This month, I’ve published two pieces about technical analysis — one on Bollinger Bands and another on the Relative Strength Indicator (RSI). It turns out these indicators are helpful in predicting stock prices… As long as they’re paired with fundamental analysis.

That’s because financial data can help investors pick the right companies for technical analysis. Consider the consumer staples and utility stocks of the Russell 3000, a group of firms that tend to mean-revert thanks to their predictable earnings.

$10,000 invested using a mean-reverting Bollinger Band strategy would have grown into $15,140 between 2018 and 2023, vastly outperforming the $9,200 obtained through a buy-and-hold strategy. The RSI Index — another mean-reversion strategy — would have yielded $14,000.

To take a specific example, here are Bollinger Bands in action for trading Colgate-Palmolive (NYSE:CL), a company that has consistently traded in a narrow $60 to $85 range since 2018. Naturally, investors who bought in the low end and sold at the high end would have earned consistent profits, even if shares went nowhere over time.

To take a specific example, here are Bollinger Bands in action for trading Colgate-Palmolive (NYSE:CL), a company that has consistently traded in a narrow $60 to $85 range since 2018. Naturally, investors who bought in the low end and sold at the high end would have earned consistent profits, even if shares went nowhere over time.

Meanwhile, technical strategies can be run in reverse to help investors avoid marginal bets. Consider Grubhub, a Chicago-based startup (now owned by Just Eat Takeaway.com (OTCMKTS:JTKWY)) that once competed in the hyper-competitive world of meal-delivery services. An investor using a reverse RSI strategy would have seen plenty of technical warnings to sell in the $70 range. By 2020, shares fell to $30.

Meanwhile, technical strategies can be run in reverse to help investors avoid marginal bets. Consider Grubhub, a Chicago-based startup (now owned by Just Eat Takeaway.com (OTCMKTS:JTKWY)) that once competed in the hyper-competitive world of meal-delivery services. An investor using a reverse RSI strategy would have seen plenty of technical warnings to sell in the $70 range. By 2020, shares fell to $30.

That’s why investors should pay particular interest to the latest 23 companies that MarketMasterAI has chosen. My AI stock-picking strategy automatically combines fundamental data, industry estimates and technical data to create stock price predictions.

The system works, as I outline here. “A+” rated firms have more than doubled the returns of “F” rated ones and the outperformance is rising over time as the system gathers more data.

Using Bollinger Bands

Bollinger Bands are a charting tool that combines moving averages (MA) with price volatility. When prices become volatile, these bands widen to dissuade investors from accumulating shares too quickly. And as prices settle back down, the bands narrow to create more buying opportunities.

Bollinger Bands are particularly helpful for identifying entry points in high-quality stocks that trade in narrow ranges. Here’s what happens when we apply the mean-reverting Bollinger Band strategy to Clorox (NYSE:CLX), a firm where shares “gravitate” back to a central price. With this strategy, we buy when prices hit the bottom band and sell when it hits the top.

Investors using this strategy could have generated significant profits. $10,000 invested in Clorox in 2021 using this strategy would have generated $3,659 of profits by 2023, compared to a $4,026 loss from a buy-and-hold strategy.

Investors using this strategy could have generated significant profits. $10,000 invested in Clorox in 2021 using this strategy would have generated $3,659 of profits by 2023, compared to a $4,026 loss from a buy-and-hold strategy.

However, identifying the right companies to track requires fundamental analysis. Not every household goods company is a stable firm; packaged food producer Kraft Heinz (NASDAQ:KHC) saw shares drop 75% between 2017 and 2020 after botched attempts at corporate cost-cutting. And not every “risky” tech company is truly high-risk. Shares of tech firm Dropbox (NASDAQ:DBX) have the same beta (a measure of risk) as blue-chip industrial goods firm Ball Corp (NYSE:BALL).

However, identifying the right companies to track requires fundamental analysis. Not every household goods company is a stable firm; packaged food producer Kraft Heinz (NASDAQ:KHC) saw shares drop 75% between 2017 and 2020 after botched attempts at corporate cost-cutting. And not every “risky” tech company is truly high-risk. Shares of tech firm Dropbox (NASDAQ:DBX) have the same beta (a measure of risk) as blue-chip industrial goods firm Ball Corp (NYSE:BALL).

That’s why these firms particularly stand out for their near-bottom Bollinger Band readings.

1. Becton, Dickinson & Co (BDX)

Medical technology company Becton, Dickinson & Co (NYSE:BDX) saw shares plummet recently on weaker-than-expected guidance. The company expects revenues of between $20.1 billion and $20.3 billion in 2024, which fell short of Wall Street’s $20.4 billion estimates.

The selloff was far too harsh. Becton Dickinson’s 2024 revenue projections still represent a 4.5% to 5.5% increase and profits are expected to continue rising. Analysts believe the firm’s EPS will hit a record $13.01 in fiscal 2024.

BDX also has a long history of outperforming estimates. Before last quarter’s 1-cent earnings miss, the company had recorded at least 19 consecutive quarters of earnings beats.

The firm is also highly profitable for its industry; its pretax return on assets (ROA) are better than 62% of companies in the medical equipment industry, thanks to high switching costs in the surgical industry. Becton is also one of the world’s largest manufacturers of needles and syringes, which gives it significant cost advantages in that commoditized space.

It’s why MarketMasterAI awards BDX a healthy “A-” grade and a 4% to 6% upside over the next several months. History has trained the algorithm to seek high-quality companies to buy on dips. A bottom-up analysis shows an even more significant upside of roughly 30%.

With BDX shares now trading well below their lower Bollinger Band range, investors have a golden opportunity to buy a high-quality medical device firm at a discount.

With BDX shares now trading well below their lower Bollinger Band range, investors have a golden opportunity to buy a high-quality medical device firm at a discount.

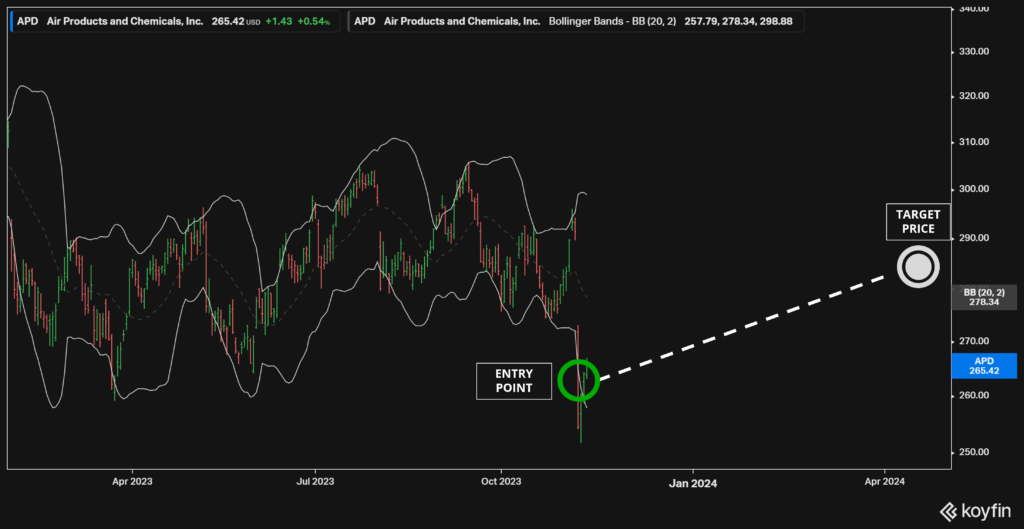

2. Air Products

Industrial gas firm Air Products (NYSE:APD) saw a similar selloff after announcing mixed Q3 earnings. Revenues of $3.03 billion missed Street estimates while EPS beat estimates. The stock cratered on the news.

This isn’t the first time Air Products has seen share prices sink on virtually no news. In Q1 2022, the stock plummeted 13% after the firm announced earnings that met Street expectations (not a miss!). And a roughly 1% EPS beat the following quarter would see a 6% selloff.

Nevertheless, Air Products’ shares quickly recovered each time. The company’s margins have continued to expand and fears of a deep world recession have proven overblown. (Management’s focus on long-term contracts also insulates Air Products from price changes). Wall Street analysts now expect net income to hit a record $2.9 billion in fiscal 2024, driven by a 140 basis point margin increase and 6% growth in revenues.

The MarketMasterAI system agrees with the Street, awarding the firm an “A-” score. Shares should recover to the $280 to $290 level by early next year.

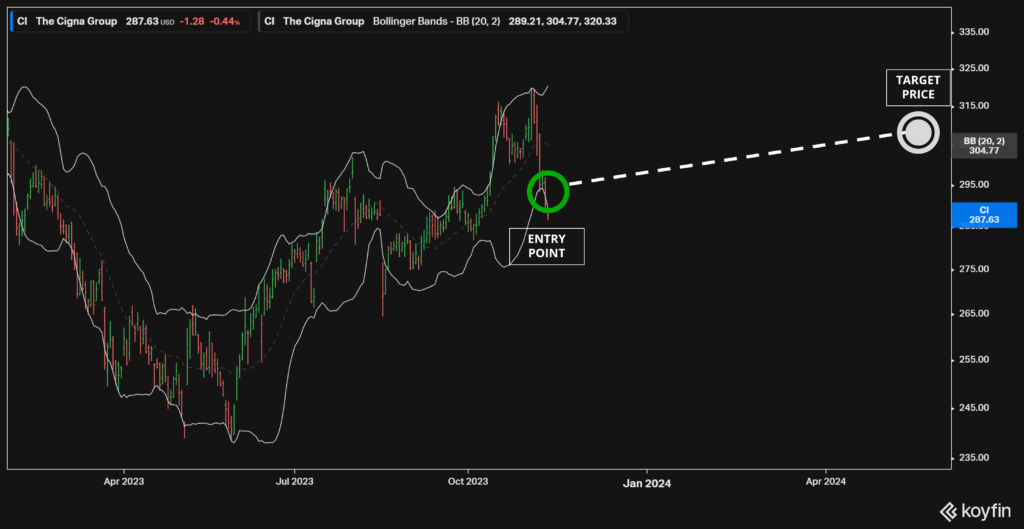

3. Cigna (CI)

3. Cigna (CI)

Shares of medical insurance firm Cigna (NYSE:CI) are now moderately valued after a 10% selloff this month. MarketMasterAI estimates that shares should recover to the $310 range by early next year.

Cigna is admittedly a riskier bet from its exposure to Congressional whims. Healthcare is a strangely regulated industry that tends to allow monopolistic pricing. In a more unrestricted market, Cigna’s financial returns would resemble levels earned by auto, life and property and casualty (P&C) insurers.

Still, a bet on Cigna is reasonable, given the current gridlock in Congress. Few lawmakers seem to have the appetite for healthcare reform. That means Cigna’s financials will likely keep growing. Analysts now expect the health insurance firm to grow revenues by 19% in fiscal 2024 and net income is set to surge to $8.2 billion.

Technical figures support this bullishness. According to the Bollinger Band strategy, investors should buy at current prices and sell in the $325 range.

Using the Relative Strength Indicator (RSI)

4. Johnson & Johnson (JNJ)

It has been a challenging year for Johnson & Johnson’s (NYSE:JNJ) stockholders. The world’s largest healthcare products firm has seen its shares sink 15% year-to-date (YTD) despite posting impressive financial results. JNJ has beat earnings by at least 5% in the last four quarters.

Behind this drawdown is a growing concern about upcoming patent expirations. Revenues for fiscal 2023 are expected to fall 10.7% and Wall Street analysts believe growth will remain in the low-single-digits through 2026.

But JNJ has several promising drugs in its pipeline. Analysts expect Tremfya, a replacement for an older immunology drug, to generate as much as $5 billion annually by 2028. Several cancer-beating drugs are also expected to become blockbusters.

JNJ also has a large, diversified business beyond pharmaceuticals. The company generates 30% of its sales from medical devices and 20% from consumer products. U.S. prescription drugs make up less than 30% of total revenues.

It’s why MarketMasterAI awards JNJ a solid “A” grade and expects shares to recover to the $160 to 170 range by 2024. Just be sure to take profits when the pendulum swings higher, since Johnson & Johnson’s shares typically trade in a narrow range.

5. Schlumberger (SLB)

5. Schlumberger (SLB)

Shares of blue-chip energy firm Schlumberger (NYSE:SLB) have been in freefall this quarter on sagging oil prices. The value of West Texas Intermediate (WTI) has now fallen 20% from its $95 peak reached in the summer. Climate forecasters are now calling for a milder-than-expected start to the winter because of the El Nino effect.

Still, technical and quantitative projections suggest that investors are better off buying the dip in “A” rated Schlumberger, a pioneer of hydraulic fracturing (fracking) technologies. The company is a leader in its field, outspending many larger rivals in research and development (R&D). Aging U.S. wells will additionally require more services to pump remaining reserves.

Most importantly for tactical traders, Schlumberger’s shares have traditionally recovered strongly after selloffs in the energy market. A 50% collapse in SLB’s share price when oil prices went “negative” in 2020 was followed by an equivalent 100% surge over the following two years. MarketMasterAI projects a $56 to $60 target price in 2024.

Note: Investors should take profits in the $60-plus range since oil markets are expected to shrink over the longer term.

Note: Investors should take profits in the $60-plus range since oil markets are expected to shrink over the longer term.

6. Mattel (MAT)

Shares of Mattel (NASDAQ:MAT) have sunk in recent weeks on fears of a consumer slowdown. Retailers from Target (NYSE:TGT) to Macy’s (NYSE:M) have previously lowered year-end guidance. A comedown from summer’s Barbie sugar rush might also be to blame.

Yet, Mattel is a well-run firm that has continuously bounced back after selloffs. The last time shares hit the oversold “30” RSI level in March, they would eventually surge 30% to $21.

This time around, it looks no different. MarketMasterAI estimates that Mattel’s shares are worth north of $20, given its strong earnings and strong estimated growth. Analysts expect the California-based firm to increase net income by 7% next year and 11% the year after, driven by more licensing deals and improving consumer demand.

This time around, it looks no different. MarketMasterAI estimates that Mattel’s shares are worth north of $20, given its strong earnings and strong estimated growth. Analysts expect the California-based firm to increase net income by 7% next year and 11% the year after, driven by more licensing deals and improving consumer demand.

Things haven’t always been smooth for Mattel. The company struggled in the late-2010s after video games began to take market share from traditional toys. The bankruptcy of retailer Toys R Us also hit sales hard. Weak forecasts led an analyst at Davidson to quip “either they are super lowballing or the company is falling apart.”

Nevertheless, a two-pronged turnaround strategy by CEO Ynon Kreiz has proven successful. By licensing its intellectual property (IP) for movies and cutting costs, Mattel has reemerged as a blue-chip toymaker to buy on the dips.

7. Dover (DOV)

Swing traders are occasionally given second chances at buying companies on the dip. Last week, Dover (NYSE:DOV) made that list after seeing a slight decline. Shares had initially dropped after a disappointing Q3 earnings report and the recent pullback brought prices back to that initial level.

Dover is a highly diversified industrial company that spans engineered products, clean energy, imaging and climate products. Essentially, they produce everything from loader dump trucks to miniature pumps for healthcare use.

The result is a stable firm with share prices that march along with economic growth. As a point of comparison, its implied volatility is about 6% lower than 3M (NYSE:MMM).

That makes the selloff in this “A+” rated stock particularly interesting. According to MarketMasterAI, shares should rise 14% over the next several months — an excellent return for a company that typically sees only a 10% rise in a year.

What Blue-Chip Stocks Tell Us About Market Timing

What Blue-Chip Stocks Tell Us About Market Timing

Earlier this month, payroll processing company ADP (NASDAQ:ADP) seemed to be in trouble. The company had just announced weaker-than-expected revenues and the stock had fallen 11%. It was ADP’s third-worst week since 2012.

But the selloff proved short-lived. Within two weeks, the stock had recovered roughly half of the selloff. An investor who bought in at the bottom could have seen gains of as much as 8% — a large amount for a very low-volatility stock.

History tells us that markets often overreact to slightly bad news, especially with blue-chip companies. Many investors seem trained to expect better-than-expected earnings and so they sell shares if things don’t meet their rosy projections.

History tells us that markets often overreact to slightly bad news, especially with blue-chip companies. Many investors seem trained to expect better-than-expected earnings and so they sell shares if things don’t meet their rosy projections.

However, these periods are often the best moments to buy. By following a consistent technical strategy — and applying it to the right companies — investors can remove emotions from the equation and see these selloffs for what they truly are: Perfect moments to buy high-quality companies at a discount drop.

— Tom Yeung

Legendary fund manager Louis Navellier – a man Forbes calls "the king of quants" – is going "ALL-IN" on this game-changing AI technology. He says, "This is the culmination of everything you've been reading about AI for the last 60 years."Get the details...

Source: Investor Place