High-quality dividend growth stocks are some of the best stocks in the world. That’s because these stocks represent equity in some of the best businesses in the world. You can’t run a terrible business while simultaneously paying out ever-larger cash dividends to shareholders. It doesn’t work like that.

No, a business has to be great in order to generate the ever-higher profit necessary to afford ever-larger dividends.

These stocks can make for excellent long-term investments. But when they’re on sale – when they’re undervalued – that’s when things can be even more excellent.

See, price and yield are inversely correlated. All else equal, lower prices result in higher yields.

This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach. Now, lower valuations often come when there’s volatility. But I always see short-term volatility as a long-term opportunity.

With all of that out of the way, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what this article is all about. Today, I want to tell you my top five dividend growth stocks for January 2024.

Ready? Let’s dig in

My first dividend growth stock for January 2024 is Air Products & Chemicals (APD). Air Products & Chemicals is a major global producer and supplier of industrial gases. There are so many things to like about this business. I’ll quickly highlight just three.

First, industrial gases are critical input for the manufacturing processes of many different end products ranging from electronics to vehicles. Second, because of the critical nature of these industrial gases, and because constant and reliable access to these gases is a must, a manufacturer will set up a long-term contract with a dependable provider of said gases. Third, Air Products & Chemicals is part of a global oligopoly – only three major companies in this space control the vast majority of the global market share.

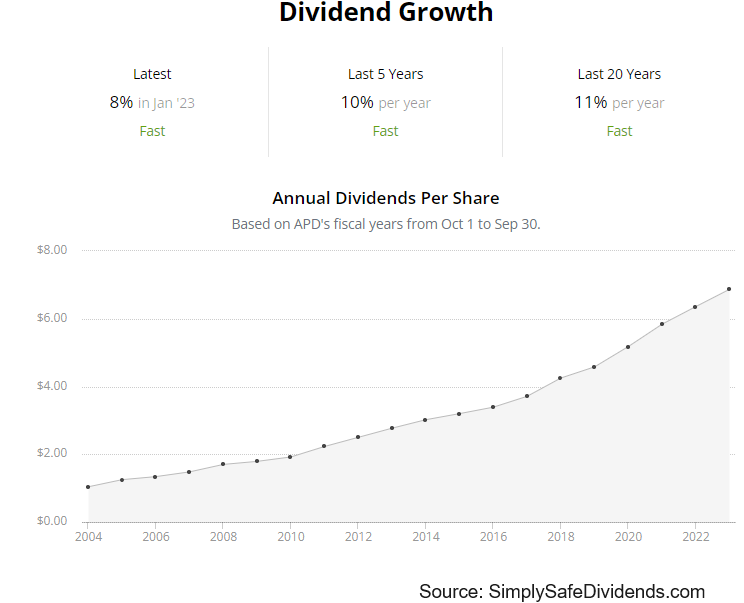

This is why Air Products & Chemicals has compounded its revenue at an annual rate of 2.2% and its EPS at an annual rate of 9.4% over the last decade. The dividend growth story here is remarkable.

With 41 consecutive years of dividend increases, this is a vaunted Dividend Aristocrat. The consistency is really something else. The 10-year dividend growth rate is 9.8%, and the dividend raises have been in a high-single-digit range, year after year, like clockwork.

Plus, the stock yields 2.6%. That’s a very respectable yield, especially for this level of dividend growth. And the payout ratio of 54.1%, based on FY 2024 adjusted EPS guidance, indicates nothing but a healthy dividend poised for more growth ahead.

Plus, the stock yields 2.6%. That’s a very respectable yield, especially for this level of dividend growth. And the payout ratio of 54.1%, based on FY 2024 adjusted EPS guidance, indicates nothing but a healthy dividend poised for more growth ahead.

This Dividend Aristocrat looks very attractive right now. Most of the multiples are well off of their respective recent historical averages. Take the earnings multiple, for instance. It’s 26.5. Its own five-year average is 29. And so it goes on down the line. We recently put together a full analysis and valuation video on this great business, and the fair value estimate came out to nearly $343/share. The stock is currently priced at about $273. A sizable disconnect on an oligopolistic business with numerous competitive advantages. Take a look.

My second dividend growth stock for January 2024 is Brown & Brown (BRO). Brown & Brown is an insurance brokerage firm. I just love Brown & Brown. First of all, it’s in insurance. But it doesn’t underwrite risk. It’s not a traditional insurer. Instead, it’s a brokerage.

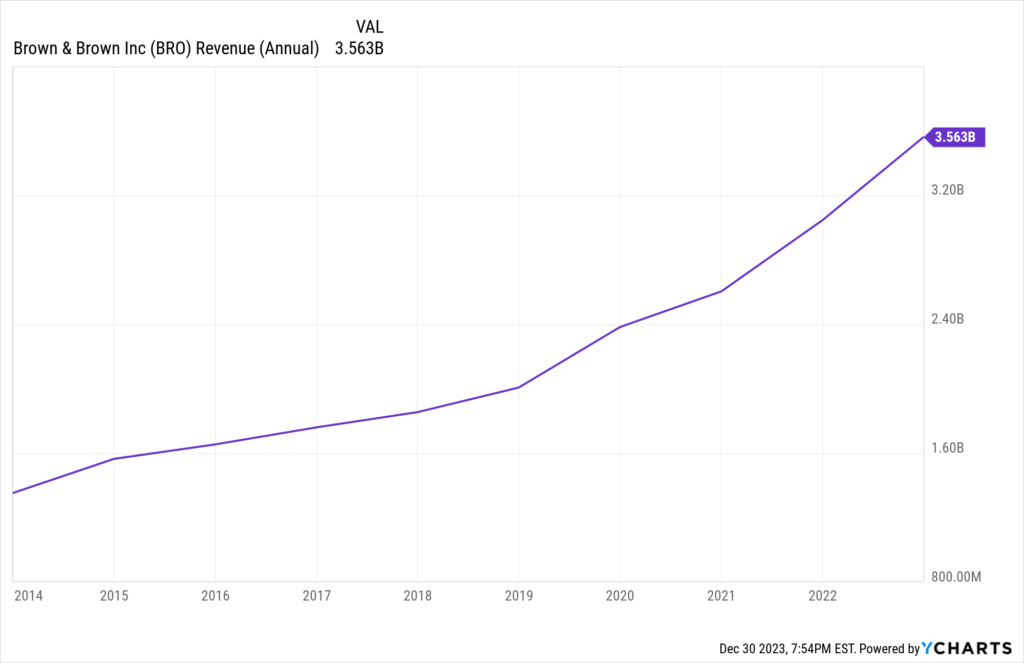

This is an asset-light business model with fat margins and high returns on capital. Brown & Brown acts as agent, or intermediary, offering solutions to clients. A brokerage is, in many ways, far better than an actual insurance business. Take growth, for example. Brown & Brown has compounded its revenue at an annual rate of 11.1% and its EPS at an annual rate of 13.8% over the last decade, and it did this without the underwriting risk.

Brown & Brown flies way under the radar. And I don’t know why. Keep in mind, this is a Dividend Aristocrat. Yes. Brown & Brown is a Dividend Aristocrat. It’s been a tremendous dividend grower for decades, despite getting very little attention.

Brown & Brown flies way under the radar. And I don’t know why. Keep in mind, this is a Dividend Aristocrat. Yes. Brown & Brown is a Dividend Aristocrat. It’s been a tremendous dividend grower for decades, despite getting very little attention.

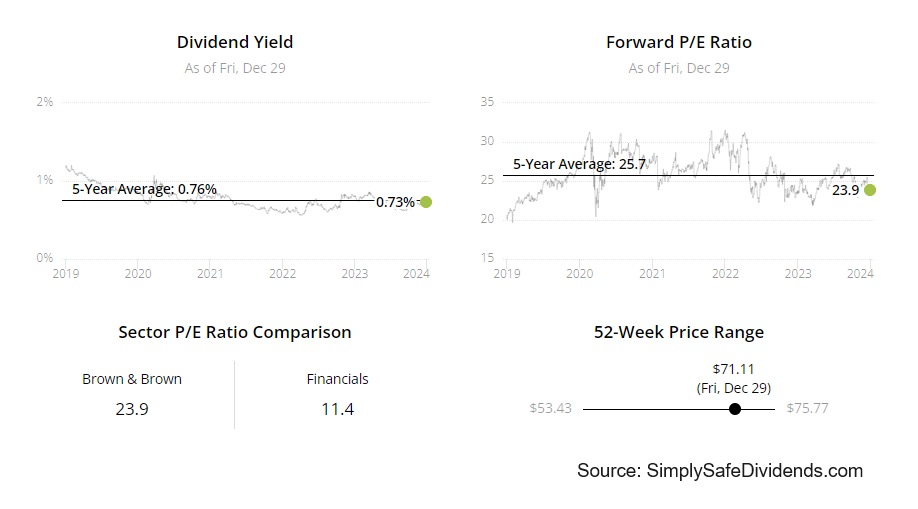

The company has increased its dividend for 30 consecutive years. The 10-year DGR is 9.4%, which is strong. Better yet, there’s been an acceleration in growth here. The most recent dividend raise was 13%. On the other hand, the stock’s lowish yield of 0.7% is what you sacrifice for the faster growth and reliable consistency of Brown & Brown. But this is pretty much in line with its own five-year average.

The stock never offers a very high yield. It’s not an income play. It’s a high-quality compounder. With an extremely low payout ratio of 19.8%, Brown & Brown’s dividend growth acceleration should continue to play out over the coming years.

A recent pullback may have created a window of opportunity to pick up shares. The stock has pulled back nearly 10% from the $76 level down to the $70 level in the middle of December. And that lowered the multiples into very reasonable territory.

For instance, the P/E ratio of 26.9 is now just under its own five-year average of 27.5. The sales multiple of 4.8 is also a hair under its own five-year average of 4.9. It’s no cheap cigar butt, but Brown & Brown is a fantastic serial acquirer with nearly 20% insider ownership by the founding Brown family.

For the first nine months of 2023, revenue is up 20.9% and EPS is up 14.1% YOY. The stock is up approximately 350% over the last 10 years. Massive wealth generator over time. Bottom line? This high-quality compounder is staring you in the face.

For the first nine months of 2023, revenue is up 20.9% and EPS is up 14.1% YOY. The stock is up approximately 350% over the last 10 years. Massive wealth generator over time. Bottom line? This high-quality compounder is staring you in the face.

My third dividend growth stock for January 2024 is Essex Property Trust (ESS). Essex Property Trust is a real estate investment trust that owns and operates a portfolio of US West Coast multifamily properties. Commercial real estate can be super hit and miss. For me, on the miss side, you’ve got stuff like movie theaters, enclosed shopping malls, and office buildings. Just not super exciting.

Some of these types of CRE are dying. However, on the hit side, I think multifamily housing rises to the top of the list. There is no future in which people will suddenly stop needing somewhere to live. It’s a basic need. With its thousands of apartment units, Essex Property Trust caters to this need.

Better yet, it does so with a focus on the US West Coast, which, due to nature, climate, and a proliferation of high-paying jobs, is among the most desirable areas in the entire world. That helps to explain the 11.3% CAGR for revenue and 6.8% CAGR for FFO/share over the last 10 years.

This is a special stock. It’s one of the only Dividend Aristocrat REITs in the world.

There are only three REITs that are Dividend Aristocrats. With its 29 consecutive years of dividend increases, this is one of them. That 29-year track record, by the way, extends all the way back to the initial IPO for the shares. That’s how reliable and relentless Essex Property Trust has been with the dividend raises.

The 10-year DGR of 7.2% is really strong, particularly for a REIT. After all, REITs tend to be slow-growth income vehicles. But fear not. You still get healthy income here. The stock yields 3.8%. Not bad at all. Well in excess of what the broader market offers. That’s for sure. And the payout ratio of 60.9%, based on midpoint guidance for this year’s FFO/share, is one of the lowest payout ratios I know of in the REIT space.

This REIT has been a monster performer over the long run. Per the company’s November 2023 shareholder presentation, Essex Property Trust has provided a 4,335% total return from its June 1994 IPO through October 2023 – far ahead of the 1,509% provided by the S&P 500 over the same time frame.

I’ve found a lot of REITs to actually be poor performers over the long term. Many might be good for income. Total return? Not so much. This Dividend Aristocrat, however, has been remarkable in both total return terms and income terms. We recently put together a full analysis and valuation video on this REIT, and the fair value estimate for the business came out to just over $270/share. The stock is trading hands for about $244. Decent upside on a great REIT.

I’ve found a lot of REITs to actually be poor performers over the long term. Many might be good for income. Total return? Not so much. This Dividend Aristocrat, however, has been remarkable in both total return terms and income terms. We recently put together a full analysis and valuation video on this REIT, and the fair value estimate for the business came out to just over $270/share. The stock is trading hands for about $244. Decent upside on a great REIT.

My fourth dividend growth stock for January 2024 is Hershey (HSY). Hershey is an American multinational confectionery and snack food company.

We all know Hershey, right? Many of us – maybe even most of us – consume and enjoy the various confectionary products. Personally, I go crazy for a Reese’s cup. Anyway, this is a just a phenomenal business that has captured nearly a 50% share of market.

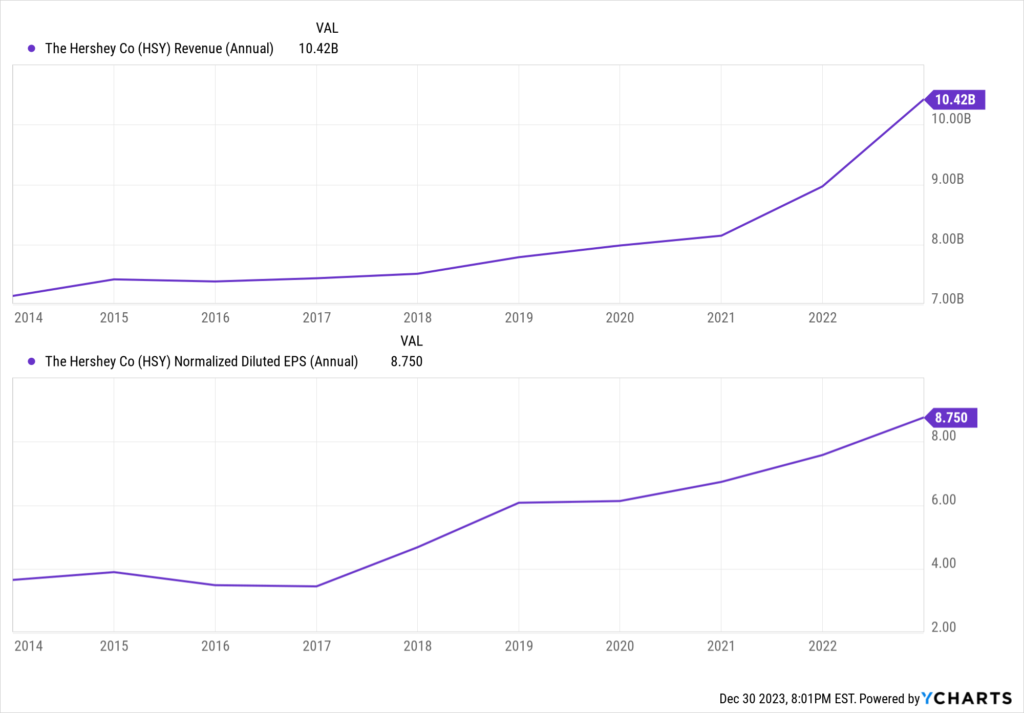

Moreover, Hershey has been broadening the business recently, expanding into salty snacks. This has been a highly successful strategy thus far. Hershey is just plain getting it done. Fat margins. High returns on capital. And plenty of growth. A 4.3% CAGR for revenue and 9.2% CAGR for EPS over the last decade.

What’s sweeter? Chocolate? Or dividend increases? Hershey has increased its dividend for 14 consecutive years, with a 10-year DGR of 9.5% – lining up very nicely with EPS growth over the same time frame. The stock also yields 2.6%. Again, just a very nice combination of yield and growth here.

What’s sweeter? Chocolate? Or dividend increases? Hershey has increased its dividend for 14 consecutive years, with a 10-year DGR of 9.5% – lining up very nicely with EPS growth over the same time frame. The stock also yields 2.6%. Again, just a very nice combination of yield and growth here.

How can you not like a near-3% yield and a high-single-digit dividend growth rate? And a payout ratio of 51.4%, which is nearly perfectly balanced, only adds to the appeal.

I love the products as much as the next guy. But I might love the stock even more. This is just a terrific business from top to bottom. I can find almost nothing to complain about. The only thing that usually draws complaints is the valuation. Like many other really great businesses, Hershey tends to command a healthy premium in the marketplace.

However, after the stock’s 22% slide over the last year, even that is hard to complain about now. The P/E ratio has dropped to a very reasonable 19.7. For perspective, the stock’s five-year average P/E ratio is 26.4. We recently finished up a full analysis and valuation video on Hershey, which should be live soon (if it’s not out already). And this video goes over the ins and outs of the business and why it’s such a compelling long-term investment idea right now. If you don’t yet have Hershey in your portfolio, it’s time to reconsider.

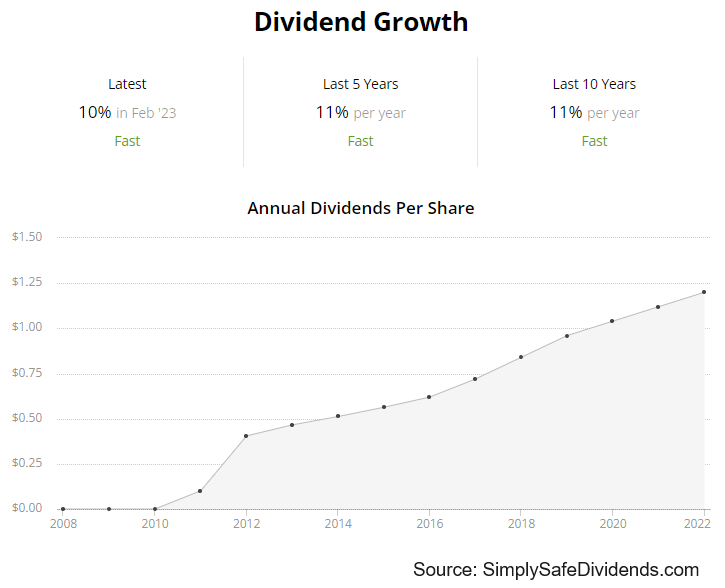

My fifth dividend growth stock for January 2024 is Xylem (XYL). Xylem is a water technology company.

Through three distinct business segments, Xylem produces products that are designed to help with the transportation, treatment, increased efficiency, and testing of water. As I’ve said many times now, I believe that water will be the “liquid gold” of this century, much like how oil was it for the last century.

Water is our most precious resource. We literally can’t survive without it. Xylem is the world’s largest pure-play water technology company, sitting in the driver’s seat as it pertains to benefiting from increasing demand for clean, usable water. Revenue has a CAGR of 4.2% over the last 10 years, while EPS has a CAGR of 9.9% over that period.

Xylem has been a solid dividend grower, and I see that continuing. The company has increased its dividend for 13 consecutive years, with a 10-year DGR of 11.5%. I’m always very happy to see sustained double-digit dividend growth like this. The stock’s yield of 1.2% isn’t much to write home about, and one does give up a bit of current income in order to access the growth and exposure to water.

That said, this yield is in line with its own five-year average, so this is a pretty typical yield level for the stock. With a payout ratio of just 35.5%, based on midpoint guidance for this year’s adjusted EPS, the dividend raises should continue to flow like water.

That said, this yield is in line with its own five-year average, so this is a pretty typical yield level for the stock. With a payout ratio of just 35.5%, based on midpoint guidance for this year’s adjusted EPS, the dividend raises should continue to flow like water.

This stock isn’t a steal. But I think the price is better than fair. And the business model, which is practically bulletproof, has a very long runway ahead of it. Most basic valuation metrics look pretty extended. The forward P/E ratio is nearly 30, based on midpoint guidance for this year’s adjusted EPS.

However, this stock’s five-year average P/E ratio is 46.8. So this is a stock that almost always commands a very healthy premium, but some of that premium has disappeared. We recently ran the business through a full analysis, and the valuation of Xylem came out to almost $120/share.

That video should be live soon, if it’s not already. With the stock’s price sitting at about $112, I think we can sneak in at a level just under fair value here. Again, it’s not a steal. But if you want to invest in the world’s ever-increasing thirst for clean, usable water, Xylem is one of the best ways to do that.

That video should be live soon, if it’s not already. With the stock’s price sitting at about $112, I think we can sneak in at a level just under fair value here. Again, it’s not a steal. But if you want to invest in the world’s ever-increasing thirst for clean, usable water, Xylem is one of the best ways to do that.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income