The world is an interesting place.

On one hand, you have wealthy, successful people who are out there making things happen.

On the other hand, you have a lot of people who are struggling just to get by.

So what separates the two?

Well, there’s no one answer, and there are many components to this, but I think living below one’s means and investing the surplus capital is certainly a big factor.

And if one is going to invest, why do it in a subpar way?

No, if we invest, we want to invest in the most effective manner possible.

This is precisely where dividend growth investing comes in.

It’s a long-term investment strategy that advocates buying and holding shares of world-class enterprises paying safe, growing dividends to shareholders.

How do we find these businesses?

A great resource for that is the Dividend Champions, Contenders, and Challengers list – a compilation of invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

You’ll notice many household names on that list.

You’ll notice many household names on that list.

For good reason.

After all, it requires ever-more profit to be able to afford ever-larger cash payouts to shareholders.

And it takes a special kind of business to produce ever-more profit.

I’ve been using this strategy for more than a decade now, allowing it to guide me as I’ve gone about building out my FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

I’ve actually been in the super fortunate position of being able to live off of dividend income since I quit my job and retired in my early 30s.

My Early Retirement Blueprint explains exactly how I was able to do that.

My Early Retirement Blueprint explains exactly how I was able to do that.

Now, the strategy involves more than just selecting the right businesses for investment.

Valuation is also key.

Whereas price represents what you pay, value represents what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Living below your means and investing your savings into high-quality dividend growth stocks at attractive valuations should allow you to separate yourself from the pack and even eventually achieve financial independence.

All that said, the whole conversation around valuation assumes a basic understanding already in place.

If that’s not in place, don’t worry.

Lesson 11: Valuation will help.

Put together by fellow contributor Dave Van Knapp, it’s part of an overarching series of “lessons” designed to teach the ins and outs of the dividend growth investing strategy.

It contains a helpful valuation template that can be used to estimate the fair value of almost any dividend growth stock out there.

Restaurant Brands International Inc. (QSR)

Restaurant Brands International Inc. (QSR)

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Restaurant Brands International Inc. (QSR) is a Canadian-American global quick-service restaurant company.

Founded in 2014, but with certain roots dating back to 1954, Restaurant Brands International (hereafter referred to as RBI) is now a $22 billion QSR giant that employs approximately 9,000 people.

With more than 31,000 restaurants worldwide, RBI is one of the largest QSR operators in the world.

The company has five reportable business segments, corresponding mainly to the company’s four restaurant brands: Tim Hortons (TH), 44% of FY 2023 adjusted operating income; Burger King (BK), 18%; Popeyes Louisiana Kitchen (PLK), 10%; and Firehouse Subs (FHS), 2%. The international segment, which comprises more than 14,000 franchised restaurants, accounts for the remaining 27%.

This is a very appealing long-term investment candidate for two big reasons.

First, it’s an easy-to-understand business model.

Nobody throws RBI into the “too hard pile”.

We all have to eat food, and almost everyone out there is likely familiar with these brands already.

And because we all have to eat food, there’s a certain amount of built-in demand for this company’s products.

It’s a “one-foot bar” one has to step over here.

Second, it’s a capital-light franchise model that results in steady royalties and fees coming straight to the parent company (RBI) from the franchisees.

That consistent, recurring cash flow is highly alluring.

All well and good, but RBI has had trouble in the past converting all of that into sustained excellent performance.

Many of its restaurants are perceived to be older and not as clean as some rivals, and food quality can be inconsistent.

The brands, especially BK, may be looked at as “tired”.

However, new management and initiatives, which I’ll delve into later, could be setting up RBI for an extended period of renewed excellence, and that bodes well for the company’s ability to drive its revenue, profit, and dividend higher over the coming years.

Dividend Growth, Growth Rate, Payout Ratio and Yield

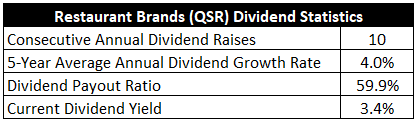

To date, RBI has increased its dividend for 10 consecutive years, dating back to its 2014 formation (after BK owner 3G Capital acquired TH and created the RBI group).

The five-year dividend growth rate is only 4%, which is disappointing, but recent growth trends (which I’ll soon touch on) are encouraging.

While the dividend growth has been pretty mediocre, the stock does yield a market-beating 3.4%.

That’s not bad at all.

That’s not bad at all.

This yield is also 10 basis points higher than its own five-year average.

And with a payout ratio of 59.9%, the dividend is easily covered and positioned to grow roughly in line with the business.

It’s hard to find a yield this high in the QSR space, and the brands are highly recognizable.

If the growth can pick up a bit, and it looks like it will, there’s definitely a compelling dividend setup here.

Revenue and Earnings Growth

As compelling as that setup may be, though, some of these dividend metrics are looking backward.

However, investors must always be looking forward, as the capital of today gets put on the line and risked for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be of use when later trying to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this manner should give us what we need to make an educated call on where the business could be going from here.

RBI moved its revenue from $4 billion in FY 2015 to $7 billion in FY 2023.

That’s a compound annual growth rate of 7.3%.

I only used a nine-year period here, dating back to FY 2015, because FY 2014’s numbers are not clean and totally applicable.

FY 2015 was the first full year in public view for RBI.

This is pretty good top-line growth.

However, it’s important to keep in mind that RBI has been acquisitive (acquiring PLK in 2017, and acquiring FHS in 2021).

This inorganic growth of the group has fueled extra revenue growth, and that clouds things.

Meanwhile, earnings per share grew from $0.50 to $3.76 over this nine-year period, which is a CAGR of 28.7%.

That’s very strong bottom-line growth, but it does look better than it ought to because of the weak starting point.

Still, RBI did produce 15.7% YOY EPS growth for FY 2023, so there’s evidence of something special being cooked up (pardon the pun).

What I see is a business that kind of struggled to get much traction between FY 2015 and FY 2020, but results since FY 2021 have been consistently strong.

Looking forward, CFRA believes that RBI will compound its EPS at an annual rate of 8% over the next three years.

For a mature QSR conglomerate, I actually think an 8% CAGR would be great.

There are a few important things to make note of here.

First, RBI brought on J. Patrick Doyle as Executive Chairman.

Doyle was CEO of Domino’s Pizza Inc. (DPZ) for nearly a decade, and he’s given much of the credit for the huge turnaround and revival at Domino’s and its products and services that led to an explosion in sales growth and a ~2,000% gain in the stock during his CEO tenure.

RBI offered a generous stock plan to Doyle.

Not only that, but Doyle personally staked $30 million of his own money on RBI’s stock.

Doyle is betting on his ability to get this business moving in the right direction.

You’ve gotta love that kind of “skin in the game”.

Early efforts are showing promise – Q1 FY 2024 showed 4.6% comps growth in an environment in which QSR competitors are struggling with comps.

EPS for Q1 FY 2024 also increased by 18% YOY.

The company recently put together a five-year outlook that calls for 8%+ system-wide sales growth and 8%+ adjusted operating income growth.

This lines up well with where CFRA is at, and I think all of this is very achievable.

Much of this should come from the company’s “Reclaim the Flame” initiative, which aims to revive the Burger King brand.

RBI plans to re-franchise the vast majority of the BK portfolio to new or existing smaller franchise operators that live in their local communities.

A huge step in this direction was the recent $1 billion acquisition of Carrols Restaurant Group (the largest BK franchisee in the US).

This acquisition will allow RBI to speed up the BK turnaround by reinvesting in the brand, remodeling restaurants, giving local franchisees the tools for success, and providing a better and more consistent experience to customers.

Also, PLK has recently shown the fastest growth among the brands (it seems to be the key growth engine for the company), with some of its products (especially its new chicken sandwich) exploding in popularity, and the 2017 acquisition of PLK by RBI may go down as one of the best moves in the QSR industry’s history.

With Doyle personally involved and invested in the story, and with results of late being so strong, I see no reason why RBI can’t deliver on its objectives.

And if those objectives are met, that would open things up for a very strong total return profile over the coming years, driven largely by higher business and dividend growth.

Plus, one gets a 3%+ yield to start off with.

So that’s 8%+ growth and a 3%+ yield, equaling an 11%+ annualized total return (assuming a static valuation).

Doyle clearly sees a lot to like.

I’m inclined to agree.

Financial Position

Moving over to the balance sheet, RBI has a poor financial position.

This is by far my least favorite part of this business.

The long-term debt/equity ratio is 2.8, while the interest coverage ratio is approximately 3.5.

These are definitely not great numbers.

To be fair to RBI, it’s not uncommon for QSR operators to run leveraged balance sheets.

A capital-light royalty collector can do that.

The aforementioned Domino’s Pizza, for instance, also has a highly leveraged balance sheet.

Still, as a bit of a stickler around debt, I am not a fan of this balance sheet.

With the focus currently on growth initiatives, not deleveraging, RBI will have to grow its way out of this situation.

Profitability, though, is decently solid.

Return on equity has averaged 33.7% over the last five years, while net margin has averaged 13.2%.

Now, ROE has been juiced by leverage.

ROIC is typically coming in at around 9% – good, but not nearly as impressive as ROE.

Overall, with the business apparently on the cusp of an inflection point, and with a key director financially incentivized to make it work, it’s a very interesting long-term investment candidate.

And with economies of scale, brand recognition, and pricing power, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Competition, in particular, is an issue, as the QSR space is extremely competitive and lacks barriers to entry.

The balance sheet is objectively among the worst in the industry, and heavy use of leverage will weigh on cash flow and limit other opportunities for capital.

QSRs, in general, aren’t perceived to provide the same value as they used to, and higher prices on end products are weighing on customers.

RBI’s BK brand doesn’t have the same brand goodwill in the US as its chief competitors, although the recent initiative to revive the brand is attempting to fix this issue.

The company’s expansive international footprint exposes it to geopolitics and currency exchange rates.

Inflation has caused input costs to rise, especially labor.

Labor can be unreliable.

The turnaround at BK faces execution risk.

I think there are serious risks to consider – perhaps more risks than with the average QSR I look at – but the business, especially with Doyle involved, still has a lot to offer.

And the low valuation also has a lot to offer…

Valuation

The stock’s P/E ratio is 17.6.

When you look at the QSR landscape, that is a comparatively low earnings multiple.

It’s also lower than its own five-year average of 24.5.

The P/CF ratio of 19.2 is also not super demanding.

And the yield, as noted earlier, is slightly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

That growth rate is on the lower end of what I usually ascribe to a QSR operator, and that’s because of the leverage and questions around the BK turnaround.

Despite the leverage, I do think other key brands (PLK and TH, namely) and Doyle’s involvement (personal and financial) are super alluring aspects of the full story here.

Now, this 7% mark is higher than RBI’s demonstrated dividend growth over the last several years.

I get that.

However, based on the company’s own longer-term growth guidance, as well as CFRA’s near-term EPS growth guidance, I think a 7% DGR is achievable.

In fact, the 7% number is lower than those two forecasts, although I’m building in a margin of safety (due to the leverage and ongoing investments in BK).

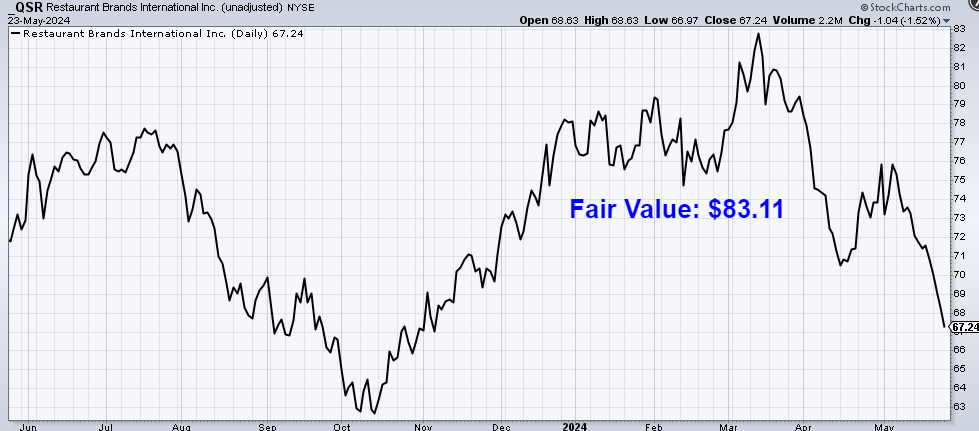

The DDM analysis gives me a fair value of $82.75.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think I took a sober look at the stock and valuation, yet some cheapness appears to be present.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates QSR as a 4-star stock, with a fair value estimate of CAD $108.00 (USD $78.91).

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates QSR as a 4-star “BUY”, with a 12-month target price of CAD $120.00 (USD $87.68).

I’m somewhere in the middle here. Averaging the three numbers out gives us a final valuation of $83.11, which would indicate the stock is possibly 18% undervalued.

Bottom line: Restaurant Brands International Inc. (QSR) controls globally renowned brands, and the company now has one of the QSR industry’s very best managers financially incentivized to get the business to its best possible state. Recent results out of the company have been very encouraging, and turnaround efforts are taking off in earnest. With a market-beating yield, mid-single-digit dividend growth, a reasonable payout ratio, 10 consecutive years of dividend increases, and the potential that shares are 18% undervalued, long-term dividend growth investors looking for an attractive investment in the QSR space may have something special being cooked up here.

Bottom line: Restaurant Brands International Inc. (QSR) controls globally renowned brands, and the company now has one of the QSR industry’s very best managers financially incentivized to get the business to its best possible state. Recent results out of the company have been very encouraging, and turnaround efforts are taking off in earnest. With a market-beating yield, mid-single-digit dividend growth, a reasonable payout ratio, 10 consecutive years of dividend increases, and the potential that shares are 18% undervalued, long-term dividend growth investors looking for an attractive investment in the QSR space may have something special being cooked up here.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is QSR’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 45. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, QSR’s dividend appears Borderline Safe with a moderate risk of being cut. Learn more about Dividend Safety Scores here.

Disclosure: I have no position in QSR.

Source: Dividends & Income