Investing has changed a lot since I first started out in 2010.

Back then, commission fees were high, information was difficult to gather, and everything took longer.

Nowadays, transactions are usually free, information is everywhere, and almost everything can be done instantaneously.

But one thing that hasn’t changed?

One thing that’s timeless?

The idea of investing great businesses for the long term.

This idea is crystallized in the dividend growth investing strategy – a strategy that advocates buying and holding shares in world-class businesses that pay safe, growing dividends.

You can see what I’m talking about by looking over the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Great businesses that can compound at high rates and generously reward shareholders with safe, growing dividend payments will never go out of style.

After all, one of the main reasons we invest is to grow our capital and generate investment income.

Dividend growth investing is one of the best ways to accomplish something like that, and I’ve personally used the strategy over the years in order to help me build my wealth and passive dividend income.

The result?

The result?

A real-life, real-money portfolio that I call the FIRE Fund.

This portfolio generates enough five-figure passive dividend income for me to live off of.

Not only that, it helped me to retire in my early 30s.

And my Early Retirement Blueprint goes over all of that.

Investing in great businesses that take care of their shareholders is a timeless concept.

Another timeless concept?

Valuation.

Price is only what you pay, but value is what you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying high-quality dividend growth stocks when they’re undervalued is a timeless approach to investing, and it’s a great method to achieve financial independence over time.

Now, valuation is something that might not be instantly intuitive.

No worries.

Fellow contributor Dave Van Knapp’s Lesson 11: Valuation, part and parcel of a comprehensive series of “lessons” on dividend growth investing, lays out a simple-to-follow valuation template which can be used to value just about any dividend growth stock you’ll run across.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Invitation Homes Inc. (INVH)

Invitation Homes Inc. (INVH)

Invitation Homes Inc. (INVH) is a real estate investment trust that owns and operates single-family homes for lease across the United States.

Founded in 2012, Invitation Homes is now a $21 billion (by market cap) real estate giant that employs more than 1,500 people.

Invitation Homes offers approximately 85,000 homes for lease across more than 20 US markets.

The company’s property portfolio is primarily focused on the Western US (40% of revenue), Florida (32%), the Southeast US (18%), and Texas (6%).

Invitation Homes aims to own and operate high-quality homes in desirable neighborhoods which feature convenient access to employment hubs, top schools, and transportation networks.

It’s known to everyone by now that the US has a housing shortage.

Because of numerous challenges, many of which date back to the GFC, housing supply has not kept up with demand for more than a decade.

The pandemic exacerbated some of these challenges and intensified the shortage further, and it’ll take years of consistent building to correct this.

Well, that’s precisely where Invitation Homes comes in.

This REIT offers spacious (averaging about 1,900 square feet) homes for rent in great neighborhoods across some of the most sought-after areas of the US (including the Sunbelt).

If a family wants a home but cannot afford to buy (because of the aforementioned dynamics leading to high prices on existing supply), a home that’s easy to move into and immediately lease at an affordable monthly payment is the next best thing.

Invitation Homes is in the right place – or right places – at the right time.

And that bodes incredibly well for the REIT’s ability to continue growing its revenue, profit, and dividend for many years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

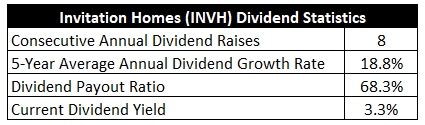

Already, the company has increased its dividend for eight consecutive years.

That dates back to the company’s 2017 IPO, so this track record is as long as it possibly could be.

Simply put, Invitation Homes has been rewarding shareholders with reliable, growing dividends right out of the gate.

The five-year dividend growth rate is 18.8%, which is just incredible.

REITs are typically low-growth income vehicles.

REITs are typically low-growth income vehicles.

I usually see low-single-digit growth rates from REITs, so this kind of dividend growth is surprising.

That said, the most recent dividend raise was 7.7%.

And I think a high-single-digit dividend growth rate is a good base case, as I’ll outline later.

With a market-beating yield of 3.3%, that kind of growth is actually enough to make a good case for long-term investment.

This yield, by the way, is 120 basis points higher than the stock’s own five-year average.

Admittedly, it’s difficult to square up an accurate comparison here, as the five-year average is skewed by a low starting yield and fast growth.

Also, the growth rate is slowing down, and the market is adjusting the yield higher in order to compensate for that.

Still, for investors who lean toward income and don’t like modeling in uncertain growth, this stock is suddenly worth considering.

It’s now living up to its status as a REIT.

With a payout ratio of 68.3%, which is pretty much in line for a REIT, I suspect the dividend will continue to grow roughly in line with the business.

For income-oriented investors who also like a healthy dash of growth, these metrics are compelling.

Revenue and Earnings Growth

As compelling as the numbers may be, though, many of them are looking into the past.

However, investors must always be looking into the future, as today’s capital is ultimately risked for the rewards of tomorrow.

This is why I’ll now build out a forward-looking growth trajectory for the business, which will be extremely useful when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done since its IPO in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this manner should give us what we need to make an informed call on where the business could be going from here.

Invitation Homes moved its revenue from $1.1 billion in FY 2017 to $2.4 billion in FY 2023.

That’s a compound annual growth rate of 13.9%.

Now, I usually like to look at a decade’s worth of growth (using that as a proxy for the long term) but Invitation Homes went public in 2017, and so I’m using the full public history.

This is strong top-line growth, but it also doesn’t tell the whole story.

When it comes to REITs, it’s imperative to look at profit growth on a per-share basis.

That’s because REITs use debt and equity to fund growth, as they’re legally required to distribute at least 90% of their taxable earnings to shareholders.

This circles back around to the point I made on REITs being income plays, and the limitations around internal funding for growth means tapping equity (by issuing shares) results in dilution.

That tends to create distortion between absolute revenue growth and profit growth relative to shares outstanding.

Also, when assessing profit for a REIT, we want to use funds from operations instead of normal earnings.

FFO (or adjusted FFO) is a measure of cash generated by a REIT, which adds depreciation and amortization expenses back to earnings.

Invitation Homes grew its FFO/share from $0.50 to $1.64 over this period, which is a CAGR of 21.9%.

Very impressive, especially for a REIT.

We can now see where the double-digit dividend growth has been coming from – it’s been fueled by double-digit FFO growth.

Looking forward, CFRA has no three-year projection for FFO/share growth.

That’s disappointing, as I do like to measure demonstrated growth against a future forecast.

However, we can glean something from this aspect of CFRA’s research: “On February 23 after further review, we raised our target $4 to $38, on a forward P/FFO of 20.2x, near the peer average at 19.0x given [Invitation Homes’] premier markets. We think [Invitation Homes] can grow its house rental portfolio even in a slower economy, but rent growth is easing. New lease rates are less at risk to affordability of rental rates and market conditions than multi-family residential properties.”

That 20.2 multiple implies next year’s FFO/share projection to be $1.88.

For reference, Invitation Homes released FY 2024 guidance that calls for $1.86, at the midpoint, in Core FFO/share.

That $1.86 number would represent 5.1% YOY growth off of FY 2023’s Core FFO/share.

I’ll also note that Invitation Homes increased FY 2023 FFO/share by 8.6% YOY – so growth is slowing right now.

Still, over the long run, Invitation Homes appears poised to grow at a high-single-digit rate, which would only be modestly faster than what some of the multifamily housing REITs have been growing at.

Based on the different dynamics, this growth premium seems warranted to me.s

CFRA notes: “Unlike the highly competitive multi-family residential market, we think [Invitation Homes] is best positioned in single-homes-for-rent (SFHR), which benefits from the major housing shortage and challenges of home ownership affordability. [Invitation Homes] has a differentiated product and living experience that fits a growing part of U.S. households wanting the flexibility and convenience of renting a single-family home.”

I think that sums it up nicely.

If we presume high-single-digit FFO/share growth, that should bleed down into similar dividend growth.

And you’re already starting off with a 3%+ yield.

That sets up shareholders for a 10%+ annualized total return from here, assuming no major changes to the multiples.

Achieving that with a fairly low-risk business model that benefits from a basic need (i.e., shelter), one could probably do a lot worse than that.

Financial Position

Moving over to the balance sheet, Invitation Homes has a good financial position.

The net debt/equity ratio is 0.8.

The company ended FY 2023 with total net debt of $8.6 billion, which isn’t overly concerning for its market cap of nearly $21 billion.

I’ll note that Invitation Homes has no debt reaching final maturity until 2026.

A common measure for a REIT’s financial position is the debt/EBITDA ratio, and I usually see REITs range from 3 to 7 on this ratio (lower is better).

Invitation Homes has a net debt/EBITDAre ratio of 5.5.

Pretty much right in the middle here.

Because REITs, by the very nature of the business model, tend to have aggressively leveraged balance sheets, and because I detest debt, I’m not a huge fan of REITs.

However, if there’s one type of commercial real estate that I am extremely enthusiastic about over the long term, it’s shelter.

People will always need somewhere to live, and there’s basically no risk of obsolescence.

That kind of long-term visibility into demand really does calm my balance sheet concerns when it comes to this particular REIT.

Overall, Invitation Homes has been putting up impressive numbers since its 2017 IPO, and I don’t see anything to indicate much of a change over the coming years, although some slowing would be natural.

And with economies of scale, an entrenched footprint in desirable locations, and favorable supply dynamics that feed demand, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

A REIT’s capital structure relies on external funding for growth, which exposes the company to volatile capital markets (through equity issuances) and interest rates (through debt issuances).

Adding to the rate conversation, higher rates can hurt this particular business model twice over: Debt becomes more expensive to take on and service, and equity can become more expensive (because income-sensitive investors have alternatives, which puts downward pressure on the stock price).

While Invitation Homes has leadership and scale, there are really no major barriers to entry that prevent competitors from replicating the business model by acquiring land and building homes.

The US continues to add houses to inventory, and more homes for sale could reduce demand for rental homes.

Multifamily housing REITs have demonstrated long-term success in the market, but single-family homes for lease at scale is a business model that isn’t as proven.

There is some exposure to the economy, as rising unemployment in the company’s key markets would likely lead to less demand, lower rents, and higher vacancies.

Since Invitation Homes must buy homes to grow its portfolio, the company is directly exposed to the US housing market (which can be quite volatile, even at local levels).

I see many of these risks as pretty standard for a REIT, although Invitation Homes is somewhat new and unique.

But with the valuation being relatively undemanding, a lot of risks are currently being priced in…

Valuation

The stock is trading hands for a P/FFO ratio of 20.5.

That is somewhat analogous to a P/E ratio on a normal stock.

For a business that has compounded its bottom line at over 20%/year since its IPO, that is not egregious at all.

Also, the P/CF ratio of 18.8 is quite a bit lower than its own five-year average of 22.1.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

That growth rate is actually at the high end of what I ordinarily allow for when dealing with a REIT.

I’m more often using a mid-single-digit growth rate for REITs, but Invitation Homes has shown an abnormal ability to grow much faster than the typical REIT.

As such, I’m accounting for that and giving the business the benefit of the doubt.

Now, this still isn’t anywhere near what Invitation Homes has delivered since the IPO.

But a slowing would be natural, and the most recent numbers out of the company seem to indicate a settling into a high-single-digit growth rate – for the time being, at least.

This kind of expectation would only be modestly ahead of what a lot of larger, more mature multifamily housing REITs get from me, but I think this company’s smaller size and favorable market dynamics give it a slight edge.

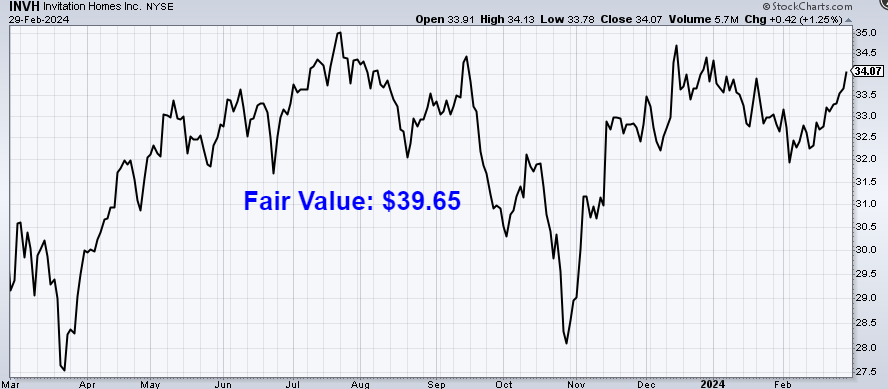

The DDM analysis gives me a fair value of $39.95.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

The stock looks decently cheap from my point of view.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates INVH as a 4-star stock, with a fair value estimate of $41.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates INVH as a 4-star “BUY”, with a 12-month target price of $38.00.

We have a pretty tight consensus this time around. Averaging the three numbers out gives us a final valuation of $39.65, which would indicate the stock is possibly 15% undervalued.

Bottom line: Invitation Homes Inc. (INVH) is a unique REIT that is in a great spot, at a great time. Its massive portfolio of homes for lease across the US are located in some of the very best spots, and a chronic shortage of housing leads to favorable demand trends that should endure for many years. With a market-beating yield, double-digit dividend growth, a moderate payout ratio, nearly 10 consecutive years of dividend increases, and the potential that shares are 15% undervalued, long-term dividend growth investors looking to increase their exposure to real estate could have a great investment opportunity on their hands with this one.

Bottom line: Invitation Homes Inc. (INVH) is a unique REIT that is in a great spot, at a great time. Its massive portfolio of homes for lease across the US are located in some of the very best spots, and a chronic shortage of housing leads to favorable demand trends that should endure for many years. With a market-beating yield, double-digit dividend growth, a moderate payout ratio, nearly 10 consecutive years of dividend increases, and the potential that shares are 15% undervalued, long-term dividend growth investors looking to increase their exposure to real estate could have a great investment opportunity on their hands with this one.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is INVH’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 60. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, INVH’s dividend appears Borderline Safe with a moderate risk of being cut. Learn more about Dividend Safety Scores here.

Disclosure: I have no position in INVH.

Source: Dividends & Income