There are a lot of ways to make money in this life.

But most of those ways require effort on one’s part.

Fair enough.

If you wish to receive, it makes sense to expect to give.

However, it isn’t always like this.

No, it is possible to make money without any effort at all.

One of the best ways to accomplish this is by way of collecting dividends.

And not just dividends but steadily rising dividends.

And not just dividends but steadily rising dividends.

Yep.

Sit back and collect ever-more passive dividend income while you go about your life.

Sounds like a dream.

But it’s more reality than you might think.

It can be as simple as instituting the dividend growth investing strategy.

This strategy advocates buying and holding shares in world-class businesses that pay safe, growing dividends to shareholders.

You can discover many examples by taking a look at the Dividend Champions, Contenders, and Challengers list.

That list has data on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I instituted this strategy for myself more than a decade ago.

What’s it done for me?

Well, it’s guided me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

To that point, this strategy also helped me to retire in my early 30s.

To that point, this strategy also helped me to retire in my early 30s.

My Early Retirement Blueprint delves into the ins and outs of how I did that.

A pillar of my success has been investing in the right businesses.

But another crucial factor has been investing at the right valuations.

Price only represents what you pay, but value represents what you actually get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Letting the dividend growth investing strategy guide you as you buy high-quality dividend growth stocks when they’re undervalued can allow you to bypass the typical work-for-income paradigm, collet ever-rising passive dividend income, and even possibly achieve financial independence over time.

Now, the whole concept of valuation seems super difficult, but it’s actually not.

My colleague Dave Van Knapp put together Lesson 11: Valuation in order to demystify and simplify things.

Part and parcel of an overarching series of “lessons” designed to teach the dividend growth investing strategy, it lays out a valuation template that can be used to quickly estimate the fair value of almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Realty Income Corp. (O)

Realty Income Corp. (O)

Realty Income Corp. (O) is a real estate investment trust that primarily leases freestanding, single tenant, triple-net-leased retail properties.

Founded in 1969, it’s now a $45 billion (by market cap) real estate monster that employs approximately 400 people.

The company’s property portfolio of over 13,000 properties is diversified across the US, Puerto Rico, Spain, Italy, and the UK.

The company serves more than 1,300 clients operating across 86 different industries.

The property portfolio has an occupancy rate of nearly 99%.

Slightly more than 80% of the properties are retail in nature, while the remainder is mostly industrial.

Realty Income is incredibly diversified, with no one tenant comprising more than 4% of annualized contractual rent.

Real estate is great.

Real estate has inherent supply/demand attributes that are very favorable and appealing.

Like the old saying about land goes: “They’re not making it anymore.”

Thus, supply for real estate (because it has to be built somewhere) is somewhat finite.

Meanwhile, real estate has built-in demand from the need to live in and interact with the physical world.

Commercial real estate takes this favorable supply/demand setup a step further by erecting profitable properties on tracts of prized land.

If one can build or buy a well-located property of some type and then rent it out to a suitable tenant, you have a cash cow on your hands.

Mastering the formula by multiplying this over and over again leads to the amassing of a large and diversified portfolio of individual cash cows.

That’s precisely what Realty Income has done.

All that said, real estate can be not so great in some ways.

It’s difficult, expensive, and time consuming to acquire real estate on your own.

Becoming your own landlord involves scouting, studying comps, lining up financing, leverage, closing, finding tenants, managing property, and so on.

And that’s just the start… with one property.

That’s before getting into how difficult it is to scale this kind of thing by yourself.

Well, this is exactly where a real estate investment trust like Realty Income enters.

Buying shares in Realty Income means you instantly own a slice of a portfolio of thousands of commercial properties that already have paying tenants installed.

You become a scaled-up landlord at that very moment… without doing any of the heavy lifting yourself.

It should go without saying how appealing this idea is.

Also, no ongoing hassles from tenants – Realty Income takes care of it.

What’s especially powerful about Realty Income’s business model is the nature of a commercial triple-net lease – a lease agreement on a property in which the tenant agrees to pay all of the expenses of the property, including real estate taxes, building insurance, and maintenance.

This minimizes Realty Income’s overhead.

Furthermore, Realty Income leases its properties to some of the most successful tenants a landlord could hope for.

Realty Income’s top 20 tenants include the likes of FedEx Corporation (FDX)and Tractor Supply Co. (TSCO).

Most of the company’s commercial real estate is designed for everyday retail – convenience, grocery, and home improvement stores are prime examples.

But the 2022 $1.7 billion sale-leaseback agreement of Encore Boston Harbor Resort and Casino catapulted the REIT into the gaming space, opening up a whole new world of opportunities.

Seeing as how there are many types of commercial real estate across a vast landscape, Realty Income should have plenty more opportunities for growth and expansion.

It’s the diversification across tenants, industries, and geographies – while maintaining a certain degree of quality – that positions Realty Income and its shareholders for continued success in commercial real estate.

With that, revenue, profit, and the dividend should continue to rise for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

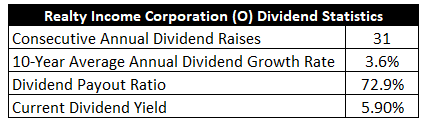

Already, Realty Income has increased its dividend for 31 consecutive years.

This makes Realty Income one of the only REITs in the world that is a Dividend Aristocrat.

Because of constant equity and debt issuances, as well as the cyclicality of real estate, it’s somewhat difficult for a REIT to attain this level of dividend growth consistency.

For perspective, this track record dates all the way back to Realty Income’s 1994 IPO.

Realty Income actually lays all of this out in its official mission: “To invest in people and places to deliver dependable monthly dividends that increase over time.”

Just goes to show how uncommonly great Realty Income has been – and how long it’s been uncommonly great for.

The 10-year dividend growth rate is only 3.6%.

And that’s the rub.

And that’s the rub.

A prospective investor has to accept that this is a slow-growth income vehicle.

To that point, Realty Income does this well.

The stock yields 5.9%.

That’s far higher than what the broader market offers.

It’s also 150 basis points higher than its own five-year average.

Plenty of yield.

Better yet, Realty Income pays this dividend monthly.

Realty Income takes its monthly dividend commitment to shareholders so seriously, it has trademarked its moniker: The Monthly Dividend Company®.

So that’s a fat dividend check – and one that’s consistently getting fatter – coming in every single month.

With a payout ratio of 72.9%, based on midpoint guidance for this year’s FFO/share, the monthly dividend appears to be as healthy as ever and primed for more low-single-digit growth.

For income-oriented dividend growth investors who desire, or depend on, large monthly dividend payments to reliably roll in, Realty Income has been, and remains, one of the better choices out there.

These dividend metrics are really appealing for that kind of investor cohort.

Revenue and Earnings Growth

As appealing as the dividend metrics might look, though, many of the numbers are looking backward.

However, investors must always be looking forward, as today’s capital gets risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be extremely useful when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this manner should give us what we need to make an informed judgment on where the business may be going from here.

Realty Income moved its revenue from $934 million in FY 2014 to $4.1 billion in FY 2023.

That’s a compound annual growth rate of 17.9%.

An incredible rate of top-line growth here.

However, it’s also misleading.

First of all, Realty Income merged with former competitor VEREIT in 2021, and this move substantially increased revenue in an immediate way.

Second, REITs fund growth via debt and equity issuances.

With a REIT, you must look at profit growth on a per-share basis.

And when assessing profit for a REIT, it’s imperative to use funds from operations (or adjusted funds from operations) instead of normal earnings.

FFO is a measure of cash generated by a REIT, which adds depreciation and amortization expenses back to earnings.

Realty Income grew its FFO/share from $2.58 to $4.07 over this period, which is a CAGR of 5.2%.

This is the much more accurate measure of Realty Income’s growth profile.

A tripling of shares outstanding acted as a pretty serious headwind for relative bottom-line growth.

While it’s obviously nowhere near the absolute top-line growth, it’s still very solid for a REIT.

Looking forward, CFRA currently has no three-year forecast for Realty Income’s FFO/share CAGR.

This is disappointing, as I do like to compare the proven past with a future forecast.

However, CFRA does shower Realty Income with praise: “We see robust demand continuing for freestanding retail space, driven by a favorable supply/demand environment. We believe [Realty Income] is poised to remain resilient in a more uncertain operating environment, given its top tenants are concentrated in industries deemed essential, such as convenience, drug, dollar, quick service restaurants, and grocery stores. [Realty Income’s] tenant diversification is also strong with its top 20 clients accounting for 40.2% of annualized rent in Q4 2023.”

My take?

Shareholders should expect more of the same.

And that’s just fine.

Indeed, we can glean quite a bit from Realty Income’s own guidance.

The REIT is guiding for $4.23 in FFO/share, at the midpoint, for FY 2024.

This would represent nearly 4% YOY growth.

That’s where we’re at with this REIT.

If an investor is okay with a ~6% yield and ~4% growth – and a lot of investors are – Realty Income is probably right up your alley.

I’ll note that Realty Income has been making interesting moves in order to drive growth and protect the enterprise, including the aforementioned VEREIT merger that created a larger, more resilient retail-focused REIT.

Realty Income also smartly spun off its office space properties in 2021, as part of the VEREIT transaction.

More recently, there was the sale-leaseback maneuver that got Realty Income into the gaming space, which I touched on earlier.

As long as Realty Income can continue to grow FFO/share at a low-single-digit rate, and it looks like they are able to do that, the dividend should continue to grow at a similar rate.

Assuming no serious multiple contraction, that sets up investors for a ~10% annualized total return (6% + 4%) – with much of it coming in the form of a large, monthly dividend.

I think a lot of investors who are older and/or partial to income will be perfectly satisfied with this, although those seeking more growth will have to look elsewhere and/or limit the exposure.

Financial Position

Moving over to the balance sheet, Realty Income has a solid financial position.

The company has $57.8 billion in total assets against $24.7 billion in total liabilities.

Realty Income’s credit ratings are well into investment-grade territory: A3, Moody’s; A-, S&P Global.

In addition, many of Realty Income’s top tenants have their own investment-grade credit ratings.

A common measure for a REIT’s financial position is the debt/EBITDA ratio, which usually ranges from 3 to 7 across most of the REITs I’ve come across.

Realty Income finished last fiscal year with a net debt/pro forma adjusted EBITDAre ratio of 5.5.

So Realty Income is somewhere in the middle on this one.

This company is doing what works in commercial real estate.

It’s combined triple-net leases with a diversified roster of top tenants, and this simplistic approach has led to one of the best long-term track records in its space.

And with deep industry expertise, long-term contracts, and massive scale, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Real estate demand is cyclical, and the financial health of Realty Income’s tenants could sour in a prolonged recession.

A REIT’s capital structure relies on external funding for growth, which exposes the company to volatile capital markets and interest rates.

Elevated interest rates, which are currently present, can hurt the company twice over: Debt becomes more expensive, and equity can also become more expensive (because income-sensitive investors have alternatives, which can reduce demand for and pricing on the stock).

A recession can also hurt the company twice over: Demand for commercial real estate can cool, and equity issuances after a presumed drop in the stock’s price would come at a higher cost.

Realty Income is heavily tied to retail, and retail has headwinds coming from e-commerce and theft.

The company’s scale is an advantage, but it also introduces questions around growth and the law of large numbers.

I see considerable risk to think over, but the quality and track record of Realty Income should also be thought over.

And the valuation, which currently looks attractive, has to be top of mind…

Valuation

The stock has a P/FFO ratio of 13.2.

That’s somewhat analogous to a P/E ratio on a normal stock, and it clearly indicates how undemanding the valuation is in absolute terms.

But it looks cheap in relative terms, too.

The cash flow multiple of 13 is well off of its own five-year average of 17.7.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 4%.

If you’ve been following along, an expectation of low-single-digit dividend growth from here is an obvious one.

This is pretty close to the 10-year dividend growth rate, and it’s also close to Realty Income’s demonstrated FFO/share growth over the last decade.

The company is guiding for ~4% FFO/share growth this year, and the dividend should grow at a similar rate to that.

This is basically where everything is pointing to.

It’s roughly where Realty Income is at right now.

This kind of growth should stay slightly ahead of inflation and inch one’s purchasing power forward, and that’s probably good enough for most income-oriented investors out there.

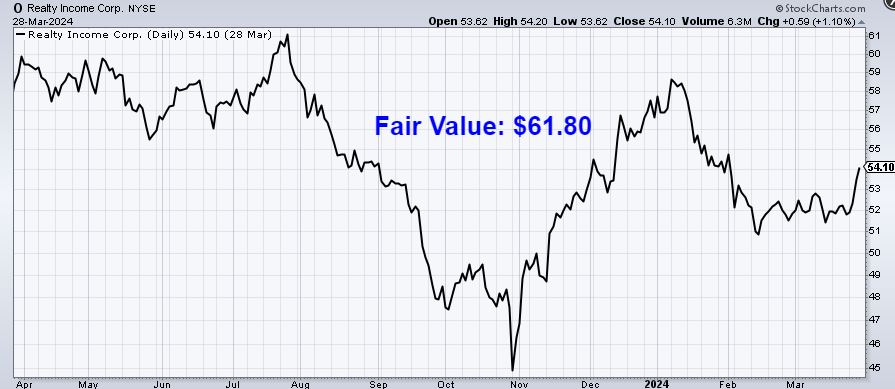

The DDM analysis gives me a fair value of $53.39.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

My valuation shows a stock that’s, at worse, fairly valued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates O as a 5-star stock, with a fair value estimate of $76.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates O as a 3-star “HOLD”, with a 12-month target price of $56.00.

I came out low, although Morningstar, which seemingly tends to show bias toward optical cheapness and high yield in its analyses, looks awfully high on this one. Averaging the three numbers out gives us a final valuation of $61.80, which would indicate the stock is possibly 13% undervalued.

Bottom line: Realty Income Corp. (O) is a high-quality REIT that has shown resilient staying power for decades, and its diversified roster of top-tier tenants should ensure a continuation of this. The REIT has an uncommon level of consistency and commitment when it comes to its large dividend – a dividend which is paid monthly. I really can’t think of a company that has a more sacrosanct dividend than this one. With a market-smashing yield, low-single-digit dividend growth, a reasonable payout ratio, more than 30 consecutive years of dividend increases, and the potential that shares are 13% undervalued, this Dividend Aristocrat could be a top long-term investment idea for income-oriented dividend growth investors.

Bottom line: Realty Income Corp. (O) is a high-quality REIT that has shown resilient staying power for decades, and its diversified roster of top-tier tenants should ensure a continuation of this. The REIT has an uncommon level of consistency and commitment when it comes to its large dividend – a dividend which is paid monthly. I really can’t think of a company that has a more sacrosanct dividend than this one. With a market-smashing yield, low-single-digit dividend growth, a reasonable payout ratio, more than 30 consecutive years of dividend increases, and the potential that shares are 13% undervalued, this Dividend Aristocrat could be a top long-term investment idea for income-oriented dividend growth investors.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is O’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 80. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, O’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Disclosure: I’m long O.

Source: Dividends & Income