There are long-term, large-scale changes that are shaping the world around us. I’m talking about global megatrends.

As you might imagine, wherever there’s change on this kind of scale, there’s money to be made. Better yet, there are also dividends to be made.

Growing dividends.

Indeed, there are many publicly-traded, world-class businesses that are benefiting from global megatrends. These same businesses produce ever-rising sales and profits… and pay ever-rising dividends. If you’re a long-term dividend growth investor, this should be music to your ears. It could mean safe, growing dividends for decades as these businesses ride the waves of global megatrends.

Today, I want to tell you about 3 global megatrends and which high-quality dividend growth stocks could benefit the most.

Ready? Let’s dig in.

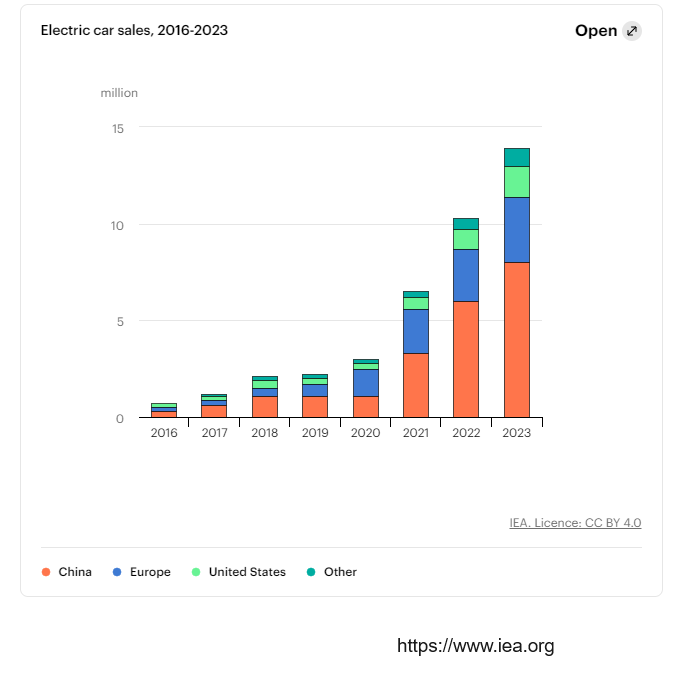

The fist global megatrend we should discuss is the rise of electric vehicles – EVs. Demand for EVs is exploding.

Per the International Energy Agency, the share of electric cars in total sales has more than tripled in only three years, from around 4% in 2020 to 14% in 2022. That is exponential growth. And it’s just getting started. It is highly likely that in 20 years from now, EVs will make up more than half of all global auto sales.

There are many ways to play this global megatrend, but one way comes to mind immediately. Lithium. That’s right. Lithium.

There are many ways to play this global megatrend, but one way comes to mind immediately. Lithium. That’s right. Lithium.

After all, what will all of these EVs need? Batteries, of course. And those batteries require lithium. Imagine being able to invest in oil & gas companies at the dawn of the automobile. We could be in a similar situation right now, in 2023, with companies that provide lithium. The good news is that you don’t need to invest in some speculative miner out in the middle of nowhere. No, there is a large US-based company that is a major lithium producer. That company is Albemarle Corporation – stock ticker ALB.

Albemarle is a specialty chemicals manufacturing company. What’s so great and unique about Albemarle is that this is a company with a long, established history as a successful, diversified business that went out and bolted a huge lithium operation on top of the business back when lithium demand was still in its infancy.

Albemarle’s corporate roots date back to 1887, so this is no unproven, new player here. With more than a century under its belt as a chemicals company, Albemarle’s management made the prescient decision to strategically invest in lithium through the 2015 acquisition of Rockwood Holdings – a rival that had already built up a successful lithium business.

Albemarle is now the top lithium producer in the world. That’s both by market cap and production volumes. However, with a market cap of only $22 billion, Albemarle is still small enough to potentially be a multi-bagger over the next few years. Even if it were to become a ten-bagger, it would still be a relatively small company in terms of global market caps. But wait. There’s more.

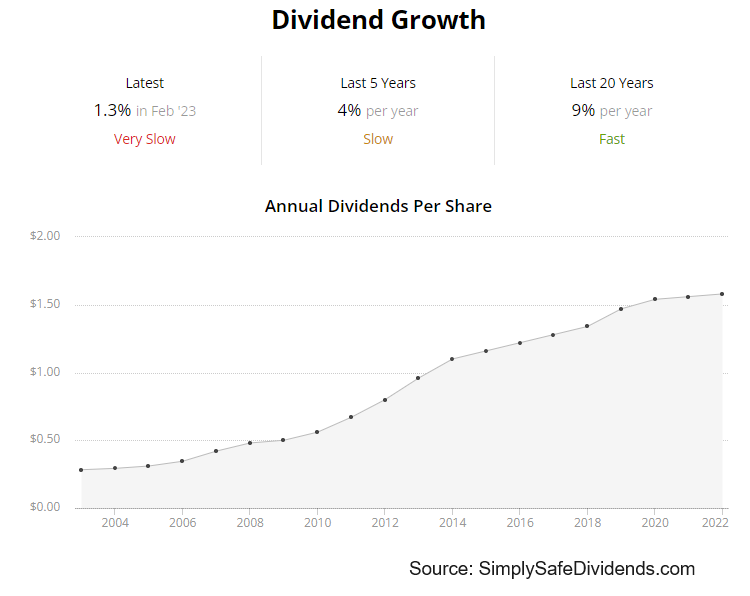

Albemarle is a Dividend Aristocrat. This is a possible multi-bagger at the forefront of a global megatrend that is also a Dividend Aristocrat with 29 consecutive years of dividend increases. You have gotta love that combination of dividend commitment and growth potential. The 10-year DGR is 7.3%, which is solid. But the yield of only 0.9% does leave something to be desired, although the yield is low because the demand for the shares is high.

Albemarle is a Dividend Aristocrat. This is a possible multi-bagger at the forefront of a global megatrend that is also a Dividend Aristocrat with 29 consecutive years of dividend increases. You have gotta love that combination of dividend commitment and growth potential. The 10-year DGR is 7.3%, which is solid. But the yield of only 0.9% does leave something to be desired, although the yield is low because the demand for the shares is high.

The payout ratio is below 6%, so the dividend is very secure. And, based on midpoint guidance for this year’s EPS, the forward P/E ratio is only 6.7. Lithium pricing will be volatile, so expect volatile multiples and stock pricing. But if you’re in it for the long term, that’s mostly just noise. Take a close look at Albemarle.

The second global megatrend I want to discuss today is the buildout of infrastructure. The world is building out infrastructure at an incredible pace.

Not to be outdone by China’s Belt and Road Initiative, a global infrastructure development strategy adopted by the Chinese government in 2013 to invest in over 100 different countries, the US, Saudi Arabia, India, and the EU announced at the recent G20 summit a multinational rail and ports deal linking the Middle East and South Asia. That comes on the back of the 2021 Infrastructure Investment and Jobs Act – a $1.2 trillion spending package that will see massive spending on all kinds of infrastructure projects.

What will all of this infrastructure require? Machinery. That’s right. You can’t put water pipes underground or build new roads without heavy machinery. An obvious way to invest in the wave of spending is to own a slice of a global business that will provide the machines necessary for the worldwide buildout of infrastructure. Which business is that? Caterpillar Inc. (CAT).

Caterpillar is a construction, mining, and engineering equipment manufacturer. With a market cap of $144 billion, Caterpillar is the world’s largest manufacturer of construction equipment. And what will infrastructure require? Construction, of course, which leads you right to the machines that Caterpillar makes.

Although Caterpillar isn’t the only company making these machines, it’s arguably the best. It’s undoubtedly the biggest. And when you want quality machinery that will get the job done right, Caterpillar is going to come to mind immediately. You know what else comes to mind immediately about Caterpillar? Its stellar dividend growth track record. Caterpillar is another Dividend Aristocrat.

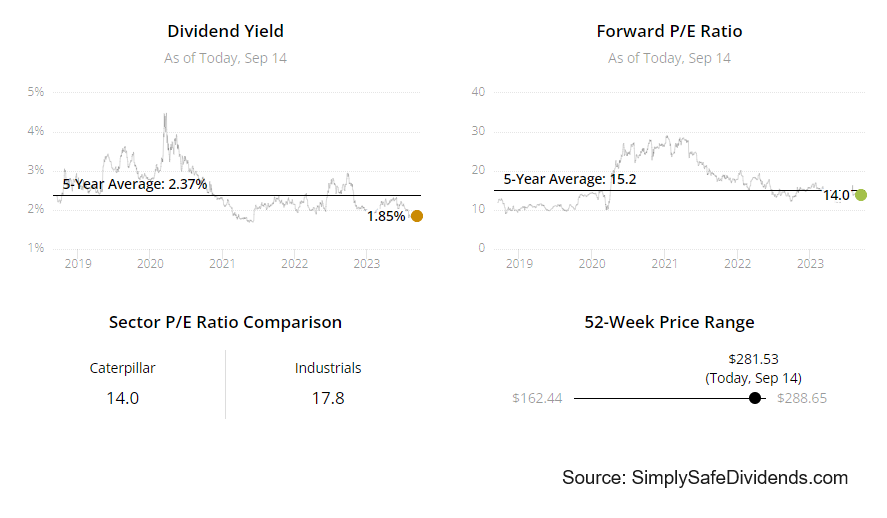

It requires at least 25 consecutive years of dividend increases to become a Dividend Aristocrat, so a company has to demonstrate relentless consistency with paying a growing dividend in order to reach this status. Caterpillar has increased its dividend for 30 consecutive years already. And you know what? The next 30 years could be even better and more successful for Caterpillar than the last 30 years, as evidenced by the spending that’s flowing into infrastructure. The 10-year DGR is 9%, which is something that Caterpillar has been very steady with. And the stock also yields a handsome, market-beating 1.8%. A payout ratio of 32.4% comfortably covers the dividend.

The world will be spending a lot of money on infrastructure. Why not get a piece of that action yourself? Caterpillar is clearly poised to benefit from the massive amount of spending that will be used to build up new infrastructure and replace aging infrastructure – both of which have been delayed for years in a number of developed countries, including the US. A P/E ratio of 17.6 isn’t egregious for a business of this quality and positioning, in my view.

The world will be spending a lot of money on infrastructure. Why not get a piece of that action yourself? Caterpillar is clearly poised to benefit from the massive amount of spending that will be used to build up new infrastructure and replace aging infrastructure – both of which have been delayed for years in a number of developed countries, including the US. A P/E ratio of 17.6 isn’t egregious for a business of this quality and positioning, in my view.

Its own five-year average P/E ratio is 19.4. On the other hand, the P/S ratio of 2.3 is running ahead of its own five-year average of 1.9. This stock has gone on a run of late – up nearly 50% over the last year alone – but any sizable pullback might be just the opportunity a long-term dividend growth investor is looking for in order to invest in a world-class business that will see a large chunk of the spending on a global megatrend come its way.

The third global megatrend I have to bring up is AI. Artificial intelligence has the promise to revolutionize the way in which we live and work.

I’m usually quite wary of the new thing, especially when there’s a lot of hype attached to it. And AI has no shortage of hype. However, I do think that AI has the potential to dramatically change our world. It could be transformational. The use cases are endless. Every single industry in the world could be impacted by it, much in the same way the Internet impacted everything. But we can’t make money on promise. We make money on results.

In my opinion, you have to invest in the companies that can clearly make money on AI right now. That means investing in established, successful businesses that are already making a lot of money and then bolting AI opportunities on top of it.

It’s taking something great and, potentially, making it even better. This means not going after some flashy IPO. It means not investing in some no-profit company that brings up AI in earnings calls. There has to be a clear strategy with obvious integration and synergies. I’ll give you a great example.

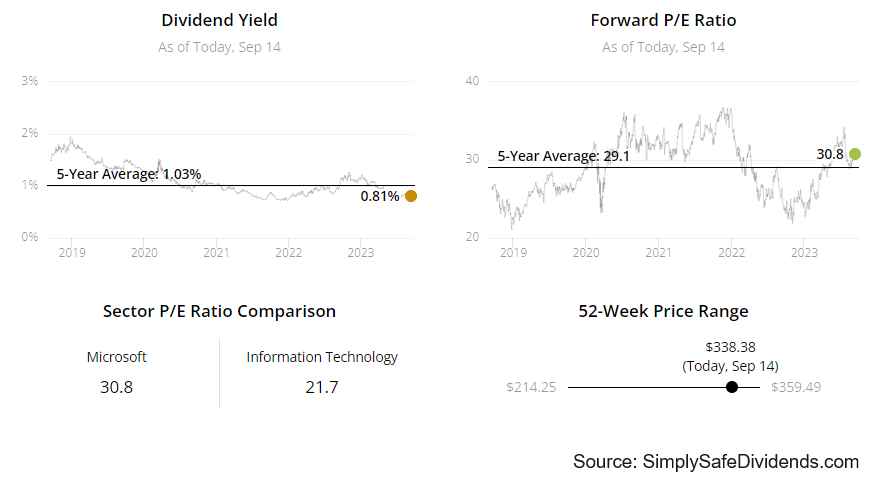

Microsoft Corp. (MSFT). Microsoft is a multinational technology corporation.

Could a play on AI get any more obvious than this? I don’t think so. Microsoft is an early investor in cutting-edge AI, via its $13 billion investment in ChatGPT-maker and AI innovator OpenAI. So what do we have here? Microsoft is already a leading technology company. With its $2.5 trillion market cap, it’s one of the largest companies in the world. It’s a software pioneer. It has video gaming. It’s a major cloud computing provider.

We have an extremely successful, all-encompassing technology company that is firmly established with real revenue generators, and it’s now bolting real AI on top of it all – AI that can easily be fit into its current suite of products and services. That’s a recipe for success, in my view. And it’s a recipe for continued business and dividend growth.

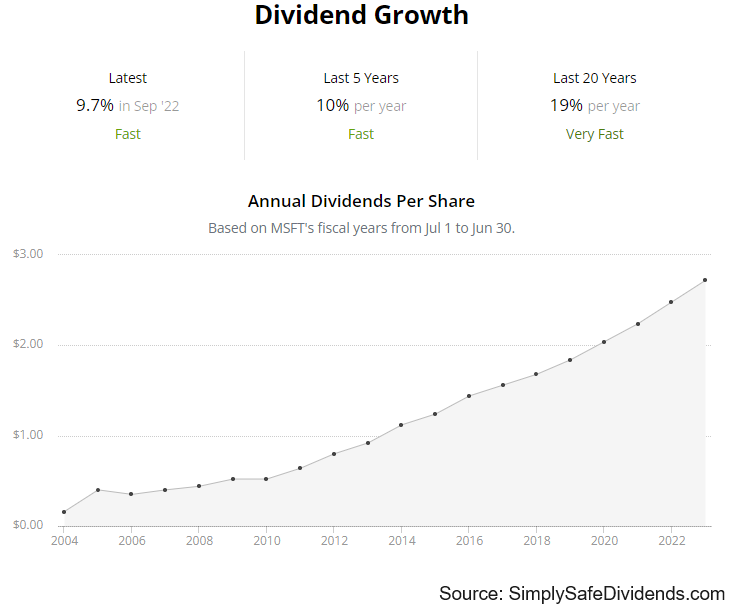

Microsoft is no stranger to either one. Regarding the dividend, Microsoft has increased its dividend for 21 consecutive years. The 10-year DGR is 11.8%, and that’s without any juice from AI. Microsoft is already a dividend growth stalwart, before even talking about this global megatrend being added to the mix. That’s incredible.

Now, the stock’s yield of 0.8% won’t entice income investors who overly focus on yield. But Microsoft is a high-quality compounder that compounds wealth and the dividend very nicely over the long run. So if you’re not only worried about income today, and you instead think about the many tomorrows to come, Microsoft has been, and will likely remain, a great long-term dividend growth investment. A payout ratio of only 28.1% ensures that there is a lot more dividend growth to come.

Now, the stock’s yield of 0.8% won’t entice income investors who overly focus on yield. But Microsoft is a high-quality compounder that compounds wealth and the dividend very nicely over the long run. So if you’re not only worried about income today, and you instead think about the many tomorrows to come, Microsoft has been, and will likely remain, a great long-term dividend growth investment. A payout ratio of only 28.1% ensures that there is a lot more dividend growth to come.

Microsoft is a long-term winner, and the winning with AI could be just getting started. The company’s stock has compounded at an annual rate of 28.5% over the last decade, which has been largely supported by an EPS CAGR of 16%. And that’s mostly before AI entered the picture. Even if AI is a total dud, which I think is highly unlikely, Microsoft is still an amazing business. Just imagine what Microsoft could do if AI lives up to its promise?

The sky’s the limit. The stock’s not cheap, nor should it be. Hasn’t been cheap for most of my existence as an investor. In fact, I kept hearing about how expensive it was last year, before it went on another 40%+ run. With a P/E ratio of 34.9, I don’t think it’s egregious for a world-beater that is just now dipping its toes into a new global megatrend. If you want to play AI with a proven winner, Microsoft comes to mind immediately.

The sky’s the limit. The stock’s not cheap, nor should it be. Hasn’t been cheap for most of my existence as an investor. In fact, I kept hearing about how expensive it was last year, before it went on another 40%+ run. With a P/E ratio of 34.9, I don’t think it’s egregious for a world-beater that is just now dipping its toes into a new global megatrend. If you want to play AI with a proven winner, Microsoft comes to mind immediately.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income