Look, we’re going to get a slowdown here in America this year—two years’ worth of rate hikes are going to hit home. Fact.

So I’m going to suggest we do something you might find a little bit weird: buy US stocks. But not any US stocks—and certainly not “dividend-dud” ETFs like the ever-popular SPDR S&P 500 ETF Trust (SPY)!

No way.

Instead we’re shopping in the small(er) cap aisle, for stocks in the midcap range kicking out surging dividends. We love these overlooked US-based dividend plays now because:

They’re cheap: while SPY has soared 19% in the last year, midcaps have treaded water, with the Vanguard Mid Cap ETF (VO)—in orange below—up just 4%.

Dividend-focused midcap ETFs like the WisdomTree MidCap Dividend ETF (DON)—in purple—have been even more shunned, slipping around 1%:

DON and VO Show Us Where the Deals Are

Plus …

Plus …

Midcaps are more US-focused: And we want to be here in the US when a slowdown hits, because we have a labor shortage that’ll take years to sort out. So spending will hold up—but not everywhere.

Which is why we don’t want to just buy the likes of VO and DON and be done with it.

Instead we’re going to “cherry-pick” smaller companies that target those parts of the economy likely to keep growing. Here are three options, all plucked from DON’s holdings.

They’re a little over the traditional definition of a midcap stock, sporting market caps of $12 billion to $15 billion, but still much smaller than the multinational monsters of the S&P 500.

Midcap Stock #1: An 88% Payout Grower With Decades of Gains Ahead

Alliant Energy (LNT) is what I call a “growth utility”—it boasts a stable core of clients (995,000 electric customers and 425,000 gas customers in Iowa and Wisconsin) and is boosting capacity to meet a coming surge in demand.

Alliant also owns a 16% stake in American Transmission Company, which has 10,000 miles of transmission lines and 560 substations.

Much of that higher demand will come from the electrification of industry, an ongoing megatrend that still has decades to run. Alliant is well-positioned to cash in, with industrial consumers accounting for 31% of energy consumption in Wisconsin.

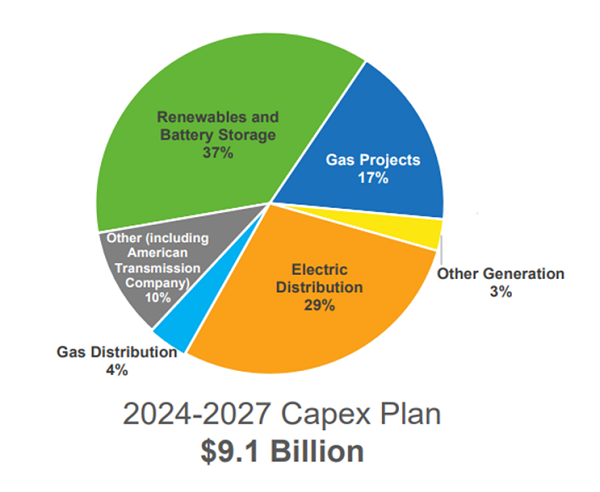

The firm is building out the capacity those businesses will draw on—especially through renewables, with nearly 40% of its capex plan focused on wind and solar, along with accompanying battery storage.

Source: Alliant Energy November 2023 investor materials

Source: Alliant Energy November 2023 investor materials

That’s a smart move as the price of renewable generation falls: according to the International Energy Agency (IEA), 96% of newly installed solar and onshore wind facilities generated electricity for less than new coal and gas plants would have in 2023.

We also like utilities now because they’re basically “bond proxies”—and that means they command higher valuations as interest rates fall, which they will as the economy gears down.

That will take bond yields down from here, and as they fall, bond (and bond proxy!) prices will rise. Utilities will also catch a tailwind as they refinance debt at lower rates.

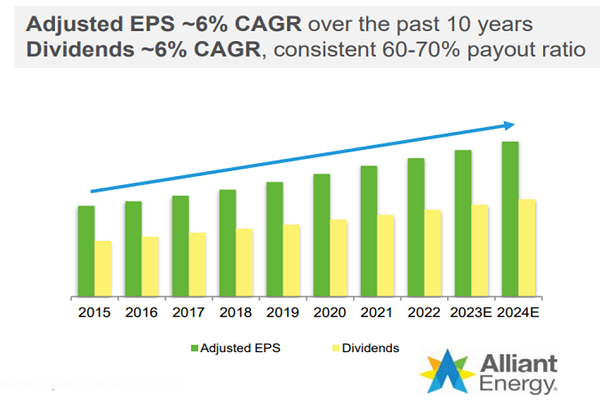

Meantime, LNT does nothing but make money, having grown EPS at a compounded annualized rate of 6% in the last decade, with the dividend coming along for the ride.

Source: Alliant Energy November 2023 investor materials

Source: Alliant Energy November 2023 investor materials

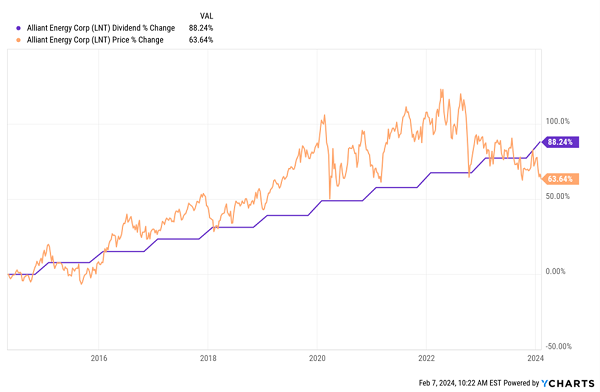

All the other “dividend digits” are working in our favor here, too: LNT kicks out a high 4% current yield, and those hikes you see above have resulted in an 88% overall increase in the payout in the last decade.

That’s paced the share price higher, point for point, a phenomenon we call the “Dividend Magnet.” And as you can see below, the stock has actually fallen behind the payout growth lately.

Alliant’s “Dividend Magnet” Is Set to Kick in Again

That’s key, because as you can see above, a “dividend gap” like this is a rare occurrence. And history tells us the price is overdue to bounce back up over the payout—where it almost always resides. The time to make a move is now, before that happens.

That’s key, because as you can see above, a “dividend gap” like this is a rare occurrence. And history tells us the price is overdue to bounce back up over the payout—where it almost always resides. The time to make a move is now, before that happens.

Midcap Stock #2: A Casino REIT Cashing in on “Landlord Friendly” Leases

Speaking of electricity, can you imagine what this power bill looks like?

Fortunately shareholders of Gaming and Leisure Properties (GLPI) don’t have to worry about it: the casino landlord’s tenants are signed up to “triple-net” leases—meaning they pay the full cost of running and maintaining the company’s 61 properties.

Fortunately shareholders of Gaming and Leisure Properties (GLPI) don’t have to worry about it: the casino landlord’s tenants are signed up to “triple-net” leases—meaning they pay the full cost of running and maintaining the company’s 61 properties.

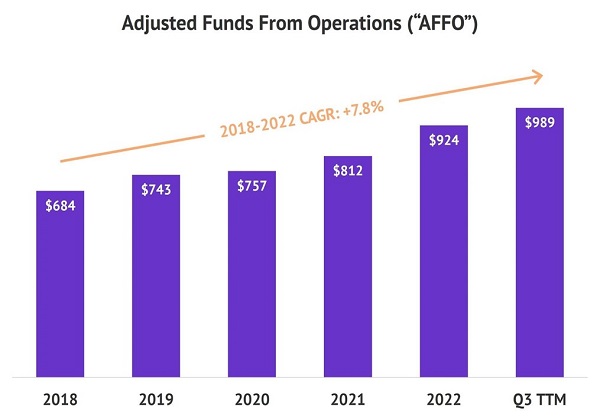

It’s a sweet deal for landlords, as is the fact that as a real estate investment trust (REIT), GLPI is exempt from corporate taxes so long as it pays out 90% of its profits as dividends. The result has been consistent cash flow growth (as measured by adjusted funds from operations, the best cash-flow metric for REITs):

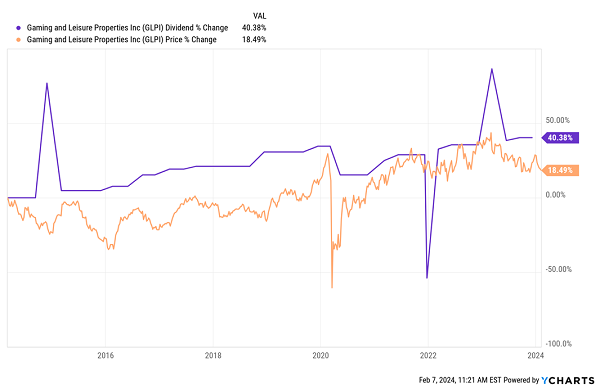

The best part is, the REIT has been sharing that cash stream through its high current yield (a tidy 6.5%) and payout growth—including three special dividends in the last 10 years (the spikes and dips in the chart below):

The best part is, the REIT has been sharing that cash stream through its high current yield (a tidy 6.5%) and payout growth—including three special dividends in the last 10 years (the spikes and dips in the chart below):

The REIT’s regular dividend was cut in 2020, as were those of most entertainment stocks when the world shut down. But the cut was modest: just 14%.

The REIT’s regular dividend was cut in 2020, as were those of most entertainment stocks when the world shut down. But the cut was modest: just 14%.

And GLPI quickly got back to its winning ways, boosting the payout nearly 22% since, while paying two special dividends. And with the share price currently trailing the dividend by the widest margin since the dark days of 2020, we’ve got some LNT-style “snap-back” upside in store for us here, too.

Forget Vegas: The Real Casino Action Is in … Toledo!?

If you’re worried that GLPI may not be able to weather a slowdown, fear not: it’s broadly diversified away from Vegas: its 61 properties are spread out across 18 states, including in cities like Toledo, St. Louis and Baton Rouge.

That’s an edge in a recession because while people may not travel to gamble, they will still gamble at their local casino. And there’s a decent chance that casino will be run by GLPI.

Midcap Stock #3: A Dividend-Growth Play on “Reno Boom II”

Masco Corp. (MAS) is the definition of a household name: it makes Peerless and Delta faucets, Kichler lighting, Behr paints, Hansgrohe shower products and other items you’ll find in (and behind the walls of) most US homes.

If you’re like many folks, you reno’ed your place in 2020, when, frankly we thought we might never leave our homes again. Despite the pullback in the home renovation market that followed, Masco has kept its profits growing.

While adjusted EPS advanced just 2% in its just-reported fiscal 2023 results, Masco expects adjusted EPS of $4.00 to $4.25 in fiscal 2024, the midpoint of which is up 7%.

Moreover, the reno space is set to bounce as rate cuts spur the real estate market, prompting sellers to polish up their places—and new owners to put their stamp on them.

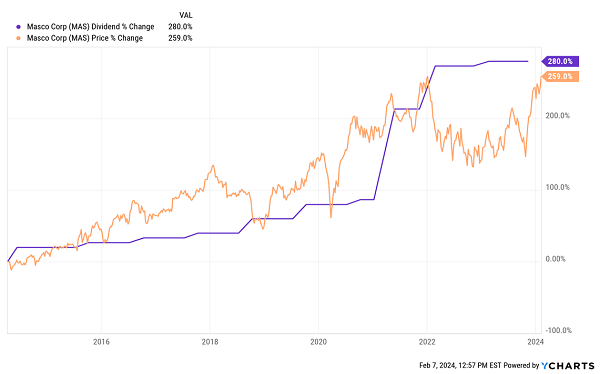

One thing we love about Masco is that management is serious about keeping the dividend safe, targeting a payout ratio of 30% of earnings. That’s far below my “safety line” of 50%, and it’ll keep this dividend/share price tango going:

Masco Can Keep Payouts—and Its Share Price—Popping in any Economy

That rapid growth more than makes up for Masco’s low 1.6% current yield.

That rapid growth more than makes up for Masco’s low 1.6% current yield.

And there’s another layer of safety for the payout in the form of Masco’s strong balance sheet: the firm’s roughly $2.3 billion of long-term debt (net of cash) is a mere 16% of its market cap. That’s very conservative—and yet another sign that management has a firm hand on the wheel here.

— Brett Owens

5 More “Dividend Magnet” Winners Primed to Skyrocket (Recession or No) [sponsor]

The Dividend Magnets you see at work on the three stocks above are much more than simple coincidence. I’ve seen this same pattern in dividend stock after dividend stock.

It’s such a powerful indicator that I’ve put it at the heart of my dividend-investing strategy. And it’s recently uncovered 5 overlooked dividend growers whose payouts aren’t only growing but accelerating—booking bigger and bigger raises yearly.

That’s pulled their share prices higher in lockstep—and the biggest gains are still ahead as these soaring payouts work their magic.

The time to buy these 5 dividend growers is now, before their next hikes are announced. Click here and I’ll show you why the Dividend Magnet is such a powerful indicator and give you access to a FREE Special Report naming my top 5 buys for surging dividends—and prices—in the year ahead.

Source: Contrarian Outlook