The stock market is a marvelous thing.

It offers ordinary people an extraordinary opportunity.

Almost anyone can enter the market and build substantial wealth and passive income over time.

Take me, for example.

Despite growing up poor, not having a college degree, and never making much money at my job, the stock market allowed me to achieve financial independence in my early 30s.

Crazily enough, I also got a late start with it!

Crazily enough, I also got a late start with it!

My Early Retirement Blueprint chronicles all of this.

It describes how I was able to retire in my early 30s – despite not starting with saving and investing until I was almost 28 years old.

A pillar of the Blueprint is the investment strategy I used.

That strategy is dividend growth investing.

This strategy advocates buying and holding shares in world-class businesses that pay reliable, rising dividends to shareholders.

You can find hundreds of examples by perusing the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I’ve been diligently living below my means and investing my excess capital into high-quality dividend growth stocks.

In the process of doing that, I built my FIRE Fund.

In the process of doing that, I built my FIRE Fund.

This is my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

Of course, you can’t blindly buy any stock.

When you buy a stock, you’re investing in an actual business.

That’s why it’s so critical to pay attention to fundamentals.

Also, valuation at the time of investment is very important.

After all, price is only what you pay, but it’s value that you end up getting.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

We have an extraordinary opportunity in front of us, and buying undervalued high-quality dividend growth stocks is a powerful way to unlock it.

Of course, this unlocking process does require one to understand the basics of valuation.

Fear not.

My colleague Dave Van Knapp put together Lesson 11: Valuation in order to make the valuation concept simple to understand.

Part of a more comprehensive series of “lessons” on dividend growth investing, it lays out a valuation template that can be applied toward just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Corning Incorporated (GLW)

Corning Incorporated (GLW)

Corning Incorporated (GLW) is a multinational materials science company that manufactures specialty glass, ceramics, optical fiber, and related materials.

Founded in 1851, Corning is now a $28 billion (by market cap) materials mammoth that employs almost 60,000 people.

The company reports results across five major business segments: Optical Communications, 35% of FY 2022 sales; Display Technologies, 23%; Specialty Materials, 14%; Environmental Technologies, 11%; and Life Sciences, 9%. All Other accounts for the remaining 7%.

Corning is an essential player in making various technologies work.

We can go down the list: optical fiber for internet access, glass for smartphones, or specialty materials for advanced R&D processes.

In fact, there’s a pretty decent chance that the glass you’re interfacing with right now (in order to consume this piece of investment research I’ve made for you) was manufactured by Corning.

Corning is a proven leader in specialty materials.

The company has demonstrated an ability to innovate and stay ahead of the competition for decades.

Morningstar puts it like this: “Corning is a materials science behemoth with differentiated glass products for televisions, notebooks, mobile devices, wearables, optical fiber, cars, and pharmaceutical packaging. In its 170 years of operation, the company has constantly innovated (including inventing glass optical fiber and ceramic substrates for catalytic converters) and oriented itself toward evolving demand trends that it can serve through its core competency of materials science. Most recently, we point to Corning’s domination of the smartphone cover glass market and deals with U.S. network carriers to supply fiber for 5G buildouts as evidence of the pivot toward growth.”

What more can you say?

Corning hasn’t been prospering for nearly two centuries by accident.

A lot of everyday tech we use, and almost take for granted, doesn’t really exist without Corning’s input.

And I’m quite confident that the tech of tomorrow, which is even more exciting, will require Corning’s input.

That’s why Corning is positioned so well to continue growing its revenue, profit, and dividend for many years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

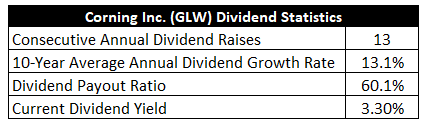

To date, Corning has increased its dividend for 13 consecutive years.

The 10-year dividend growth rate is 13.1%, which is strong.

That dividend growth rate has also been pretty consistent over the last decade.

And you get to kick things off with the stock’s market-beating 3.3% yield.

And you get to kick things off with the stock’s market-beating 3.3% yield.

This yield, by the way, is 60 basis points higher than its own five-year average.

The payout ratio of 60.1%, based on TTM adjusted EPS, is slightly elevated but unconcerning.

I tend to like dividend growth stocks in what I refer to as the “sweet spot” – a yield of between 2.5% and 3.5%, paired with a high-single-digit (or higher) dividend growth rate.

We’re clearly in the sweet spot here.

You’re getting a pretty satisfactory amount of both yield and growth from Corning.

Revenue and Earnings Growth

As satisfactory as these metrics may be, most of them are looking into the past.

However, investors must look into the future, as today’s capital is being risked for the rewards of tomorrow.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will be of great aid when the time comes to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then unveil a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this manner should allow us to confidently estimate where the business could be going from here.

Corning moved its revenue from $7.8 billion in FY 2013 to $14.2 billion in FY 2022.

That’s a compound annual growth rate of 6.9%.

Solid top-line growth here.

I’d usually expect a mid-single-digit top-line growth rate from a fairly mature business such as this.

Corning did even better than that.

Meanwhile, earnings per share grew from $1.34 to $2.09 (adjusted) over this period, which is a CAGR of 5.1%.

The company’s last fiscal year saw unusual restructuring charges, which is why I used adjusted EPS.

Coring has suffered through some margin compression, which affected bottom-line growth.

These are pretty decent numbers, but I’d like to see EPS growth pick up.

We may have some good news on that front.

Looking forward, CFRA is projecting a 10% CAGR for Corning’s EPS over the next three years.

That would be more like it!

Some areas of Corning are doing really well.

Other areas are not.

CFRA sums up the lumpiness in growth across Corning with this passage: “The company is combating softening demand for smartphones, TVs, and automobiles, but this is offset by content growth of inputs for smartphone cameras, gasoline particulate filters for [internal combustion engines], and larger in-cabin displays for automobiles. We are encouraged by investments in fiber infrastructure as operators expand capacity, capability, and access. In addition, we expect life sciences momentum to continue due to strong research funding and lab utilization, partially offset by weak Covid product demand.”

The last few years have been especially lumpy, undoubtedly affected by the pandemic.

But there’s evidence that a bottom is behind us and Corning is on the upswing.

The company’s most recent quarterly report, for Q2 FY 2023, showed 10% YOY growth in adjusted EPS.

That’s precisely in line with CFRA’s near-term EPS growth forecast.

If we take this as our near-term base case, which I think is a reasonable assumption to make, that sets up Corning for like dividend growth.

I would actually expect something less than that, as the payout ratio is slightly elevated.

But even a high-single-digit dividend growth rate is more than enough to get the job done.

After all, you get that 3%+ yield to start off with.

Financial Position

Moving over to the balance sheet, Corning has a good financial position.

The long-term debt/equity ratio is 0.5, while the interest coverage ratio is over 7.

That latter number was hurt by low GAAP earnings in the last fiscal year, and I’d expect a higher interest coverage ratio in future years.

Profitability is okay.

The firm’s net margin has averaged 7.1% over the last five years, while return on equity has averaged 8%.

I prefer higher returns on capital, but Corning has done well anyway.

Overall, Corning is an enviable position of being the company when it comes to a variety of specialized materials.

And with economies of scale, IP, vertical integration, R&D, and switching costs, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

The company faces risks around technological obsolescence, and Corning must continue to innovate in order to stay ahead of the competition.

Corning’s end markets are sensitive to economic cycles, which leaves Corning somewhat vulnerable to a recession.

Vertical integration is an advantage, but input costs are rising.

Being an international organization, the company is exposed to currency exchange rates and geopolitical risks.

The company is mildly acquisitive, which introduces execution risks.

I don’t see any of these risks as being overly cumbersome, especially when compared to the total profile of the business.

Plus, the valuation appears to be at least mildly appealing…

Stock Price Valuation

The stock is trading hands for a P/E ratio of 18.4.

That’s using TTM adjusted EPS.

It’s a below-market earnings multiple on a peerless business.

The P/S ratio of 2.2 is also below its own five-year average of 2.3.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

That’s well below Corning’s proven dividend growth over the last decade.

In addition, the near-term forecast for EPS growth is well above this rate.

However, the payout ratio is slightly elevated, which is a result of EPS growth over the last decade not quite keeping up with dividend growth.

If management is prudent, some moderation in the dividend growth, in order to reduce the payout ratio, would be wise.

Still, a high-single-digit dividend growth rate is really not a bad deal at all here.

And it’s possible that I’m erring on the side of caution, which I’m often liable to do.

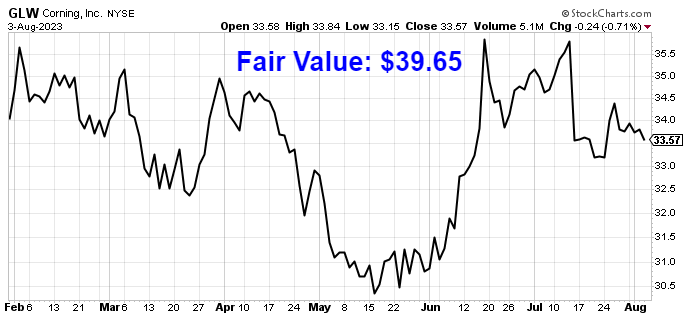

The DDM analysis gives me a fair value of $39.95.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think I put together a reasonable model, yet the stock comes out looking downright cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates GLW as a 4-star stock, with a fair value estimate of $39.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates GLW as a 4-star “BUY”, with a 12-month target price of $40.00.

Boy, you won’t see a much tighter consensus than this. Averaging the three numbers out gives us a final valuation of $39.65, which would indicate the stock is possibly 15% undervalued.

Bottom line: Corning Incorporated (GLW) is an under-the-radar company providing some of the specialized materials that are crucial to making a lot of everyday products work. In some ways, it’s peerless. With a market-beating yield, a double-digit long-term dividend growth rate, a reasonable payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 15% undervalued, long-term dividend growth investors looking for an outside-of-the-box idea have one right here.

Bottom line: Corning Incorporated (GLW) is an under-the-radar company providing some of the specialized materials that are crucial to making a lot of everyday products work. In some ways, it’s peerless. With a market-beating yield, a double-digit long-term dividend growth rate, a reasonable payout ratio, more than 10 consecutive years of dividend increases, and the potential that shares are 15% undervalued, long-term dividend growth investors looking for an outside-of-the-box idea have one right here.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is GLW’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 77. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, GLW’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income