I’ve learned a lot from Warren Buffett.

He’s been a bit of a surrogate grandfather to me, passing on his timeless lessons to an eager ear.

After digesting so much of his wisdom over the many years, I think a lot of what he has to say can be summed up pretty succinctly.

Much of it comes down to living below your means and intelligently investing your savings.

That’s a simple but highly effective combination for building significant wealth and passive income over time.

But it’s all easier said than done, right?

But it’s all easier said than done, right?

Perhaps.

However, whereas living below one’s means is largely an individual lifestyle call, intelligent investing is something that has broader implications.

I’d argue that one very intelligent way to invest is to use the dividend growth investing strategy.

This is a long-term investment strategy whereby one buys and holds shares in world-class businesses that pay reliable, rising cash dividends to their shareholders.

You can find many examples of these businesses on the Dividend Champions, Contenders, and Challengers list.

That list has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

That list has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Dividend growth investing works so well because it automatically funnels you right into some of the world’s best businesses.

After all, only great businesses can reliably pay rising dividends, as that kind of behavior requires the underlying economic activity (rising revenues and profits) to support it.

This strategy has guided me for more than a decade now as I’ve gone about building the FIRE Fund – my real-money portfolio that generates enough five-figure passive dividend income for me to live off of.

Indeed, I’ve been fortunate enough to be able to live off of dividend income since I retired in my early 30s.

My Early Retirement Blueprint explains how I was able to retire at such a young age.

A lot of my success can be traced back to the idea of intelligent investing.

But intelligent investing is about more than just selecting the right businesses for investment.

It’s also about valuation at the time of investment.

Price is only what you pay, but it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

If you can live below your means and consistently buy undervalued high-quality dividend growth stocks with your savings, you have an excellent shot at building significant wealth and passive dividend income over time.

Of course, this does require one to have some kind of basic understanding of valuation.

But it’s not as difficult as you might think.

Fellow contributor Dave Van Knapp’s Lesson 11: Valuation will help to explain valuation in very simple-to-understand terms.

It’s part of a comprehensive series of “lessons” that are designed to teach the dividend growth investing strategy, and it does a great job of laying out a valuation template that can be easily understood and applied.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Abbott Laboratories (ABT)

Abbott Laboratories (ABT)

Abbott Laboratories (ABT) is a multinational medical devices and health care company.

Founded in 1888, Abbott Laboratories is now a $158 billion (by market cap) healthcare giant that employs 115,000 people.

The company reports results across four segments: Diagnostics, 38% of FY 2022 revenue; Medical Devices, 34%; Nutrition, 17%; and Established Pharmaceuticals, 11%.

Nearly 60% of the company’s sales are international, while the remaining ~40% come from the US.

As we can see, this is a broadly diversified healthcare company.

That’s true both in product and geography terms.

And that’s a great spot to be in as we enter 2024 soon.

I say that because of the demographic tailwinds that are blowing this company’s way.

Healthcare is in secular growth mode.

The world is becoming larger, older, and richer – simultaneously.

It does not take a big mental leap to understand how that directly leads to more demand for high-quality healthcare products and services.

After all, we’re talking about a larger pool of human beings who are living longer, and these same human beings are increasingly able to afford the kind of healthcare that is often necessary throughout the aging process to lengthen life and/or make life more comfortable.

This is actually quite circular.

It’s partly because of higher-quality healthcare, and more access to it, that many people are living longer than ever before.

If you zoom back to 1900, we didn’t even have antibiotics yet.

Modern healthcare is a miracle in many ways.

As one of the world’s largest and most dynamic healthcare conglomerates, Abbott Laboratories is at the tip of that spear.

That’s why the company is positioned so well to continue growing its revenue, profit, and dividend for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

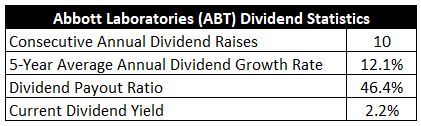

Already, Abbott Laboratories has increased its dividend for 10 consecutive years.

While a good start on its face, this somewhat short track record belies the company’s true dividend growth commitment, which actually stretches back many decades.

Indeed, Abbott Laboratories is a Dividend Aristocrat.

A company has to have at least 25 consecutive years of dividend increases in order to become a Dividend Aristocrat.

This disconnect can be explained by the spin-off of pharmaceutical assets by Abbott Laboratories into a new, independent company called AbbVie Inc. (ABBV) back in 2013.

This move “reset” the dividend and its growth, even though shareholders of Abbott Laboratories who kept their AbbVie shares were made whole and saw their dividend income continue to rise straight through this process.

Putting that aside, Abbott Laboratories has declared 399 consecutive quarterly dividends since 1924 and has increased its dividend for 51 consecutive years.

The dividend pedigree here is unquestionably great.

The dividend pedigree here is unquestionably great.

A five-year dividend growth rate of 12.1% shows plenty of gas in the tank, despite decades of dividend growth already.

And you get to pair that dividend growth with the stock’s market-beating 2.2% yield.

This yield, by the way, is 60 basis points higher than its own five-year average.

And the dividend is protected by a payout ratio of 46.4%, based on midpoint guidance for FY 2023 adjusted EPS.

Abbott Laboratories has one of the most storied dividend growth histories out there.

This is the stuff of legend.

Other than investors who only go after high-yield stuff, I really can’t think of anybody who would dislike anything here.

Revenue and Earnings Growth

As much as there is to like about these dividend metrics, most of them are looking into the past.

However, investors must peer into the future, as today’s capital is being risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be useful when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast like this should give us the information we need in order to judge what the future growth path of the business could look like.

Abbott Laboratories raised its revenue from $19.7 billion in FY 2013 to $43.7 billion in FY 2022.

That’s a compound annual growth rate of 9.3%.

Strong.

I like to see mid-single-digit top-line growth from a mature business like this, but Abbott Laboratories is knocking it out of the park.

Meanwhile, earnings per share grew from $1.62 to $3.91 over this period, which is a CAGR of 10.3%.

Boy, double-digit bottom-line growth from a Dividend Aristocrat?

One can do a lot worse than that.

Looking forward, CFRA currently has no three-year EPS CAGR forecast for Abbott Laboratories.

That’s unfortunate, as I do like to line up the proven past with a future forecast, even though the future is obviously so difficult to predict with any kind of reliable accuracy.

That said, CFRA does have an interesting and insightful nugget in their analysis.

CFRA sees “record EPS of $5.58 by 2026 as ABT’s stand-out glucose monitoring technology (Freestyle Libre) gains market share.”

So there you go.

If we compare that to the $3.91 that Abbott Laboratories printed for FY 2022, that would be a CAGR of 9.3% over this upcoming five-year period.

Basically, CFRA seems to be assuming a continuation of the status quo, more or less.

I don’t see anything wrong with that, as Abbott Laboratories has been a model of consistency for decades.

It just steadily marches its revenue, profit, and dividend higher in a very unceremonious way.

I’d also like to point out this glowing passage from CFRA on Abbott Laboratories: “We think shares of [Abbott Laboratories] will outperform the market and peers over the long term, driven by its highly innovative diversified health care businesses allowing for growing market share over time, a strong financial position, and a consistently growing dividend.”

Isn’t that beautiful?

It succinctly highlights what’s so great about a long-term investment Abbott Laboratories, which is supported by outperformance and a dividend that consistently grows through thick and thin.

If we take CFRA’s near-term model as our base case for what Abbott Laboratories can do in terms of EPS growth, that would allow for similar dividend growth.

With the payout ratio being low, there’s even flexibility for the dividend growth to slightly outpace EPS growth.

That is to say, the dividend is set up for low-double-digit growth over the coming years, which would be right in line with what’s been occurring over the last several years already.

Again, it’s incredible consistency.

And you get a market-beating yield while you wait for those dividend raises to stack up.

I find that to be very compelling.

Financial Position

Moving over to the balance sheet, Abbott Laboratories has a fantastic financial position.

The long-term debt/equity ratio is 0.4, while the interest coverage ratio is over 11.

These numbers don’t really do the balance sheet justice, though, as cash on hand nearly covers all long-term debt.

Moreover, long-term debt has decreased meaningfully over the last several years, all while the company’s cash position has simultaneously increased.

There has been a marked improvement in the balance sheet here.

This is against a backdrop of many other companies out there gorging on cheap debt, showcasing great stewardship from the management team at Abbott Laboratories.

Profitability is very good.

Net margin has averaged 12.8% over the last five years, while return on equity has averaged 14.8%.

There is a lot to like about this Dividend Aristocrat.

And with economies of scale, IP, R&D, entrenched sales relationships, technological know-how, regulatory expertise, and barriers to entry, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

I see all three of those risks as elevated for this particular business model relative to a lot of other business models.

On the other hand, high regulatory hurdles, especially around medical devices, act as barriers to entry and stave off new competition.

Being an international business, Abbott Laboratories has exposure to different jurisdictions and currency exchange rates.

Product recalls are a constant risk.

There’s execution and product quality risk, as evidenced by the company’s recent issues with baby formula production.

The introduction of new weight-loss drugs in the marketplace may reduce demand for some of the company’s various offerings.

The company faces some technological obsolescence risk, especially around medical devices.

I think these risks are worth considering, but the quality and growth of the business must also be considered.

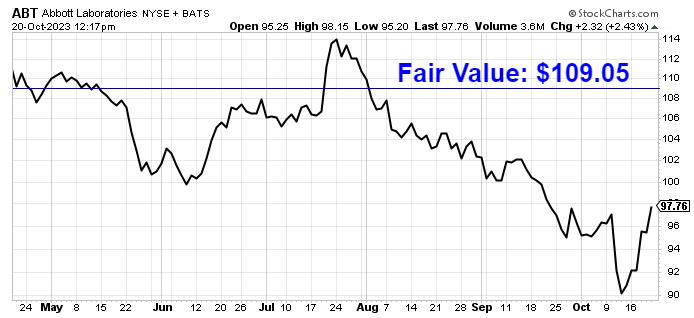

And with the stock down more than 30% from its all-time high, the valuation, which looks attractive, has to be considered…

Stock Price Valuation

The stock is trading hands for a P/E ratio of 22.3.

That’s based on TTM adjusted EPS.

For a company that’s reliably grown its bottom line at double-digit rates, that strikes me as a very reasonable earnings multiple.

I’d also point to the P/S ratio of 4.2 being well off of its own five-year average of 4.9.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

That dividend growth rate is at the very upper end of what I allow for, but Abbott Laboratories is exactly the kind of business model that gets the benefit of the doubt.

This is a Dividend Aristocrat that’s proven a rare ability to grow the dividend at a high rate for decades on end.

Anything can change, and nothing is ever guaranteed in business, but Abbott Laboratories has been one of the most reliable dividend growers that’s ever existed.

With the payout ratio being low and the near-term picture for earnings growth being supportive of low-double-digit dividend growth, I think my model is, if anything, just slightly cautious.

The DDM analysis gives me a fair value of $110.16.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Despite what was arguably a pretty conservative look at things, the stock still comes out looking relatively cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates ABT as a 4-star stock, with a fair value estimate of $104.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates ABT as a 4-star “BUY”, with a 12-month target price of $113.00.

I came out pretty much right in the middle. Averaging the three numbers out gives us a final valuation of $109.05, which would indicate the stock is possibly 12% undervalued.

Bottom line: Abbott Laboratories (ABT) is a terrific business benefiting from long-term, structural demographic tailwinds that put its entire industry in secular growth mode. With a market-beating yield, a low payout ratio, double-digit dividend growth, 10 consecutive years of dividend increases, and the potential that shares are 12% undervalued, long-term dividend growth investors looking for a good deal on a great business have a strong candidate here.

Bottom line: Abbott Laboratories (ABT) is a terrific business benefiting from long-term, structural demographic tailwinds that put its entire industry in secular growth mode. With a market-beating yield, a low payout ratio, double-digit dividend growth, 10 consecutive years of dividend increases, and the potential that shares are 12% undervalued, long-term dividend growth investors looking for a good deal on a great business have a strong candidate here.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is ABT’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 90. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, ABT’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income