I wish I didn’t have to write this column ever, let alone every couple of years. But this is ground we have to cover, like it or not: dividend stocks during war.

We invest in dividend stocks. There are wars and conflicts that affect our money. That’s reality.

Let’s start with last Saturday, while my daughter was in the middle of their monthly Girl Scouts meeting. I gulped at the headline on my phone: Drones heading towards Israel. Ugh.

So, on the drive to pick up my daughter, I flipped on the news in the Dadmobile. My sweety jumped into the car. Oops. Forgot I had the war on. I lunged for the volume and turned it all the way off. Good save?

Maybe I’m naïve. Surely they discuss world events at school, and this is a big one. My daughter knows there is a bad guy invading Ukraine. But kids are kids, so I returned to the events of daily life and asked about her troop’s latest project, interviewing residents of an assisted-living facility. Good stuff.

So, we’ll do the same here, my contrarian friend—return to daily life and why we’re here. You read this column to grow and protect your retirement portfolio. Onward, to income investments that rise during war.

Q: Should we buy oil?

In a word—no. At least, not now.

As contrarian investors, we want to buy energy stocks when oil is out of the headlines. Or, even better, the focus of negative attention.

Buying low and selling high is the name of the game. Oil is high today. Possible to sell even higher? Sure. But I prefer buying the black goo when it is in the bargain bin.

I’m talking ONEOK (OKE) in 2020, just two months after oil futures had dipped into negative territory. Remember that? Traders weren’t just giving away oil—they were paying people to take it!

Energy toll bridge OKE yielded 13% and traded for just four-times its peak earnings! If the world economy rebounded and profits bounced back, the stock was going to be a steal. And it sure was. OKE treated Contrarian Income Report readers to 183% total returns.

Blue-chip producer Exxon Mobil (XOM), meanwhile, was dirt cheap into 2021. At the time the company was borrowing money to pay its dividend. Not a good sign! Vanilla investors stayed away.

Here’s what they missed. Beneath the surface, a positive catalyst was bubbling: a rally in crude. In the oil patch, the cure for low prices is always low prices. The weaker producers are forced to cut production, which crimps supply and eventually leads to a price rebound.

XOM benefited from oil’s inevitable bounce. Profits rebounded. The stock’s dividend went from living on borrowed money to being well funded by cash flows. Brave XOM buyers enjoyed some sweet gains—CIR readers banked 111% returns in less than two years!

Fast forward to February 2022. The bad guy invaded Ukraine. We made blue and yellow cookies in our house and explained the situation to our children, and how fortunate we are to live in a country with friendly neighbors.

Mainstream investors, who hated oil in 2020 and 2021, decided that this was the time to pile into energy. They anticipated that sanctions and fewer Russian supplies would spike the price.

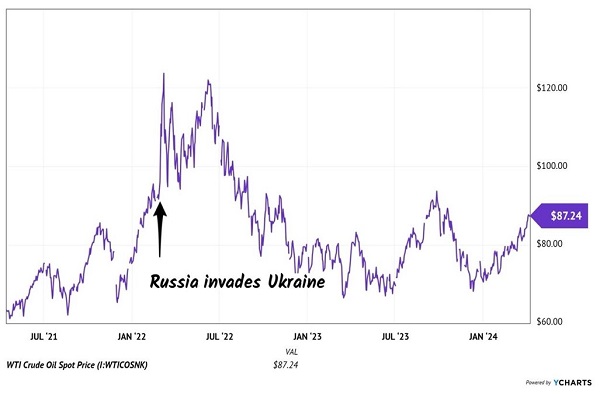

They were correct for about a month. After that, Texas tea topped and subsequently tanked. Six months after the invasion began, crude prices were lower.

March 2022 was not a good time to pile into energy. The rest of the planet was already in that trade. Oil prices popped shortly after Russia invaded Ukraine, but soon reversed course and plunged as traders realized supply concerns were overdone.

Oil Jumped, Then Sagged, After Russia Invaded Ukraine

I’m reading a similar bullish narrative for oil today. I’m also reading this everywhere. Which makes me cautious on crude.

I’m reading a similar bullish narrative for oil today. I’m also reading this everywhere. Which makes me cautious on crude.

How about natural gas stocks as a backdoor play? They have less froth for sure, with gas at multi-year lows.

But the optimal time to purchase natural gas companies was two months ago. We “backed up the truck” and bought Antero Midstream (AM) which has rallied 19% while EQT Corp (EQT) has forged ahead 14%.

Let’s be patient and not chase the energy sector on headlines. I’d rather buy the dips and, of the two energy options, natural gas has more near-term upside thanks to its current low prices.

Q: How about defense stocks?

It’s a bull market in military budgets, to put it lightly. NATO. Tensions in the Middle East. And, not to mention the Pacific.

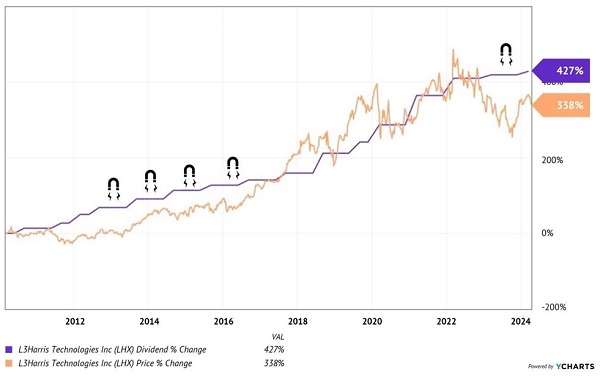

L3Harris Technologies (LHX) is a payer that may have you scratching your head because, on the surface, LHX never appears to yield much. It pays a modest 2.3% today.

However, LH constantly raises its dividend. Which, over time, pulls its price higher and higher (and higher). The purple dividend line below acts as a “magnet” that pulls this share price higher:

LHX’s “Dividend Magnet” Pulls Its Price Higher

And, you’ll notice, the dividend magnet is “due” to pull LHX higher once again. Its price is lagging its payout.

And, you’ll notice, the dividend magnet is “due” to pull LHX higher once again. Its price is lagging its payout.

LHX’s historical dividend growth is especially impressive given that most of this timeframe was geopolitically calm. With tensions on the rise, LHX will benefit from the inevitable increases in defense spending across the globe.

The current edition of L3Harris was formed on June 29, 2019, when L3 Technologies merged with the Harris Corporation. Their marriage created one of the world’s largest defense contractors with products for air, land, sea and even space applications.

LHX originally caught my attention when tensions increased in the Pacific. The defense firm makes what the US needs to compete with China militarily. For example, China now has the world’s largest navy, at least with respect to the number of ships. The US Navy has taken note and recently awarded LHX a contract worth $3.69 billion to supply advanced communications solutions for our Navy.

The company acquired Aerojet Rocketdyne, a leader in missile technology, last year. The “new” L3Harris is not only now a leader in missile defense, but also hypersonics (where the US reportedly lags Russia) and space (where the superpowers are jockeying for position). As we saw over the weekend, missile defense is crucial.

LHX shares trade for only 15-times forward earnings while management expects free cash flow to jump 40% by 2026. Cheap.

That’s not the only upside. If the dividend can deliver 427% gains during a mostly tranquil 14.5-year period, what is it going to do in the years ahead? Probably soar.

As if there isn’t enough to love about LHX, here’s another. Management has repurchased 7.3% of its outstanding shares over the past three years. A smart move while shares were cheap and a sign of confidence in the business.

I hate to paint a picture of more world conflict ahead. But, if it’s accurate, we want LHX in our portfolios.

— Brett Owens

Sponsored Link: LHX is is the kind of recession-resistant dividend we contrarians want to own in the rocky months ahead. Click here and Brett will explain how to find these types of 15%+ yearly total returns.

Source: Contrarian Outlook