the coming years.

The last ten years was a period in which PMI was mostly a dying tobacco company.

It wasn’t until recently that IQOS started to hit an inflection point, and ZYN wasn’t brought on until late 2022 (which is when PMI acquired ZYN maker Swedish Match).

PMI’s level of leverage, especially after the Swedish Match acquisition, will have to be thoughtfully managed, but the twin growth engines now firing for PMI does position the overall company for faster dividend growth over the next 10 years compared to what transpired over the last 10 years.

The payout ratio of 83.2%, based on midpoint guidance for FY 2024 adjusted EPS, is high, but PMI has typically operated with a payout ratio of over 80%.

This is not uncommonly high for PMI, but it does leave little capital to reinvest back into the business and further reinforce its nature as an income play.

For income-seeking investors, this 5%+ yield with new, exciting growth kickers might be one of the most interesting and appealing opportunities out there.

Revenue and Earnings Growth

As interesting as this may be, though, many of these numbers are based on the past.

However, investors must always be thinking about the future, as today’s capital is risked for tomorrow’s rewards.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be extremely useful when the time comes later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this way should give us enough information to make a judgment call on where the business might be going from here.

PMI advanced its revenue from $29.8 billion in FY 2014 to $35.2 billion in FY 2023.

That’s a compound annual growth rate of 1.9%.

Not much top-line growth, to be sure, but any growth at all over the last 10 years, even while the core product is clearly in secular decline, strikes me as pretty impressive and just goes to show how powerful the pricing power is for this business.

Meantime, earnings per share grew from $4.76 to $5.02 over this period, which is a CAGR of 0.6%.

Again, PMI hasn’t been moving the needle much over the last 10 years, which explains why the stock has been pretty flat over the last decade.

Now, if I thought the next decade would look a lot like the last decade, I wouldn’t be covering this business today, and I wouldn’t see anything appealing about it.

However, there’s a clear case that the next decade will look much better than the last decade, with IQOS turning the corner and ZYN now on board.

One must believe in PMI’s overarching smoke-free strategy in order to see an investable business for the long run.

Otherwise, if one is confident that PMI is just another dying tobacco company, it’s better to stay away.

It comes down to seeing brighter days ahead.

We invest in where a business is going, not where it’s been.

You can’t make money on yesterday’s results.

Looking forward, CFRA believes that PMI will grow its EPS at a compound annual rate of 6% over the next three years.

So there’s the faster growth that I’ve been harping on.

CFRA highlights the pricing power and two growth engines, first with this passage: “Despite declining global cigarette consumption, we look for pricing gains and growth in emerging markets to support revenues. We think the sales growth of [PMI]’s heated tobacco product, IQOS, will lead to market share gains and help offset cigarette volume weakness. We also view [PMI]’s strong cash flow generation as supportive of its dividend, which was recently increased to $5.20/share.”

And then there’s this from CFRA: “[PMI] acquired Swedish tobacco/snus manufacturer Swedish Match for about $14 billion. We viewed the acquisition positively for [PMI], as it is expected to be accretive to adjusted EPS and helps increase [PMI]’s exposure to faster-growing products. Over two-thirds of Swedish Match’s total revenue came from oral products, such as nicotine pouches and snus prior to the acquisition.”

This is the essence of the long-term investment thesis for PMI.

The company’s immense pricing power helps it to slowly grow, or at least tread water, while cigarette volumes slowly shrink, giving the two new growth engines time to rev up and take over.

If we zoom into PMI’s most recent quarter – Q1 FY 2024 – adjusted EPS (ex. currency) showed 23.2% YOY growth.

Tying that in with the volumes coming out of IQOS and ZYN provides clear evidence that PMI’s growth trajectory has improved significantly.

Now, I wouldn’t necessarily expect high-single-digit EPS growth to translate into the same level of dividend growth.

It would be wise for PMI to dedicate some cash flow toward deleveraging.

Still, there should be room for mid-single-digit (or thereabouts) dividend growth over the coming years as the newfound growth allows for decent dividend raises while also responsibly managing the balance sheet.

And that should be good enough to drive a ~10% annualized total return, even without any kind of multiple rerating (which is certainly possible, as the higher growth rate could command higher multiples in the marketplace).

Not bad at all for what is really an income play.

Financial Position

Moving over to the balance sheet, PMI has a decent financial position.

Because of negative shareholders’ equity, there’s no debt/equity ratio.

PMI finished FY 2023 with just over $41 billion in long-term debt.

I don’t think that’s egregious for a company with a market cap of $150+ billion.

The interest coverage ratio is nearly 8, which is good but not great.

I don’t think the balance sheet is of immediate concern, but there’s a fairly large chunk of debt here, and I would like to see PMI slowly deleverage over the coming years (which was occurring before the Swedish Match acquisition).

Profitability is, as one might expect, outstanding.

ROE isn’t applicable because of negative equity, but net margin has averaged 26.5% over the last five years.

ROIC is typically coming in at well over 30%.

When you produce an addictive product at very low costs, it’s not surprising to see sky-high margins and returns on capital.

Unfortunately, because of the secular decline issue, PMI hasn’t benefited as much as they could have from the high returns on capital (because it’s been unable to effectively reinvest back into growth).

You want both high growth and high returns on capital to really get compounding moving, and that’s why the combination of IQOS and ZYN is so exciting.

Overall, PMI might just be in the best position it’s been in since the initial spin-off.

And the company does benefit from durable competitive advantages, including pricing power, brand loyalty, global economies of scale, and high barriers to entry.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

The very business model introduces above-average regulation and litigation risks.

Smoking bans, prohibitions on flavored tobacco products, and crackdowns on e-cigarettes are all examples of rising regulatory pressure on the business model (although PMI does not sell any cigarettes in the US, which shields the company from US-specific regulation).

On the other hand, competition is somewhat limited, as the entrenched players, while competitive with one another, are unlikely to see any major new competition ever because of how impossibly difficult it would be to start to a new tobacco company from scratch today.

Being headquartered in the US and reporting results in USD while deriving most of its sales from outside of the US exposes the company to volatile currency exchange rates more than the average US-based business.

Any slowing of the worldwide adoption of cigarette alternatives (vis-à-vis IQOS and ZYN) would negatively affect the company’s ability to offset decline traditional cigarette volumes with growth elsewhere.

Lastly, any speedup in the annual contraction of cigarette volumes would harm the company’s ability to cover its dividend, manage the debt load, and pivot toward new growth areas.

There are serious risks to contend with.

But with the valuation being as reasonable as it is, even while growth appears to be accelerating, could make the risks worth the stretch…

Valuation

The stock is trading hands for a P/E ratio of 19.5, using TTM GAAP EPS.

That is not a particularly high earnings multiple in this market.

Using midpoint guidance for FY 2024 adjusted EPS, the forward P/E ratio drops to 15.9.

That’s downright low in this environment.

The P/S ratio of 4.3 is slightly lower than its own five-year average of 4.5.

And the yield, as noted earlier, is close to its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 4.5%.

That’s about as low as I go in the model, but I think low expectations are warranted here.

This isn’t far off from PMI’s demonstrated 10-year dividend growth rate, which strikes me as a good baseline.

It is lower than the near-term forecast for EPS growth, and it looks downright pessimistic when compared to recent results out of PMI, but the debt load will have to be juggled alongside dividend growth.

Keep in mind, the most recent dividend raise out of PMI was only 2.4%, so I am assuming a nice uptick in divided growth over the coming years (supported by IQOS and ZYN).

The DDM analysis gives me a fair value of $98.80.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

This stock looks appropriately valued based on my model.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates PM as a 3-star stock, with a fair value estimate of $103.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates PM as a 4-star “BUY”, with a 12-month target price of $110.00.

I came out a tad low this time around. Averaging the three numbers out gives us a final valuation of $103.93, which would indicate the stock is possibly 4% undervalued.

Bottom line: Philip Morris International Inc. (PM) is a company with some of the best brand recognition and pricing power on the planet. Prescient investments in adjacent products with explosive growth are finally paying off, and the business appears to be at an inflection point. With a market-smashing yield, moderate dividend growth, a manageable payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 4% undervalued, income-oriented dividend growth investors who want an exciting growth kicker could have a very interesting long-term investment opportunity on their hands.

Bottom line: Philip Morris International Inc. (PM) is a company with some of the best brand recognition and pricing power on the planet. Prescient investments in adjacent products with explosive growth are finally paying off, and the business appears to be at an inflection point. With a market-smashing yield, moderate dividend growth, a manageable payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 4% undervalued, income-oriented dividend growth investors who want an exciting growth kicker could have a very interesting long-term investment opportunity on their hands.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is PM’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 64. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, PM’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long PM.