You and I, my fellow contrarian, are old enough to remember when “I bonds”—US savings bonds designed to protect you from inflation—yielded 9.62%.

It was May 2022. Just 14 months ago!

Ah, the good ol’ days. Since then, Series I savings bond rates have tumbled to 4.3%.

Many readers wrote in with I bond questions earlier this year. The savings vehicles boasted a still sweet 6.89%. But they had two major limitations:

- I bonds tie up our money for a year.

- We can only invest $15,000 in them annually.

(The annual limit is $10,000 per person, plus an extra $5,000 per year if using a federal tax refund. These position sizes and liquidity restrictions prevented I bonds from being a big play for us.)

Having $15K tied up earning 9.62% or even 6.89% is one thing. A lousy four-point-three percent is another.

Ah, the problem with “short duration” vehicles like I bonds. It’s great when rates are rising and our yields reset higher. But with inflation trending lower, this dividend party is done for now.

I bonds, our customer service team is going to miss questions about you. For forty years we heard nothing, then a clamor, and now, quiet again. I bonds, you were the Mayfly of the investing world. Gone but not forgotten.

So, my I bond refugees, where are we stashing our up-to-$15K that is rolling off? Of course, we’re not settling for 4.3% like vanilla investors!

Heck no. We’re on to the next payer. This time, we’re going to lock in duration (how long until a bond matures). Let’s kick off our shoes and stay a while.

What to buy? Simple. The Federal Reserve is keeping rates high, for as long as they can—they told us so last week. What Chairman Jay Powell didn’t say, at least explicitly, is that they are going to hold rates high until we hit a recession.

Yeah, I know. He’ll never admit he’s gunning for the “R” word. But he is. Powell’s perfect scenario is the “soft landing” that cools demand and finally takes inflation below his 2% target.

As the economy eventually slows down, interest rates will drop. That’s bullish for “bond proxies” like utility stocks. High flyers like tech and AI stocks will lose their luster. The investing playbook preached by our grandparents will be dusted off.

Utility dividends. That’s about as old school as it gets, and it’s exactly what we want as this much-anticipated recession arrives!

These stocks are likely to be the darlings of 2024. Which is why we are loading up on them now.

Last week, we discussed Dominion Energy (D), my favorite blue-chip utility stock. D yields 5% today. It rarely pays this much.

I bond investors can not only get a pay raise with D, but they can “lock in” a 5% yield for years to come.

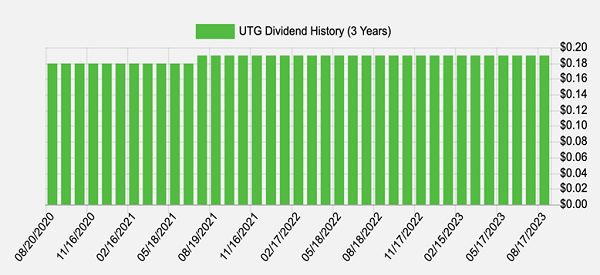

Want more yield from the utility sector? Consider closed-end funds (CEFs). While the mainstream media talks tech, we “second-level” investors revel in Reaves Utility Income (UTG).

UTG focuses on traditional utilities like Duke Energy (DUK) and Southern Co (SO). (Surprisingly, no Dominion! Which is fine—we’ll help ourselves.)

The fund frequently trades at premiums to its NAV, in recent years as high as 13%! But as I write, UTG trades at NAV, which is about as “cheap” as it ever gets.

UTG pays a sweet monthly dividend, which adds up to an elite 8.2% per year. Plus the occasional payout raise, too.

Source: Income Calendar

Source: Income Calendar

We’re not interested in paying $1.13 for $1 in assets. But we’ll take the $1 for $1 UTG “fair trade” available today. Especially at this near-term top in long rates, which should be a nice tailwind for UTG.

— Brett Owens

Sponsored Link: And thanks to the recent bear market, most of my 8% Monthly Payer Portfolio is flashing buy signals today! Don’t miss out on these dividend deals—learn more here!

Source: Contrarian Outlook