Although I grew up very poor in Detroit, Michigan, I never let this define me.

I long ago decided to be a survivor, not a victim.

It’s the only way to go through life.

And it’s the only way to approach investing.

If you let yourself become a victim of macroeconomics and/or politics, instead of becoming the survivor that ignores the noise and regularly invests in great businesses, you will get left behind.

I’ve stayed ahead by enthusiastically participating in the compounding machine that is the US stock market.

However, I do this in a very specific way.

However, I do this in a very specific way.

I do it by using the dividend growth investing strategy.

This is a long-term investment strategy whereby one buys and holds shares in terrific businesses that reward shareholders with reliable, rising dividend payments.

You can find many examples of what I’m talking about by taking a look at the Dividend Champions, Contenders, and Challengers list.

This list has compiled data on more than 600 US-listed stocks that have raised dividends each year for at least the past five consecutive years.

Many stocks on this list have been consistently raising dividends for decades, which is just incredible.

Of course, reliable, rising dividends are only possible over an extended period of time when reliable, rising profit is being generated by the business.

And that kind of circular logic is at the heart of why dividend growth investing tends to automatically funnel one into great businesses that perform well over time.

By the way, I put my money where my mouth is.

I’ve been using this strategy for more than a decade now, letting it guide me as I’ve gone about building my FIRE Fund.

That’s my real-life, real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

Indeed, I’ve been in the fortunate position of being able to live off of dividends for years now, even being able to retire in my early 30s.

My Early Retirement Blueprint lays out how I was able to accomplish that feat.

My Early Retirement Blueprint lays out how I was able to accomplish that feat.

A major pillar of my success has, of course, been the type of businesses I’ve invested in.

But valuation at the time of investment has also been critical.

After all, price is only what you pay, but it’s value that you actually get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Avoiding victimhood by adopting a survivor mindset and regularly investing capital into undervalued high-quality dividend growth stocks will set you up to not just survive but thrive over the long run.

Now, with that out of the way, recognizing undervaluation requires one to first understand valuation.

Fear not.

My colleague Dave Van Knapp put together Lesson 11: Valuation in order to help with that.

Part of a comprehensive series of “lessons” designed to teach the A-Z of DGI, it puts forth a valuation template that can be easily used to estimate the fair value of just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Essex Property Trust Inc. (ESS)

Essex Property Trust Inc. (ESS)

Essex Property Trust Inc. (ESS) is a real estate investment trust that owns and operates a portfolio of US West Coast multifamily properties.

Founded in 1971, the company is now a $16 billion (by market cap) real estate giant that employs more than 1,700 people.

Essex Property Trust focuses on three different supply-constrained markets: Southern California, 42% of NOI; Northern California, 40%; and Seattle, 18%.

The company’s property portfolio consists of approximately 62,000 apartment homes across 252 apartment communities.

Commercial real estate is fraught with pitfalls, largely because most forms of it are rather discretionary.

Commercial real estate is fraught with pitfalls, largely because most forms of it are rather discretionary.

Office buildings, enclosed shopping malls, restaurant buildings, etc.

However, Essex Property Trust separates itself from the REIT pack by focusing on shelter – a very non-discretionary basic need in life.

The demand for shelter is built right in, and the runway for that demand extends out for as far as humans will need somewhere to live (i.e., forever).

Shelter has, effectively, no risk of obsolescence.

Technology is changing our world in all kinds of amazing ways, but it’s hard to imagine it changing shelter.

As such, I see multifamily housing as being far more “investable” for the long term in comparison to many other forms of commercial real estate.

One thing that makes Essex Property Trust unique, relative to its US multifamily housing brethren, is the company’s property portfolio footprint.

Essex Property Trust has concentrated itself along the US West Coast.

This could be both the company’s greatest strength and greatest weakness.

On one hand, a combination of unique geography and heavy-handed regulation across West Coast jurisdictions conspire to limit supply.

The West Coast is filled with natural areas that are prohibitive to building much of anything, limiting the supply of usable land for construction and acting as a natural barrier to entry.

Regulatory red tape only adds to supply constriction.

Existing supply is that much more valuable when it’s so difficult to bring new supply to market.

These same supply issues plague single-family houses in these markets, which only serves to make apartments more affordable by comparison.

All of that plays right into the hands of Essex Property Trust.

On the demand side, the West Coast is highly desirable: It has an alluring mixture of high-paying jobs, temperate climates, and beautiful nature.

California is, by far, the most-populated state in the US for good reasons.

If California were its own country, it’d have the fifth-highest GDP in the world.

So it’s both strong demand and limited supply working to the REIT’s favor.

On the other hand, a homelessness crisis, rising crime along the I-5 corridor, and an extremely high cost of living combine to mitigate demand for West Coast living.

In addition, the work-from-home trend, which has demonstrated some staying power, makes it easier for remote workers to move to cheaper locations inland without losing their high-paying jobs.

But fully remote jobs are still somewhat rare, and you can’t take the climate and ocean with you when you leave.

In my view, many (but not all) of the problems facing the West Coast are fixable and most likely temporary in nature (at least, to the degree at which they’re currently present).

However, the appeal of the West Coast is not temporary, nor is the need for shelter.

Both are enduring.

And that’s exactly what positions Essex Property Trust to continue growing its revenue, profit, and dividend for many years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

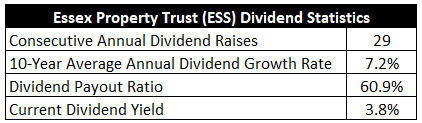

Essex Property Trust has already increased its dividend for 29 consecutive years.

Two quick reasons why this is amazing.

First, it dates all the way back to the company’s original IPO, showing just how reliable and relentless Essex Property Trust has been since the very beginning.

First, it dates all the way back to the company’s original IPO, showing just how reliable and relentless Essex Property Trust has been since the very beginning.

Second, it makes Essex Property Trust a vaunted Dividend Aristocrat – one of only three REITs in the world that can claim that status.

The 10-year dividend growth rate of 7.2% is strong, as most REITs are slow-growth income vehicles.

On the flip side, the stock’s 3.8% yield isn’t as high as what you can find among many competing options in the REIT space.

However, I’d argue that the high, consistent growth and long-term compounding prowess is worth the short-term yield trade-off.

Moreover, this yield is well over what the broader market offers and 60 basis points higher than its own five-year average.

And with a payout ratio of 60.9%, based on midpoint guidance for this year’s FFO/share, Essex Property Trust has a healthy dividend.

Most REITs that I track have payout ratios in the 70% (or higher) range, so this relatively low payout ratio is encouraging.

A near-4% yield paired with a high-single-digit dividend growth rate from a Dividend Aristocrat?

I think that’s pretty compelling.

Revenue and Earnings Growth

As compelling as it might be, though, many of these dividend metrics are looking into the past.

However, investors must always be thinking about the future, as today’s capital is being risked for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be of great aid when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this way should give us the ability to determine what the future growth path of the business may look like.

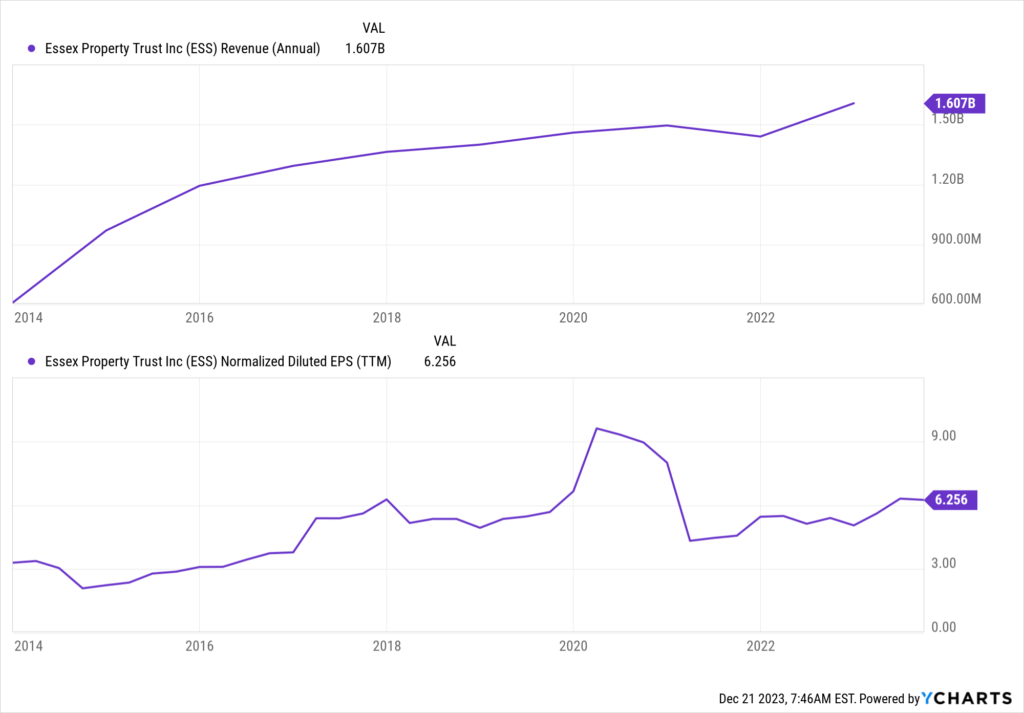

Essex Property Trust advanced its revenue from $611 million in FY 2013 to $1.6 billion in FY 2022.

That’s a compound annual growth rate of 11.3%.

Excellent top-line growth.

Excellent top-line growth.

Unfortunately, it’s slightly misleading.

When it comes to REITs, it’s imperative to look at profit growth on a per-share basis.

That’s because REITs use debt and equity to fund growth, as they’re legally required to distribute at least 90% of their taxable earnings to shareholders.

This circles back around to the point I made on REITs being income plays.

Limitations around internal funding for growth means tapping equity (by issuing shares), resulting in dilution.

That tends to create distortion between absolute revenue growth and profit growth relative to shares outstanding.

Also, when assessing profit for a REIT, we want to use funds from operations instead of normal earnings.

FFO (or adjusted FFO) is a measure of cash generated by a REIT, which adds depreciation and amortization expenses back to earnings.

Essex Property Trust grew its FFO/share from $7.59 to $13.70 over this period, which is a CAGR of 6.8%.

This is a more realistic portrayal of the company’s true growth profile.

Not as amazing as top-line growth, but it’s still very good.

It’s a high-single-digit growth out of a basic need that has practically no risk of obsolescence.

When you adjust for the risk, the growth profile is appealing.

We can also see how well dividend growth has tracked FFO/share growth over the last decade, showing deft stewardship from management.

Looking forward, CFRA currently has no three-year growth projection for the REIT’s FFO/share.

That’s a shame.

I generally like to compare the proven past up against a future forecast, which helps with extrapolating out results and narrowing a range of possible outcomes.

Absent this information, I’ll instead lean on recent guidance provided by Essex Property Trust itself.

The company’s most recently released guidance is calling for $15.10 to $15.22 in FFO/share for FY 2023.

At the midpoint of $15.16/share, that would represent 10.7% YOY growth.

And that’s in a tough environment for comps.

Keep in mind, this is coming on top of a multi-year bonanza for multifamily housing.

For a variety of reasons, the pandemic resulted in a demand boom for suburban housing options.

That played right into the hands of the likes of Essex Property Trust, since most of its inventory is in more suburban locations.

It’s mighty impressive to see Essex Property Trust maintaining above-average growth off of an elevated profit base.

All that said, Essex Property Trust doesn’t need to produce extraordinary results in order to make shareholders plenty of money.

If the company can simply maintain its ordinary, historical level of growth, it’ll do well.

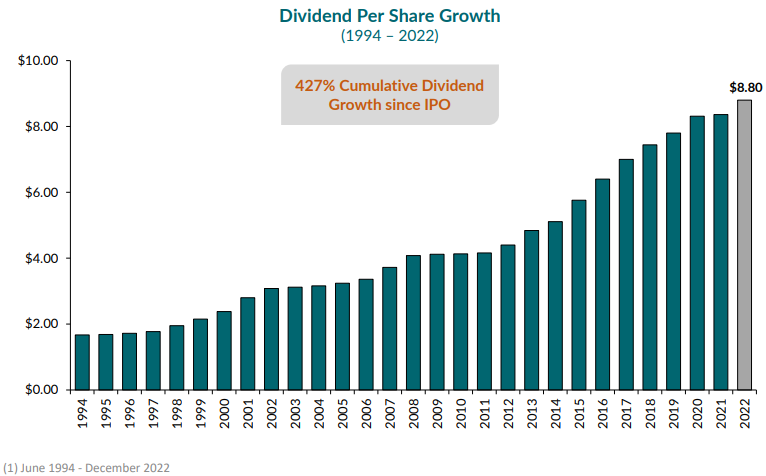

Indeed, this has been a winner of epic proportions since the IPO.

Per the company’s November 2023 shareholder presentation, Essex Property Trust has provided a 4,335% total return from its June 1994 IPO through October 2023 – far ahead of the 1,509% provided by the S&P 500 over the same time frame.

Also, I think it’s time to clear up the misconception that people are fleeing the West Coast.

That’s simply not showing up in the numbers.

The company’s Q3 FY 2023 earnings report showed same-property portfolio occupancy at 96.4% – up from the 96% mark one year ago.

Occupancy is up, not down.

If there is any fleeing occurring, it’s most certainly not happening at Essex Property Trust properties.

Overall, I see nothing to indicate that Essex Property Trust cannot continue to deliver the high-single-digit dividend growth that shareholders have come to expect.

The business is doing well, and the payout ratio offers a large cushion.

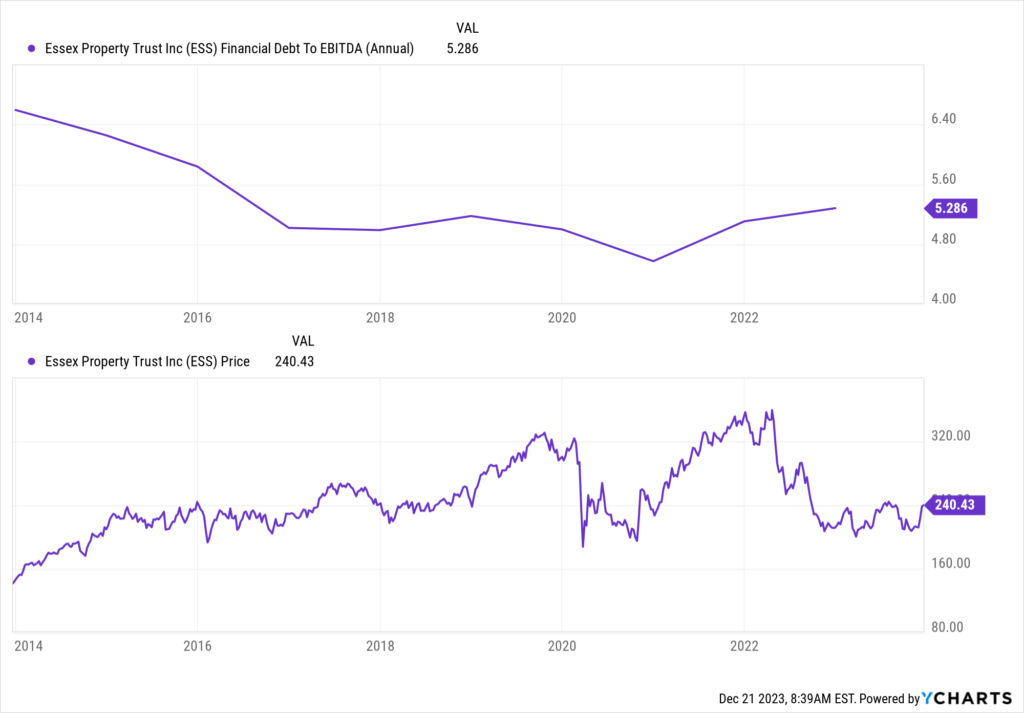

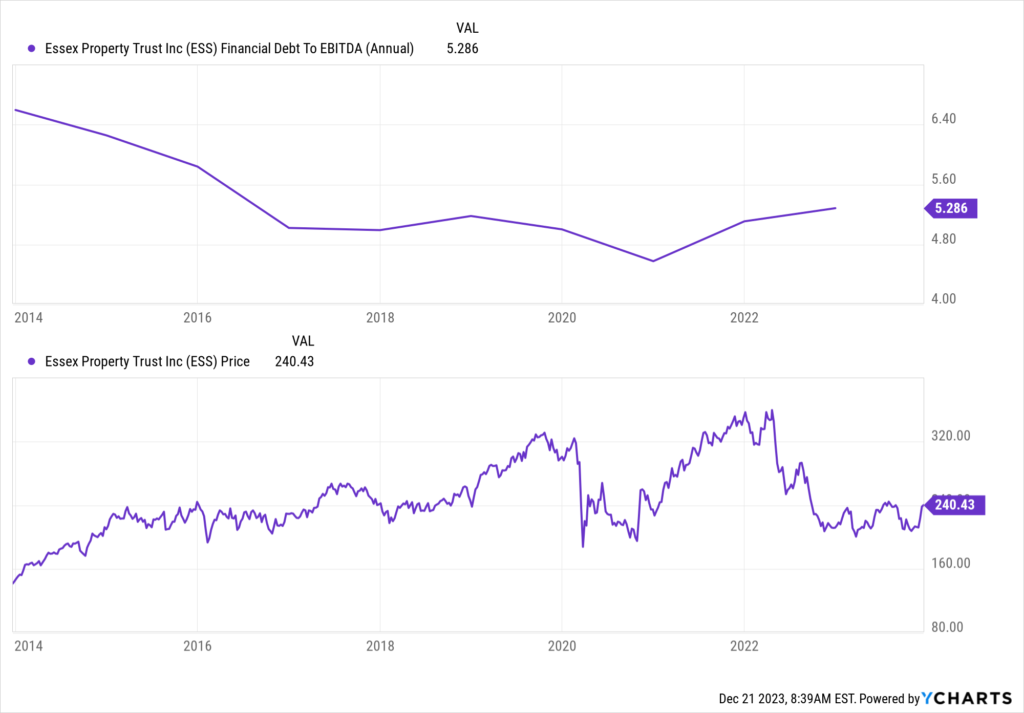

Financial Position

Moving over to the balance sheet, Essex Property Trust has a good financial position.

The company finished last year with a bit under $6 billion in long-term debt, which isn’t terribly high relative to the market cap.

A common measure for a REIT’s financial position is the debt/EBITDA ratio, which is 5.5 (on an adjusted basis) for Essex Property Trust.

I usually see REITs range from 3 to 7 on this ratio, putting Essex Property Trust at somewhere in the middle.

The weighted average interest rate on its debt stands at 3.4%, putting its cost of capital at a reasonable level.

The weighted average interest rate on its debt stands at 3.4%, putting its cost of capital at a reasonable level.

Moreover, the company has investment-grade credit ratings: BBB+, Fitch; Baa1, Moody’s; and BBB+, Standard & Poor’s.

Overall, there’s a lot to like about this REIT, not the least of which is the fact that its core offering is a basic need that just so happens to be located in one of the most in-demand areas of the entire world.

And with economies of scale, regulatory know-how in difficult markets, natural barriers to entry, and an entrenched footprint in supply-constrained and desirable locations, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

California’s infamous red tape is a double-edged sword – constraints on bringing new inventory to market help to boost the value for existing properties, but it’s also difficult to grow the portfolio.

Real estate is generally cyclical, although the basic need of shelter does mitigate some of that cyclicality.

Essex Property Trust has indirect exposure to the technology industry, as a lot of tech companies are based on the West Coast.

The capital structure of a REIT relies on external funding (both debt and equity) for growth, and rising interest rates can create harm in two ways: Debt becomes more expensive when rates are higher, and competitive yields elsewhere reduces demand for the equity.

Essex Property Trust lacks geographic diversification.

The West Coast exposure introduces risks of natural disasters, such as earthquakes.

As work becomes more flexible, more remote workers could choose to leave the West Coast for cheaper locations inland.

While these risks should be weighed, the quality of the business should also be weighed.

The valuation, which looks attractive, is also something that has to be weighed…

Stock Price Valuation

The stock is trading hands for a forward P/FFO ratio of 15.9, based on midpoint guidance for this year’s FFO/share.

That’s somewhat analogous to a P/E ratio on a normal stock.

Not demanding at all.

The P/CF ratio of 16.4 is also well off of its own five-year average of 20.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 6.5%.

This mark is below the company’s demonstrated FFO/share and dividend growth over the last decade.

With the payout ratio where it’s at, and with business growth as good as ever, I don’t see why the foreseeable future will look much different than the recent past.

After all, this is a type of commercial real estate that has built-in, enduring demand, and the geographic footprint fortifies the firm’s advantages.

The DDM analysis gives me a fair value of $281.16.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think my model was fair and balanced, yet the stock looks cheap anyway.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates ESS as a 4-star stock, with a fair value estimate of $305.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates ESS as a 3-star “HOLD”, with a 12-month target price of $225.00.

We have a fairly broad range here. Averaging the three numbers out gives us a final valuation of $270.39, which would indicate the stock is possibly 11% undervalued.

Bottom line: Essex Property Trust Inc. (ESS) is a great REIT that offers the basic, enduring need of shelter to willing renters in some of the most desirable locations in the world. Because of regulatory hurdles and natural barriers to entry, its entrenched supply is a powerful advantage. With a market-beating yield, a moderate payout ratio, a high-single-digit dividend growth rate, nearly 30 consecutive years of dividend increases, and the potential that shares are 11% undervalued, long-term dividend growth investors should take a close look at this Dividend Aristocrat.

Bottom line: Essex Property Trust Inc. (ESS) is a great REIT that offers the basic, enduring need of shelter to willing renters in some of the most desirable locations in the world. Because of regulatory hurdles and natural barriers to entry, its entrenched supply is a powerful advantage. With a market-beating yield, a moderate payout ratio, a high-single-digit dividend growth rate, nearly 30 consecutive years of dividend increases, and the potential that shares are 11% undervalued, long-term dividend growth investors should take a close look at this Dividend Aristocrat.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is ESS’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 93. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, ESS’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income