High-quality dividend growth stocks are great. Why? Because these stocks represent equity in world-class businesses. Think about it. A business has to be great in order to generate the ever-higher profit necessary to afford the ability to pay ever-larger cash dividends.

It’s easy to see why these stocks are appealing. But when they’re on sale – when they’re undervalued – that’s when the appeal is cranked up even more.

See, price and yield are inversely correlated. All else equal, lower prices result in higher yields. This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach. Now, lower valuations often come when there’s volatility. But I always see short-term volatility as a long-term opportunity.

That perspective helped me to go from below broke at age 27 to financially free at 33. By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

With all of that out of the way, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what it’s all about.

Today, I want to tell you my top 5 dividend growth stocks for December 2023.

Ready? Let’s dig in.

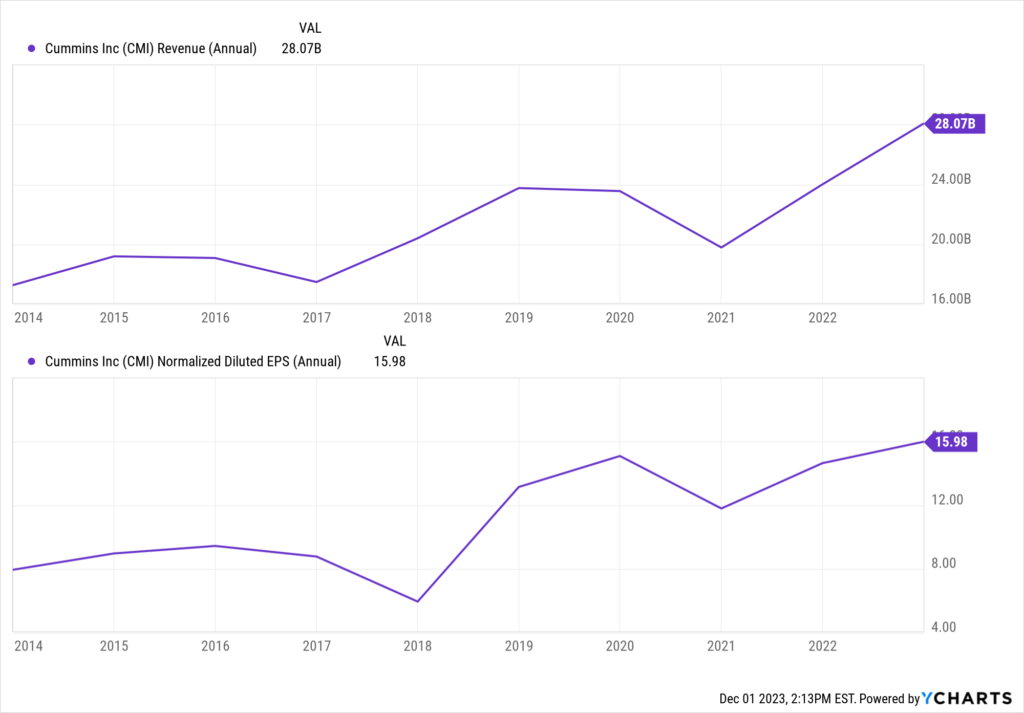

My first dividend growth stock for December 2023 is Cummins (CMI). Cummins is an engines, filtration, and power generation products company.

Mobility is behind everything. It’s behind transportation. Logistics. The global supply chain. And what’s behind mobility? Cummins. Been true since its 1919 founding. And as a word leader in engines and power generation products, it’s still true today.

Not only that but this company is adapting to what mobility is shaping into tomorrow. Just this year, Cummins launched Accelera by Cummins, which aims to bring more zero-emission vehicles to market. This is a steady-eddy company that continues to grind its revenue and profit higher. Revenue has a CAGR of 5.5% over the last decade, while EPS has a CAGR of 7.5% over that time frame. This company also continues to grind out an ever-larger dividend.

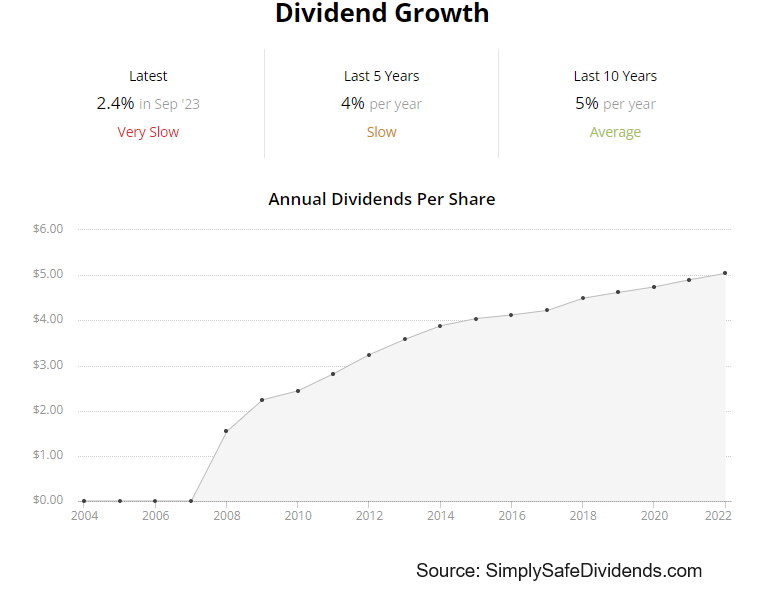

Indeed, Cummins has increased its dividend for 18 consecutive years. The 10-year DGR of 12.9% is strong, especially when you see that it’s paired with the stock’s market-beating yield of 3%. A payout ratio of 34.2% offers a lot of dividend safety here, and it gives Cummins plenty of room to continue handing out generous dividend raises for years to come.

Indeed, Cummins has increased its dividend for 18 consecutive years. The 10-year DGR of 12.9% is strong, especially when you see that it’s paired with the stock’s market-beating yield of 3%. A payout ratio of 34.2% offers a lot of dividend safety here, and it gives Cummins plenty of room to continue handing out generous dividend raises for years to come.

This stock looks cheeeeeap.

Every basic valuation metric is low both in absolute and relative terms. Take the P/E ratio of 11.5, for example. Undemanding in and of itself. No doubt about it. Nearly a single-digit earnings multiple. In addition, relative to its own five-year average of 15.1, it’s very low.

We recently put together a full analysis and valuation video on Cummins, which should be live soon. In that video, the estimate for fair value on the business came out to just under $270/share. The stock’s current pricing is right about $225. Very nice upside potential on a very nice business. Take a look.

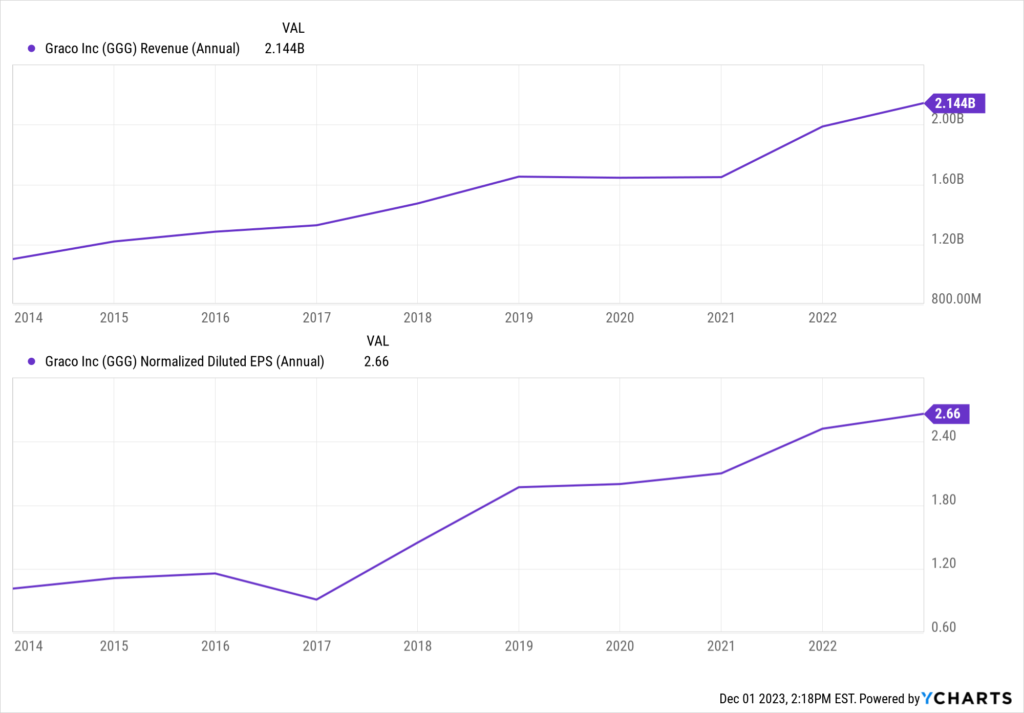

My second dividend growth stock for December 2023 is Graco (GGG). Graco develops and manufactures fluid-handling systems and products.

This is a terrific business. What I love about the business model is the fact that Graco has entrenched itself into a niche with limited competition. Graco manufactures all kinds of systems that are designed for difficult-to-handle fluids – be it corrosive, viscous, etc.

Not exactly the kind of business model that every entrepreneur dreams of. Yet Graco is putting up impressive growth anyway. The company has compounded its revenue at an annual rate of 7.5% over the last decade, while EPS has compounded at an annual rate of 10.1% over that period.

The dividend growth track record here is incredible. That’s true for two key reasons. First, longevity. Graco has increased its dividend for 26 consecutive years. If Graco were in the S&P 500, it’d be a Dividend Aristocrat. Second, the consistent, linear nature of dividend growth. The 10-year DGR is 10.8%, and almost every dividend raise from Graco comes in at a low-double digit rate. It’s like clockwork.

Now, the stock’s 1.2% yield isn’t lighting the world on fire. But with that double-digit growth being supported by a low payout ratio of only 31%, this idea is right in the wheelhouse for those seeking a high-quality compounder.

Now, the stock’s 1.2% yield isn’t lighting the world on fire. But with that double-digit growth being supported by a low payout ratio of only 31%, this idea is right in the wheelhouse for those seeking a high-quality compounder.

Now, Graco isn’t cheap. Never really has been. Probably never will be. This falls into the camp of a wonderful business at a fair price.

No, the multiples aren’t optically cheap. But I also don’t see anything particularly egregious here. Remember: Price is what you pay, but value is what you get. Ferraris cost more than Toyotas, just like terrific businesses cost more than terrible businesses. Graco’s P/E ratio of 26.8 might look high at first glance. But it’s actually not. Its own five-year average is 28.2.

We can also see a cash flow multiple of 23.5 that looks elevated but compares favorably to its own five-year average of 26.3. So on and so forth. Our recent deep dive video into Graco estimated intrinsic value for the business to be $77.57/share. And that’s an average that included what might be a lowball number from yours truly. The stock’s current pricing of about $81.50 is higher than that. But if Graco pulls back ever so slightly, that might be your chance to jump on it.

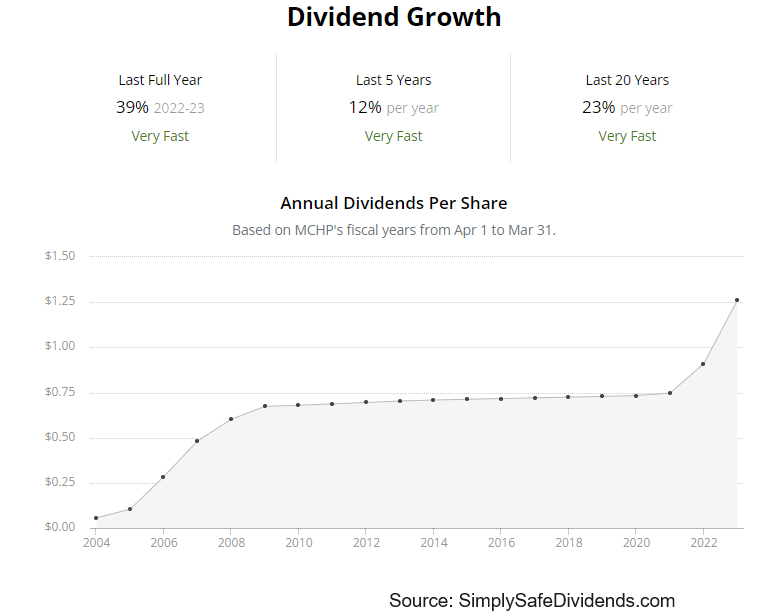

My third dividend growth stock for December 2023 is Microchip Technology (MCHP). Microchip Technology develops and manufactures microcontrollers, analog semiconductors, and other semiconductor products.

Microchip Technology offers a lot of the upside of investing in tech – i.e., growth – without too much of the downside – i.e., technological obsolescence. That’s because MCUs and analog chips are not reliant on leading-edge chip design, which reduces CapEx needs and obsolescence risks.

And many of the products that require MCUs and analog chips are everyday electronic devices that have high value and low cost (to the OEM) – there’s a bit less cyclicality there relative to a business that might cater to high-end, expensive technology. That has translated to solid growth. Over the last decade, the company has compounded its revenue at an annual rate of 18% and its EPS at an annual rate of 18%.

Double-digit business growth. Double-digit dividend growth.

Now, let me qualify what I just said. Microchip Technology has increased its dividend for 22 consecutive years, which is great. But the 10-year DGR for Microchip Technology is only 5.1%. That’s not double-digit dividend growth. However, there’s been a serious acceleration in dividend growth over the last several years.

The five-year dividend growth rate is 9.9%, and the three-year dividend growth rate is 16.5%. There’s the double-digit dividend growth. More like it, right? And with a 2.2% yield, the combination of yield and growth here is not bad at all. With a payout ratio of 38.5%, I suspect a continuation of that more recent rate of dividend growth.

This stock is up about 18% on the year, and that strong performance has reduced some of the value. But I think there’s still a decent amount of it here.

This stock is up about 18% on the year, and that strong performance has reduced some of the value. But I think there’s still a decent amount of it here.

Most of the multiples being commanded by Microchip Technology are not overly demanding. The P/E ratio of 17.9, for instance, is not overly high. Neither is the sales multiple, which is sitting at just over 5. We recently put together a full analysis and valuation video on Microchip Technology, and the estimate for the business’s fair value came out to $88.35/share. The stock is currently priced at about $82. Decent upside on a great business. It’s worth consideration.

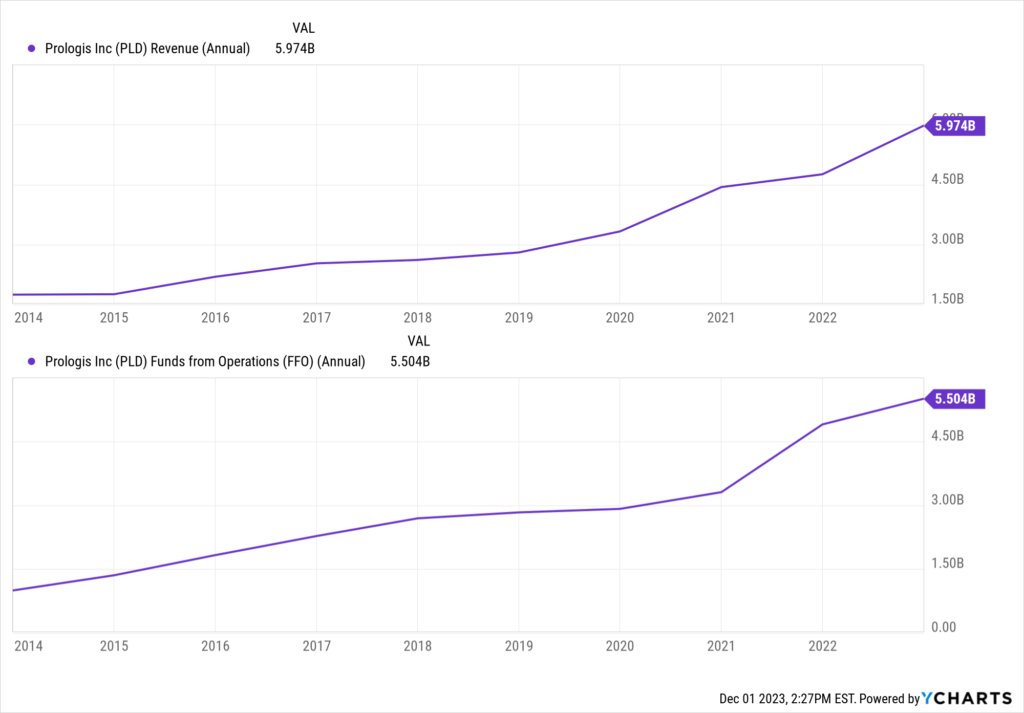

My fourth dividend growth stock for December 2023 is Prologis (PLD). Prologis is a global real estate investment trust.

Honestly, I’m not a huge fan of REITs. Too much leverage, too little returns. Yield chasers love REITs, much to the detriment of their money. But Prologis is one of the few REITs that I really, really like. This is an infrastructure/logistics play.

Prologis leases industrial and logistics buildings to approximately 6,700 different customers worldwide. The company’s property portfolio consists of more than 5,500 properties comprising a total of 1.2 billion square feet. We are not talking about dying malls and movie theaters here. And that’s why you see a 14.3% CAGR in revenue and 13.5% CAGR in Core FFO/share over the last decade.

Prologis is a dividend growth monster, which is rare for a REIT. Most REITs are growing dividends very slowly. But not Prologis. Its 10-year DGR is 10.9%. That is not very REIT-like, which I love. Now, the stock yields 3.1%. And that’s also where Prologis is not very REIT-like. But that’s actually why I’m such a fan of Prologis. It’s not some high-yield junk stock with poor growth and low returns.

Prologis is a dividend growth monster, which is rare for a REIT. Most REITs are growing dividends very slowly. But not Prologis. Its 10-year DGR is 10.9%. That is not very REIT-like, which I love. Now, the stock yields 3.1%. And that’s also where Prologis is not very REIT-like. But that’s actually why I’m such a fan of Prologis. It’s not some high-yield junk stock with poor growth and low returns.

Prologis has increased its dividend for 10 consecutive years. And with a payout ratio of 62.3%, based on midpoint guidance for this year’s Core FFO/share, I think Prologis is set to continue that track record for years to come. This stock’s attractiveness is about as high as it’s ever been.

Prologis has usually commanded a very heavy premium. And that’s made sense. It’s a higher-quality REIT with more growth. But it’s really come off the boil. When valuing a REIT, you want to use cash flow, or FFO. This stock’s five-year average cash flow multiple is 27.7. So you can see what kind of premium has usually been in place. Now? The cash flow multiple is 19.1.

Not super low, even after the compression, but we’re certainly in much more reasonable territory. We’ll have a full analysis and valuation video coming out soon on Prologis, and it’ll show why this high-quality REIT is about as appealing as it’s ever been. Stay tuned for that.

My fifth dividend growth stock for December 2023 is Philip Morris International (PM). Philip Morris is the world’s largest publicly traded tobacco company.

Most tobacco companies are melting ice cubes. Traditional cigarette volumes for pretty much every major tobacco company are in secular decline and headed toward zero. These businesses are getting caught in a black hole – a gravitational well toward non-existence. That’s just the truth of the matter. And investors who don’t see it are willfully ignoring reality. But this is where Philip Morris is actually different.

Thanks to prescient investments in smoke-free alternatives like IQOS – which uses heat-not-burn technology – and ZYN – smoke-free nicotine pouches – Philip Morris is seeing its overall volumes increase. That’s what positions the business for growth acceleration, despite industry dynamics and the lackluster 0.2% CAGR in revenue and 1.1% CAGR in EPS over the last decade. That also sets the dividend up for an acceleration in growth.

Already, Philip Morris has increased its dividend for 16 consecutive years – dating back to its initial spin-off. The 10-year DGR is 4.7%, which is not at all bad when you pair that with the stock’s market-smashing yield of 5.6%. And with a payout ratio of 85.7%, which is elevated but not uncommon for the business, you might think it’ll be more of the same.

However, with ZYN now on board and IQOS showing serious strength, Philip Morris seems to be on the other side of a long cycle of planning and investment. And that could mean more dividend growth and better returns for shareholders on a go-forward basis. That encouraging setup does not appear to be fully appreciated by the market.

However, with ZYN now on board and IQOS showing serious strength, Philip Morris seems to be on the other side of a long cycle of planning and investment. And that could mean more dividend growth and better returns for shareholders on a go-forward basis. That encouraging setup does not appear to be fully appreciated by the market.

Most multiples are pretty pedestrian. The forward P/E ratio, using the company’s midpoint guidance for adjusted EPS for this year, is 15.5. That’s not overly demanding at all. The sales multiple of 4.3 is also not very high, and it’s lower than its own five-year average of 4.5.

We recently put together a video on this business that will analyze it and estimate its fair value, and that video should be out soon (if it’s not already). The fair value estimate came out to just under $104/share. The stock’s current price is about $94. This rare industry growth story looks attractively valued, and you get a 5.6% yield while you wait for that story to unfold. You could do a lot worse than that.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income