Investing can be many things to many people.

For some, it’s simply about money and the compounding of it over time in order to build wealth.

For others, it’s a joy to follow businesses, learn about the world, and financially benefit along the way.

And for a large contingent out there, much of it comes down to attaining (and maintaining) financial independence and the freedom that comes with it.

No matter what investing may be to you, I believe one strategy can unite us all.

That strategy is dividend growth investing.

This strategy is all about buying and holding shares in world-class enterprises that reward shareholders with safe, growing dividends.

Those safe, growing dividends are funded by safe, growing profits.

And since only great businesses can routinely produce safe, growing profits, this strategy has a way of funneling investors right into some of the best long-term investments out there.

You can see what I mean by looking at the Dividend Champions, Contenders, and Challengers list, which has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I’ve been using this strategy for myself for more than a decade now.

I’ve been using this strategy for myself for more than a decade now.

What’s it done for me?

Well, it’s guided me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

This strategy also helped me to retire in my early 30s.

I describe in my Early Retirement Blueprint exactly how I was able to achieve such a feat.

Now, while dividend growth investing can funnel you right into great businesses, what you pay at the time of investment is of critical importance.

It comes down to valuation.

It comes down to valuation.

See, price is what you pay, but it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

No matter what you’re looking to get out of investing, buying undervalued high-quality dividend growth stocks can probably get you there.

All that said, being able to estimate the fair value of a business might seem difficult.

But it’s actually not as challenging as you might think.

Fellow contributor Dave Van Knapp put together Lesson 11: Valuation a while back, and it lays out an easy-to-follow valuation template that can be applied toward just about any dividend growth stock you’ll run across.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

American Water Works Company Inc. (AWK)

American Water Works Company Inc. (AWK)

American Water Works Company Inc. (AWK) is a utility company that provides water and wastewater services in the United States.

Founded in 1886, American Water Works is now a $24 billion (by market cap) water utility giant that employs more than 6,000 people.

American Water Works provides its water (approximately 93% of FY 2022 revenue) and wastewater (approximately 7% of FY 2022 revenue) services to roughly 14 million people across 14 different states.

By customers, this is the largest publicly-traded water and wastewater utility in the US.

The company’s main segment is Regulated Businesses, which accounted for 92% of FY 2022 revenue and comprises the core water and wastewater utility operations.

A small component of the company is unregulated, serving 18 different military installations on long-term (usually 50 years) contracts.

American Water Works is, essentially, a regulated water and wastewater utility business that primarily serves residential and commercial customers.

While it might not feature explosive growth prospects, this can still be a highly appealing long-term investment.

The main reason?

Well, it comes down to what that American Water Works is providing to millions of customers.

That what is something I’d call “liquid gold”.

Whereas oil had that moniker for the last century, water may take it for the next century.

I say that because we can’t live without water.

It’s our most precious resource.

And, for a variety of reasons, it’s becoming more expensive and difficult to get it.

There are all kinds of things that one could live without in a modern-day society.

Maybe one wouldn’t like to live without things like a smartphone or internet access.

But one literally cannot survive without water.

However, because the business is heavily regulated, American Water Works cannot take unfair advantage of the situation and charge its customers whatever price it comes up with.

There is a lid on the price the company can charge for a resource with ceaseless demand.

Indeed, the company estimates that its monthly water bill to its customers is less than 1% median household income.

When you charge a low price for something so vital, the value proposition is extremely high.

Reliably providing a precious and required resource at a low cost is why American Water Works has been around for more than a century, and it’s also why the company should be able to continue increasing its revenue, profit, and dividend for many, many years into the future.

Dividend Growth, Growth Rate, Payout Ratio and Yield

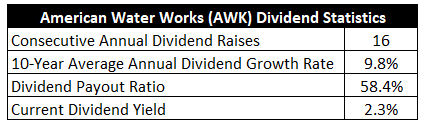

To date, the company has increased its dividend for 16 consecutive years.

The 10-year dividend growth rate is 9.8%.

There’s been a minor deceleration in dividend growth of late, but American Water Works has consistently increased its dividend at a high-single-digit (8%+) rate.

Along with that dividend growth, the stock yields a market-beating 2.3%.

Along with that dividend growth, the stock yields a market-beating 2.3%.

This yield, by the way, is 70 basis points higher than its own five-year average.

With a payout ratio of 58.4%, backed further by a product that must be consumed for life, this dividend is about as safe as it gets.

Very solid dividend metrics here.

Good yield, strong growth, and plenty of safety.

Revenue and Earnings Growth

As solid as these dividend metrics may be, though, the numbers are mostly looking into the past.

However, investors much always be thinking about the future, as capital of today is being put on the line for the rewards of tomorrow.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be of great use when the time comes to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Fusing the proven past with a future forecast in this way should give us enough information to roughly gauge where the business could be going from here.

American Water Works advanced its revenue from $2.9 billion in FY 2013 to $3.8 billion in FY 2022.

That’s a compound annual growth rate of 3.1%.

Fairly middling top-line growth here.

But much of it can be explained by a dip in FY 2022 revenue, which was due to the company’s decision to sell its Homeowner Services Group unit, a warranty and homeowner services business, for nearly $1.3 billion in late 2021.

The company’s most recent quarter showed an 8.3% YOY gain in revenue, and that may be more indicative of what’s actually occurring.

Meanwhile, earnings per share grew from $2.06 to $4.51 over this 10-year period, which is a CAGR of 9.1%.

Now, the company did record a one-time gain in FY 2022 (from the HSG sale), but this doesn’t seem far off from what American Water Works has been producing over longer stretches of time.

The company has been mildly dilutive with its shares over the last decade, but a nice expansion in margins has really helped to drive some excess bottom-line growth.

Looking forward, CFRA believes that American Water Works will compound its EPS at an annual rate of 8% over the next three years.

That’s a very reasonable take on things.

American Water Works has repeatedly publicized its long-term targets that include 7% to 9% CAGRs for EPS and the dividend.

CFRA is simply splitting the middle here, and I think that’s an appropriate stance.

Backing this view up is recent guidance from American Water Works – $4.77 in EPS (at the midpoint) for FY 2023, and $5.15 in EPS (at the midpoint) for FY 2024.

That $5.15 number is almost exactly 8% YOY growth (compared to FY 2023 midpoint guidance).

What is helpful to keep in mind about American Water Works, which totally differentiates it from a gas/electric utility, is that it’s not limited to a geographic footprint.

American Water Works is employing the serial acquirer playbook to slowly consolidate the industry, expand its reach, and build out a water and wastewater empire.

It routinely acquires smaller municipal water and wastewater systems, such as the recent City of Donahue’s water and wastewater systems for nearly $1.8 million.

In fact, American Water Works completed 26 regulated acquisitions in 2022 alone.

So you have what’s already a powerful business model (providing a resource people literally can’t live without), and then you’re adding to it the powerful serial acquirer model.

Being able to stretch out, geographically, while still maintaining those localized monopolies, is what makes this business much more appealing, in my view, than a power utility business.

I’m willing to accept this 8% growth mark at face value and use that as my base case.

That sets up American Water Works for like dividend growth, and you’re starting that dividend growth journey off with a 2%+ yield.

Assuming no detrimental change in valuation, that positions shareholders for ~10% annualized total returns from here.

On a business with incredible revenue visibility from locked-in customers with no competitive alternatives, I think that’s rather appealing.

Financial Position

Moving over to the balance sheet, the company has an okay financial position.

Like pretty much every other utility out there, American Water Works is heavily leveraged.

The long-term debt/equity ratio is 1.4, while the interest coverage ratio is approximately 3.5.

Its senior unsecured debt gets investment-grade credit ratings: A, S&P Global; Baa1, Moody’s.

I’d say the balance sheet is the one glaring blemish for me, which is a similar case for all utilities.

But American Water Works can safely carry a lot of debt, due to the annuity-like stream of its revenue.

This is as close as it gets to a “recession-proof” business.

Profitability is decently robust for a utility.

Return on equity has averaged 12.1% over the last five years, while net margin has averaged 21.7%.

ROE is juiced by the debt, so keep that in mind.

Notably, net margin was closer to 14% at the start of the last decade.

Overall, there’s a lot to like about this business as a long-term investment.

Upgrading aging infrastructure, passing on higher fees, and adding inorganic growth through acquisitions are easy growth levers to pull over the coming years.

And with economies of scale, localized monopolies, high barriers to entry, regulatory support for profit recovery, and entrenched infrastructure, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

This is a rare business with, essentially, no competition in its service network.

Regulation is a double-edged sword; regulation caps profit (to eliminate the possibility of price gouging), but regulators put a floor under the business by allowing a recouping of investments through higher service fees to customers.

The company’s acquisitive behavior requires management to be prudent around purchase pricing.

There are execution risks stemming from the integration of acquisitions.

Accessing water, due to natural changes, may become increasingly challenging and difficult for the company over time.

I see some risks worth weighing, but the overall risk profile of the business seems more than acceptable.

And with the stock down 35% from all-time highs, the valuation also looks more than acceptable…

Valuation

The stock is trading hands for a P/E ratio of 25.3.

In absolute terms, that’s actually not super appealing.

However, water utilities have alluring durability, resiliency, and visibility of revenue.

And that high degree of confidence in growth has allowed the stocks to command premium multiples over the years.

This stock’s own five-year average P/E ratio is 33.2.

In light of that, relative to itself, the stock actually looks cheap.

The cash flow multiple of 13.7 is also well off of its own five-year average of 18.9.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

That growth rate is as high as I’ll go, but it fits perfectly here.

The company’s long-term guidance, which it’s living up to, calls for 8% annual EPS and dividend growth (at the midpoints, respectively).

Also, the near-term forecast from CFRA calls for American Water Works to compound its EPS at an 8% annual rate over the next few years.

And the company’s long-term demonstrated EPS and dividend growth have both been over the 9% level.

Nothing is guaranteed in life or business, but it seems awfully likely that American Water Works (which has been around for more than a century) will continue growing its profit and dividend at a high-single-digit rate for many years to come.

The DDM analysis gives me a fair value of $152.82.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think my model was sensible enough, yet the stock comes out looking cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates AWK as a 4-star stock, with a fair value estimate of $142.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates AWK as a 3-star “HOLD”, with a 12-month target price of $143.00.

I came out a bit high, but we’re all in the same neighborhood here. Averaging the three numbers out gives us a final valuation of $145.94, which would indicate the stock is possibly 16% undervalued.

Bottom line: American Water Works Company Inc. (AWK) has something close to a “recession-proof” business, providing customers with a precious resource they literally can’t live without. Continued consolidation, infrastructure upgrades, and steady rate increases nearly guarantee more growth for years to come. With a market-beating yield, high-single-digit dividend growth, a moderate payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 16% undervalued, long-term dividend growth investors looking for a sleep-well-at-night investment with highly recurring revenue ought to consider this business.

Bottom line: American Water Works Company Inc. (AWK) has something close to a “recession-proof” business, providing customers with a precious resource they literally can’t live without. Continued consolidation, infrastructure upgrades, and steady rate increases nearly guarantee more growth for years to come. With a market-beating yield, high-single-digit dividend growth, a moderate payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 16% undervalued, long-term dividend growth investors looking for a sleep-well-at-night investment with highly recurring revenue ought to consider this business.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is AWK’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 70. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, AWK’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I have no position in AWK.