A lot of people fear investing.

They think it’s “risky”.

I’d argue the risky thing to do is to not invest.

Over the long run, cash is almost guaranteed to lose money (to inflation).

Over the long run, high-quality businesses are almost guaranteed to make money.

It’s pretty clear to me which choice is the right one to make.

And when I think of high-quality businesses, my mind immediately goes to the dividend growth investing strategy.

This strategy advocates buying and holding shares in world-class businesses that pay safe, growing dividends to their shareholders.

You can find hundreds of examples by looking over the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I’ve been personally using this strategy to great effect for more than a decade.

I’ve been personally using this strategy to great effect for more than a decade.

It’s guided me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

Indeed, I’ve been in the extremely fortunate position of being able to live off of dividends since I decided to retire in my early 30s.

How did I do that?

My Early Retirement Blueprint spells it out.

Much of my success is owed to investing in the right businesses.

But investing at the right valuations has also been key.

See, it’s price that you pay, but it’s value that you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Investing isn’t as risky as it’s made out to be, and buying high-quality dividend growth stocks at attractive valuations only makes the venture that much less risky and more rewarding over the long run.

Of course, being able to spot attractive valuations means one is already versed in the valuation subject.

No worries.

My colleague Dave Van Knapp’s Lesson 11: Valuation, which is part and parcel of a larger series of “lessons” designed to teach dividend growth investing, lays out the concept of valuation in simple terms and even provides a valuation template that can be used to estimate the fair value of almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

WEC Energy Group Inc. (WEC)

WEC Energy Group Inc. (WEC)

WEC Energy Group Inc. (WEC) is an American energy company.

Founded in 1896, WEC Energy is now a $26 billion (by market cap) major power utility player.

WEC Energy provides electricity to 1.6 million customers across the states of Michigan and Wisconsin.

WEC Energy also provides natural gas to 3 million customers across the states of Illinois, Michigan, Minnesota, and Wisconsin.

The company does this by using 71,700 miles of electric distribution and transmission lines, 7,700 megawatts of power capacity, and 52,000 miles of natural gas distribution and transmission pipeline.

Electric supply mix for 2023 was: 37%, natural gas; 32%, coal; 22%, nuclear; and 9%, renewables.

I’ll note that WEC Energy plans to eliminate coal as an energy source by the end of 2032.

This is a large power utility business, which offers much to like and some things to not like.

The main aspect to like is the fact that what this business provides is a non-negotiable basic need.

The company has 4.6 million captive customers that effectively cannot live without power in a modern-day society.

There’s a lot of certainty, durability, and staying power in something like that, which explains why this company has been around for nearly 130 years.

Moreover, there’s almost always only one power provider in any one geographic area.

That’s a monopoly on something essential.

Put simply, it’s a business model that is nearly bulletproof.

So what’s not to like?

Well, because of how reliant people are on power, and because these are local monopolies, utilities are heavily regulated.

Regulation puts a profit ceiling on the business.

A local regulatory body will basically offer a reasonable return on investment but cap the possible upside beyond that by limiting what a utility can charge.

Fortunately, WEC Energy has been working with a favorable regulatory framework.

As Morningstar puts it: “Nearly 75% of earnings come from areas with constructive Wisconsin and Federal Energy Regulatory Commission regulation.”

This helps to explain why WEC Energy has been growing at a relatively fast clip for years (and faster than most other power utilities that I follow), which has helped to fuel faster-than-average dividend growth.

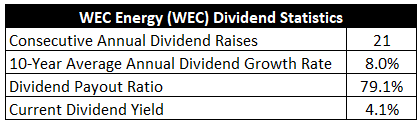

Dividend Growth, Growth Rate, Payout Ratio and Yield

Indeed, WEC Energy has increased its dividend for 21 consecutive years.

A multidecade track record of consistent, yearly dividend increases is always nice to see.

The 10-year dividend growth rate is 8%.

That really stands out for a power utility, as most of the power utilities that I know of offer much lower dividend growth rates (often in a low-single-digit range).

Super impressive growth here, and even the most recent dividend raise came in at over 7%.

Meantime, the stock still offers a utility-like yield of 4.1%.

Meantime, the stock still offers a utility-like yield of 4.1%.

A rare best-of-both-worlds scenario for a power utility.

This market-beating yield, by the way, is 120 basis points higher than its own five-year average.

The market usually assigns a much lower yield to this stock (its five-year average is below 3%), and that’s exactly where the opportunity could be.

With a payout ratio of 79.1% – elevated but not uncommonly so for a power utility – the dividend should continue to grow at a rate that roughly matches business growth.

I’m not a big fan of power utilities for my own portfolio, and a general lack of growth is only one reason why, but WEC Energy clearly bucks the anemic growth trend.

This uncommonly strong combination of yield and growth is very enticing.

Revenue and Earnings Growth

As enticing as this combination may be, though, many of the dividend metrics are based on the past.

However, investors must always be looking toward the future, as the capital of today gets risked for the rewards of tomorrow.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be very handy when the time comes to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this way should give us what we need to roughly gauge where the business might be going from here.

WEC Energy increased its revenue from $5 billion in FY 2014 to $8.9 billion in FY 2023.

That’s a compound annual growth rate of 6.6%.

This is very, very good top-line growth from a large power utility.

Meanwhile, earnings per share grew from $2.59 to $4.63 (adjusted) over this 10-year period, which is a CAGR of 6.7%.

I’m using adjusted EPS for FY 2023 only because there was a large non-cash charge related to previous capital investments which were disallowed by the Illinois regulatory body.

This one-time, non-cash charge unfairly skews GAAP EPS for FY 2023, and so I’m trying to show a more accurate growth profile of the business.

While this growth is nothing to sneeze at for a power utility, it’s where the first crack shows.

We can see that EPS growth has not fully kept up with dividend growth over the last decade, which explains why the payout ratio is slightly elevated – an expansion of the payout ratio has driven excess dividend growth.

I don’t necessarily find mid-single-digit growth disappointing for this kind of business – if you want fast growth, you’re in the wrong place – but the higher 10-year dividend growth rate might mislead investors who only look at the surface.

WEC Energy’s most recent dividend raise of 7.1%, which is closer to business growth, is probably a better number to base one’s future expectations upon.

Looking forward, CFRA is projecting that WEC Energy will compound its EPS at an annual rate of 7% over the next three years.

CFRA is basically assuming a continuation of the status quo.

WEC Energy has been growing the business at nearly 7% annually over the last decade, and I don’t see anything to indicate a major change on the horizon.

CFRA succinctly lays out the trade-offs with this passage: “We expect margin growth from higher electric & gas rates, returns on capital investments, and falling operations and maintenance costs as [WEC Energy] carries out coal plant retirements in Wisconsin. Offsetting these trends, we note the somewhat weak sales growth outlook and the challenging rate case outcome in Illinois.”

Adding to this, CFRA states: “On a compounded annual basis, we expect EPS growth between 6.5%-7.0% between 2023- 2026, competitive with peers. We think EPS growth will be driven by customer growth, equity earnings from the ATC (electric transmission) subsidiary as it completes new projects, and rate increases as [WEC Energy] carries out its capital spending program.”

I’ll note that WEC Energy is guiding for long-term EPS growth of 6.5% to 7%, so CFRA’s number is right in line.

To this end, WEC Energy has a plan to invest $7 billion in regulated renewables from 2024 to 2028, quadrupling its generation here, and the business should earn a satisfactory return on these investments.

In addition, data centers have been coming to key markets, including SE Wisconsin.

Since data centers tend to consume a lot of power, this should bode well for WEC Energy.

Overall, we’ve got an easy-to-understand power utility business growing its revenue, EPS, and dividend at approximately 7% annually.

And you get a 4%+ yield to start off with.

Assuming no major changes to the valuation, that can get one to a 10%+ annualized total return.

I find it hard to complain too much about any of this.

Although I can certainly understand (and sympathize with) the investors out there who simply want much more growth, these numbers are actually pretty strong for this kind of business and offer a lot to like for investors who do lean a bit more toward current income.

Financial Position

Moving over to the balance sheet, WEC Energy has a relatively good financial position.

Now, power utilities, in general, have heavily leveraged balance sheets.

Because investments are implicitly backed by a reasonable returns from regulators, there’s almost an incentive here to take on debt and fund growth projects.

The long-term debt/equity ratio is 1.3, while the interest coverage ratio is slightly over 3.

Great metrics?

No.

However, for this kind of business, these are commonplace numbers.

To be honest, industrywide debt is one of the other reasons why I’m not a huge fan of utilities, but WEC Energy does not have a dangerous balance sheet by any stretch of the imagination.

Profitability is in a similar boat – good but not outstanding.

Return on equity has averaged 11.8% over the last five years, while net margin has averaged 15.3%.

Overall, WEC Energy appears to be running an above-average power utility business selling something its customers basically cannot live without.

And with economies of scale, a geographic monopoly, and a constructive regulatory structure that just about guarantees some level of profit, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Regulation is a double-edged sword.

Regulators allow for utilities to make a reasonable profit, where profit scales with costs, putting a profit floor in place.

On the flip side, because electricity is necessary and there’s often only one power provider in any one geographic area, regulators install a profit ceiling by limiting the rates a utility can charge.

This is a rare industry in which competition at a local level doesn’t exist, as WEC Energy runs local monopolies across its territory.

A key possible risk is a future in which customers become competitors by generating and storing power at the site of consumption (via solar).

Like all power utilities, WEC Energy is captive to the evolving regulatory structure and population growth of its service territories.

Elevated interest rates pressure the levered balance sheet.

The company is exposed to volatile input costs around natural gas, and there’s a risk that natural gas could be phased out in the future.

There’s nuclear risk here, and renewables do not yet have a lengthy track record of attractive economics.

Overall, I see many of these risks as pretty standard for this kind of business model, even though WEC Energy is, in some ways, an above-average operator.

In addition, the valuation is well below average…

Valuation

The stock is trading hands for a P/E ratio of 19.3.

While that isn’t necessarily low in absolute terms, it does compare quite favorably to its own five-year average of 22.9.

It’s also below where the broader market is at.

The sales multiple of 2.9 is lower than its own five-year average of 3.5.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 6.5%.

This 6.5% number very closely lines up with WEC Energy’s revenue and EPS growth over the last decade.

It’s also at the low end of WEC Energy’s own near-term EPS growth guidance.

CFRA’s forecast, as shared earlier, is slightly above this level.

The most recent dividend raise was only barely above this level.

I think it’s fair to say that WEC Energy is growing its revenue, profit, and dividend at somewhere around 7% annually, but I’d really rather err on the side of caution, and that explains why I’m dialing the expectations back just a skosh.

The DDM analysis gives me a fair value of $101.63.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I don’t see anything overly aggressive about my valuation, yet the stock comes out looking quite cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates WEC as a 4-star stock, with a fair value estimate of $96.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates WEC as a 3-star “HOLD”, with a 12-month target price of $86.00.

I came out a bit high, but we all see some appeal here. Averaging the three numbers out gives us a final valuation of $94.54, which would indicate the stock is possibly 14% undervalued.

Bottom line: WEC Energy Group Inc. (WEC) is an above-average power utility enterprise, offering relatively high growth and a constructive regulatory backdrop. With local monopolies selling something its customers can’t really live without, long-term prosperity and profitability is nearly certain. With a market-smashing yield, high-single-digit dividend growth, a reasonable payout ratio, more than 20 consecutive years of dividend increases, and the potential that shares are 14% undervalued, dividend growth investors aiming to increase their utility exposure have a prime prospect on their hands.

Bottom line: WEC Energy Group Inc. (WEC) is an above-average power utility enterprise, offering relatively high growth and a constructive regulatory backdrop. With local monopolies selling something its customers can’t really live without, long-term prosperity and profitability is nearly certain. With a market-smashing yield, high-single-digit dividend growth, a reasonable payout ratio, more than 20 consecutive years of dividend increases, and the potential that shares are 14% undervalued, dividend growth investors aiming to increase their utility exposure have a prime prospect on their hands.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is WEC’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 87. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, WEC’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long WEC.