We all want to become extraordinary investors.

So how do we do that?

Well, I think it’s simpler than it might initially seem.

Extraordinary investors get extraordinary results.

And it’s extraordinary businesses that can provide extraordinary results over time.

And it’s extraordinary businesses that can provide extraordinary results over time.

It comes down to buying and holding shares in extraordinary businesses, and then letting the process of compounding play out over a long period of time.

This is why I’m such a fan of dividend growth investing – a strategy whereby one buys and holds shares in world-class businesses that pay safe, growing dividends to shareholders.

Because it requires growing profit to afford growing dividends, and because it requires a business to be great in order to consistently generate growing profit, dividend growth investing can funnel one right into the extraordinary businesses.

You can see what I mean by looking over the Dividend Champions, Contenders, and Challengers list .

This list has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

The strategy has guided me for more than a decade as I’ve gone about building the FIRE Fund.

This is my real-life, real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

In fact, I’ve been in the extremely fortunate position of being able to live off of dividends since I quit my day job and retired in my early 30s.

My Early Retirement Blueprint explains how I was able to do such a thing.

Now, while investing in extraordinary businesses can take you far, valuation at the time of investment is still very important.

Price is what you pay, but value is what you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Simply buying shares of extraordinary businesses when undervaluation is present, then holding for the long term, can set one up to become an extraordinary investor.

But being ready and able to acknowledge undervaluation means one already understands the concept of valuation.

Well, that’s where Lesson 11: Valuation comes in.

Written by my colleague Dave Van Knapp, it’s a valuation guide which includes an easy-to-follow valuation template that can be used to estimate the fair value of almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Prologis Inc. (PLD)

Prologis Inc. (PLD)

Prologis Inc. (PLD) is a global real estate investment trust that develops, acquires, and operates industrial and logistics facilities.

Founded in 1983, Prologis is now a $100 billion (by market cap) real estate behemoth that employs approximately 2,500 people.

The company’s property portfolio consists of more than 5,600 properties comprising a total of 1.2 billion square feet.

Its two largest markets (by properties) are the US (nearly 3,900 properties) and Europe (nearly 1,100 properties).

Prologis leases its industrial and logistics buildings to more than 6,700 different customers worldwide.

No single customer accounts for more than 5% of annualized rent.

Average occupancy for the most recent quarter (Q1 FY 2024) was 96.8%.

By market cap, Prologis is the largest REIT in the world.

Before I begin, let’s get the obvious out of the way: There has been a lot of concern of late around commercial real estate, as rising interest rates and the work-from-home trend have conspired to hammer the values of certain commercial real estate properties.

However, much of this distress is concentrated in the office building category of CRE (especially among older office buildings in relatively poor locations).

Industrial properties, which is what Prologis owns and operates, are actually holding up just fine and performing quite well.

And there are two key reasons for this: criticality and cost.

Industrial properties, such as warehouses, are critical to the global supply chain.

$2.7 trillion in economic value of goods flow through the company’s distribution centers each year, representing 2.8% of the world’s GDP.

And yet, these centers form a low portion of total supply chain costs.

Per the 2022 CBRE Supply Chain Advisory, when looking at the distribution of supply chain costs, fixed costs (including rent) make up 3% to 6% of the total (versus 45% to 70% from transportation).

When something is both critical and low in cost, it’s highly likely to be “sticky” and retain demand, even as its pricing increases over time (because the costs, as a percentage of the total, remain low).

In addition, seeing as how the global supply chain is broadening out and modernizing after suffering major supply issues during the pandemic, the company’s worldwide fleet of distribution centers are set to become even more critical than before.

And with the secular trend of e-commerce becoming a larger part of the daily living experience for people all over the world, along with the fact that goods need to be more available and move faster than ever before, all of which increases demand for distribution centers, Prologis is in the driver’s seat.

This is why the REIT should continue to deliver higher revenue, profit, and dividends over the years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

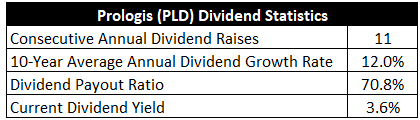

Already, Prologis has increased its dividend for 11 consecutive years.

The 10-year dividend growth rate is 12%.

That rate is strong, in and of itself, but it’s especially strong for a REIT.

Most REITs are income plays with low growth rates.

Seeing a 10%+ dividend growth rate from a REIT is rare and exceptional, and even the most recent dividend raise (announced in February) came in at over 10%.

On the flip side, this stock doesn’t offer the type of yield that can typically be had among REITs.

The yield is 3.6%.

The yield is 3.6%.

Not necessarily a REIT-like yield, but this is still a very attractive market-beating yield to pair with low-double-digit dividend growth.

Assuming a static valuation, the sum of yield and dividend growth should roughly approximate one’s total return.

So we can see how Prologis could be setting up investors for a double-digit annualized total return over the coming years.

Plus, this yield is 130 basis points higher than its own five-year average.

That’s a huge discrepancy.

And with a payout ratio of 70.8%, based on midpoint guidance for this year’s Core FFO/share, Prologis has a well-covered dividend that should continue to grow in line with the business.

There’s a lot to like about these dividend metrics – a sizable yield and double-digit dividend growth isn’t something you find every day.

Revenue and Earnings Growth

As much as there is to like, though, some of these numbers are looking in the past.

However, investors must always be looking toward the future, as today’s capital is risked for the tomorrow’s rewards.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful when it comes time to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should give us what we need to calculate where the business may be going from here.

Prologis advanced its revenue from $1.8 billion in FY 2014 to $8 billion in FY 2023.

That’s a compound annual growth rate of 18%.

Very impressive top-line growth from Prologis.

However, it’s also somewhat misleading.

First of all, Prologis acquired competing industrial REIT Duke Realty Corporation in 2022 for $26 billion, greatly increasing the size and revenue of the combined entity.

Furthermore, with REITs, it’s always imperative to look at profit growth on a per-share basis.

That’s because REITs use debt and equity to fund growth, as they’re legally required to distribute at least 90% of their taxable earnings to shareholders.

This circles back around to the point I made earlier on REITs typically being income plays, which is nice for those who prioritize income, but the limitations around internal funding for growth means tapping equity (by issuing shares) – resulting in dilution.

This structure can create wild distortions between absolute revenue growth and profit growth relative to shares outstanding.

Also, when assessing profit for a REIT, we want to use funds from operations instead of normal earnings.

FFO (or adjusted FFO) is a measure of cash generated by a REIT, which adds depreciation and amortization expenses back to earnings.

Prologis grew its Core FFO/share from $1.88 to $5.61 over this 10-year period, which is a CAGR of 12.9%

So that’s the truer indication of the company’s growth profile, and it’s still really quite impressive.

It also shows where that dividend growth came from – the 10-year dividend growth rate lines up nicely with the 10-year Core FFO/share CAGR.

Looking forward, CFRA currently has no three-year FFO/share CAGR projection.

That’s unfortunate, as I do like to compare the proven past up against a future forecast in order to roughly gauge what the growth trajectory might look like.

That said, CFRA does include this nugget:

“We see strong demand for [Prologis]’s logistics centers in key locations, with high barriers to entry given difficult-to-obtain zoning entitlements. We believe [Prologis]’s current land bank, with an estimated value creation potential of about $40 billion, is a key differentiator in these markets where land remains scarce. Pricing power should remain in most markets despite an influx of new supply, especially as difficult financing conditions result in slowing supply growth in 2024. We believe concerns around slowing e-commerce growth and a consumer shift toward services are excessive as many e-commerce and 3PL providers require more industrial space to meet current demand. [Prologis]’s best-in-class balance sheet with $5.9 billion of liquidity also provides the company plenty of flexibility moving forward.”

Really, that says it all.

Prologis is a best-in-class operator with numerous growth levers and ways to win.

It should also be noted that Prologis has two growth verticals that weren’t really present over the last decade.

First, the company is putting up solar energy installations on top of its buildings, which is a newer revenue driver.

Prologis is already ranked second in the US in terms of onsite solar installations and generation.

Second, Prologis is just now starting to build out its data center footprint.

From AI to e-commerce, Prologis is situated with, arguably, the very best global real estate portfolio in the world, and this portfolio is only becoming larger, broader, and more effective.

Now, the company is guiding for $5.42 in Core FFO/share, at the midpoint, for FY 2024.

So it’s a near-term step-down in growth, reflecting macroeconomic softness and a normalization of operations (after a very explosive but temporary period during the pandemic).

Prologis is starting off the next decade with a much larger portfolio, which offers resiliency and should allow investors to sleep well at night.

But this larger absolute size will likely make it more challenging for Prologis to grow as fast as it did before on a relative basis.

Is the added resiliency worth less growth?

I think a good case could be made that it is, but that’s up to the individual investor.

Overall, though, I don’t see why Prologis can’t or won’t grow at a high-single-digit rate from here.

While that would be a bit slower than what the business was able to do over the last decade, part of that period included an abnormal catalyst for growth (i.e., the pandemic, which fueled shopping from home).

This kind of growth rate would be more than enough to fuel like dividend growth and an appealing total return over the coming years (part of which comes from that sizable 3.6% yield).

It might not be the most exciting thing out there, but there could be good money to be made here for those who are patient and happy to collect a fat, growing dividend.

Financial Position

Moving over to the balance sheet, Prologis has a very solid financial position.

Prologis finished FY 2023 with $29 billion in long-term debt, which is less than 1/3 of its market cap.

A common measure for a REIT’s financial position is the debt/EBITDA ratio.

Prologis has a debt/adjusted EBITDA ratio of 4.6.

I usually see REITs range from 3 to 7 on this ratio, so Prologis is on the lower end.

The company’s weighted average interest rate on its share of total debt is only 3%, with a weighted average term of 9.1 years.

It’s worth noting that Prologis has no significant debt maturities until 2026.

In addition, the REIT has excellent credit ratings that are well into investment-grade territory: A3, Moody’s; A, S&P.

Overall, Prologis isn’t just the largest REIT in the world but also quite possibly the best.

And with economies of scale, switching costs, and entrenched infrastructure, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

A REIT’s capital structure relies on external funding for growth, which exposes the company to volatile capital markets (through equity issuances) and interest rates (through debt issuances).

Adding to the rate conversation, higher rates can hurt this particular business model twice over: Debt becomes more expensive to take on and service, and equity can also become more expensive (because income-sensitive investors have alternatives, which puts downward pressure on the stock price).

Prologis has exposure to the global economy, and any broad economic slowdown would naturally reduce demand for logistics (via less movement of goods).

The type of real estate Prologis specializes in (logistics/warehouses) is simplistic, and it’s not difficult for competitors to come in and build out warehouses on acquired land.

Being international, Prologis has exposure to currency exchange rates and geopolitics.

The company’s large size may start to introduce questions around the law of large numbers and limit its growth prospects.

Any major changes in commerce, especially e-commerce, would impact Prologis.

I see many risks that are standard for pretty much all REITs, even though Prologis is anything but standard.

And with the stock down more than 30% from all-time highs, the valuation is also anything but standard right now…

Valuation

The forward P/FFO ratio is 20.3, based on midpoint guidance for FY 2024 Core FFO/share.

That’s roughly analogous to a P/E ratio on a normal stock, and we can see an undemanding multiple for a best-in-class operator.

Another common multiple to use for valuing a REIT is the P/CF ratio, which tends to mirror the P/FFO ratio (because we’re looking at cash generation).

The stock’s P/CF ratio is 19.6.

To put the appeal of that perspective, its own five-year average P/CF ratio is 26.2.

And the yield, as noted earlier, is is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in 10% discount rate and a long-term dividend growth rate of 7%.

Depending on one’s viewpoint, that growth rate can look aggressive or demure.

On one hand, I rarely model in a higher rate of growth like this when dealing with a REIT.

REITs are usually income plays which are heavily indebted and grow slowly.

On the other hand, Prologis has proven itself capable of unusually fast growth for a REIT.

Also, the balance sheet isn’t as leveraged as what many other REITs are dealing with.

Keep in mind, this 7% mark is lower than the company’s demonstrated dividend growth over the last three, five, and ten years.

So I am assuming some kind of modest slowdown here, reflecting the company’s larger size (which can limit relative growth) but also offset a bit by the new growth verticals touched on earlier.

The DDM analysis gives me a fair value of $136.96.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I don’t think my valuation model was overly aggressive, yet the stock looks quite cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates PLD as a 4-star stock, with a fair value estimate of $120.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates PLD as a 4-star “BUY”, with a 12-month target price of $128.00.

I came out a tad high, but there’s a fairly tight grouping here. Averaging the three numbers out gives us a final valuation of $128.32, which would indicate the stock is possibly 14% undervalued.

Bottom line: Prologis Inc. (PLD) is a best-in-class operator with fundamentals that are second to none. Its massive portfolio of industrial properties is perfectly situated for multiple secular growth stories, including e-commerce, AI, and renewable energy. With a market-beating yield, double-digit dividend growth, a reasonable payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 14% undervalued, long-term dividend growth investors looking for exposure to resilient real estate should have a close eye on this clear winner.

Bottom line: Prologis Inc. (PLD) is a best-in-class operator with fundamentals that are second to none. Its massive portfolio of industrial properties is perfectly situated for multiple secular growth stories, including e-commerce, AI, and renewable energy. With a market-beating yield, double-digit dividend growth, a reasonable payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 14% undervalued, long-term dividend growth investors looking for exposure to resilient real estate should have a close eye on this clear winner.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is PLD’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 61. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, PLD’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long PLD.