There are so many different investment methods and asset choices out there, which is a good problem to have.

One could commit to slowly amassing a real estate empire, renting out properties and earning a steady income.

One can hoard precious metals, such as gold and silver, although it’s difficult to generate income that way.

There’s also fixed-income choices, such as CDs and bonds.

Some good ideas here, but I think there’s one strategy that rises above them all.

It’s dividend growth investing.

This long-term investment strategy advocates buying and holding shares in high-quality businesses that reward shareholders with safe, growing dividends.

You can find hundreds of examples of what I mean by taking a look at the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

This strategy simply makes sense.

This strategy simply makes sense.

Businesses that can actually afford to pay growing dividends are producing growing profits.

Well, only great businesses can reliably produce growing profits in a consistent way over long periods of time.

And great businesses tend to perform better than lousy businesses over the long run.

So it’s a source of steadily rising passive income and outperformance.

This explains why I’ve been personally using the strategy for more than a decade now, letting it guide me as I’ve built out my FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

Indeed, I’ve been in the fortunate position of being able to live off of dividends for many years now.

This position allowed me to retire in my early 30s.

This position allowed me to retire in my early 30s.

My Early Retirement Blueprint shares how I was able to accomplish such a thing.

While strategy was vital to my success, it’s not all.

There’s also valuation at the time of making any investment.

Price is only what you pay, but it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

There are as many ways to invest and make money as there are ways to skin a cat, but buying high-quality dividend growth stocks when they’re undervalued might just be the very best way to invest over the long run.

Of course, recognizing and taking advantage of undervaluation first requires one to have a basic understanding of valuation.

No problem.

Fellow contributor Dave Van Knapp penned Lesson 11: Valuation in order to assist with this quandary.

Part of a comprehensive series of “lessons” on dividend growth investing, it succinctly lays out a valuation template that can be easily applied toward just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Discover Financial Services (DFS)

Discover Financial Services (DFS)

Discover Financial Services (DFS) is an American financial services company.

Founded in 1985, Discover Financial is now a $27 billion (by market cap) major financial services player that employs more than 20,000 people.

The company reports results across two business segments: Digital Banking, 98% of FY 2023 revenue; and Payment Services, 2%.

On one hand, Discover Financial might look like a bank.

And, in a way, that’s exactly what it is.

Traditionally speaking, that’s been a pretty good business model.

Banks have been around for thousands of years, showing a rare kind of long-lasting resiliency in the business world.

Without an organized way to handle commerce, which banks carry out, our society doesn’t really function.

Banks fill a necessary role, and they make plenty of money in so doing.

Not only that, but banks make money from other people’s money.

This occurs through the float, which is the low-cost, low-risk source of capital that accrues to a bank via deposits.

Take in money at one rate, lend at a higher rate, earn from the spread.

Not too shabby.

Discover Financial does this, except it takes the idea to the next level by operating totally digitally.

The company boasts $84 billion in direct-to-consumer deposits.

Going direct as a digital bank reduces overhead.

And that’s only part of it – the “next level”, in this case, goes beyond this one step.

Discover Financial has also bolted a digital payment network on top of the digital bank.

In fact, Discover Financial operates one of the world’s four major payment networks, putting it in an exclusive (and profitable) club.

Its Discover Network processed $263 billion in volume in FY 2022.

The world is increasingly becoming cashless as people gravitate toward using digital payments.

This secular trend directly benefits Discover Financial.

While the Payment Services business segment is quite small on paper for Discover Financial, I’d argue that it’s more vital than it initially seems.

A symbiotic and harmonious business model has been designed where the networks feeds into the Digital Banking side of the business by creating customers, transactions, and loans (via credit card balances).

Since Discover Financial has no physical footprint, its Payment Services segment serves as a major gateway into the company’s fold.

Discover Financial operates two businesses that are independently powerful, but it splices them together in a highly complementary manner that allows for intelligent customer acquisition and retention.

This one-two punch is why the company is set up so well to continue growing its revenue, profit, and dividend for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

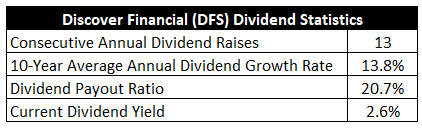

Already, Discover Financial has increased its dividend for 13 consecutive years.

While it’s not the longest track record out there, Discover has gotten off to a very nice start.

The 10-year dividend growth rate is 13.8%.

Better yet, there’s actually been a recent acceleration in dividend growth, with the most recent divided raise coming in at 16.7%.

Along with this double-digit dividend growth, the stock offers a market-beating 2.6% yield.

That’s awfully compelling, as you don’t often see a yield this high paired with a dividend growth rate this high.

This yield, by the way, is 30 basis points higher than its own five-year average.

This yield, by the way, is 30 basis points higher than its own five-year average.

And with a payout ratio of just 20.7%, this is an extremely healthy dividend with plenty of coverage.

Nobody dislikes a fast-growing dividend, but the trade-off is usually a low yield.

In this case, you get a pretty respectable yield to go along with the fast growth.

Again, it’s quite compelling.

Revenue and Earnings Growth

As compelling as it all may be, though, these metrics are largely looking backward.

However, investors must always be looking forward, as today’s capital is being risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be instrumental for estimating intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this manner should give us the information we need to roughly gauge what the future growth path of the business might look like.

Discover Financial moved its revenue from $9.4 billion in FY 2013 to $15.2 billion in FY 2022.

That’s a compound annual growth rate of 5.5%.

Solid.

I like to see at least a mid-single-digit top-line growth rate from a fairly mature company.

Discover Financial delivered.

Meanwhile, earnings per share grew from $4.96 to $15.50 over this period, which is a CAGR of 13.5%.

We have a lot of excess bottom-line growth here, which can be explained by the company’s prolific usage of share buybacks.

The outstanding share count has been reduced by an incredible 43% over the last decade.

That cannibalization of shares is remarkable.

Seeing as how the stock has typically commanded low multiples and been priced lower than it is today over the last decade, I’d say this has been a good move.

Also, we can now see how well EPS and dividend growth line up over the last decade.

The two growth rates are nearly the same, showing excellent control by management.

Looking forward, CFRA currently has no three-year forecast for Discover Financial’s EPS CAGR.

That’s unfortunate, as I do like to line up the proven past against a future forecast in order to better flesh out a possible growth trajectory.

Discover Financial is going through a bit of a tough patch right now.

The company reported last year that prior card misclassifications required the company to provide refunds to merchants and merchant acquirers, which resulted in a pause in share buybacks while the company reviewed its compliance management.

There was then the sudden departure of longtime CEO Roger Hochschild.

Furthermore, Discover Financial has been wrangling with elevated credit loss provisions and charge-off rates for several quarters.

That said, all of this is temporary and not indicative of some kind of actual business model problem.

I’d expect modest, if any, EPS growth over the very near term.

In fact, recent EPS numbers have been significantly down on a YOY basis.

However, long-term investors should never be focused on the near term.

Thanks to a low payout ratio, the company could afford to hand out solid (say, mid-single-digit) dividend increases over the next year or two while it moves past some of the near-term headwinds.

Said another way, relatively modest dividend growth could easily play out while EPS growth temporarily stalls out.

Once the business normalizes and is on the other side of some compliance missteps, it seems very possible, if not likely, that low-double-digit EPS and dividend growth returns.

That might seem rosy.

Maybe, maybe not.

Either way, Discover Financial doesn’t need to deliver on something like that.

The expectations being built in, based on the multiples, are extremely low, and even just high-single-digit growth would be enough to set shareholders up for nice returns over the years ahead.

If, on the other hand, the company can get back to what it was doing before, a combination of growth and multiple expansion could unleash powerful results over the next decade.

Financial Position

Moving over to the balance sheet, the company appears to have a good financial position (although it’s extremely difficult to read a bank’s complex balance sheet).

The long-term debt/equity ratio is 1.4.

The parent company’s senior debt has the following credit ratings: Baa2, Moody’s; BBB-, S&P; BBB+, Fitch.

While these are investment-grade credit ratings, they’re near the lower end of that spectrum.

By design, Discover Financial runs on leverage.

Any kind of cascading of charge-off rates could be a real problem here, and that’s something to watch.

For the most recent quarter, Discover Financial’s net credit card charge-off rate was 4.7% (up approximately 230 basis points YOY).

That’s relatively high.

Of the four major card issuers, Discover Financial appears to consistently have the lowest credit quality of the bunch, which is probably my biggest concern about this company long term.

On the other hand, profitability for the firm is fairly robust.

Return on equity has averaged 29.4% over the last five years, while net margin has averaged 27.3%.

Net interest margin was 11% for FY 2022.

Discover Financial is routinely putting up high returns on capital, which I love to see.

With two complementary business models that accentuate one another, Discover Financial is a very interesting long-term investment idea.

And with “sticky” bank deposits, brand power, an entrenched float, a built-out payment network, and implied switching costs for cardholders, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

As we saw in early 2023, bank runs are a major risk for all banks; however, Discover Financial is somewhat insulated from this because of the payments side of the house.

Banks are highly exposed to economic cycles; a recession could hurt the bank through reduced deposits and loan demand on the income statement, as well as higher credit losses on the balance sheet.

A recession would also likely reduce spending, in general, which could negatively impact card transactions and the associated fees.

Discover Financial usually runs higher charge-off rates than some of its card-issuing peers, indicating persistent credit quality issues.

Recent compliance problems show governance cracks.

The company is exposed almost completely to only the US, with the network’s lack of an international footprint limiting long-term growth potential.

I see some risks worth considering, but the risks are only one part of the puzzle.

Another big part of the puzzle is the valuation, which appears to be surprisingly low right now…

Valuation

This stock is on the market for a P/E ratio of 9.6.

Whenever I see a single-digit P/E ratio, my attention is captured.

To be fair, this is a stock that routinely gets assigned low multiples.

For perspective on that, its own five-year average P/E ratio is 9.9.

Still, we are currently below that already low level.

Also, the P/B ratio of 1.7 is quite a bit lower than its own five-year average of 2.3.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

That growth rate isn’t as high as I can go, but it is on the higher end of the scale.

It doesn’t seem at all unreasonable.

This is a company that has reliably increased its dividend at a low-double-digit rate for a decade, and the payout ratio is low enough for that to continue for years to come – even absent much near-term EPS growth.

Keep in mind, this is a long-term average.

I wouldn’t be surprised to see a few lackluster dividend raises over the next year or two.

But I’d expect the dividend growth rate to pick back up again after we get through a rough patch.

If anything, a high-single-digit long-term growth rate is setting the bar pretty low for this company.

It wouldn’t really take much for Discover Financial to return to low-double-digit dividend growth over the coming years, blowing the doors off of the model.

However, I’d rather err on the side of caution, as I do acknowledge persistent credit quality issues at the firm.

The DDM analysis gives me a fair value of $120.40.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Even after an easy, cautious take on the valuation, the stock looks slightly undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates DFS as a 4-star stock, with a fair value estimate of $141.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates DFS as a 4-star “BUY”, with a 12-month target price of $125.00.

I came out a bit low. Averaging the three numbers out gives us a final valuation of $128.80, which would indicate the stock is possibly 16% undervalued.

Bottom line: Discover Financial Services (DFS) is running two business models that are powerful on their own, but the firm has put them together in a very symbiotic, complementary way. With a market-beating yield, a low payout ratio, double-digit dividend growth, more than 10 consecutive years of dividend increases, and the potential that shares are 16% undervalued, long-term dividend growth investors looking for a cheap gem in the market may have a great investment opportunity here.

Bottom line: Discover Financial Services (DFS) is running two business models that are powerful on their own, but the firm has put them together in a very symbiotic, complementary way. With a market-beating yield, a low payout ratio, double-digit dividend growth, more than 10 consecutive years of dividend increases, and the potential that shares are 16% undervalued, long-term dividend growth investors looking for a cheap gem in the market may have a great investment opportunity here.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is DFS’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 45. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, DFS’s dividend appears Borderline Safe with a moderate risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long DFS.