Let’s talk about five dividends that are set to soar when the Federal Reserve cuts interest rates.

Not that these stocks need help. They are already in multi-year bull runs because they have the power of the “dividend magnet” on their side. This is a situation where dividend growth pulls a stock’s price higher and higher.

Let’s take coffee giant Starbucks (SBUX) as an example. Starbucks has beaten the S&P 500 by more than 300 percentage points since 2010. That’s also the year in which SBUX started paying dividends.

But it’s not just that Starbucks has clobbered the broader market. It’s the way in which the stock price and dividends have largely moved in tandem, with one seemingly pulling the other higher over time.

The “Attraction” Is Obvious

If it seems like shares are taking their cue from dividend hikes (or vice versa), well, that’s actually what’s happening. Dividend hikes entice more investors to snap up shares. But the shares also are being driven higher by underlying company growth, which helps SBUX afford additional dividend hikes over time.

If it seems like shares are taking their cue from dividend hikes (or vice versa), well, that’s actually what’s happening. Dividend hikes entice more investors to snap up shares. But the shares also are being driven higher by underlying company growth, which helps SBUX afford additional dividend hikes over time.

So where does the Fed come in?

As the U.S. central bank starts paring back interest rates, the yields on bonds and bond funds will broadly head lower. That’s a boon to just about any dividend stock, whose yield will look increasingly attractive as bond coupons shrink—but certainly for dividend raisers, whose payouts are actually growing at the same time debt yields are declining.

Consider yet another potential source of wind at the back for these five stocks that have posted red-hot dividend growth of 21% to 73% in the past year, and that are due to announce new dividend actions sometime within the next couple months.

The best time to consider these stocks is right now—before the broader investing herd comes running.

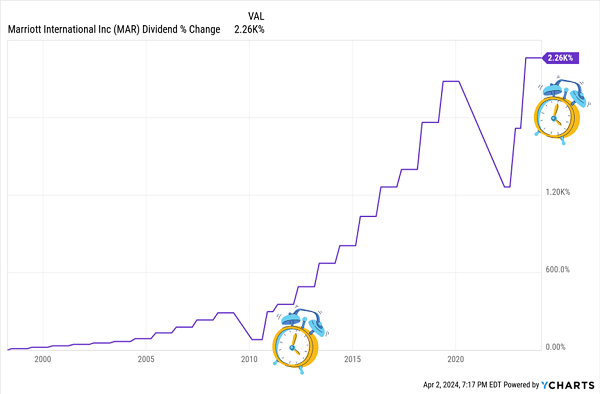

Marriott International (MAR)

Dividend Yield: 0.8%

2023 Increase(s): 73%

Projected Q2 Dividend Announcement: Mid-May

Marriott International (MAR) is an international hotelier whose roughly 8,700 properties—across dozens of brands, including Ritz-Carlton, St. Regis, Sheraton, Renaissance, MGM, Aloft, and the namesake Marriott—span 139 countries and territories.

Vanilla income investors sleep on Marriott’s sub-1% yield. Too bad for them, because this payout is popping.

A Little Lumpy, But the Direction Is Back Up to Snuff

Marriott’s dividend has been prone to the occasional stumble—during recessions. Each time it has subsequently rebounded in a big way.

Marriott’s dividend has been prone to the occasional stumble—during recessions. Each time it has subsequently rebounded in a big way.

Marriott was among the companies forced to suspend their dividends during COVID. It resumed payouts in 2022 at 63% of pre-COVID levels; then, in a pair of subsequent hikes, it pushed its payout beyond those old highs.

Marriott’s hotels have been roaring back to speed since COVID, showing particular strength overseas of late. Most recently, quarterly international RevPAR (revenue per available room, a vital hotel-industry operational metric) jumped 17% year-over-year, while comparable RevPAR improved by 7.5%.

That growth is important to future improvements in the dividend. While MAR’s current distribution accounts for less than a quarter of free cash flow, Marriott might be loath to stretch that ratio much more than that in the wake of its COVID suspension (and now that its quarterly dividend is back to “normal” levels). But we’ll likely get a better idea of how Marriott plans to manage its payout going forward sometime in mid-May, when it typically makes dividend-increase announcements.

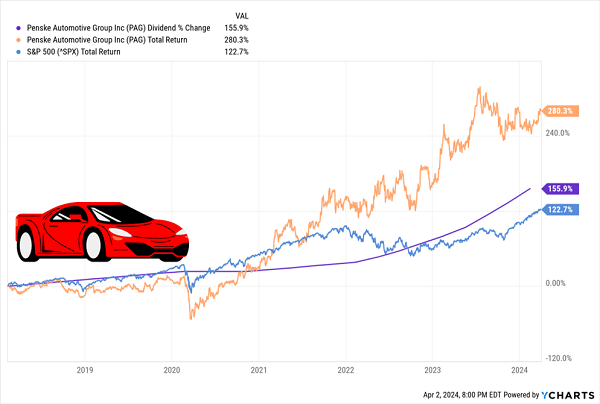

Penske Automotive Group (PAG)

Dividend Yield: 2.0%

2023 Increase(s): 32%

Projected Q2 Dividend Announcement: Mid-May

Let’s step back a few years for this next dividend grower.

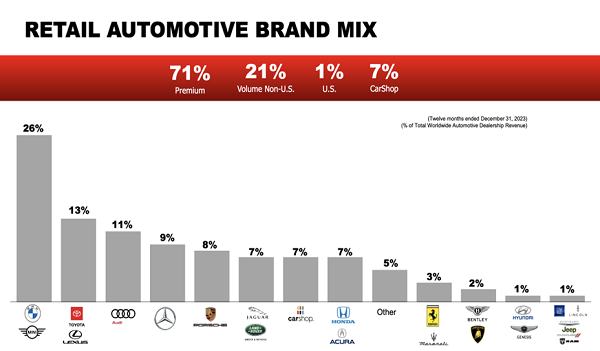

Penske Automotive Group (PAG) is an international automobile retailer that operates dealerships not just in the U.S., but also the U.K., Germany, Italy, Canada, and Japan. These dealerships cover just about every international brand under the sun.

Source: Penske Automotive Q4 2023 Earnings Presentation

Source: Penske Automotive Q4 2023 Earnings Presentation

It also boasts a thriving commercial-truck retail business across North America, and it distributes and retails commercial vehicles, power systems, engines, and more across Australia and New Zealand. In addition to all that, it owns roughly 29% of Penske Transportation Solutions, a North American transportation services, logistics, and supply-chain management services provider.

Back in 2017, I wrote about PAG as one of several attractive (and cheap!) dividend growers, and I said there was “no chance” of its dividend growth slowing down.

Accurate Prediction? Check.

What the chart doesn’t show is a two-quarter suspension of the dividend in 2020. But it resumed payouts the very same year at the same level as before, then immediately went back to raising as if nothing happened. So what you have is an almost uninterrupted run of quarterly dividend hikes going back more than a decade.

What the chart doesn’t show is a two-quarter suspension of the dividend in 2020. But it resumed payouts the very same year at the same level as before, then immediately went back to raising as if nothing happened. So what you have is an almost uninterrupted run of quarterly dividend hikes going back more than a decade.

Penske typically announces its Q2 raise sometime during mid-May. Its Q2 2023 payout was 32% higher than it was in 2022, and the dividend has improved another 32% since then.

But I will note that one thing has changed since that 2017 article: While cheap before, Penske is now trading well above its historical valuations.

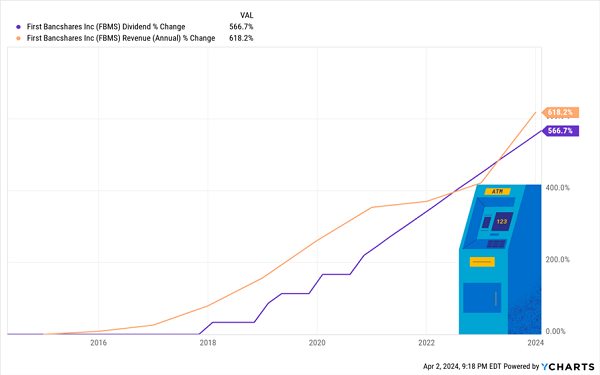

The First Bancshares (FBMS)

Dividend Yield: 3.8%

2023 Increase(s): 22%

Projected Q2 Dividend Announcement: Late May

The First Bancshares (FBMS) is the parent of The First Bank, which isn’t actually the first bank. But is a bank—one headquartered in Mississippi, with operations in Georgia, Alabama, Florida, and Louisiana as well. All told, it boasted nearly $8 billion in assets as of the end of 2023.

After years of remaining level, FBMS’s dividend got off the launchpad in 2018 in tandem with a massive expansion of the business, including a number of mergers and acquisitions for the likes of Heritage Southeast Bank, Beach Bank, and Southwest Georgia Bank.

First Bancshares Shares the Wealth With Investors

FMBS is another quarterly raiser—its Q2 2023 dividend was 22% higher year-over-year, and the payout has grown another 13% since then.

FMBS is another quarterly raiser—its Q2 2023 dividend was 22% higher year-over-year, and the payout has grown another 13% since then.

So, what will its next announcement—likely in late May—hold for investors?

First Bancshares is fresh off a new $50 million repurchase authorization and another penny-per-share quarterly raise, but also a big earnings miss and a weak net interest margin (NIM) guide. FBMS’s commitment to a relentless dividend upgrade schedule will definitely be tested.

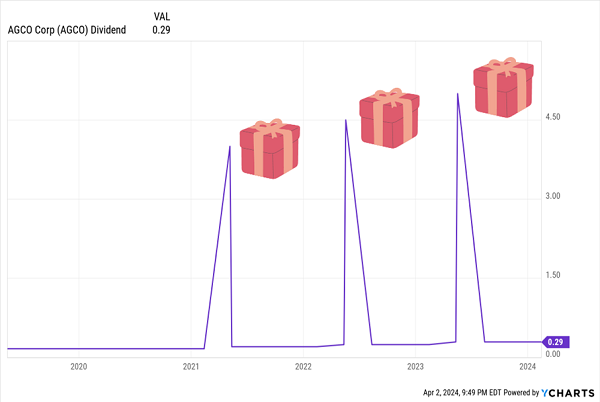

AGCO Corp. (AGCO)

Dividend Yield: 5.1%

2023 Increase(s): 21%

Projected Q2 Dividend Announcement: Late April

AGCO Corp. (AGCO) is a large agricultural machinery and equipment producer, with brands including Fendt, AGCO’s Grain & Protein, Massey Ferguson, Precision Planting and Valtra.

AGCO is coming off a couple of bumper years, and while the industry is thought to be entering a downcycle, AGCO’s recent 2024 guidance has been much more robust than feared. The company, for one, is leaning into an environment that should see more demand for parts and repairs than outright replacements.

But now, income investors are faced with two questions:

Will the dividend, which has rapidly grown from 16 cents per share in 2021 to 29 cents currently, reflect that slowdown?

And what about the special dividend, which makes up roughly 80% of the current stated yield?

AGCO’s Regular & Specials Have Been Blooming

If past is precedent, we’ll likely find out the answers to both in late April, which is when AGCO tends to make its dividend announcements.

If past is precedent, we’ll likely find out the answers to both in late April, which is when AGCO tends to make its dividend announcements.

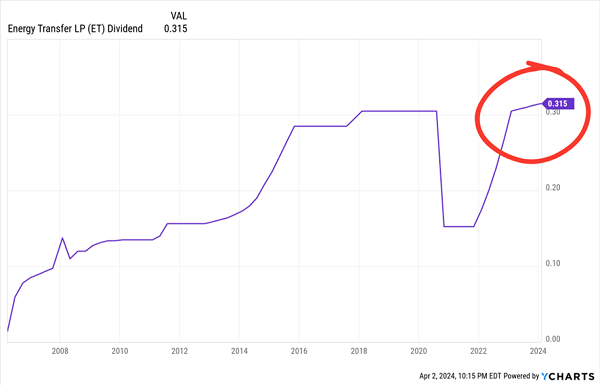

Energy Transfer (ET)

Dividend Yield: 8.0%

2023 Increase(s): 53.8%

Projected Q2 Dividend Announcement: Late April

Energy Transfer (ET) is responsible for 125,000 miles of America’s energy infrastructure—according to the company, some 30% of the country’s natural gas and 35% of its crude oil moves through its pipelines.

Following the COVID energy collapse, ET has been working on reducing leverage and making several large capital investments, including expanding its Nederland facility, building a new treating capacity in the Haynesville Shale, and closing on its acquisition of Crestwood Equity Partners. The top and bottom lines have snapped back, and the company is better poised to take advantage of rising U.S. production.

More importantly to income investors, ET doesn’t just offer a massive 8% yield—it’s a serial dividend raiser to boot. Its Q2 2023 payout was up 54% year-over-year (spread across four quarterly hikes).

But that’s largely ET playing catch-up after halving its payout during COVID. What the company has done since then makes me wonder whether a brisk pace of dividend growth is in the cards anymore.

Now That It’s Caught Up, Will ET Phone It In?

Since this time last year, the payout has only grown by a little more than 2%. Slower dividend growth is more forgivable when your yield is in high single digits, but ET shareholders and would-be buyers will still want to pay attention to pacing when the company announces its next dividend action—likely sometime in late April.

Since this time last year, the payout has only grown by a little more than 2%. Slower dividend growth is more forgivable when your yield is in high single digits, but ET shareholders and would-be buyers will still want to pay attention to pacing when the company announces its next dividend action—likely sometime in late April.

— Brett Owens

A Simple, Safe Way to Lock In 15% Yearly Returns … For Life! [sponsor]

The dividend growers above aren’t exactly perfect, but they’re still excellent examples of the right strategy—a simple but potent two-step recipe for success that has proven itself to investors again, and again, and again:

- Step 1: Buy aggressive dividend growers that are actually expanding their businesses, too.

- Step 2: That’s it! There is no Step 2! Just keep targeting elite dividend growers!

If you invest your money with corporate managers who both effectively deploy capital for growth and know how to reward shareholders, you will clobber the market on a regular basis—and better still, as the years roll on, more and more of those returns will come from cold, hard cash.

You can put this income-printing strategy to work today with a simple-to-manage, easy-to-understand group of just 7 specific tickers that are quietly handing investors a steady 15%, 17%, 21% or more every year—and growing income streams!

Better still, they’re trading at far more attractive prices—a value proposition that will further boost our price returns over time.

Your next move is simple: Buy now and set yourself up for annual returns of at least 15%. That’s far better than the market’s historical average, and it’s a level of return that would double your nest egg every five years!

You can get the full breakdown on each of these standout names within seconds. Click here to get my complete research: names, tickers, dividend histories and a full breakdown of their operations—everything you need to buy with confidence.

Source: Contrarian Outlook