Successful long-term investing need not be complicated.

Investing is really all about laying out and risking capital today for more capital tomorrow.

Capital gets invested in something that should earn a satisfactory rate of return over a specified period of time.

All well and good, but that “something” is what ends up confounding a lot of people.

Fortunately, there are great investment ideas all around us.

Just take a look at the world.

There are great businesses everywhere – the businesses providing you with food, electricity, technology, etc.

By providing you (and many, many other people) with certain products and/or services, these businesses tend to make a lot of money.

So much money, in fact, that these businesses end up returning some of that money directly back to shareholders… in the form of cash dividends.

And not just dividends but growing dividends (because the profits are also growing).

And not just dividends but growing dividends (because the profits are also growing).

You can see what I mean by taking a look at the Dividend Champions, Contenders, and Challengers list.

This list has important data on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

If growing profit and a growing dividend are a good initial litmus test for business quality (and I believe that to be the case), this list is an excellent quality screener.

Every stock on the list conforms to the dividend growth investing strategy, which is a strategy whereby one buys and holds shares in high-quality businesses that pay reliable, rising dividends.

I’ve been personally using this strategy for more than a decade now.

It’s guided me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

In fact, I’ve been fortunate enough to be able to live off of dividends for years now.

I even retired in my early 30s.

I even retired in my early 30s.

And my Early Retirement Blueprint explains how I was able to do that.

Suffice it to say, living below my means and consistently investing my hard-earned savings into high-quality dividend growth stocks has been key to my success.

But it’s more than just picking the right businesses.

There’s also picking the right valuations.

Whereas price is what you pay, it’s value that you actually get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Successful long-term investing can be as simple as buying high-quality dividend growth stocks when they’re undervalued, holding for decades, and reinvesting those growing dividends along the way.

Of course, as simple as that may sound, the undervaluation part of the equation requires one to first have some kind of understanding of how to go about valuing businesses.

No worries.

My colleague Dave Van Knapp put together Lesson 11: Valuation in order to help with this.

Part and parcel of an overarching series of “lessons” on dividend growth investing, it helps to simplify valuation by providing an easy-to-use valuation template.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Skyworks Solutions Inc. (SWKS)

Skyworks Solutions Inc. (SWKS)

Skyworks Solutions Inc. (SWKS) is an analog and mixed-signal semiconductor company focusing on cellular system solutions that enable wireless connectivity.

Founded in 1962, Skyworks Solutions is now a $17 billion (by market cap) tech titan that employs nearly 10,000 people.

Approximately two-thirds of the company’s revenue comes from the US, whereas the other one-third is derived from international markets (primarily China, Taiwan, and South Korea).

This is a global company with 18 design centers, 15 sales offices, and six manufacturing sites.

Skyworks Solutions produces a large range of components that are used in various electronic devices.

Its extensive product portfolio includes: amplifiers, attenuators, diodes, filters, mixers, modulators, switches, and voltage regulators.

It provides these products to more than 6,000 different customers.

While it is diversified in terms of products and customers, the majority of the company’s revenue is sourced from mobile devices that require products to enable wireless connectivity (i.e., RF).

Skyworks Solutions is one of the world’s RF leaders, and the increasing complexity of smartphones and networks leads to the requirement for more advanced content per device.

Plus, the world is demanding more and more devices that are interconnected (i.e., IoT) through high-speed networks (such as 5G).

More devices requiring more advanced content per device is a powerful one-two demand punch for Skyworks Solutions over the coming years, which should lead to a multiyear tailwind for the company and its vast suite of products.

And that should lead to lots of continued growth across its revenue, profit, and dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

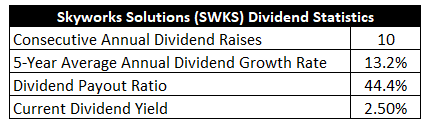

To date, the company has increased its dividend for 10 consecutive years.

With a five-year dividend growth rate of 13.2%, the company is off to a very nice start here.

The dividend has been reliably growing at a high-single-digit to low-double-digit rate, and the most recent dividend raise of 9.7% is more evidence of that.

Along with that growth, the stock offers a market-beating 2.5% yield.

Along with that growth, the stock offers a market-beating 2.5% yield.

If you can line up a 2.5% yield and ~10% dividend growth, you’re sitting pretty.

This yield, by the way, is 70 basis points higher than its own five-year average yield.

The fairly large, fast-growing dividend is protected by a healthy payout ratio of 44.4%.

Just solid stuff right across the board.

You get yield, growth, and safety.

Great dividend metrics, and something to like for everyone.

Revenue and Earnings Growth

As great as these dividend metrics are, though, these numbers are mostly using data from the past.

However, investors must always be thinking about the future, as today’s capital is being risked for the rewards of tomorrow.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful for when the time comes to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this way should give us enough information to make an educated decision on what the business’s future growth path could look like.

Skyworks Solutions advanced its revenue from $2.3 billion in FY 2014 to $4.8 billion in FY 2023.

That’s a compound annual growth rate of 8.5%.

I usually look for a mid-single-digit top-line growth rate from an established business like this, and Skyworks Solutions more than delivered.

Meanwhile, earnings per share grew from $2.38 to $6.13 over this period, which is a CAGR of 11.1%.

That’s strong.

We can now see how double-digit dividend growth has been powered by double-digit bottom-line growth.

The two numbers line up well, indicating deft control by management.

Consistent buybacks helped to propel excess EPS growth, with the outstanding share count down by 17% over the last decade.

Hard to fault any of this.

Skyworks Solutions isn’t producing explosive growth, but it’s been consistently great over the last decade (although the pandemic did result in a temporary boost).

Looking forward, CFRA is forecasting that Skyworks Solutions will compound its EPS at an annual rate of 8% over the next three years.

While that is a slight deceleration in growth relative to what’s transpired over the last decade, I think it’d still be a welcome outcome for long-term shareholders.

Keep in mind, the 11.1% 10-year EPS CAGR from Skyworks Solutions was improved by a temporary increase in demand, which resulted from a number of pandemic-specific events.

CFRA does a pretty good job of highlighting the positives with this passage: “Still, we like secular prospects in broad markets, on greater penetration across the automotive, infrastructure, and industrial markets, as well as the shift to WiFi 6E and 7.”

On the other hand, CFRA notes: “High customer concentration remains a risk while new customer wins within the Android ecosystem are likely to come a lower margin. Although Mobile has benefited from the shift to 5G by smartphone makers (higher RF content), growth will be limited as 5G mobile adoption gains have largely taken place.”

This sums it up well.

Although Skyworks Solutions has an extremely deep and broad product portfolio, the company is largely reliant on sales of smartphone components (especially RF).

Moreover, Skyworks Solutions is further concentrated by customer: Apple Inc. (AAPL) accounts for approximately 60% of revenue.

Thus, Skyworks Solutions is largely a play on the iPhone – a highly successful play for many years.

But the key risk with that is, Apple continues to vertically integrate in every possible way.

As Apple looks to bring more manufacturing and products in-house, Skyworks Solutions could see its growth and margins erode as it gets cut out.

A victim of its own success, perhaps, but winning new customers, developing new products, and tackling new applications will be crucial for Skyworks Solutions over the coming years.

Indeed, I see the broadening out of the business as the linchpin of future success.

To this end, management has been taking the right steps to diversify end markets, with the $2.8 billion deal for the Infrastructure & Automotive business of Silicon Laboratories (SLAB) in 2021 being a perfect example of this.

Summing it all up, I don’t see anything to indicate that CFRA’s near-term growth projection is unrealistic.

If 8% annual EPS growth is achieved over the next few years, that would easily line up the dividend for similar growth.

When starting off with a 2.5% yield, you’ve got a compelling package of yield and growth here.

As long as multiples don’t compress, this is a 10%+ annualized total return setup.

Financial Position

Moving over to the balance sheet, the company has a fantastic financial position.

The long-term debt/equity ratio is 0.2, while the interest coverage ratio is nearly 18.

While these ratios are great, they don’t do full justice to the health of the balance sheet.

Skyworks Solutions ended FY 2023 with about $260 million in net long-term debt, which is relatively minuscule for a $17 billion company.

Profitability is outstanding.

Return on equity has averaged 23.7% over the last five years, while net margin has averaged 25.4%.

Skyworks Solutions has high returns on capital, which I love to see.

This is an impressive business.

And with economies of scale, IP, R&D, and technological know-how, the company does benefit from durable competitive advantages.

Potential Risks

Of course, there are risks to consider.

Competition, regulation, and litigation are omnipresent risks in every industry.

I see customer concentration as the biggest risk of all, as Skyworks Solutions is heavily reliant on sales to one company (Apple) which is actively trying to cut out external suppliers.

The adoption of 5G has mostly played out, leaving the company with less near-term growth potential from this opportunity.

The company is taking steps to diversify the business, but these steps add uncertainty and execution risks.

A global sales footprint exposes the company to currency exchange rates and geopolitics.

The very business model is a risk unto itself, and the company must stay ahead of the tech curve in order to not get left behind.

There are definitely some risks to consider, but the growth and quality profile of the business must also be considered.

And with the stock down nearly 50% from all-time highs, the attractive valuation is important to consider…

Valuation

The stock is trading hands for a P/E ratio of 17.6.

That is ultra reasonable in the land of tech, where P/E ratios of 30 and over are not uncommon at all.

It’s quite a bit lower than the broader market’s earnings multiple.

It’s also below the stock’s own five-year average P/E ratio of 18.9.

The sales multiple of 3.6 is below its own five-year average of 4.8.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

That dividend growth rate isn’t as high as I’ll go, and I actually usually go higher for fast-growing tech businesses.

With double-digit EPS and dividend growth demonstrated by the company over the last decade, as well as a near-term forecast for high-single-digit EPS growth, this looks cautious.

Well, it is cautious, and that’s because of the overreliance on a single customer that is, arguably, antagonistic.

The diversification efforts are laudable, but it remains to be seen how that’ll play out.

It’s certainly possible that Skyworks Solutions does better than this over the coming years, and I’d welcome the upside surprise, but I’d rather err on the side of caution.

The DDM analysis gives me a fair value of $116.96.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I put together pretty modest assumptions, yet the stock looks underpriced anyway.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates SWKS as a 4-star stock, with a fair value estimate of $133.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates SWKS as a 3-star “HOLD”, with a 12-month target price of $100.00.

I came out right in the middle this time around. Averaging the three numbers out gives us a final valuation of $116.65, which would indicate the stock is possibly 8% undervalued.

Bottom line: Skyworks Solutions Inc. (SWKS) is a high-quality tech firm that is taking laudable steps to diversify the business, and it might be one of the very last reasonably priced tech names out there. High returns on capital and a strong balance sheet give me a lot of enthusiasm about this idea. With a market-beating yield, double-digit long-term dividend growth, a healthy payout ratio, 10 consecutive years of dividend increases, and the potential that shares are 8% undervalued, long-term dividend growth investors looking to up their tech exposure without overpaying should be looking at this name.

Bottom line: Skyworks Solutions Inc. (SWKS) is a high-quality tech firm that is taking laudable steps to diversify the business, and it might be one of the very last reasonably priced tech names out there. High returns on capital and a strong balance sheet give me a lot of enthusiasm about this idea. With a market-beating yield, double-digit long-term dividend growth, a healthy payout ratio, 10 consecutive years of dividend increases, and the potential that shares are 8% undervalued, long-term dividend growth investors looking to up their tech exposure without overpaying should be looking at this name.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is SWKS’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 68. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, SWKS’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I have no position in SWKS.