What makes investing so difficult for some people?

Well, I think there are a lot of pitfalls.

Using too short a time period, succumbing to any number of psychological biases, and/or not fully understanding what’s being invested in are all thorns waiting to sting some market participants.

Fortunately, there are solutions to all of investing’s problems.

And I’d argue that one particular investment strategy is a great “catch-all” solution.

That strategy is dividend growth investing.

This strategy advocates buying and holding shares in high-quality businesses that pay safe, growing dividends to shareholders.

You can see what I mean by perusing the Dividend Champions, Contenders, and Challengers list – a compilation of invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

The strategy is so effective because it almost automatically funnels an investor right into great long-term investments, bypassing so many of the possible pitfalls out there.

The strategy is so effective because it almost automatically funnels an investor right into great long-term investments, bypassing so many of the possible pitfalls out there.

I’ve personally used the strategy for more than a decade now, allowing it to guide me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

I’m not only able to live off of dividends now, but I’ve been able to for years.

In fact, I was able to quit my job and retire in early 30s… all thanks to dividend income.

My Early Retirement Blueprint explains how I accomplished this feat.

A pillar of the Blueprint is, of course, the strategy I just outlined.

But that’s not all.

Valuation at the time of investment is also crucial.

Valuation at the time of investment is also crucial.

After all, price only represents what you pay, but value represents what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Using the dividend growth investing strategy as a long-term framework to consistently buy undervalued high-quality dividend growth stocks can allow an investor to avoid most common investment pitfalls, succeed, and even become financially independent.

Of course, traversing down that road does require one to first have a basic understanding of valuation.

Fear not.

My colleague Dave Van Knapp put together Lesson 11: Valuation in order to help with that.

Part and parcel of a comprehensive series of “lessons” on dividend growth investing, it lays out a valuation template that can be used to estimate the fair value of almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

EOG Resources Inc. (EOG)

EOG Resources Inc. (EOG)

EOG Resources Inc. (EOG) is an American energy company that engages in hydrocarbon exploration and production.

Founded in 1999, EOG Resources is now a $66 billion (by market cap) energy monster that employs nearly 3,000 people.

EOG Resources primarily operates across a number of US shale fields and basins, including Williston Basin, Powder River Basin, DJ Basin, Anadarko Basin, Barnett Shale, Permian Basin, Eagle Ford, Dorado, South Texas, Utica, and the Columbus Basin.

The company finished FY 2022 with net proved reserves at 4.2 billion barrels of oil equivalent (approximately 13 years of production).

EOG Resources produced just over 908 thousand barrels of oil equivalent per day in FY 2022, of which 73% was oil and natural gas liquids and 27% was natural gas.

There are some things to like… and some things to not like about an O&G E&P company like EOG Resources.

First, the bad news.

EOG Resources is a commodity play.

As such, it’s a price taker, not a price maker.

The company is largely captive to energy market forces for its revenue and profit.

And seeing as how it is a relatively smaller player (compared to the fully integrated supermajors), EOG Resources is not totally in control of its own destiny.

This has led to wild swings in results over most of the last two or so decades.

With that out of the way, let’s get to the good news.

First, the company is producing vital energy products which must be consumed in order to enjoy a modern-day standard of living in a developed country – think electricity, transportation, technology, etc.

There’s a base level of demand here.

Otherwise, without hydrocarbons, because renewable forms of energy are not yet enough to meet basic needs, we’d effectively be back to a pre-industrial civilization.

Plus, this base level of demand is rising, as developing countries are consuming more energy as they grow, increase consumption, and raise their standard of living.

Beyond that built-in demand, supply properties have been improved thanks to an entire industry which has been reevaluated and revitalized in recent years – so we have a favorable supply and demand story here.

It used to be a “drill, baby, drill” mantra, where it was all about maximizing production in order to drive higher revenues.

That’s all gone now.

Major E&P companies are no longer focused on more production at all costs.

Instead, there’s been a rationalization among the major players, where the new focus is on sustainable cash flow.

So it’s less “hydrocarbon production”, more “cash flow production”.

The industry now prioritizes low costs, rational pricing, and the generation of free cash flow (which can be returned back to investors via buybacks and dividends).

EOG Resources has been, perhaps, the poster child of this new line of thinking.

As Morningstar states: “The firm differentiates itself by finding prospective areas before peers catch on, enabling it to secure leasehold at attractive rates, rather than overpaying for land after the market overheats. It has only one large-scale M&A deal under its belt, related to its 2016 entry to the Permian Basin. Nevertheless, the firm is also active in most other name-brand shale plays, including the Bakken and Eagle Ford. Additionally, the focus now includes the Powder River Basin and a new natural gas play in southern Texas called Dorado.”

EOG Resources takes low costs, cash flow production, and prudent stewardship seriously.

As a long-term investor who cherishes cash flow and returns, I like this very much.

What this new industry direction does is, it creates two powerful dynamics for companies and shareholders to feed off of.

First, because of scaled-back production, oil prices can remain higher (via reduced supply) and reserves can be protected for longer.

Second, and because of that first point, revenues and profits for E&P companies are higher and healthier than they’ve been in many years.

Indeed, EOG Resources has been steadily and rapidly increasing both, which has bled down into a large, growing dividend for shareholders to enjoy.

Dividend Growth, Growth Rate, Payout Ratio and Yield

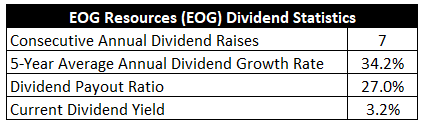

The company has increased its dividend for seven consecutive years.

While this is a decent start to what could be a lengthy track record of dividend growth, this belies the company’s impressive, multidecade faithfulness to its dividend.

The company has 26 years of a stable and growing dividend – some years were “just” stable, but there’s no dividend cut here across nearly three decades.

The five-year dividend growth rate is 34.2%, which goes to show you what an under-the-radar dividend growth monster EOG Resources is.

Better yet?

Better yet?

No major sacrifice on yield.

The stock offers a solid 3.2% yield.

That easily beats what the broader market gives you, and it’s 130 basis points higher than its own five-year average.

But wait.

There’s more.

EOG Resources regularly pays out special dividends.

The company paid two special dividends in 2023, adding up to an additional $2.50/share (over and above the regular dividends).

That’s a 2.2% yield kicker right there (using 2023’s special dividends at today’s stock price) – bringing the all-in yield up to 5.4%.

Now, there are no guarantees of continued special dividends.

But the dividend profile here is already great, and special dividends possibly waiting in the wings only adds to the appeal.

Moreover, management has committed to distribute a minimum of 70% of free cash flow back to shareholders from 2024, and that would portend more special dividends.

With a payout ratio of just 27%, which is quite low, EOG Resources certainly has the capability to handle both double-digit dividend growth and some special dividends.

I’ve gotta say, EOG Resources is shaping up to be a tremendous dividend growth stock.

Fantastic dividend metrics right across the board.

Revenue and Earnings Growth

As fantastic as these metrics might be, though, many of the numbers are looking backward.

However, investors must always be looking forward, as the capital of today is put on the line for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be instrumental when the time comes later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should give us a pretty good idea of where the business may be going from here.

EOG Resources advanced its revenue from $14.5 billion in FY 2013 to $25.7 billion in FY 2022.

That’s a compound annual growth rate of 6.6%.

Good stuff.

The company has been moving the top-line needle at a nice clip.

Meanwhile, earnings per share grew from $4.02 to $13.22 over this 10-year period, which is a CAGR of 14.1%.

Drastically improved profitability, thanks to the industry dynamics I already touched on, helped to drive a lot of excess bottom-line growth.

Looking forward, CFRA is forecasting that EOG Resources will compound its EPS at an annual rate of -2% over the next three years.

So it’s basically a call on the cycle, and CFRA apparently sees a near-term top on that.

And that’s okay.

All EOG Resources has to do is keep doing what it’s been doing – keep costs low, manage responsible production, and focus on cash flow.

The rest will work out by itself.

CFRA highlights this: “EOG maintains strong positions in key liquids-rich plays, Dorado adds a gas play near export markets, and the company has expanded in the Ohio Utica and Powder River Basin plays. EOG was already focusing on returns over production before the pandemic, and about 75% of the cost reductions achieved in 2020 look to be sustainable, delivered via innovation/efficiencies rather than via service cost reductions which could snap back.”

Because of the strong FCF and low payout ratio, EOG Resources is in a great position to continue growing its regular dividend and hand out special dividends – even with some near-term questions around commodity pricing.

CFRA notes this: “EOG has stated a goal of returning at least 70% of annual free cash flow to shareholders via buybacks and dividends, starting in 2024. We estimate 2024 free cash flow of $6.2B, and note the regular dividend chews up $2.1B.”

With the regular dividend set to consume approximately 34% of 2024’s FCF, there’s a lot of room for management to take extra care of shareholders and meet its commitment.

Regardless of near-term commodity pricing, I see more double-digit dividend raises to come.

And with a 3%+ starting yield, you’ve really got to like that kind of setup.

Financial Position

Moving over to the balance sheet, EOG Resources has a fantastic financial position.

The long-term debt/equity ratio is 0.2, while the interest coverage ratio is over 65.

While these are both really great numbers already, they actually don’t do the financial position full justice.

I say that because EOG Resources has a net cash position.

The company finished FY 2022 with nearly twice as much cash on hand as long-term debt.

The balance sheet improvement over the last few years has been remarkable.

For example, long-term debt has been halved since FY 2016, while cash on hand quadrupled over that period.

This speaks to the overall rationalization of the entire industry that I dived into earlier.

Profitability is outstanding.

Return on equity has averaged 17.9% over the last five years, while net margin has averaged 17.5%.

Again, these numbers don’t tell the whole story.

That improvement theme plays out once more, as ROE has come in at over 30% for the last two fiscal years – without balance sheet juicing.

It’s hard to overstate just how much better EOG Resources is today compared to, say, just five years ago.

It’s almost like looking at two totally different businesses.

And with economies of scale, low-cost operations, barriers to entry, and favorable acreage, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

While the world still requires hydrocarbons for energy, there’s a long-term risk that renewable forms of energy will fully displace oil & gas.

This is a capital-intensive business model that is highly cyclical.

EOG Resources is a price taker and highly dependent on commodity pricing.

The company’s reserves must continually be added to so as not to risk running out of supply.

Fields naturally get depleted over time, and there are questions around just how much supply is left in the world.

The industry sees constant pressure from some environmental groups which may result in negative goodwill across parts of society.

Overall, I don’t see the risks here as out of the ordinary for this type of business, and the lack of meaningful international exposure actually limits the kind of geopolitical risk that some larger peers contend with.

Furthermore, with the stock down 20% from recent highs, the valuation looks rather attractive…

Valuation

The stock is trading hands for a P/E ratio of 8.6.

That’s not only low in absolute terms but also relative terms.

It’s obviously way lower than the broader market’s earnings multiple.

It’s also notably below the stock’s own five-year average P/E ratio of 13.2.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

That’s a fairly moderate type of growth rate, and it’s definitely dialed down a bit.

This is, after all, a capital-intensive and cyclical business model that is captive to extremely volatile commodity prices.

I think it makes a lot of sense to be cautious around long-term growth rates, knowing that cycles will result in bursts and slowing as it relates to growth.

Smoothing things out, averaging out across the cycles, I do see EOG Resources as being easily capable of a high-single-digit dividend growth rate.

The near term may be especially lucrative, if only because of that gap between FCF and the current dividend level, but that may slow over the coming years.

The most recent dividend raise was 10.3%, and I think that’s a pretty good yardstick for the next year or two, but looking out beyond that type of time frame is where things start to get more iffy.

All that said, this valuation model only accounts for the regular dividend.

Seeing as how EOG Resources pays special dividends, the shares are, possibly, worth even more than what the model shows.

Still, if I’m guilty of erring on the side of caution, I’m okay with that.

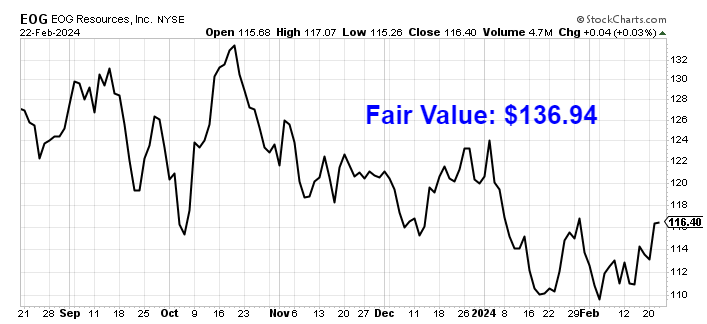

The DDM analysis gives me a fair value of $129.83.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Even with a conservative take on the valuation, not accounting for special dividends, the stock comes out looking decently cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates EOG as a 4-star stock, with a fair value estimate of $129.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates EOG as a 4-star “BUY”, with a 12-month target price of $152.00.

I came out extremely close to where Morningstar is at on this one. Averaging the three numbers out gives us a final valuation of $136.94, which would indicate the stock is possibly 15% undervalued.

Bottom line: EOG Resources Inc. (EOG) is a high-quality energy company that has been radically improved in recent years. This business now looks better than it ever has before. For as long as the world runs on hydrocarbons, this firm and its shareholders should do well. With a market-beating yield, double-digit dividend growth, a low payout ratio, nearly 10 consecutive years of dividend increases, and the potential that shares are 15% undervalued, long-term dividend growth investors looking to intelligently boost their energy exposure have an interesting opportunity on their hands with this one.

Bottom line: EOG Resources Inc. (EOG) is a high-quality energy company that has been radically improved in recent years. This business now looks better than it ever has before. For as long as the world runs on hydrocarbons, this firm and its shareholders should do well. With a market-beating yield, double-digit dividend growth, a low payout ratio, nearly 10 consecutive years of dividend increases, and the potential that shares are 15% undervalued, long-term dividend growth investors looking to intelligently boost their energy exposure have an interesting opportunity on their hands with this one.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is EOG’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 82. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, EOG’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long EOG.