US stocks are some of the best and most sought-after assets in the whole world. But within that broader universe, there’s a subset of stocks that is particularly compelling.

I’m talking about high-quality dividend growth stocks. These stocks represent equity in world-class businesses selling the products and/or services the world demands more and more of. These businesses are so adept at producing gobs of growing cash flow, they’re left with a lot of money they can’t effectively use.

Well, they end up returning some of that back to shareholders, via growing dividend payments. And those growing dividend payments can be a fantastic source of passive income… which one can even live off of.

It’s easy to see why high-quality dividend growth stocks are compelling. But when they’re on sale – when they’re undervalued – that’s when the appeal is off the charts. Price and yield are inversely correlated. All else equal, lower prices result in higher yields.

This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach. Now, lower valuations often come when there’s volatility. But I always see short-term volatility as a long-term opportunity.

That perspective helped me to go from below broke at age 27 to financially free at 33. By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

With all of that out of the way, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what this article is all about. Today, I want to tell you my top 5 dividend growth stocks for September 2023.

Ready? Let’s dig in.

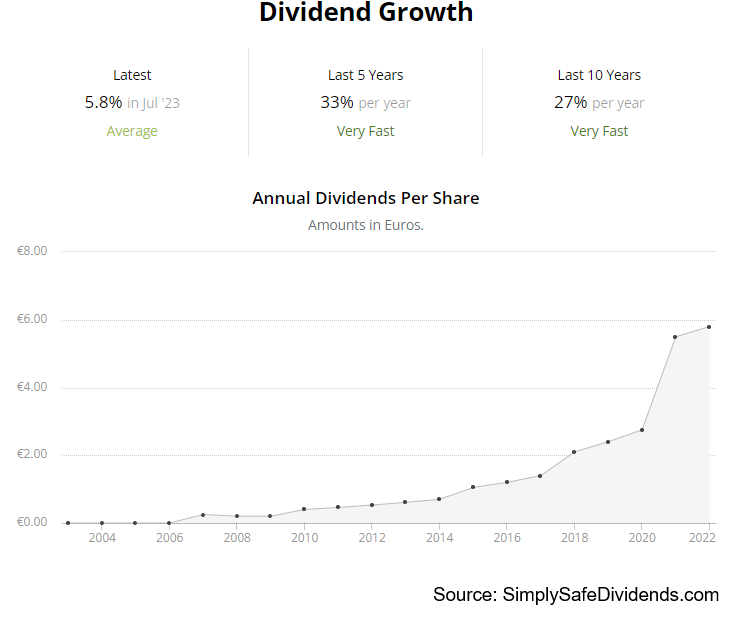

My first dividend growth stock for September 2023 is ASML Holding (ASML). ASML develops, produces, markets, sells, and services advanced semiconductor equipment systems.

It’s almost impossible to imagine a future in which we’re using less semiconductors, right? Everyday life in modern-day society is increasingly becoming dependent on advanced semiconductors, which are powering almost everything we use – electronics, cars, TVs, even light bulbs.

Well, those advanced semiconductors don’t just get magically dreamed up. They have to be manufactured. And in order to manufacture them, which is an incredibly complex process, you need certain specialized machines. Specialized machines like those that ASML – and ASML alone – makes. Monopolistic economics explain why ASML has put up a 16.9% CAGR in revenue and 22.1% CAGR in EPS over the last decade. This is one of the fastest-growing dividends in the world.

ASML has increased its dividend for 13 consecutive years, in its native currency. Between FY 2019 and FY 2022, the dividend more than doubled. We’re talking about a 34.2% CAGR in the dividend, which is obviously just fantastic. Despite that high growth rate, the payout ratio is still fairly moderate, at only 41%.

That’s because the business is growing at such a high rate, limiting the expansion of the payout ratio. Now, you’re not going to get a fat yield from a high-quality compounder like this. The stock yields only 1%. But if you’re really in it for the long term, that dividend growth will add up and allow for meaningful income over time from an ASML investment that’s made today. The potential undervaluation here is also meaningful.

That’s because the business is growing at such a high rate, limiting the expansion of the payout ratio. Now, you’re not going to get a fat yield from a high-quality compounder like this. The stock yields only 1%. But if you’re really in it for the long term, that dividend growth will add up and allow for meaningful income over time from an ASML investment that’s made today. The potential undervaluation here is also meaningful.

Is the stock a steal at current prices? No. I don’t believe so. But this is one of the best businesses I’ve ever seen. Why would a terrific business be in the bargain bin? That wouldn’t make any sense. Instead, I think we have what appears to be noticeable undervaluation on a wonderful business.

I already put together a full analysis and valuation report on ASML, and the video should be live soon, if it’s not already, and the fair value estimate on this business worked out to just over $791/share. The stock is currently priced at about $650. Great business. Pretty good valuation. Take a look.

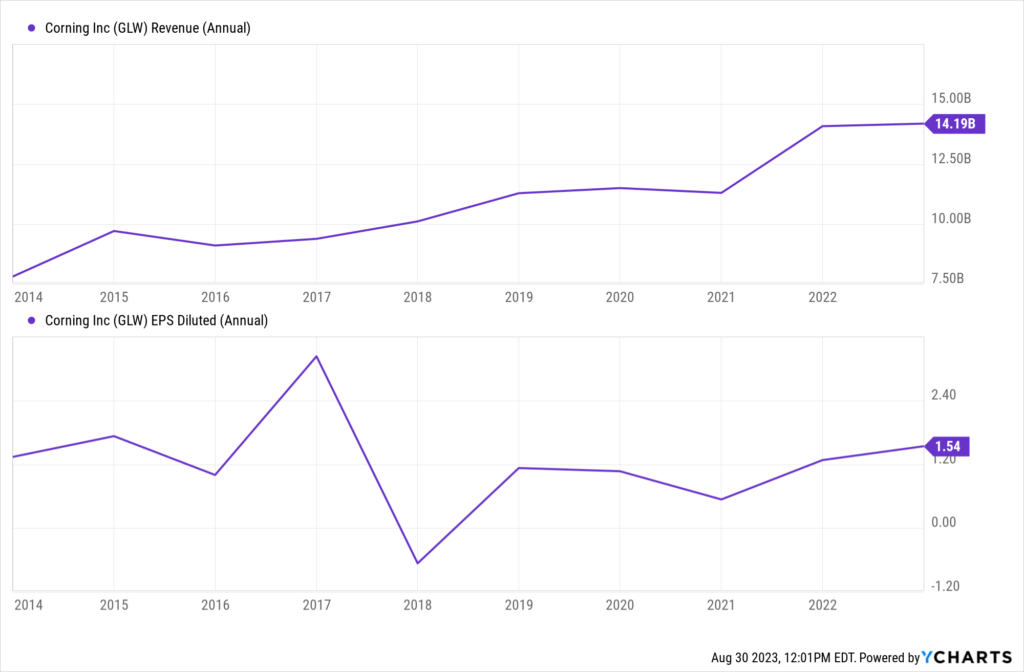

My second dividend growth stock for September 2023 is Corning (GLW). Corning is a multinational materials science company.

Corning manufactures specialty glass, ceramics, optical fiber, and related materials. An essential player in making various technologies work. We can go down the list: optical fiber for internet access, glass for smartphones, or specialty materials for advanced R&D processes. In fact, there’s a pretty decent chance that the glass you’re interfacing with right now (in order to read this article) was manufactured by Corning. This company flies under the radar. Despite that, it’s still putting up very respectable growth – a 6.9% CAGR in revenue and 5.1% CAGR in EPS over the last decade. Also respectable is the dividend growth story.

Corning has increased its dividend for 13 consecutive years. The 10-year DGR is 13.1%. Good stuff. Well in excess of inflation, even today’s level of inflation. Along with that double-digit dividend growth, the stock yields a rather juicy 3.5%. So you don’t really have to sacrifice yield nor dividend growth here, which is nice. The only thing to be wary of, perhaps, is the elevated payout ratio, which is 60.1%, based on TTM adjusted EPS. Corning doesn’t necessarily wow me. But it’s a good business. And the valuation strikes me as reasonable.

Corning has increased its dividend for 13 consecutive years. The 10-year DGR is 13.1%. Good stuff. Well in excess of inflation, even today’s level of inflation. Along with that double-digit dividend growth, the stock yields a rather juicy 3.5%. So you don’t really have to sacrifice yield nor dividend growth here, which is nice. The only thing to be wary of, perhaps, is the elevated payout ratio, which is 60.1%, based on TTM adjusted EPS. Corning doesn’t necessarily wow me. But it’s a good business. And the valuation strikes me as reasonable.

Again, Corning flies under the radar. So I’m not surprised that it’s not some high-flying stock that has a big premium attached to it. Instead, this stock just kind of steadily plods along, just like the business. And that’s okay for a lot of investors.

You get a good-sized dividend that’s growing at a strong clip, and it’s coming from a company that’s been around since 1851. A lot to like about something like that. We recently published a full analysis and valuation video on Corning, with the intrinsic value estimate shaking out to almost $40/share. The stock’s pricing is sitting at under the $33 mark. Very decent upside potential while you collect a 3.5% yield.

My third dividend growth stock for September 2023 is Fifth Third Bancorp (FITB). Fifth Third is is a diversified regional bank holding company.

So I must be honest here. I’m not as sanguine on banks as I used to be. The entire business model just isn’t as good as it once was. Banks have been handicapped by heavy regulations. Competition is thick. When not whipsawing, interest rates are low. And growth has been hard to come by for many years now.

That said, banks like Fifth Third have saw what was coming and have turned themselves into diversified financial operations that have exposure to a range of steady, fee-based businesses. That’s helped to breathe new life into something that, in some ways, is arguably dying. This helped Fifth Third to put up a 3.3% CAGR in revenue and 5.8% CAGR in EPS over the last ten years – a really tough decade for banks. This prescient diversification has also helped to keep the dividend growing.

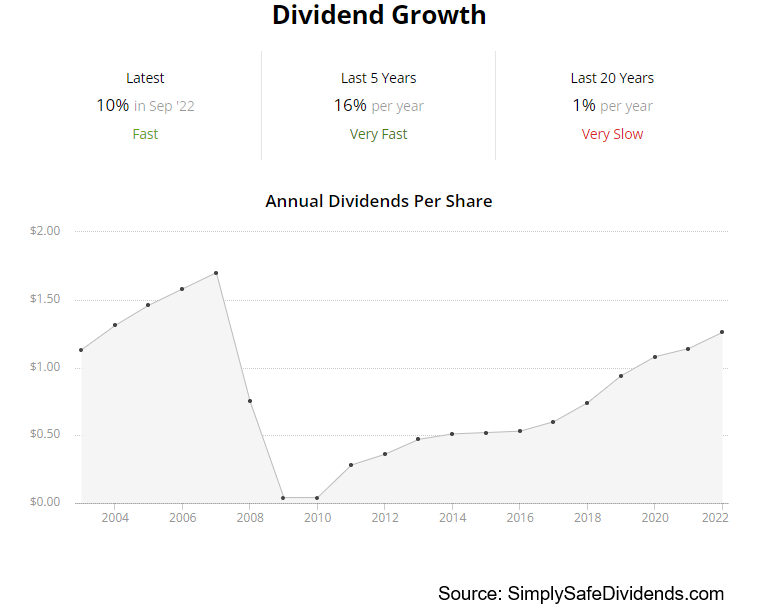

Indeed, Fifth Third has increased its dividend for 12 consecutive years, with a 10-year DGR of 13.1%. Not too bad for a business that isn’t as good as it used to be. Just imagine what Fifth Third could do if banking were the great institution it once was! Ordinarily, you wouldn’t get a high yield with a dividend growth rate at this level.

However, bank stocks have had a miserable 2023 – many falling significantly after certain idiosyncratic bank failures caused panic to spread over the sector like wildfire. Since price and yield are inversely correlated, lower prices have caused yields to rise. In this case, Fifth Third’s stock now yields a monstrous 5.2%. That’s in territory typically reserved for yield plays, like REITs. And in spite of the hysteria, the payout ratio of 37.7% indicates no issues whatsoever with the sustainability of the dividend. This one is in the bargain bin.

However, bank stocks have had a miserable 2023 – many falling significantly after certain idiosyncratic bank failures caused panic to spread over the sector like wildfire. Since price and yield are inversely correlated, lower prices have caused yields to rise. In this case, Fifth Third’s stock now yields a monstrous 5.2%. That’s in territory typically reserved for yield plays, like REITs. And in spite of the hysteria, the payout ratio of 37.7% indicates no issues whatsoever with the sustainability of the dividend. This one is in the bargain bin.

The stock is down more than 20% YTD. And that’s with the S&P 500 up 15% YTD. That is awful performance. Like I said, it’s been a miserable year for many bank stocks. Has it been overdone? Sure looks like it. The valuation is at multiyear lows, pushing the P/E ratio down to almost 7.

I’m not a huge fan of banks. But the market disdain is unwarranted, in my view. The content for an upcoming analysis and valuation video on Fifth Third has already been put together, and that just has to be edited. But the estimate for fair value on this bank came out to $36.33/share. The stock is currently priced at just over $25. For bargain hunters, this has gotta be interesting right here.

My fourth dividend growth stock for September 2023 is Lockheed Martin (LMT). Lockheed Martin is the world’s largest defense contractor.

Do I wish the world had no conflict? No violence? No war? Of course. Who wouldn’t wish for such a thing? But we have to live in, and invest in, the world we have, not the one we want. In this reality, human conflict has been around since… well, humans. And it’ll likely be the way for as long as our species exists.

Lockheed Martin produces the sovereign defense tools that nations need to, hopefully, prevent conflict before it starts. And if conflict does start, those same tools will come in handy. By the way, those tools? Not just necessary but expensive. And increasingly so. So it’s progressive pricing on top of built-in demand. That’s why Lockheed Martin has compounded its revenue at an annual rate of 4.2% and its EPS at an annual rate of 10.1% over the last 10 years. Double-digit EPS growth. Double-digit dividend growth.

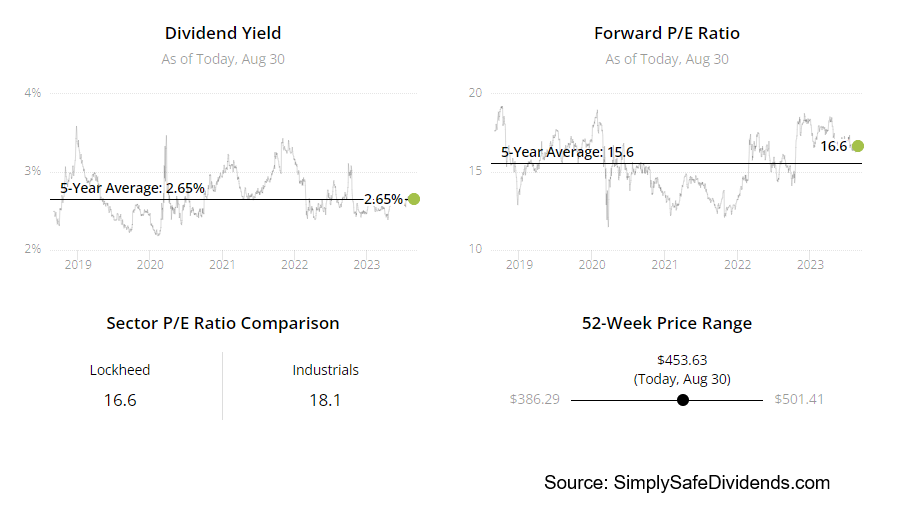

The dividend, which has been increased for 19 consecutive years, has a 10-year DGR of 10.6%. You can see how cleanly dividend growth lines up with EPS growth. Great control from management. And kicking the passive income train off is the stock’s market-beating yield of 2.7%. With a moderate payout ratio of 44%, this train should keep moving for years to come. Great business. Great dividend. Great valuation.

The dividend, which has been increased for 19 consecutive years, has a 10-year DGR of 10.6%. You can see how cleanly dividend growth lines up with EPS growth. Great control from management. And kicking the passive income train off is the stock’s market-beating yield of 2.7%. With a moderate payout ratio of 44%, this train should keep moving for years to come. Great business. Great dividend. Great valuation.

Despite Lockheed Martin’s obvious quality, and despite the built-in demand for its products and services from clients with nearly-endless money, the valuation here is surprisingly low. The P/E ratio of 16.5, for example, isn’t just below the broader market’s earnings multiple but also Lockheed Martin’s own five-year average P/E ratio of 19.1. I’m currently putting together a full analysis and valuation report on Lockheed Martin, which should be live soon. Meanwhile, if you haven’t yet got enough of this world-class defense contractor in your portfolio, now would be a good time to consider right-sizing that exposure.

Despite Lockheed Martin’s obvious quality, and despite the built-in demand for its products and services from clients with nearly-endless money, the valuation here is surprisingly low. The P/E ratio of 16.5, for example, isn’t just below the broader market’s earnings multiple but also Lockheed Martin’s own five-year average P/E ratio of 19.1. I’m currently putting together a full analysis and valuation report on Lockheed Martin, which should be live soon. Meanwhile, if you haven’t yet got enough of this world-class defense contractor in your portfolio, now would be a good time to consider right-sizing that exposure.

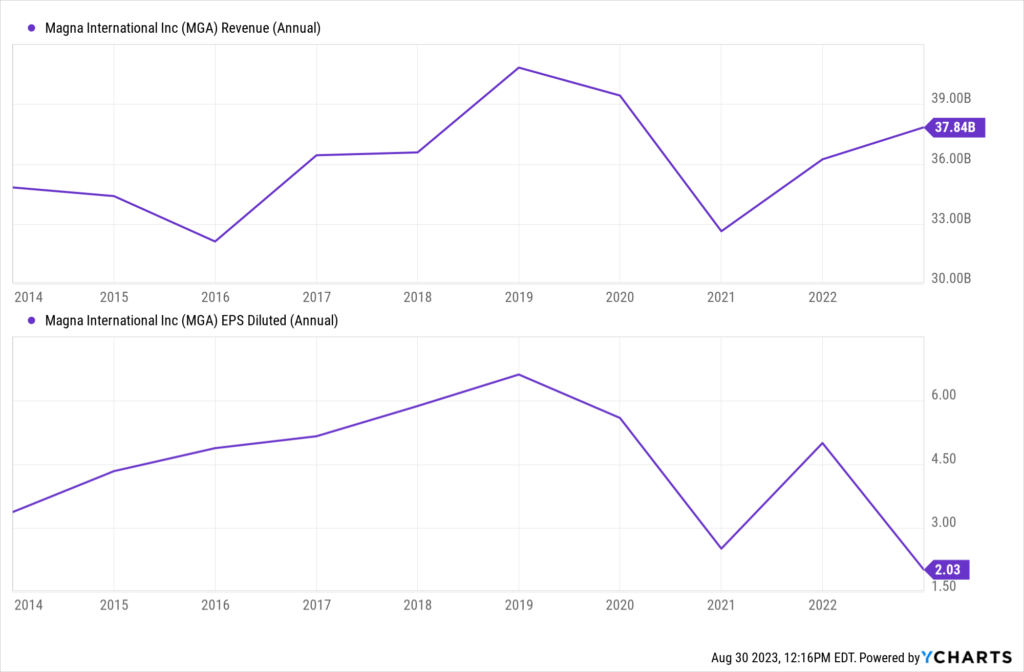

My fifth dividend growth stock for September 2023 is Magna International (MGA). Magna is is a multinational mobility solutions and technology company.

This company designs, develops, and manufactures automotive systems, assemblies, modules, and components for automakers. In fact, Magna is so adept at manufacturing components for automakers, they could practically make their own cars, if they were so inclined. But they’re not inclined.

Magna is doing quite well in their niche. And this niche is only getting better, as mobility is becoming increasingly pervasive and complex. All that does is strengthen the likes of Magna. After all, the carmakers need a capable and reliable manufacturing partner.

Magna is one of the most capable and reliable out there. While the 0.9% CAGR for revenue and 2.2% CAGR for EPS over the last decade looks downright poor, that’s mainly because the last two years have been heavily impacted by the pandemic. But we invest in where a company is going, not where it’s been. On that front, the near-term forecast for growth looks good. And Magna most recently reported 81% YOY growth in adjusted EPS.

The last few years have been tough on the business, but Magna never let its shareholders down when it comes to the dividend. It would have been easy to excuse Magna for cutting the dividend. It was an unprecedented period for the business and, well, the industry at large. But Magna held firm. Never cut the dividend.

The last few years have been tough on the business, but Magna never let its shareholders down when it comes to the dividend. It would have been easy to excuse Magna for cutting the dividend. It was an unprecedented period for the business and, well, the industry at large. But Magna held firm. Never cut the dividend.

To the contrary, it kept increasing right on schedule. That speaks volumes. The dividend has been increased for 14 consecutive years, with a 10-year DGR of 12.6%. Not bad, right? If that doesn’t entice you, the yield of 3.2% might. The dividend, by the way, looks safe. Growth is rebounding quickly. And the payout ratio of 42.3%, based on TTM adjusted EPS, offers a lot of headroom here.

This isn’t my favorite business. It’s capital intensive. Margins are a bit thin. However, the low valuation seems to factor all of that in… and then some.

The P/E ratio, using TTM adjusted EPS, is sitting at right about 13. That is low. Even for a business that doesn’t exactly “wow” me. We recently published a full analysis and valuation video on Magna, estimating fair value for the business at right about $67/share. The stock’s pricing of $57 seems to have a lot of upside potential. And you’re getting a 3.2% yield growing at a nice clip while you wait for the rebound to play out and the stock to catch up to all of that. Not a bad setup at all.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income