I love being a dividend growth investor. It’s the easiest and best “job” I’ve ever had.

What does a dividend growth investor do? They buy shares in world-class businesses that pay reliable, rising dividends. And they hold these shares for the long term.

For all of that hard work, they collect ever-more passive dividend income, year in and year out, all while they watch their wealth also slowly increase. Not bad, right?

Today, I want to tell you about six dividend growth stocks that just increased their dividends.

Ready? Let’s dig in.

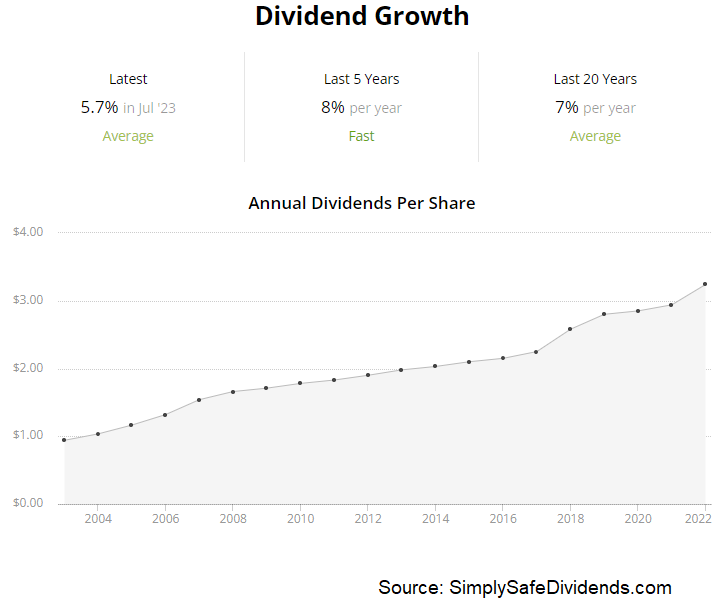

The first dividend increase I have to tell you about is the one that came in from Cullen/Frost Bankers (CFR). Cullen/Frost just increased its dividend by 5.7%.

Cullen/Frost flies under the radar. But it’s been money when it comes to dividend increases. Super, super consistent. How consistent? The bank has increased its dividend for 30 consecutive years.

How about that? That’s Dividend Aristocrat territory. Really incredible. Want more evidence of consistency? Well, the 10-year DGR is 5.5%. This most recent dividend raise was almost dead on. Now, a 5.5% dividend growth rate isn’t super high, no.

However, the stock does offer a pretty nice yield of 3.5%. So you get a nice yield. And very decent growth. With a payout ratio of 34.5%, Cullen/Frost likely has many, many years left in the dividend growth tank.

However, the stock does offer a pretty nice yield of 3.5%. So you get a nice yield. And very decent growth. With a payout ratio of 34.5%, Cullen/Frost likely has many, many years left in the dividend growth tank.

Like pretty much every other bank stock out there, this name is pretty cheap. The thing is, bank stocks have been cheap for as long as I’ve been investing. Probably always will be cheap. Still, you really don’t need much multiple expansion to make money here.

As long as Cullen/Frost continues to advance the business and dividend, even a static valuation can get you to a 10% annualized total return. And that’s not bad. Seeing as how this is a small bank – its market cap is only $7 billion – and its advantageous location in Texas, I don’t see why Cullen/Frost can’t keep pushing forward at a good clip. Meantime, neither the P/E ratio of 10.6 nor the P/B ratio of 2.1 are overly demanding.

The second dividend increase we have to go over is the one that was announced by Cummins (CMI). Cummins just increased its dividend by 7%.

Solid. Especially with inflation coming way down and back into a normal range. Using the Rule of 72, a 7% growth rate doubles your money every 10 years. So that’s double the income from Cummins in a decade, at this growth rate. Not bad at all!

This marks the 18th consecutive year of dividend increases for the engine and power generation company. Cummins is mostly known for its engines. But some of us know Cummins as a dividend growth engine. The 10-year DGR is 12.9%.

But the five-year DGR of 7.5% is really more in line with what Cummins has been doing. And you can see that high-single-digit dividend growth rate show up once again this year. Seeing as how the stock yields 2.6%, a 7% or so dividend growth rate is enough to get the job done. And I think that job keeps getting done, as the payout ratio is only 37.9%.

But the five-year DGR of 7.5% is really more in line with what Cummins has been doing. And you can see that high-single-digit dividend growth rate show up once again this year. Seeing as how the stock yields 2.6%, a 7% or so dividend growth rate is enough to get the job done. And I think that job keeps getting done, as the payout ratio is only 37.9%.

This is a great business. And the valuation looks to be pretty decent. We last covered Cummins earlier this year, highlighting it as an undervalued high-quality dividend growth stock to consider. Back then, the the stock was priced at around $245. It’s now in the $260 range. So a bit of a bump. Not surprising. The whole market has been on a tear.

However, in that video, the estimate for fair value on Cummins came out to $269.35/share. Perhaps slightly undervalued here. Not the deal it was before. But one could also do a lot worse than Cummins, in my view.

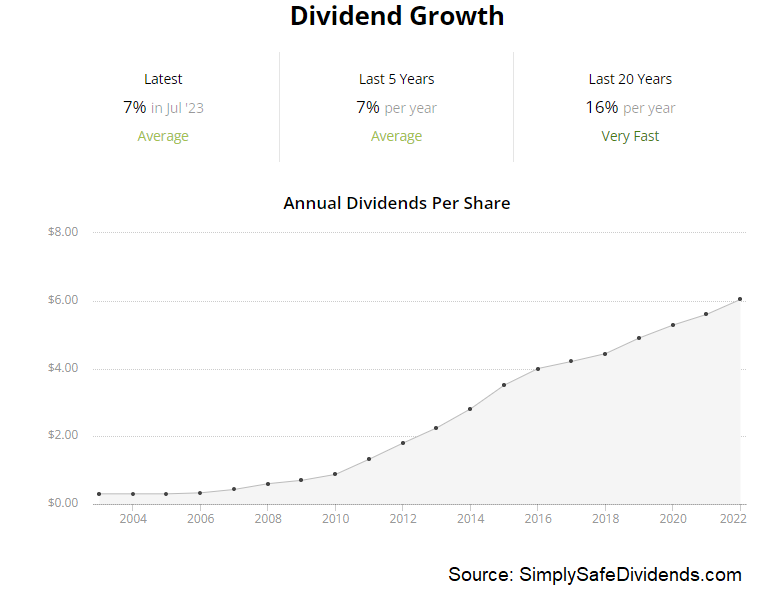

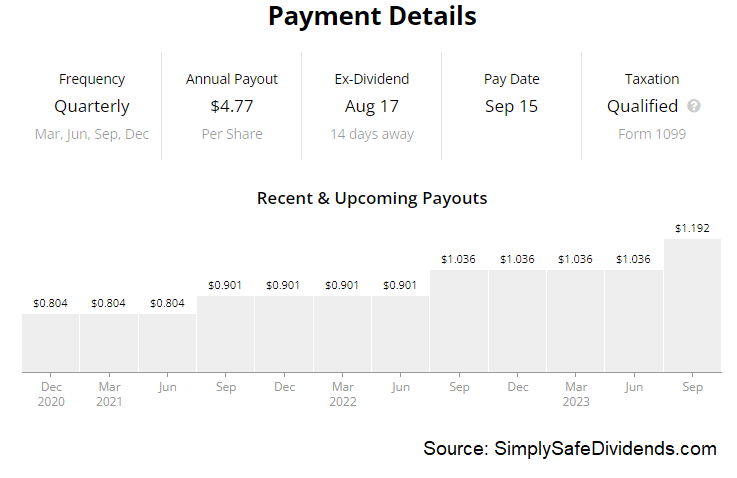

The third dividend increase I have to tell you about is the one that came courtesy of Cintas (CTAS). Cintas just increased its dividend by 17.4%.

Boom. You just have to love this stuff. That’s a 17.4% pay raise without lifting a finger. All Cintas shareholders had to do in order to get this bump to their dividend income was not sell their shares. Like I said, dividend growth investing is the easiest job ever. This is the 41st consecutive year of dividend increases for the business services company.

Cintas has been a dividend growth star for decades. The 10-year DGR is 20.7%. And this recent dividend raise isn’t all that far off. The only bummer here might be the yield, which is just 1.1%. But that’s basically right in line with its own five-year average. When your dividend is growing at a double-digit rate like this, the yield isn’t going to be super high, nor does it need to be. It’s a total return story. And the payout ratio of 41.3% indicates that this story isn’t ending any time soon.

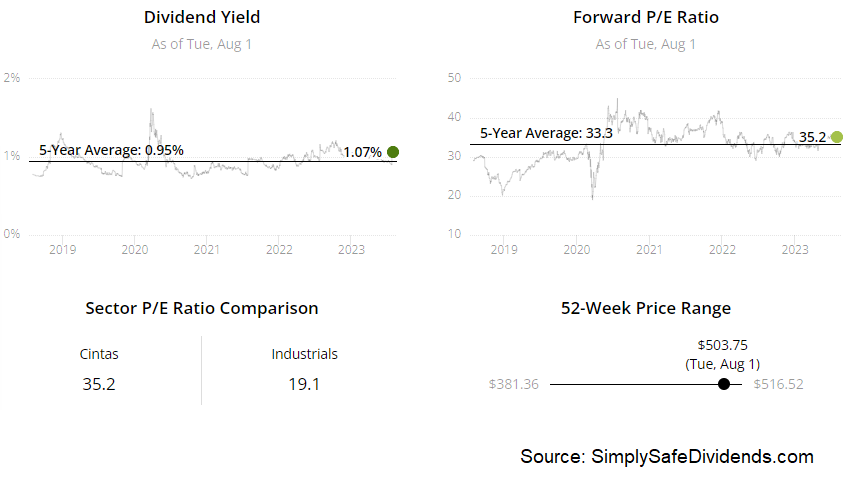

Cintas isn’t cheap. Never is. Never will be. Cintas has looked expensive for years. But guess what? The stock has been a monster anyway. It’s up by almost 1,000% over the last 10 years. You tend to get what you pay for in life. And quality is worth more.

Cintas isn’t cheap. Never is. Never will be. Cintas has looked expensive for years. But guess what? The stock has been a monster anyway. It’s up by almost 1,000% over the last 10 years. You tend to get what you pay for in life. And quality is worth more.

Some investors will just never understand that. Getting back to that total return story, the stock’s 10-year CAGR, with dividends reinvested, is almost 30%. Unreal. That’s more than 10x your money in just a decade. A quick 10-bagger, folks. Now, the P/E ratio on Cintas is close to 40. The cash flow multiple is over 30. Cintas isn’t for bargain hunters or yield chasers. But those who can appreciate quality and are looking for an outstanding total return over time, Cintas is amazing.

The fourth dividend increase we must have a quick conversation about is the one that came shareholders’ way from Hershey (HSY). Hershey just increased its dividend by 15.1%.

Man. That is what dividend growth investing is all about. You go to bed at one income level. You wake up the next day at an income level that’s 15.1% higher. And you did nothing at all but sleep.

The confectionary and snack company has now increased its dividend for 14 consecutive years. Hershey brings the sweets. And not just chocolate but sweet, sweet dividend raises. The 10-year DGR is 9.5%, but there’s been a clear acceleration in dividend growth over the last decade. Music to shareholders’ ears. And you even get a respectable 2% yield here, which is right in line with its own five-year average. A balanced payout ratio of 54.9% indicates plenty of more sweet dividend raises yet ahead.

The confectionary and snack company has now increased its dividend for 14 consecutive years. Hershey brings the sweets. And not just chocolate but sweet, sweet dividend raises. The 10-year DGR is 9.5%, but there’s been a clear acceleration in dividend growth over the last decade. Music to shareholders’ ears. And you even get a respectable 2% yield here, which is right in line with its own five-year average. A balanced payout ratio of 54.9% indicates plenty of more sweet dividend raises yet ahead.

Hershey is a very high-quality business. And quality does not come cheap. Most multiples are slightly elevated in comparison to their respective recent historical averages. So, relative to itself, the stock looks, perhaps, just a touch overvalued.

However, those average multiples are all quite high. The P/E ratio, for instance, has averaged 26.3 over the last five years. Hershey tends to command a premium. And rightfully so, in my view. The P/E ratio is currently 28.5. Higher than normal. I think Hershey is worth paying more for. Just not sure it’s worth paying so much more than usual for. I’d probably let this one come back down a bit before thinking about buying it.

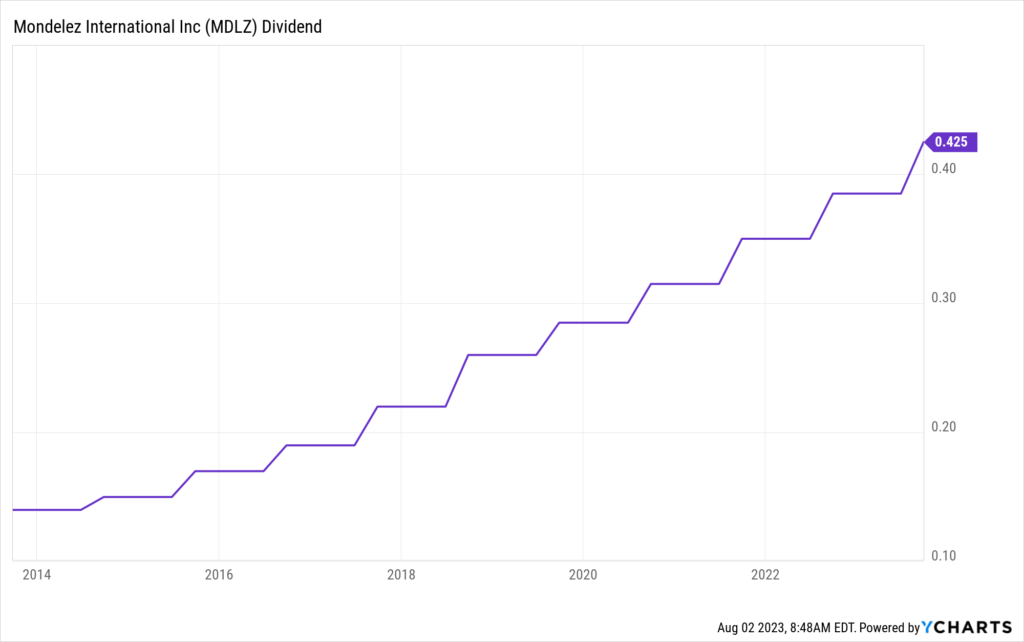

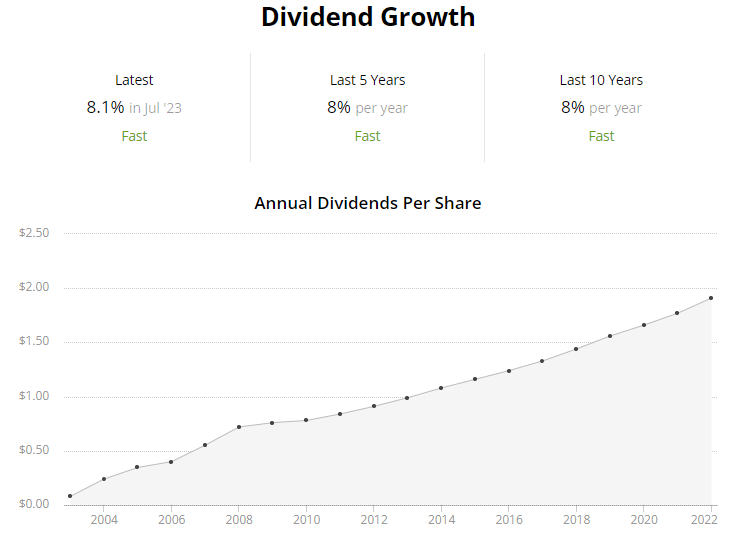

The fifth dividend increase we should talk about is the one that came courtesy of Mondelez International (MDLZ). Mondelez just increased its dividend by 10.4%. Yet another high-quality business. Yet another double-digit boost to the dividend payments it send out shareholders. This stuff is just so, so good.

This marks the 12th consecutive year of dividend increases for the confectionary, snack, and beverage company. We just went over Hershey.

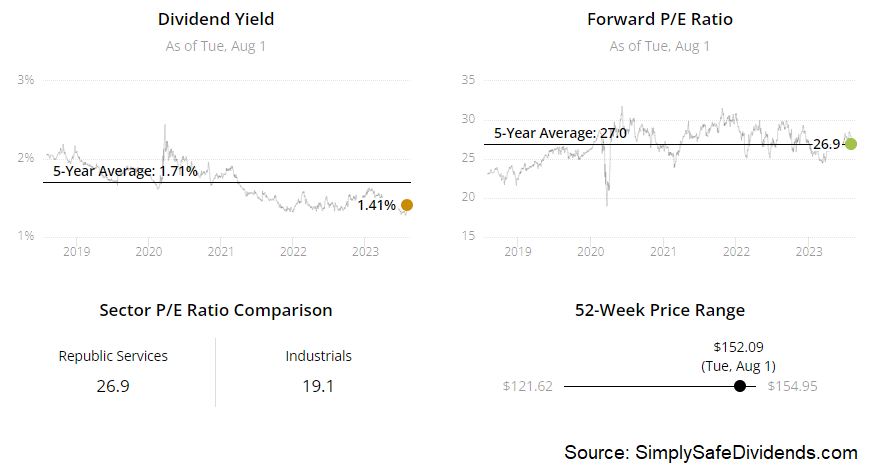

Well, Mondelez doesn’t get as much attention as Hershey. But it’s running a pretty comparable business. The five-year DGR is 11.8%. And Mondelez has been good for that kind of low-double-digit growth for a number of years now, including this year. The stock also offers a market-beating 2.3% yield, which is 20 basis points higher than its own five-year average. Not a bad yield with this kind of dividend growth. And we’ve got another balanced payout ratio of 56.5%.

Well, Mondelez doesn’t get as much attention as Hershey. But it’s running a pretty comparable business. The five-year DGR is 11.8%. And Mondelez has been good for that kind of low-double-digit growth for a number of years now, including this year. The stock also offers a market-beating 2.3% yield, which is 20 basis points higher than its own five-year average. Not a bad yield with this kind of dividend growth. And we’ve got another balanced payout ratio of 56.5%.

This stock has gone on a nice run this year. Might want to let it cool down a bit. It’s up 14% on the year. And we’re barely more than halfway done with 2023. Most multiples look slightly extended now. The P/E ratio of 26.2 is lower than Hershey’s, sure.

But it’s notably higher than its own five-year average of 22.8. The cash flow multiple of 26.4 is also much higher than its own five-year average of 20.3. Mondelez is a great business. It’s worth a premium. But the current premium looks to be too heavy. The stock is currently priced at $75. Something closer to $70 is more interesting.

The sixth dividend increase I have to cover is the one that was given out by Republic Services (RSG). Republic Services just increased its dividend by 8%. Not quite as impressive as some of the other dividend increases I’ve covered today, but it’s still 8% more money. There is something magical about getting paid more money without doing anything in return, isn’t there?

The waste disposal company has now increased its dividend for 21 consecutive years. Nothing trashy about that. The 10-year DGR is 7.7%, so Republic Services is right on target yet again. Now, the stock only yields 1.4%. And you might think that yield isn’t good enough with a high-single-digit dividend growth rate.

The waste disposal company has now increased its dividend for 21 consecutive years. Nothing trashy about that. The 10-year DGR is 7.7%, so Republic Services is right on target yet again. Now, the stock only yields 1.4%. And you might think that yield isn’t good enough with a high-single-digit dividend growth rate.

But this business model ensures steady business, no matter what. Humans will continue to produce a lot of trash. And that kind of visibility into the future is worth a lot. With a payout ratio of 44.7%, we’ve certainly got a lot of dividend growth viability here.

Love this business. Don’t love the valuation. It’s hard to not love this business. The certainty that this business model offers is really, really attractive. And I think it’s definitely worth a premium. But how much of a premium is the question. Is the current earnings multiple of almost 32 too high? It’s up there for sure.

Its own five-year average P/E ratio is 28.2. And every other basic multiple is showing something similar. A premium is justified here. But the premium right now is awfully strong. A 10% pullback would make Republic Services a highly compelling long-term investment idea.

Its own five-year average P/E ratio is 28.2. And every other basic multiple is showing something similar. A premium is justified here. But the premium right now is awfully strong. A 10% pullback would make Republic Services a highly compelling long-term investment idea.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income