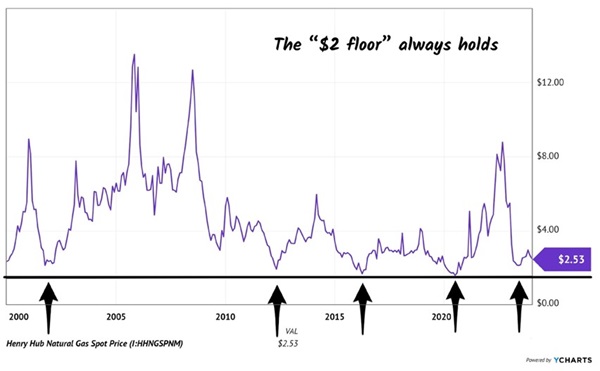

Natural gas did it again! It fell below $2 per million BTUs. These washout levels typically represent a floor for nat gas prices.

Every time it drops below this $2 linoleum level, the price eventually pops and tests the ceiling. Now that we have this ideal setup again, let’s back up the truck!

Death, taxes and the cyclical nature of natural gas are the only three things we contrarians can be certain about! Natural gas always bounces back. The cure for low commodity prices is low prices.

The reason for this is simply supply and demand. When natural gas prices are low, producers stop producing. Which means less supply.

Natural gas companies can cut (“shut in”) production quickly. They do it out of self-preservation—to save money so that they can live to see another “up cycle” in prices.

Of course, they all cut at once! Which crimps supply. Which ensures rising prices that eventually test the ceiling, because while it’s easy to shut in gas wells, it takes years to bring them—and higher supply—back. Gas producers cut quickly and ramp slowly.

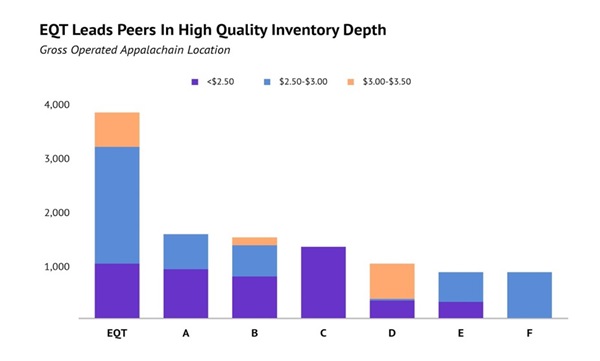

When natural gas is low, unloved and due to rally, EQT Corp (EQT) is my “go to” stock. Here’s EQT’s inventory versus competitors at various price levels. (I’ve hidden the names of lesser competitors to protect the innocent. Or really, the less profitable.)

The prices above indicate at what level the company’s gas is profitable to drill. Notice that EQT leads the pack overall, and with gas less than $2.50 the producer has more than double the inventory of its nearest competitor!

The prices above indicate at what level the company’s gas is profitable to drill. Notice that EQT leads the pack overall, and with gas less than $2.50 the producer has more than double the inventory of its nearest competitor!

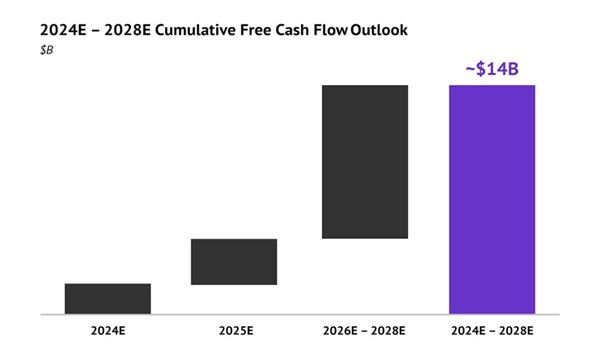

EQT trades for a cheap six-times free cash flow (FCF) as I write. But the bargain is about to get even better because FCF is about to soar. Over the next five years, the company will generate about $14 billion in free cash!

This is notable because EQT trades for a market cap around $15 billion today. Which means we can buy it here and theoretically get paid back (via dividends and buybacks) by the end of 2028.

This is notable because EQT trades for a market cap around $15 billion today. Which means we can buy it here and theoretically get paid back (via dividends and buybacks) by the end of 2028.

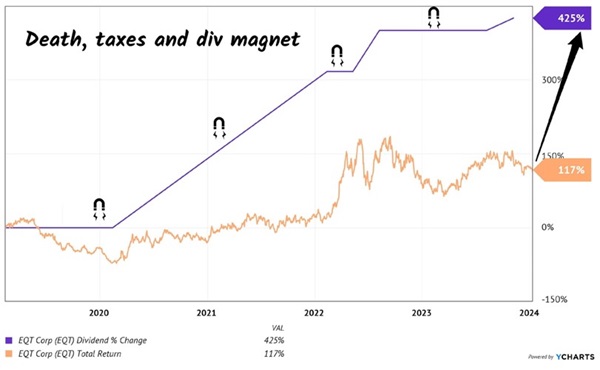

We could easily double our money holding EQT because its stock price is due to climb. For months and even a few years, tickers can meander independently of their dividends. But eventually, they follow their payouts higher like a puppy dog. EQT’s dividend has leaped above its stock, and that is a coiled spring for the price:

EQT’s Dividend Magnet is Due

Antero Midstream (AM) is a high-yield natural gas play, a pipeline operator that was formed by parent company, producer Antero Resources, in 2012. AM (our “Antero”) is a toll bridge that moves gas from the Appalachian Basin in West Virginia to the rest of North America.

Antero Midstream (AM) is a high-yield natural gas play, a pipeline operator that was formed by parent company, producer Antero Resources, in 2012. AM (our “Antero”) is a toll bridge that moves gas from the Appalachian Basin in West Virginia to the rest of North America.

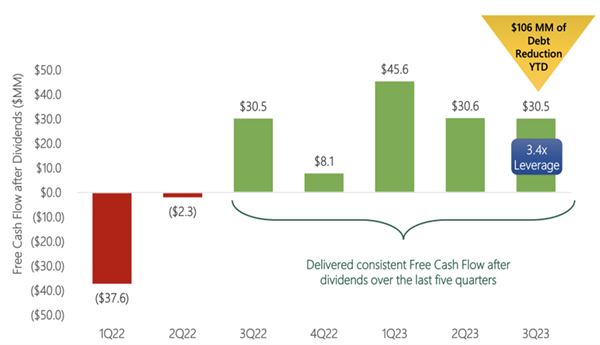

This is an ideal time to buy AM, which achieved positive cash flow more than its dividend payments during the second half of 2022. The stock is at an opportunistic inflection point. The company generates more money than it needs to grow and pay investors. Which is why this “cheap gas” play and its 7.6% payout look promising here.

With AM now generating cash flow in excess of its big dividend payments and need to reinvest in its core business, four good things are going to happen:

- Antero will keep de-levering (paying down debt), which will unlock a virtuous shareholder cycle.

- Less debt and more cash flow will prompt the company to repurchase shares.

- Which means AM will lighten its dividend obligation, with fewer quarterly payments to send out.

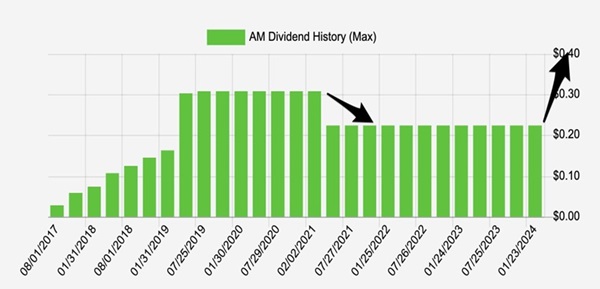

- This will support AM’s dividend raise. So, anyone who locks in a 7.6% dividend today will look back on this purchase fondly, because this “yield on cost” will rise over time. Likely soon, because AM is constantly hiking!

Management began going on “offense” in 2021 via a targeted $17 billion acquisition spree. AM has also paid down debt to lower the company’s financial leverage and give management more flexibility going forward for dividend hikes and share repurchases.

Overall debt load is already down to 3.4-times EBIDTA. Next stop is sub-3x leverage:

As Antero achieves its debt goals, it turns to share repurchases. Chief Financial Officer (CFO) Brendan Krueger admitted this during the company’s last earnings call:

As Antero achieves its debt goals, it turns to share repurchases. Chief Financial Officer (CFO) Brendan Krueger admitted this during the company’s last earnings call:

I think share repurchases continue to make a lot of sense for that further return of capital.

I agree with Brendan—it makes sense for the company to buy back its own stock first. Then, even more good moves can come. Every time AM buys back shares, it no longer must pay dividends on them. That means more cash to raise its dividend for us. It’s a virtuous circle!

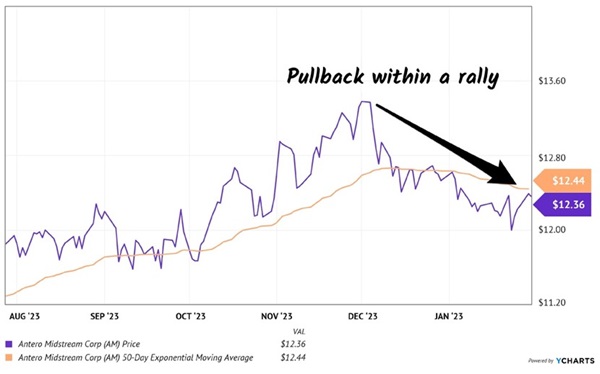

The stock price has recently pulled back. This is an ideal dip to buy. Your move, Brendan:

Let’s Buy the Dip

But wait! Before Brendan moves, we contrarians should grab our stake. Again, we want to snare AM before it boosts its payout:

But wait! Before Brendan moves, we contrarians should grab our stake. Again, we want to snare AM before it boosts its payout:

This 7.6% Payer is Poised to Hike

Source: Income Calendar

Source: Income Calendar

It’s impressive that Antero achieved this inflection point with natural gas prices in the tank. Check out this chart, which represents the monthly average price of nat gas:

Nat Gas Price Floor and Ceiling

As I write, natural gas fetches just $1.85 per million BTUs, even less than its most recent monthly average. We should prepare ourselves for a big bounce.

As I write, natural gas fetches just $1.85 per million BTUs, even less than its most recent monthly average. We should prepare ourselves for a big bounce.

— Brett Owens

Sponsored Link: There will be no Hallmark cards for natural gas stocks today. So, in honor of these discarded dividends, let’s show some love and appreciation:

Roses are red,

Violets are blue,

Let’s buy these cheap divvies,

While nat gas is below two.

And these cheap natural gas payers have company. Thanks to recent volatility in the bond market, some additional dividend deals have popped up—and are poised to pop!

Like EQT, these are companies that are raising their payouts quickly. Which means their stock prices are likely to rise rapidly as Wall Street moves on from its obsession with its expensive “magnificent seven” to these safe, cheap dividend stocks.

I’m talking annual returns of 15% per year, every year, from these secure payers. What’s not to like? It’s the simple and safe route to 15%+ returns every year.

Source: Contrarian Outlook