Why are high-quality dividend growth stocks appealing? Well, these stocks represent equity in some of the world’s best businesses.

How do you know that these are great businesses? Because the reliable, rising dividends the stocks pay out get funded by the reliable, rising profits the businesses are generating. It’s pretty difficult to write ever-larger checks to shareholders without being able to back that up. And if you can build a portfolio of high-quality dividend growth stocks that pay enough dividend income for you to live off of, that’s financial independence.

It’s easy to see why these stocks are appealing. But when they’re on sale – when they’re undervalued – that’s when the appeal is cranked up even more.

See, price and yield are inversely correlated. All else equal, lower prices result in higher yields. This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach.

Now, lower valuations often come when there’s volatility. But I always see short-term volatility as a long-term opportunity. That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint. With all of that out of the way, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what this analysis is all about.

Today, I want to tell you my top 5 dividend growth stocks for November 2023.

Ready? Let’s dig in.

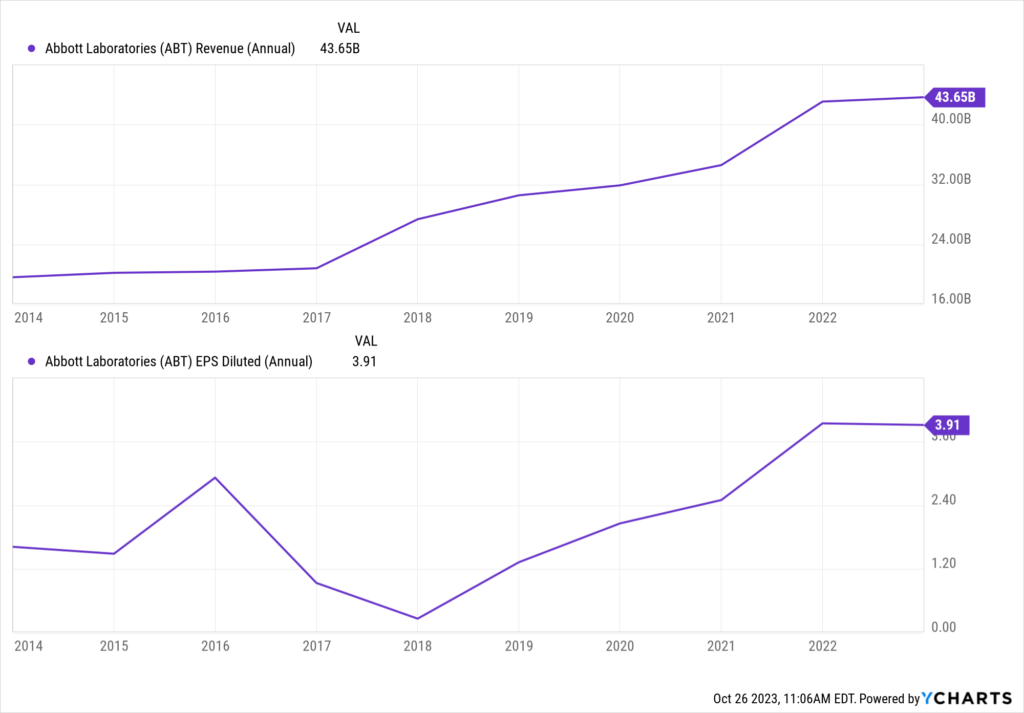

My first dividend growth stock for November 2023 is Abbott Laboratories (ABT). Abbott Laboratories is a multinational medical devices and health care company.

I really love global, diversified healthcare conglomerates. These businesses are in the driver’s seat. We already know that the human race continues to grow. We’re at 8.1 billion people now. Simultaneously, on average, we’re living longer than ever before and richer than ever before.

A larger pool of older people naturally creates more demand for quality healthcare, due to the human condition. And with more disposable income, the means to pay for that demand is present. That explains why this company consistently puts up the results. Over the last decade, Abbott Laboratories compounded its revenue at an annual rate of 9.3% and its EPS at an annual rate of 10.3%. This is one of the most dependable dividends out there.

While Abbott Laboratories in its current form has only increased its dividend for 10 consecutive years, it’s actually a Dividend Aristocrat. That’s because the dividend growth track record stretches back before Abbott Laboratories spun-off its pharmaceutical arm, now known as AbbVie (ABBV).

While Abbott Laboratories in its current form has only increased its dividend for 10 consecutive years, it’s actually a Dividend Aristocrat. That’s because the dividend growth track record stretches back before Abbott Laboratories spun-off its pharmaceutical arm, now known as AbbVie (ABBV).

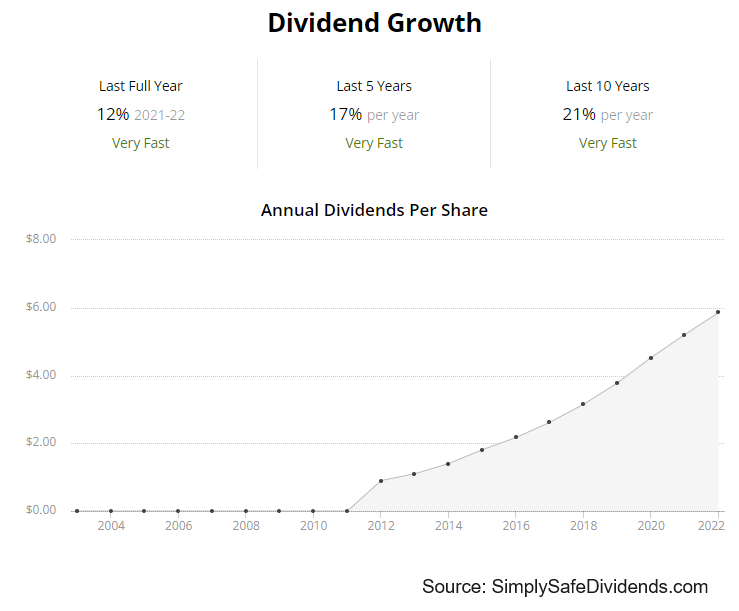

Abbott Laboratories has declared 399 consecutive quarterly dividends since 1924 and has increased its dividend for 51 consecutive years. The five-year DGR is 12.1%. And you pair that double-digit dividend growth with the stock’s market-beating 2.2% yield. With a 46.4% payout ratio, based on midpoint guidance for FY 2023 adjusted EPS, this dividend looks as dependable as it ever has. This Dividend Aristocrat looks attractively valued after a recent 15% slide.

The stock has gone almost straight down since late July. But the business continues to slowly move ahead. That’s the constant disconnect that exists between businesses and their shares over shorter periods of time.

We recently put together a full analysis and valuation video on Abbott Laboratories, which should be live by the time this video comes out. The estimate for fair value on the healthcare conglomerate came out to just over $109/share. The stock’s current pricing in the mid-$90 area looks pretty compelling against that. Take a look at this Dividend Aristocrat.

My second dividend growth stock for November 2023 is American Tower (AMT). American Tower is is a real estate investment trust that owns, operates, and develops broadcast communications infrastructure.

We have a pretty simple business model here. American Tower erects, then rents out vertical antenna sites to service providers. Service providers sign multiyear leases in order to access towers and install their equipment. This equipment is necessary to carry out services such as telephony, mobile data, radio, and broadcast television.

A linchpin of American Tower’s future success revolves around how 5G and IoT are converging to make American Tower’s infrastructure more necessary and important than ever before. If past is prologue, there’s a lot to look forward to. The company’s 10-year CAGR for revenue is 13.6%, while the 10-year CAGR for AFFO/share is 11.9%. Unlike a lot of other REITs out there, this dividend has been growing quickly.

Most REITs tend to be slow-growth income vehicles. And, you know, that’s okay for income-oriented investors who are more concerned with income than total return. However, American Tower has been a growth and return monster. The dividend, which has been increased for 13 consecutive years, has a 10-year DGR of 20.3%, which blows away almost every other REIT out there. Now, the dividend growth rate has slowed of late.

We’re looking at something closer to a high-single-digit rate recently. On the other hand, in order to calibrate for that, the stock’s yield has risen to 4.1%. That is nearly twice as high as the stock’s own five-year average yield. Even if growth slows permanently from here, you’re now able to lock in a 4%+ yield, which is almost unheard of for American Tower. And with a payout ratio of 66.8%, based on midpoint guidance for this year’s AFFO/share, this is one of the most well-covered dividends in REITdom.

We’re looking at something closer to a high-single-digit rate recently. On the other hand, in order to calibrate for that, the stock’s yield has risen to 4.1%. That is nearly twice as high as the stock’s own five-year average yield. Even if growth slows permanently from here, you’re now able to lock in a 4%+ yield, which is almost unheard of for American Tower. And with a payout ratio of 66.8%, based on midpoint guidance for this year’s AFFO/share, this is one of the most well-covered dividends in REITdom.

This stock’s near-50% slide in price from its all-time high has created a great long-term investment opportunity, in my view.

American Tower was a rare REIT that, for many years, acted more like a high-quality compounder than an income play. And that often came with a high valuation and low yield to match the performance. With the recent fall from grace in the stock, which has been prompted by a confluence of factors ranging from higher interest rates to a slowdown in the business, this REIT finally offers up a high yield and low valuation.

Take the P/CF ratio of 17, for example. Its five-year average? 25.7. That is a massive dislocation. We’ll have a full analysis and valuation video coming out soon on American Tower, so keep an eye out for that. In the meanwhile, this name has to be on your radar.

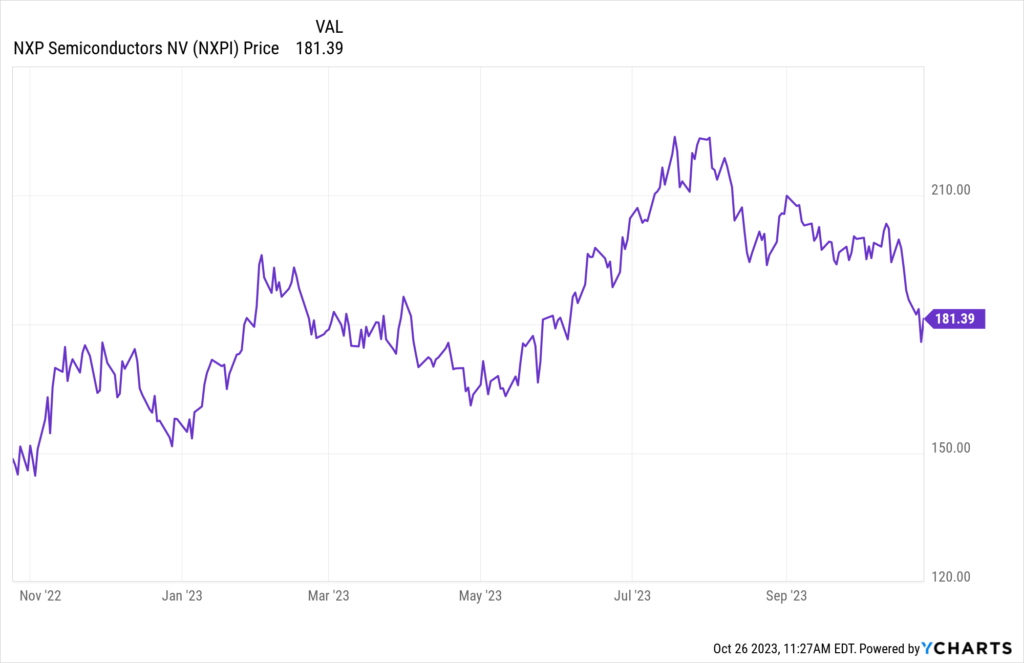

My third dividend growth stock for November 2023 is NXP Semiconductors (NXPI). NXP Semiconductors is a Dutch semiconductor company that supplies high-performance mixed-signal chips.

The entire chip industry is ripe for picking for long-term dividend growth investors. The demand for and usage of chips is only increasing. Our world is becoming increasingly technological, and chips power all of that. Meanwhile, all of these different chip companies have these facets to them that offer a lot of differentiation.

In the case of NXP Semiconductors, this company has really focused itself on automotive. Not a bad place to be at all, as autos are becoming more smart and more electric. What does that mean? More content per car. And that bodes very well for this company, which has already compounded its revenue at an annual rate of 11.9% and its EPS at an annual rate of 25.6% over the last decade. Double-digit business growth. Double-digit dividend growth.

This company’s track record of six consecutive years of dividend growth might be a bit short, but what a start NXP Semiconductors is off to. I say that because the three-year DGR is 40.2%. Even the most recent dividend raise was 20%. Very, very strong dividend growth here. The stock yields 2.2%, which is more than decent against the growth profile. And the payout ratio is only 38.2%. With a fairly low payout ratio and brisk business growth, I’d expect the dividend to continue growing at a high rate for years to come.

This company’s track record of six consecutive years of dividend growth might be a bit short, but what a start NXP Semiconductors is off to. I say that because the three-year DGR is 40.2%. Even the most recent dividend raise was 20%. Very, very strong dividend growth here. The stock yields 2.2%, which is more than decent against the growth profile. And the payout ratio is only 38.2%. With a fairly low payout ratio and brisk business growth, I’d expect the dividend to continue growing at a high rate for years to come.

This isn’t the cheapest stock out there. But it’s a great business. And the valuation doesn’t seem to be fully accounting for the quality.

Like just about everything else out there, this stock has had a tough go of it recently. It’s down nearly 20% from its 52-week high and now priced at about $185. This steep drop has created an interesting entry point for those looking to get in for the long haul. We already put together a full analysis and valuation video on this great Dutch business, and that video should go live soon. The estimate for the business’s intrinsic value worked out to $236.41/share. So you can see the gap there between pricing and potential value. If you don’t yet own a slice of this business, it could be a good time to think about changing that.

Like just about everything else out there, this stock has had a tough go of it recently. It’s down nearly 20% from its 52-week high and now priced at about $185. This steep drop has created an interesting entry point for those looking to get in for the long haul. We already put together a full analysis and valuation video on this great Dutch business, and that video should go live soon. The estimate for the business’s intrinsic value worked out to $236.41/share. So you can see the gap there between pricing and potential value. If you don’t yet own a slice of this business, it could be a good time to think about changing that.

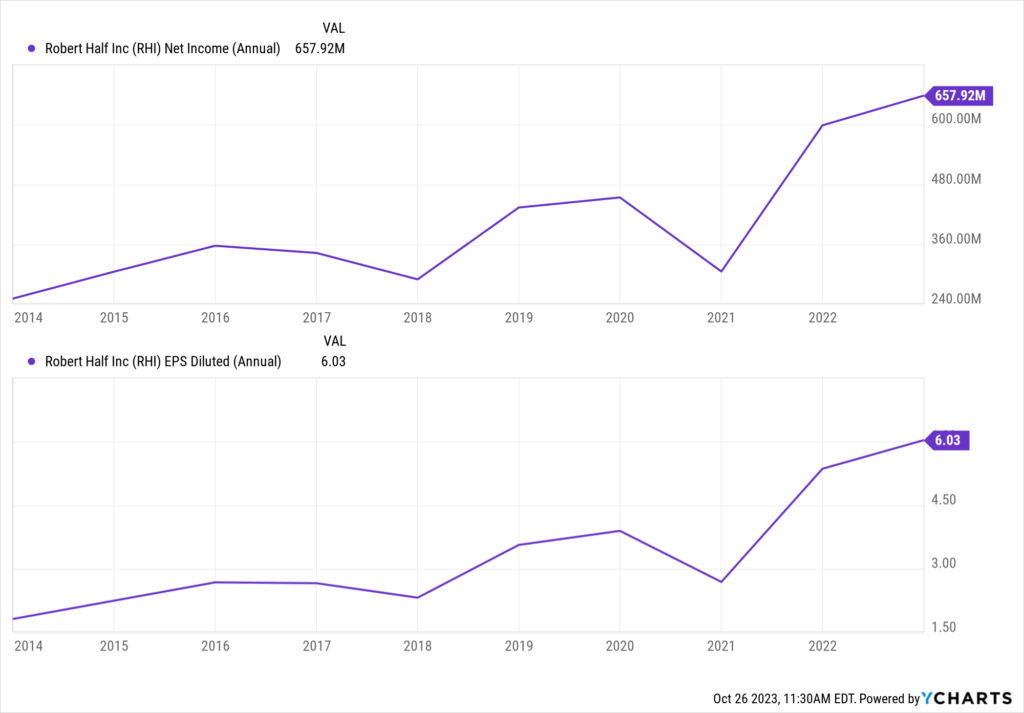

My fourth dividend growth stock for November 2023 is Robert Half (RHI). Robert Half is a global staffing and consulting company.

This is one of those boring, under-the-radar business models that rarely even comes to mind as an investment idea. But that’s not a bad thing. If anything, it’s a good thing. Most of my best investments over the years have been hidden gems that nobody is talking about. And let’s be clear. Robert Half is a gem of a business. High returns on capital. Fat margins. No long-term debt. And plenty of growth. We’re talking a 6.2% CAGR in revenue and a 14.2% CAGR in EPS over the last decade. The dividend growth track record here is impressive, despite the lack of fanfare.

Again, who’s talking about Robert Half? Almost nobody, other than me. But this company has increased its dividend for 20 consecutive years, with a 10-year DGR of 11.1%. Better yet, the dividend raises have been remarkably linear, with the dividend rising by a steady 11%+ year after year. The stock yields 2.7%, which is more than decent. And the payout ratio is only 38%, indicating what a well-covered dividend it is. Partly because of the lack of attention, the stock usually has low multiples. But it looks especially cheap right now.

Again, who’s talking about Robert Half? Almost nobody, other than me. But this company has increased its dividend for 20 consecutive years, with a 10-year DGR of 11.1%. Better yet, the dividend raises have been remarkably linear, with the dividend rising by a steady 11%+ year after year. The stock yields 2.7%, which is more than decent. And the payout ratio is only 38%, indicating what a well-covered dividend it is. Partly because of the lack of attention, the stock usually has low multiples. But it looks especially cheap right now.

The stock’s five-year average P/E ratio is 17.9. Not super demanding. However, it’s currently 14.4. So we’re well below what’s already a pretty low level. If our full analysis and valuation video on Robert Half isn’t out yet, it should be soon. And in that video, the estimate for the business’s fair value came out to $92.56/share.

Shares are currently going for about $72.50. If you pull up the 40-year stock chart on Robert Half, you’ll see that the stock has returned more than 16,000% – before dividends. It’s been a remarkable long-term performer. A long-term entry point could be open right now. Take a look.

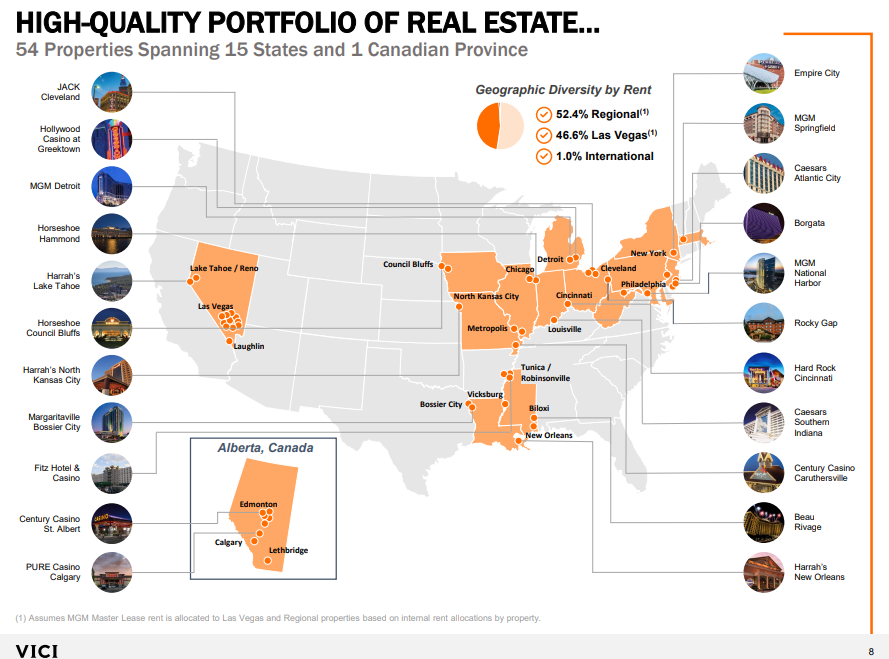

My fifth dividend growth stock for November 2023 is VICI Properties (VICI). Vici Properties is a real estate investment trust that specializes in casino properties.

This is a unique REIT. Whereas most REITs offer easy exposure to pretty standard commercial real estate, such as apartment complexes or shopping centers, Vici Properties has concentrated itself on casino properties across the Las Vegas Strip. In fact, Vici Properties is the largest landlord on the Strip. Investing in Vici Properties is investing in Las Vegas, and I think that city’s future looks bright.

Vici Properties had its IPO in 2018, so I don’t have a decade’s worth of top-line and bottom-line growth to throw at you. However, I can tell you that Vici Properties has 100% occupancy and collected 100% of rent during the pandemic. Why? These properties are highly unique and are not going to be just given up by their tenants. These are captive customers. For FY 2022, AFFO/share grew by 6.1% YOY. If we look at midpoint guidance for FY 2023, YOY AFFO/share growth is projected to be 10.1%.

Vici Properties had its IPO in 2018, so I don’t have a decade’s worth of top-line and bottom-line growth to throw at you. However, I can tell you that Vici Properties has 100% occupancy and collected 100% of rent during the pandemic. Why? These properties are highly unique and are not going to be just given up by their tenants. These are captive customers. For FY 2022, AFFO/share grew by 6.1% YOY. If we look at midpoint guidance for FY 2023, YOY AFFO/share growth is projected to be 10.1%.

This REIT has put up the dividend growth right out of the gate. Vici Properties has increased its dividend for five consecutive years, so it’s off to a running start. The three-year DGR is 8.2%, which lines up with the high-single-digit bottom-line growth the REIT has been producing thus far. That kind of growth definitely exceeds what a lot of other REITs out there offer.

Yet the 6.1% yield is very much REIT-like. The payout ratio, at 78.3%, based on midpoint guidance for this year’s AFFO/share, is quite reasonable by REIT standards and shows a pretty healthy dividend that should continue to grow roughly in line with AFFO/share.

Like most other REITs, this stock is having a miserable 2023. However, that’s exactly where the long-term opportunity could be.

Like I said earlier, short-term volatility is a long-term opportunity. This stock is down nearly 15% this year. Yet the business isn’t down 15% at all. To the contrary, the most recent report – Q2 – showed 11.9% YOY AFFO/share growth. If you want to own a slice of trophy properties like Caesars Palace and The Venetian, Vici Properties is your gateway into them.

The P/CF ratio is now at just 13.2. That is ludicrously low. Its own five-year average is 16.5, which, in and of itself, isn’t very high. There is $16.3 billion in net debt and steady dilution to deal with here – debt and dilution is a common theme in REITdom – but it’s a pretty fascinating real estate concept that comes with a nice yield and undemanding valuation.

The P/CF ratio is now at just 13.2. That is ludicrously low. Its own five-year average is 16.5, which, in and of itself, isn’t very high. There is $16.3 billion in net debt and steady dilution to deal with here – debt and dilution is a common theme in REITdom – but it’s a pretty fascinating real estate concept that comes with a nice yield and undemanding valuation.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income