Investors are always on the lookout for “cheap” stocks that may have more upside not solely based on an affordable price tag but fundamental value as well.

When the risk to reward is right, strengthening prospects of stocks like this is often hard to overlook and here are three companies that are making this case right now.

Direct Digital (DRCT)

Among the consumer discretionary sector, advertising and marketing technology company Direct Digital is attractive with its stock sporting a Zacks Rank #1 (Strong Buy). Trading around $13 a share, investors may want to take notice of Direct Digital’s expansion with high double-digit percentage growth forecasted on the company’s top and bottom lines in fiscal 2024.

Direct Digital is expected to round out its current FY23 with earnings up 194% to $0.50 per share versus $0.17 a share in 2022. This year’s projections of 43% EPS growth is very compelling as Direct Digital’s top line has continued to accelerate as well. Illustrating Direct Digital’s future earnings potential is that total sales are projected to soar 107% in FY23 and climb another 32% in FY24 to $240.39 million.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

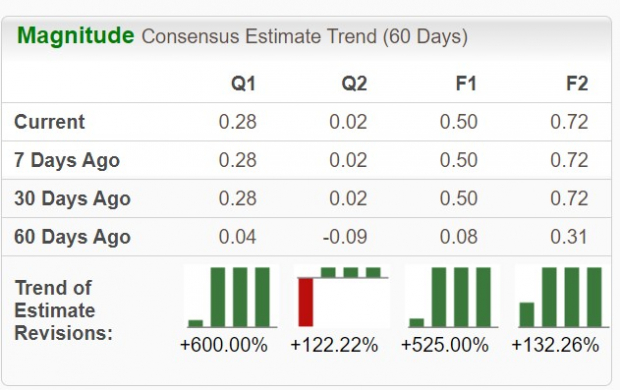

At a 17.5X forward earning multiple investors aren’t paying an over-the-top premium for Direct Digital’s market share-taking expansion. Furthermore, the fact that FY23 and FY24 earnings estimate revisions have skyrocketed 525% and 132% over the last 60 days respectively; bolsters the notion that advertising-related businesses may do very well as inflation continues to ease.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Vaalco Energy (EGY)

Just under $5, Vaalco Energy’s stock also sports a Zacks Rank #1 (Strong Buy) and is a very intriguing pick out of the energy sector as an independent energy company engaged in the acquisition of crude oil and natural gas. Vaalco’s outlook suggests its penny stock status could be short-lived as FY24 EPS is projected at $1.49 per share which would be a strong rebound from end-of-year estimates of $0.35 a share for FY23.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

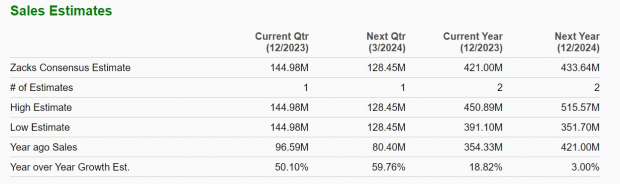

Vaalco Energy looks extremely undervalued at what is just a 3.1X forward earnings multiple based on FY24 EPS projections and the company’s 1.2X price-to-sales valuation is attractive as well. To that point, total sales are now forecasted to jump 19% in FY23 and rise another 3% in FY24 to $433.64 million.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Grifols (GRFS)

We’ll round out this list in the medical sector with Grifols, a Spain-based healthcare company. Sporting a Zacks Rank #2 (Buy) Grifols has a unique niche as a global specialty pharmaceutical company that develops a broad range of biological medicines based on plasma-derived proteins.

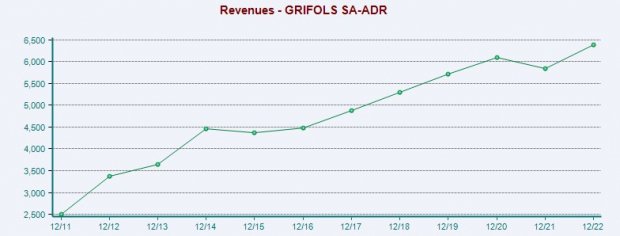

With its stock trading around $11, Grifols’ steady top-line growth and increased profitability are certainly attractive. Grifols is expected to end FY23 with total sales up 10% to $7.03 billion and FY24 sales are projected to leap another 8%. More importantly, Grifols’ EPS is anticipated at $0.69 per share in FY23 and up 109% from $0.33 a share in 2022. Grifols stock trades attractively at 9.7X forward earnings as FY24 EPS is expected to leap another 67% to $1.16 per share.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Bottom Line

These stocks are starting to look fundamentally undervalued at the beginning of the year which supports their attractive price tags. From their current levels, it would be no surprise if Direct Digital, Vaalco Energy, and Grifols’ stock moved much higher in 2024.

— Shaun Pruitt

Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks