Investing is such a fascinating occupation.

It’s a lifelong exercise in growth.

You grow, your knowledge grows, and your portfolio grows.

You grow, your knowledge grows, and your portfolio grows.

After investing and growing for nearly 15 years now, I’ve learned a huge lesson.

That lesson is this: Focus on quality.

Be it life or business, quality tends to win out over the long run.

That’s why dividend growth investing is such a powerful investment strategy.

This strategy is all about buying and holding shares in world-class businesses that pay reliable, rising dividends to their shareholders.

You can find many examples of these businesses by taking a look at the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

See, dividend growth investing, by its very nature, tends to funnel you right into quality businesses.

After all, a junk business would have a very difficult time being able to consistently pay out ever-larger cash dividends to shareholders – an activity that is only sustainable when it is supported by ever-higher profit.

By focusing my own capital on high-quality dividend growth stocks for more than a decade, I’ve built the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

In fact, largely because of this portfolio, I was able to retire in my early 30s.

In fact, largely because of this portfolio, I was able to retire in my early 30s.

My Early Retirement Blueprint lays out exactly how I was able to accomplish such a feat.

Now, quality is very important.

But so is valuation.

Price is only what you pay, but it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying and holding undervalued high-quality dividend growth stocks is a nearly-bulletproof way to build substantial wealth and passive dividend income over the long run.

Of course, doing that does require one to have an understanding of valuation.

But it’s not that difficult to build this understanding.

My colleague Dave Van Knapp’s Lesson 11: Valuation can assist with building that understanding, if you need the assistance.

Part of an overarching series of “lessons” on dividend growth investing, it shares a simple-to-follow valuation system that can be applied toward just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Graco Inc. (GGG)

Graco Inc. (GGG)

Graco Inc. (GGG) develops and manufactures fluid-handling systems and products.

Founded in 1926, Graco is now a $12 billion (by market cap) industrial might that employs 4,000 people.

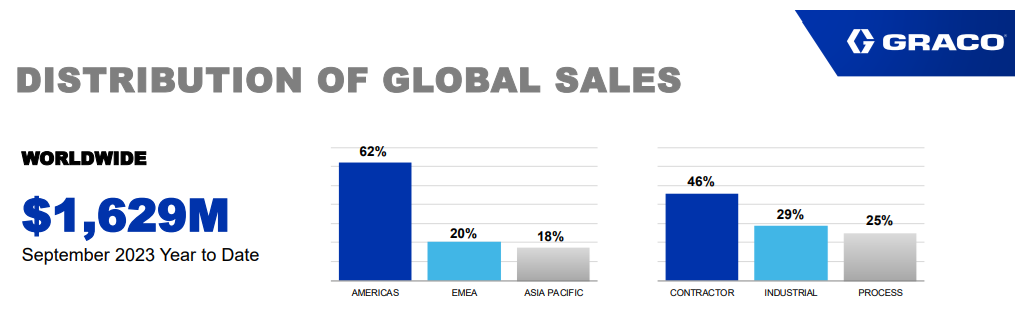

The company reports results across three segments: Contractor, 47% of FY 2022 sales; Industrial, 30%; and Process, 23%.

The Americas account for 60% of sales; Europe, Middle East, and Africa account for 21% of sales; and the remainder is Asia Pacific.

This is one of those under-the-radar industrial businesses that just consistently puts up the numbers.

This is one of those under-the-radar industrial businesses that just consistently puts up the numbers.

Graco has carved out a successful niche by focusing on products that help to manage fluids, coatings, and adhesives.

Its products include industrial pumps, valves, meters, hoses, and filters.

The company markets its products to a range of end markets, such as automotive manufacturing and the cosmetics industry.

There are a number of applications in which fluid has to be moved, metered, and controlled, which is exactly where Graco’s products come in.

An example of a Graco product in action would be professional paint sprayers used for buildings.

Many times, fluids that have to be moved are difficult in some way – corrosive, viscous, etc.

Graco specializes in producing products that can properly manage these fluids and has built a reputation for itself.

Morningstar highlights this key aspect to the investment thesis: “The company differentiates itself by manufacturing specialized products that handle difficult-to-move liquids, often used for niche applications where competition is limited.”

Specialization within a small niche, which wards off competition, has seemingly been a cornerstone of Graco’s winning strategy for decades now.

I don’t see anything on the horizon that changes this for Graco, which positions the company well for continued revenue, profit, and dividend growth.

Dividend Growth, Growth Rate, Payout Ratio and Yield

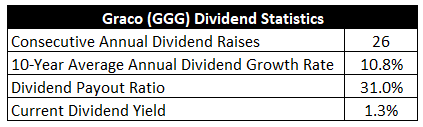

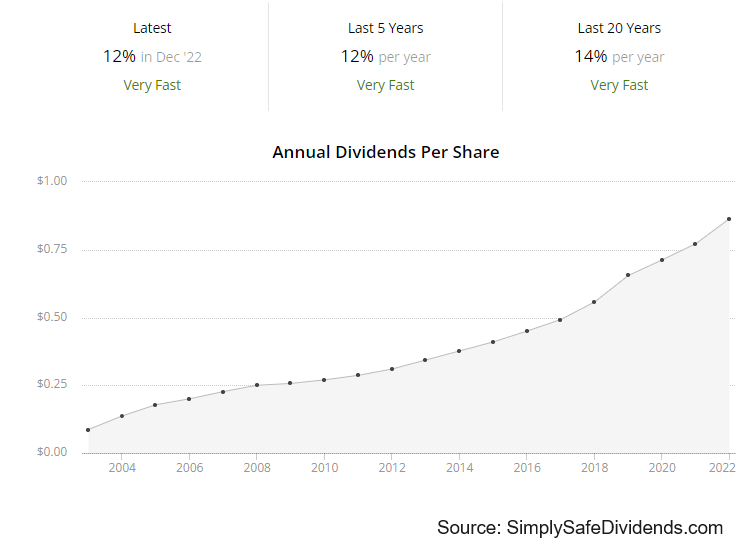

Already, Graco has increased its dividend for 26 consecutive years.

A very impressive track record that would qualify the company for Dividend Aristocrat status, if it were in the S&P 500.

The 10-year dividend growth rate is 10.8%.

That’s strong.

That’s strong.

But it’s even better than it looks.

Two reasons why.

First, the dividend growth has been about as linear as I’ve ever seen.

Graco has been incredibly consistent, relentlessly increasing the dividend at a low-double-digit rate for years.

Second, there’s been a modest acceleration in dividend growth.

The last two dividend raises came in at approximately 12%.

Awesome stuff.

The only drawback here might be the yield.

At 1.3%, there’s not a lot of current income to be had.

While it is 10 basis points higher than its own five-year average, this yield is such that it really does require one to be a long-term investor that can allow for those sizable dividend raises to stac k up over time.

k up over time.

And with the payout ratio at only 31%, I would expect those sizable dividend raises to keep stacking up.

For those who have the patience and time horizon necessary to let a high-quality compounder go to work, Graco clearly has the makings of a serious long-term builder of wealth and passive dividend income.

This is a healthy dividend that is growing at a rather high rate, which I think is super compelling (unless one is in or near retirement).

Revenue and Earnings Growth

As compelling as these metrics may be, many of them are looking backward.

However, investors must always be looking forward, as today’s capital is risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful when the time comes later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast like this should allow us to determine what the future growth path of the business could look like.

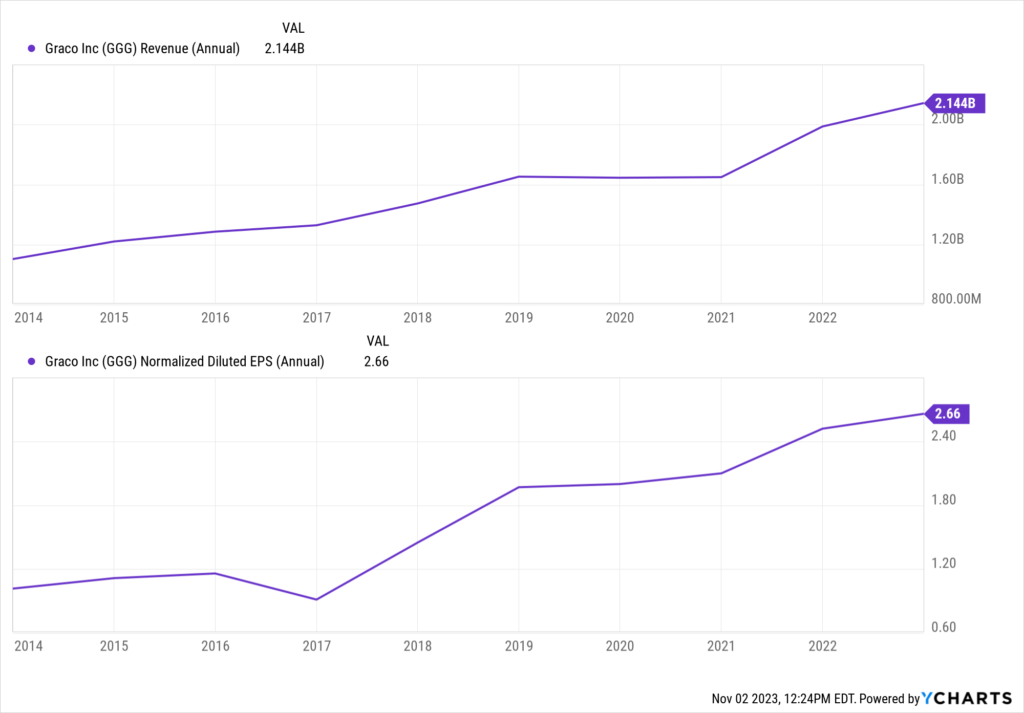

Graco increased its revenue from $1.1 billion in FY 2013 to $2.1 billion in FY 2022.

That’s a compound annual growth rate of 7.5%.

Really good.

I usually look for a mid-single-digit top-line growth rate from a fairly mature business like this, and Graco is more than delivering.

Meanwhile, earnings per share grew from $1.12 to $2.66 over this 10-year period, which is a CAGR of 10.1%.

We can now see where that double-digit dividend growth has been coming from.

We can now see where that double-digit dividend growth has been coming from.

The close relationship between EPS growth and dividend growth over the last decade shows deft control by management.

Excess bottom-line growth has been fueled by modest margin expansion and share buybacks.

For perspective on the latter point, the outstanding share count has been reduced by 8% over the last decade.

It’s worth pointing out that Graco’s growth has been very smooth and consistent over the years, showing very few bumps along the way.

The secular nature of the growth is very alluring.

Looking forward, CFRA is projecting a 10% CAGR for Graco’s EPS over the next three years.

CFRA is apparently forecasting a continuation of the status quo.

That seems realistic to me.

Graco’s most recent earnings report, Q3 FY 2023, showed 14.9% YOY growth in EPS.

In my view, that’s remarkable.

With rising interest rates, challenging comps, spotty growth, and normalization trends off of the pandemic booms, many other businesses out there have found the current environment to be tough.

I’ve seen countless earnings reports out there showing YOY declines, even among high-quality businesses, yet Graco put up above-trend growth.

Now, it did come off of roughly flat YOY sales.

But expanded margins saved the quarter.

CFRA stated this after the report: “We’re encouraged by [Graco]’s execution on margins amid a more difficult demand environment and see enhanced profitability driving EPS expansion in Q4 and into 2024.”

Boy, continued margin expansion in this kind of environment is heartening.

I think that just goes to show how great and durable this business model really is.

A lot of this likely comes down to the fact that approximately 40% of Graco’s sales are tied to aftermarket sales of parts and accessories that are designed to service the installed base of products (since these difficult-to-handle fluids naturally cause plenty of wear and tear).

If we take CFRA’s projection as our near-term base case, that easily sets up Graco to grow its dividend at a like rate.

The low payout ratio, which could be slowly expanded, would even allow for some modest surplus growth to the dividend.

Put another way, Graco has a clear road ahead for low-double-digit dividend growth, which would be right in line with what it’s already been doing for years now.

Starting off with the 1.3% yield pieces together a picture of low-double-digit annualized total return from here, assuming no major changes with the valuation.

That’s quite appealing, especially considering how consistent Graco is.

I will note that Graco has been a total return monster over the years, with the stock price up ~188% over the last 10 years alone.

Graco has been a tremendous builder of wealth and passive dividend income over the decades, and nothing indicates any serious disruptions to this on a go-forward basis.

Financial Position

Moving over to the balance sheet, Graco has a nearly flawless financial position.

Long-term debt is immaterial and near $0.

It’s essentially a debt-free business.

Graco has a net cash position, which positions the company very well in an environment with elevated interest rates.

Profitability is extremely robust.

Net margin has averaged 21.2% over the last five years, while return on equity has averaged 32.1%.

Graco sports very high returns on capital, which I love to see.

There is little to fault here.

Simply put, this is a phenomenal operation.

And with economies of scale, switching costs, entrenched share within a small niche, specialization, and reputation, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Graco is mildly acquisitive, and this introduces execution risks.

Graco’s international footprint exposes the company to idiosyncratic foreign markets and currency exchange rates.

There is cyclicality in many of Graco’s end markets, which means Graco is somewhat reliant on the overall health of the global economy.

Graco’s niche is an advantage in terms of warding off competition, but it also could be the biggest risk in terms of limiting long-term growth potential.

These risks are worth carefully considering, but the quality and growth profile of the business must also be considered.

Also, the valuation, which looks attractive after the stock’s 15%+ drop in price from its 52-week high, is worthy of consideration…

Stock Price Valuation

The stock is trading hands for a P/E ratio of 24.4.

In and of itself, that’s not a terribly low earnings multiple.

However, it’s a different story on the relative side of things.

The stock’s own five-year average P/E ratio is 28.2, so it’s come down in a meaningful way.

The sales multiple of 5.5 is also quite a bit lower than its own five-year average of 5.9.

And the yield, as noted earlier, is higher than its own recent historical average.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 12% dividend growth rate for the next 12 years, and a long-term dividend growth rate of 8%.

I’m assuming a continuation of the dividend growth status quo for the medium term, similar to what CFRA is baking into their earnings growth forecast.

I see nothing to indicate how or why Graco won’t be able to continue delivering low-double-digit dividend raises for the foreseeable future.

The last two dividend raises both came in at around 12%.

And Graco’s most recent earnings report showed 14.9% YOY EPS growth.

Now, I wouldn’t expect this to persist forever, and I do see that slowing down when moving out into a longer time horizon (which is in the model).

But the low payout ratio, stellar balance sheet, and high business growth all give Graco the room necessary to keep moving the dividend needle at an aggressive pace for years to come.

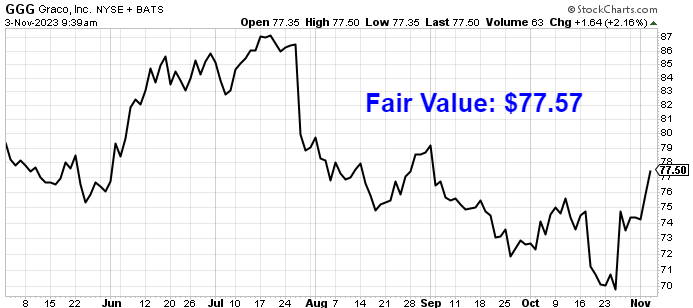

The DDM analysis gives me a fair value of $75.72.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think I put together a fair and balanced model, yet the stock comes out looking at least slightly undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates GGG as a 3-star stock, with a fair value estimate of $77.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates GGG as a 3-star “HOLD”, with a 12-month target price of $80.00.

I came out the lowest, but we’re all in a fairly tight grouping. Averaging the three numbers out gives us a final valuation of $77.57, which would indicate the stock is possibly 4% undervalued.

Bottom line: Graco Inc. (GGG), with its secular growth, high returns on capital, and stellar balance sheet, is one of the highest-quality businesses I’ve ever looked at. With a market-like yield, double-digit dividend growth, a low payout ratio, more than 25 consecutive years of dividend increases, and the potential that shares are 4% undervalued, this is a great candidate for long-term dividend growth investors who are willing to accept only modest undervaluation on a wonderful business and prefer high-quality compounders to optically cheap, higher-yield shares of lesser-quality businesses.

Bottom line: Graco Inc. (GGG), with its secular growth, high returns on capital, and stellar balance sheet, is one of the highest-quality businesses I’ve ever looked at. With a market-like yield, double-digit dividend growth, a low payout ratio, more than 25 consecutive years of dividend increases, and the potential that shares are 4% undervalued, this is a great candidate for long-term dividend growth investors who are willing to accept only modest undervaluation on a wonderful business and prefer high-quality compounders to optically cheap, higher-yield shares of lesser-quality businesses.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is GGG’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, GGG’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income