Why do we invest?

What’s the point of it all?

There are probably as many different answers as there are investors out there, but I think one common reason unites us all.

Financial independence.

Yes, almost every single investor out there wants to achieve financial independence.

This is where you can go and do what you want, when you want, where you want, with whom you want.

It’s ultimate freedom.

It’s ultimate freedom.

The cool thing is, it isn’t crazy difficult to achieve it.

But one does need to live below their means and intelligently invest their capital.

Importantly, income from investments must be generated.

Well, that’s where dividend growth investing comes in.

This is a strategy whereby one buys and holds shares in world-class businesses that pay safe, growing dividends to shareholders.

Once you have enough safe, growing dividend income to live off of – voila!

You can find hundreds of businesses that pay safe, growing dividends by perusing the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I’ve used this strategy for myself for more than a decade now, allowing it to guide me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

I’ve been financially independent for a number of years now, and I even retired in my early 30s.

I’ve been financially independent for a number of years now, and I even retired in my early 30s.

My Early Retirement Blueprint shares the details on how all of that played out for me.

Living below my means and investing my capital into great businesses that pay safe, growing dividends did a lot of the heavy lifting.

But that’s not all.

Valuation at the time of investment has also been critical.

Whereas price is simply what you pay, value is what you actually get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Achieving the ultimate outcome of investing – financial independence – can be as simple as living below your means and buying high-quality dividend growth stocks when they’re undervalued.

Of course, being able to spot possible undervaluation means one has a mental framework around the concept of valuation already built up.

That’s exactly where Lesson 11: Valuation comes in.

Penned by my colleague Dave Van Knapp, it provides an easy-to-follow valuation template that can be applied to just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

UnitedHealth Group Inc. (UNH)

UnitedHealth Group Inc. (UNH)

UnitedHealth Group Inc. (UNH) is a managed healthcare firm that provides health insurance, pharmacy benefit management, and care delivery to millions of clients.

Founded in 1974, UnitedHealth is now a $439 billion (by market cap) healthcare behemoth that employs approximately 440,000 people.

The company reports results across two primary business segments: UnitedHealthcare, 55% of FY 2023 revenue; and Optum, 45%.

UnitedHealthcare primarily provides risk-based, fee-based health insurance (via UnitedHealth) to more than 50 million people globally.

There’s immense value in this service, as forgoing health insurance can lead to financial ruin in the event that a major health issue crops up (especially in the US).

This service gives a client access to cost-effective health services within a specified network of care.

Also, UnitedHealthcare provides supplemental Medicare insurance to seniors, as well as Medicaid management services for state governments.

Optum is largely comprised of the conglomerate’s pharmacy benefit manager, OptumRx.

The PBM engages in drug price negotiation, the establishing of drug formularies, pharmacy network creation, and drug claim processing.

Optum, via the OptumHealth arm, also provides healthcare services to patients through networks of outpatient facilities.

As you can see, UnitedHealth is about as “vertically integrated” as this business model can possibly get, managing upstream clients on the insurance side and downstream clients on the healthcare side.

This is an incredibly powerful setup, where each side of the business complements and reinforces the other.

Morningstar touches on this: “Under one roof, UnitedHealth combines a top-tier health insurer (UnitedHealthcare), pharmacy benefit manager (Optum Rx), provider (Optum Health), and health analytics franchise (Optum Insight). The company’s integrated strategy has resulted in some of the best returns in the industry in recent years…”

Morningstar then adds: “By providing those diverse yet connected services, UnitedHealth aims to grow in nearly any regulatory environment. It is shooting for 13%-16% annual earnings growth in the long run, including strong operational growth and capital allocation activities, such as acquisitions and repurchases. While some regulatory scenarios could eventually cut into that mission, we suspect the value that UnitedHealth provides to the U.S. healthcare system will help it remain relevant in the long run.”

Seeing as how the US healthcare complex is, well, extremely complex (and nearly unaffordable without insurance), having health insurance and access to an associated care network is almost a necessity.

Not only that, but once a person has health insurance and is established in a network, that service is very “sticky” – particularly if it’s through an employer (where a change will likely only occur if one leaves that job).

This locks clients into both the insurance and the care.

And, due to prevailing demographic trends, that client pool is growing larger, older, and wealthier (on average) – all of which put upward pressure on demand for quality healthcare (and the insurance to affordably access it).

If all of that weren’t already compelling enough, UnitedHealth reaps the massive rewards of the hidden genius behind the insurance business model.

Because of the time delay between receiving money for premiums and paying out on claims, an insurance company builds up what’s known as a “float” – the sum of capital that accrues over time because of this delay.

It’s a built-in virtue.

UnitedHealth ended last fiscal year with $75.2 billion in cash, cash equivalent, available-for-sale debt securities, and equity securities balances – a humongous pile of capital that earns a healthy, sweat-free, low-risk profit for the business.

Simply put, UnitedHealth has many ways to win, and its vertical integration across the healthcare value chain has created a business that is close to unassailable.

It’s hard to imagine any future in which UnitedHealth doesn’t do very well and grow its revenue, profit, and dividend at high rates.

Dividend Growth, Growth Rate, Payout Ratio and Yield

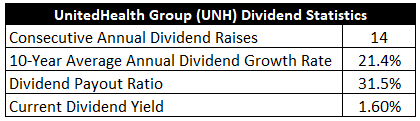

Already, UnitedHealth has increased its dividend for 14 consecutive years.

The 10-year dividend growth rate is 21.4%, which is incredible – especially for a company of this size.

While recent dividend raises have been smaller, UnitedHealth has been a lock for double-digit dividend raises.

In fact, the most recent dividend raise was nearly 14%.

In fact, the most recent dividend raise was nearly 14%.

For such a large and mature conglomerate, it’s very impressive to see this.

On the other hand, the stock’s 1.6% yield means that high growth is required in order to make sense of the investment.

This one does lean a bit more toward growth than income, and that’s totally fine by me.

I will point out, though, that this yield is 20 basis points higher than its own five-year average.

With a payout ratio of only 31.5%, I suspect shareholders will be receiving many more double-digit dividend raises over the years to come.

For investors who prefer long-term growth and compounding over the immediate gratification of high yield, there’s a lot to like here.

Revenue and Earnings Growth

As much as there is to like, though, these metrics are largely looking backward.

However, investors must always be looking forward, as today’s capital is being risked for tomorrow’s rewards.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this manner should give us what we need to make an informed determination of where the business may be going from here.

UnitedHealth increased its revenue from $130.5 billion in FY 2014 to $371.6 billion in FY 2023.

That’s a compound annual growth rate of 12.3%.

Very strong top-line growth here.

I usually like to see a mid-single-digit top-line growth rate from a mature business like this, but UnitedHealth is knocking it out of the park.

Meanwhile, earnings per share grew from $5.70 to $23.86 over this period, which is a CAGR of 17.2%.

Even better.

It is so difficult for a company of this size and scale to cook like this.

It’s hard to overstate how wowed I am.

A combination of margin expansion and share buybacks helped to drive that excess bottom-line growth.

For perspective on the latter, the outstanding share count has been reduced by approximately 5% over the last decade.

Looking forward, CFRA is forecasting a 14% CAGR for UnitedHealth’s EPS over the next three years.

This is a very grounded expectation.

As noted earlier, UnitedHealth is targeting a 13% to 16% long-term EPS growth rate.

The company has actually overshot this over the last decade, but it certainly won’t be getting any easier from here.

Here’s CFRA’s take on this target: “We find [UnitedHealth’s] goal of 13%-16% long-term EPS growth achievable, and we anticipate two-thirds of the earnings growth will derive from operations and the remainder from capital deployment, including acquisitions and share repurchases.”

With that target out in the open, CFRA is basically splitting the difference.

For reference, UnitedHealth’s most recent quarter – Q4 FY 2023 – showed 15.9% YOY EPS growth.

UnitedHealth has been so consistent and reliable, it’s difficult to find any reason at all to step in and argue with what’s clearly happening.

I accept this 14% number as the near-term base case, and it’s likely that it’s actually the long-term base case.

With the payout ratio still as low as it is, this sets up the dividend for at least 14% annualized growth over the next several years.

Adding that kind of dividend growth on top of the 1.6% yield could be positioning shareholders for a mid-teens annualized total return over the next decade or so – assuming no major degradation of multiples.

This is on a nearly-unassailable business that offers something many people cannot afford to live without in the 21st century.

I think that is highly, highly attractive.

Financial Position

Moving over to the balance sheet, UnitedHealth has a stellar financial position.

The long-term debt/equity ratio is 0.6, while the interest coverage ratio is almost 10.

While these are very good metrics, they don’t do full justice.

UnitedHealth’s total long-term debt load of approximately $58 billion is overwhelmed by the cash and investments noted earlier.

This is a very conservative balance sheet, which is unsurprising.

An insurance company is in the business of shouldering risk, and the balance sheet must be a pillar of strength.

Profitability for the firm is strong.

Return on equity has averaged 26% over the last five years, while net margin has averaged 6%.

I love the high returns on capital here, and UnitedHealth doesn’t even employ a lot of leverage for it.

Circling back around to margin expansion, net margin was closer to the 4% area at the beginning of the last decade.

Overall, this is just a fantastic business.

And with economies of scale, “sticky” memberships, vertical integration, an established float, and network effects, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

I see all three of these risks as elevated relative to the average business model.

Speaking of regulation, UnitedHealth is currently being probed by the DOJ over antitrust concerns.

UnitedHealth recently experienced a cyberattack that affected its ability to manage claims.

It’s always possible that that US healthcare complex undergoes some kind of fundamental change in the future, and any changes would almost certainly impact UnitedHealth in a major and direct way.

The advent of GLP-1s could cause a spike in spending for UnitedHealth (due to the cost of covering these drugs).

The size of UnitedHealth, while an advantage, may also be a disadvantage if the company runs into the law of large numbers and slowing growth in the future.

I think these risks are easily outweighed by the rewards of investing in UnitedHealth over the long run.

And with the valuation appearing to be attractive, those long-term rewards may be even bigger than normal…

Valuation

The stock’s P/E ratio is 20.5.

For a business that’s been reliably growing at a mid-teens rate, that is a very reasonable number.

It puts the PEG ratio at well below 2.

This earnings multiple is lower than where the broader market is at, and it’s also lower than the stock’s own five-year average P/E ratio of 22.1.

The cash flow multiple of 16.7 is also lower than its own five-year average of 17.8.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 10-year dividend growth rate of 14%, and a long-term dividend growth rate of 7.5%.

I’m basically assuming that UnitedHealth will continue to grow its dividend over the next decade as it has over the last several years.

With CFRA’s near-term forecast for EPS growth backing up UnitedHealth’s own guidance that calls for ~14% long-term EPS growth, I can’t imagine why the dividend can’t or won’t grow at that same kind of rate.

Of course, that kind of growth is not indefinite.

And I do see some moderation when going out past the next decade.

But there are so many tailwinds here for UnitedHealth, and a longer-term expectation for high-single-digit growth could actually be selling the firm short.

Outside of the elimination of private health insurance altogether, which is extremely unlikely, I simply do not see anything stopping this juggernaut.

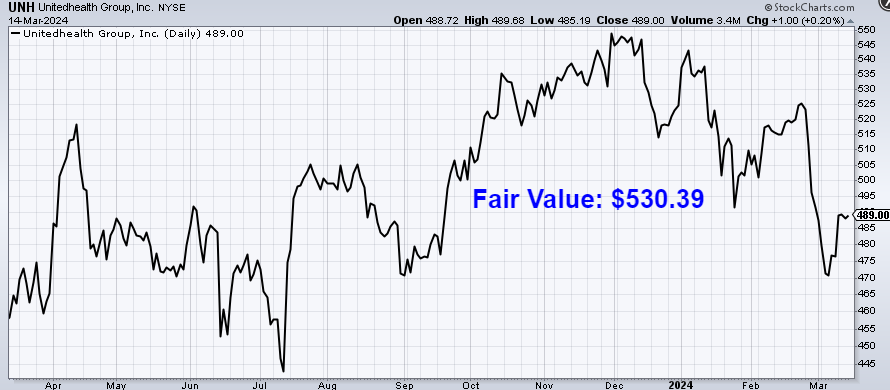

The DDM analysis gives me a fair value of $554.18.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

What I see is a very high-quality business that has an undemanding valuation.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates UNH as a 3-star stock, with a fair value estimate of $520.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates UNH as a 3-star “HOLD”, with a 12-month target price of $517.00.

I came out slightly high, but we’re all in a decently tight range here. Averaging the three numbers out gives us a final valuation of $530.39, which would indicate the stock is possibly 8% undervalued.

Bottom line: UnitedHealth Group Inc. (UNH) is a world-class business with industry-leading scale and vertical integration. Its offerings practically sell themselves, and customers are very “sticky”. With a market-like yield, double-digit dividend growth, a low payout ratio, nearly 15 consecutive years of dividend increases, and the potential that shares are 8% undervalued, long-term dividend growth investors looking for a premier healthcare firm should have their eyes on this name.

Bottom line: UnitedHealth Group Inc. (UNH) is a world-class business with industry-leading scale and vertical integration. Its offerings practically sell themselves, and customers are very “sticky”. With a market-like yield, double-digit dividend growth, a low payout ratio, nearly 15 consecutive years of dividend increases, and the potential that shares are 8% undervalued, long-term dividend growth investors looking for a premier healthcare firm should have their eyes on this name.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is UNH’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, UNH’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long UNH.