High-quality dividend growth stocks are some of the best stocks money can buy.

After all, these stocks represent ownership in world-class businesses that are so good at making ever-more money, they pay out ever-larger cash dividends to their shareholders. Many of these businesses are selling you the products and/or services that you use. May as well earn some of that spending back, right?

These stocks can be highly appealing for long-term investment. But when they’re on sale – when they’re undervalued – that’s when the appeal is off the charts.

See, price and yield are inversely correlated. All else equal, lower prices result in higher yields. This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach.

Now, lower valuations often come when there’s volatility. But I always see short-term volatility as a long-term opportunity. That perspective helped me to go from below broke at age 27 to financially free at 33. By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

With all of that out of the way, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what this article is all about.

Today, I want to tell you my top 5 dividend growth stocks for October 2023.

Ready? Let’s dig in.

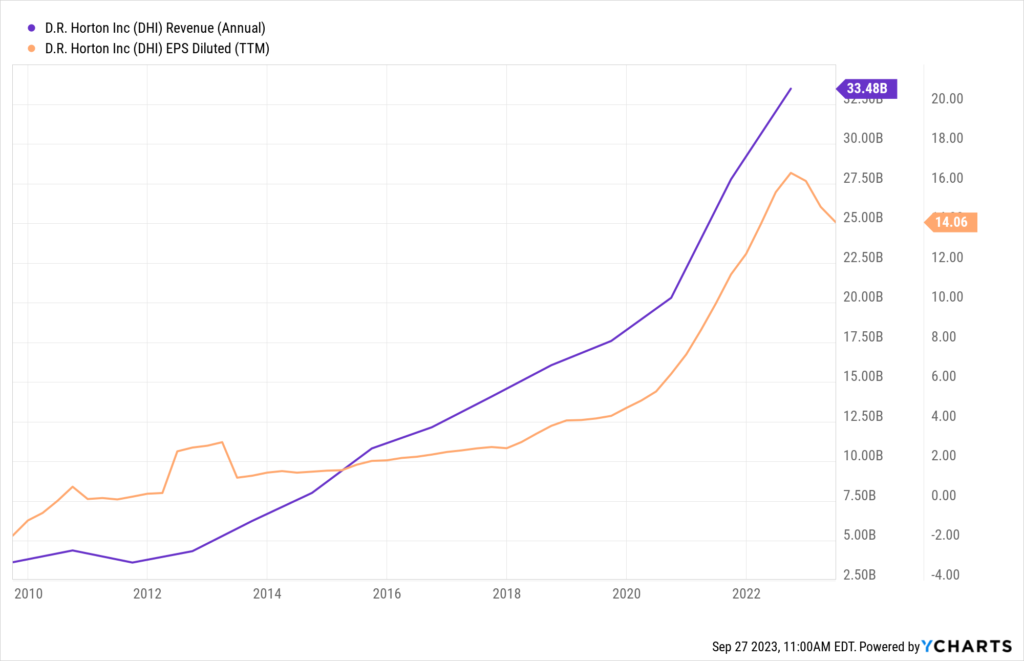

My first dividend growth stock for October 2023 is D.R. Horton (DHI). D.R. Horton is an American home construction company.

This used to be a really tough industry to invest in. It was viewed as a capital-intensive business model susceptible to the boom-and-bust cycles of US housing demand. So what’s changed? Well, a lack of supply. That’s what. After the GFC fallout in 2009, supply has not been brought to market in the same way it used to. The US is chronically short on the housing supply it needs to meet market demand.

This imbalance between supply and demand is a structural problem that will likely be a multiyear tailwind for D.R. Horton – the “800-pound gorilla” of the industry. Already, over the past decade, this business has put up amazing growth. We’re talking about a 20.4% CAGR in revenue and 32.3% CAGR in EPS over that stretch. That rapid business growth has supported rapid dividend growth.

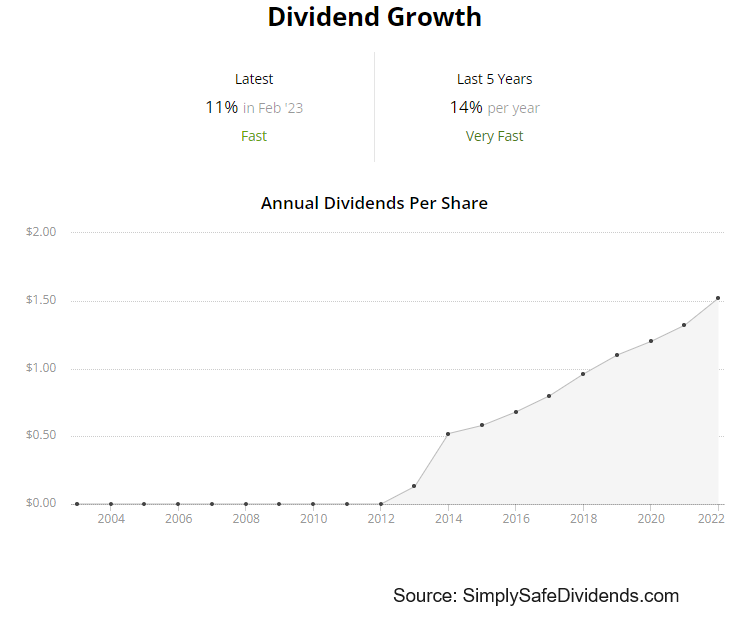

D.R. Horton has increased its dividend for nine consecutive years. The track record is a bit short, if only because of the aforementioned problems coming out of the GFC. But with a five-year DGR of 16.8%, D.R. Horton is making up for lost time. The stock only yields 0.9%, so it really is more of a high-quality compounder. However, this dividend is supported by an extremely low payout ratio of only 7.1%. Plenty of leeway for large dividend increases well into the years ahead.

D.R. Horton has increased its dividend for nine consecutive years. The track record is a bit short, if only because of the aforementioned problems coming out of the GFC. But with a five-year DGR of 16.8%, D.R. Horton is making up for lost time. The stock only yields 0.9%, so it really is more of a high-quality compounder. However, this dividend is supported by an extremely low payout ratio of only 7.1%. Plenty of leeway for large dividend increases well into the years ahead.

This could be your opportunity to invest alongside the legendary Warren Buffett. That’s right. Buffett’s conglomerate, Berkshire Hathaway, recently invested in D.R. Horton. In the past, I would have questioned the move. However, after looking at how much change has occurred here in terms of industry dynamics, I think it’s a great move, assuming it’s a long-term investment.

I already put together my end of a full analysis and valuation video on D.R. Horton. Just have to get it edited. In that video, the fair value estimate for the business came out to just over $124/share. The stock’s current pricing of about $109 looks favorable. Take a look.

My second dividend growth stock for October 2023 is Intercontinental Exchange (ICE). Intercontinental Exchange is an operator of global financial exchanges and clearing houses, and also provides data services.

We’re all investors, right? That makes us very familiar with this company’s crown jewel, the New York Stock Exchange – the largest stock exchange in the world. If you want to buy any stock that is listed on the NYSE – which encompasses thousands – you have to go through this company.

If a miniature monopoly wasn’t good enough, Intercontinental Exchange has also bolted high-margin data and technology services on top of it all. That’s why revenue has compounded at an annual rate of 18.4% over the last decade, while EPS has a CAGR of 26.5% over that period. Why not get paid back – through growing dividends – from some of your own investing activity?

Whenever someone deals with this company and earns Intercontinental Exchange money, that goes toward the cash flow that eventually helps to fund the dividend. If you’re interacting with the NYSE anyway, why not participate in some of that action yourself? This company has increased its dividend for 11 consecutive years, with a five-year DGR of 13.7%.

Whenever someone deals with this company and earns Intercontinental Exchange money, that goes toward the cash flow that eventually helps to fund the dividend. If you’re interacting with the NYSE anyway, why not participate in some of that action yourself? This company has increased its dividend for 11 consecutive years, with a five-year DGR of 13.7%.

You also get a 1.5% yield to go along with that double-digit dividend growth. And the payout ratio of 31.1%, based on TTM adjusted EPS, gives the company plenty of room for future dividend growth. It’s not super cheap, but this is a terrific business.

Every time I’ve chased cheapness over quality, I’ve been burned. This is the opposite of that. It’s a high-quality business, albeit not a super cheap one. That said, I do think we have some mild undervaluation present, and that might be just the window of opportunity one needs in order to make a successful long-term investment.

We’ll have a full analysis and valuation video coming out soon on the business, if it’s not live already. But I can tell you that every basic valuation metric here is below its respective recent historical average. For example, based on TTM adjusted EPS, the P/E ratio is 20.4. Its own five-year average is 25.5. This is the kind of business that one invests in with the intention to hold for decades.

My third dividend growth stock for October 2023 is NextEra Energy (NEE). NextEra Energy is an American energy company.

This is a premier energy company. In fact, I’d argue that it’s the very best utility business in all of America. If one wanted to build the best possible utility business from scratch, it’d probably look a lot like NextEra Energy. On one hand, NextEra Energy’s Florida Power & Light unit provides electricity to over 12 million people across the state of Florida – one of the fastest-growing states in the US, and a state with a favorable regulatory structure.

On the other hand, the company’s NextEra Energy Resources unit is the world’s largest generator of renewable energy from the wind and sun, and it’s also a world leader in battery storage. Powerful one-two punch here. And it’s why revenue has a CAGR of 3.7% over the last decade, while EPS has a CAGR of 11.2%. This is a one of only three utilities that is a Dividend Aristocrat.

Despite what some investors may think, it’s actually rare for a utility to become a Dividend Aristocrat. Utilities usually feature a lot of debt and dilution. Unfortunately, dividend cuts are not uncommon across the utility space. But NextEra Energy bucks the trend. The company has increased its dividend for 29 consecutive years. Another way in which NextEra Energy bucks the trend is with dividend growth.

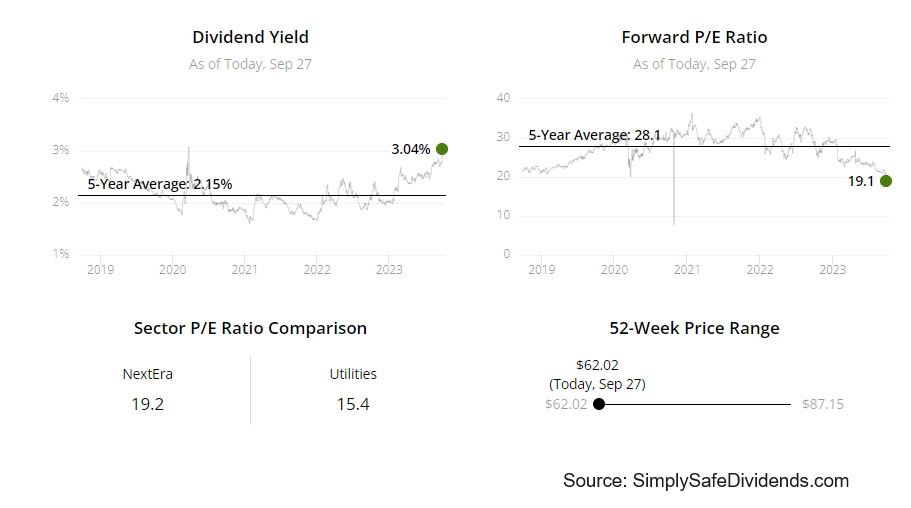

Its 10-year DGR is 11%, which is a growth rate that is almost unheard of for a utility business. Now, the stock’s yield of 2.8% isn’t super high for this space, but I think the growth more than makes up for it. And the 60.9% payout ratio, based on midpoint guidance for this year’s adjusted EPS, is lower than what I see across many competitors.

This stock’s recent correction could be a great chance to buy a Dividend Aristocrat on sale. The stock is down more than 20% from its recent high, despite the business chugging along normally. Of course, rising interest rates have hit utility stocks hard. Higher rates make new debt more expensive. And there are more options out there for income-oriented investors.

This stock’s recent correction could be a great chance to buy a Dividend Aristocrat on sale. The stock is down more than 20% from its recent high, despite the business chugging along normally. Of course, rising interest rates have hit utility stocks hard. Higher rates make new debt more expensive. And there are more options out there for income-oriented investors.

Nonetheless, this is a great business that is poised to do very well in total return terms over the long term. Our recent analysis and valuation of the business estimated fair value at $81.47/share, and the video on that should be live soon. Against that valuation, the stock’s pricing of about $67.50 looks quite interesting.

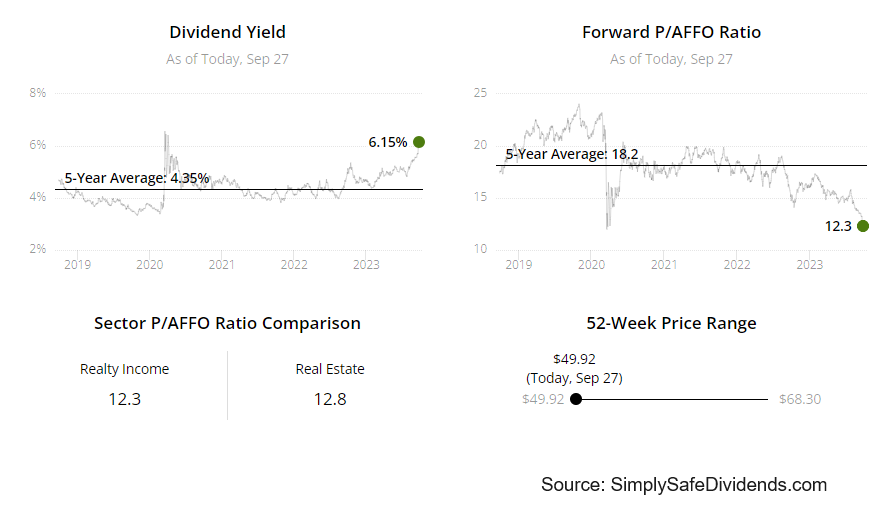

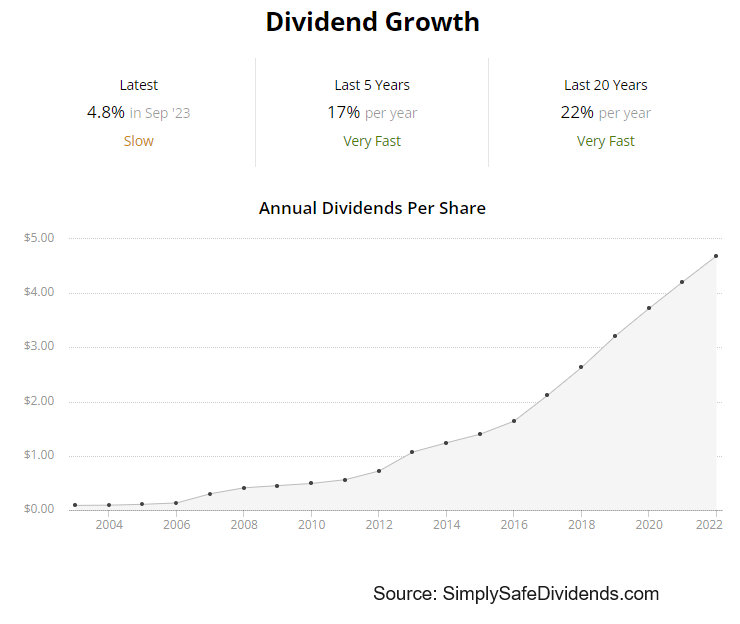

My fourth dividend growth stock for October 2023 is Realty Income (O). Realty Income is is a real estate investment trust.

Realty Income is a REIT behemoth that leases freestanding, single tenant, triple-net-leased retail properties. Here are some amazing stats for you. The property portfolio is comprised of over 13,000 properties and is diversified across the US, Puerto Rico, Spain, Italy, and the UK. The company serves more than 1,300 clients operating across 85 different industries. The occupancy rate is 99%, because these properties are often “mission critical” for tenants.

Realty Income has been about as consistent as it gets, even if the growth won’t necessarily “wow” you. The company’s 17.4% CAGR in revenue over the last decade is somewhat misleading due to the way in which a REIT functions, but its 5.9% CAGR in FFO/share is a pretty accurate reflection of the growth. And that’s not bad at all. Also not bad? The company’s impressive dividend growth track record.

We’ve got yet another Dividend Aristocrat on our hands. Realty Income has increased its dividend for 30 consecutive years. Real estate is a tough business. It’s a bit of a meat grinder. But Realty Income has been successfully navigating real estate for decades. Good stuff.

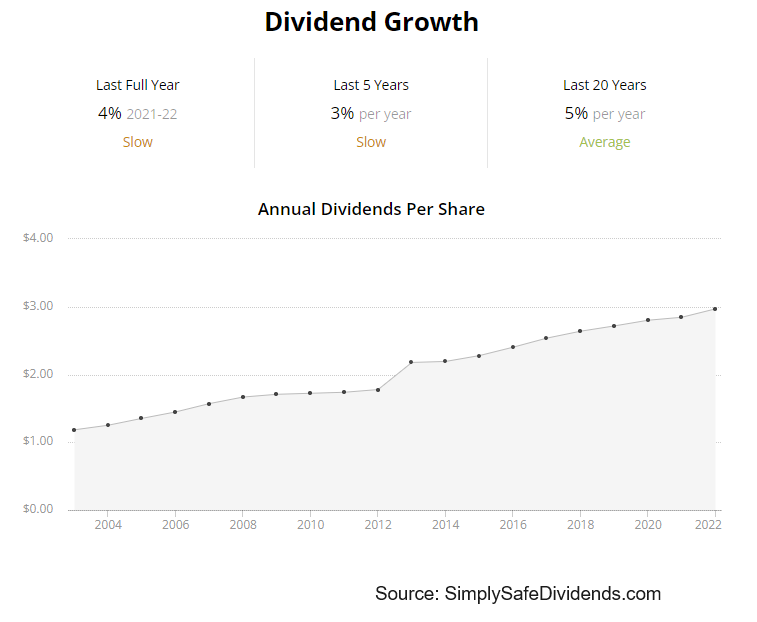

The 10-year DGR of 5.3% lines up pretty well with bottom-line growth. Again, not huge growth. However, the stock yields 6%. One doesn’t need lights-out growth with a 6% yield. By the way, this big dividend? It’s paid monthly. How about that? The 76.9% payout ratio, based on AFFO/share guidance for the year, is slightly elevated, but it’s not at all unusual for a REIT.

The 10-year DGR of 5.3% lines up pretty well with bottom-line growth. Again, not huge growth. However, the stock yields 6%. One doesn’t need lights-out growth with a 6% yield. By the way, this big dividend? It’s paid monthly. How about that? The 76.9% payout ratio, based on AFFO/share guidance for the year, is slightly elevated, but it’s not at all unusual for a REIT.

This stock has performed miserably this year, but that’s exactly where the opportunity might be.

Indeed, this stock is down 20% in 2023. Meanwhile, the S&P 500 is up nearly 20% on the year. That is a massive amount of relative underperformance, and it’s rare to see that kind of delta for Realty Income. But rates are on the rise. Questions around commercial real estate are swirling. And investors are skittish. However, the fundamentals of the business appear to be as solid as ever.

Again, it’s not a high-growth investment. But it is a Dividend Aristocrat offering a large, safe, monthly dividend that is growing at a good clip. And I also think there’s some undervaluation present. Our recent analysis and valuation piece on Realty Income came up with a final valuation of $66.78/share, and that video should be live soon. The stock is priced at about $51 as I write this, which, outside of the pandemic, is the lowest price on this stock in five years. Realty Income is worth a good look right now.

Again, it’s not a high-growth investment. But it is a Dividend Aristocrat offering a large, safe, monthly dividend that is growing at a good clip. And I also think there’s some undervaluation present. Our recent analysis and valuation piece on Realty Income came up with a final valuation of $66.78/share, and that video should be live soon. The stock is priced at about $51 as I write this, which, outside of the pandemic, is the lowest price on this stock in five years. Realty Income is worth a good look right now.

My fifth dividend growth stock for October 2023 is Texas Instruments (TXN). Texas Instruments is an American technology company.

Texas Instruments mostly focuses on analog semiconductors, which measure real-world information like temperature and process that information into signals for electronics. From top to bottom, this is a high-quality company. High returns on capital. Fat margins. Stellar balance sheet. Almost nothing to dislike. Growth is also solid. Texas Instruments has compounded its revenue at an annual rate of 5.7% and its EPS at an annual rate of 19.4% over the last decade. Awesome.

Also awesome is this company’s track record of dividend growth. Texas Instruments has increased its dividend for 20 consecutive years in a row, with the most recent dividend raise coming in only days ago. The five-year DGR is 17.2%, but dividend growth for the near term will be muted because of the company’s heavy CapEx cycle as it invests in capacity. Still, the stock’s 3.2% yield pays you to wait. And a payout ratio of 61.5% ensures the safety of the dividend while the cycle plays out. A bit of recent underperformance here. But this stock outperforms over the long run.

The stock is down just slightly this year. About 1%. But in a year in which the S&P 500 is up nearly 20%, that’s a lot of underperformance. However, this is a long-term compounder of the highest quality, and the stock’s 10-year CAGR of 18% tells the better and more accurate story. As we zoom back into today, the stock’s P/E ratio of 19.3 is decently off of its own five-year average of 22.6.

The stock is down just slightly this year. About 1%. But in a year in which the S&P 500 is up nearly 20%, that’s a lot of underperformance. However, this is a long-term compounder of the highest quality, and the stock’s 10-year CAGR of 18% tells the better and more accurate story. As we zoom back into today, the stock’s P/E ratio of 19.3 is decently off of its own five-year average of 22.6.

The sales multiple of 7.9 is similarly off of its own five-year average of 8.6. Even great businesses like Texas Instruments can see their stocks massively underperform over short periods of time. However, those short-term price-to-value disconnects are where future fortunes are built, because that long-term outperformance starts to build up again as the coiled spring uncoils.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income