US stocks are some of the best most sought-after assets in the whole world.

But within that broader universe, there’s a subset of stocks that is particularly compelling.

I’m talking about high-quality dividend growth stocks.

These stocks represent equity in world-class businesses selling the products and/or services the world demands more and more of.

These businesses are so adept at producing gobs of growing cash flow, they’re left with a lot of money they can’t effectively use.

Well, they end up returning some of that back to shareholders, via growing dividend payments.

And those growing dividend payments can be a fantastic source of passive income… which one can even live off of.

It’s easy to see why high-quality dividend growth stocks are compelling.

But when they’re on sale – when they’re undervalued – that’s when the appeal is off the charts.

Price and yield are inversely correlated.

All else equal, lower prices result in higher yields.

This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach.

Now, lower valuations often come when there’s volatility.

But I always see short-term volatility as a long-term opportunity.

That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

With all of that out of the way, it’s a big market, and some ideas are better than others.

Focusing on the very best long-term ideas right now is what this article is all about.

Today, I want to tell you my top 5 dividend growth stocks for August 2023.

Ready? Let’s dig in.

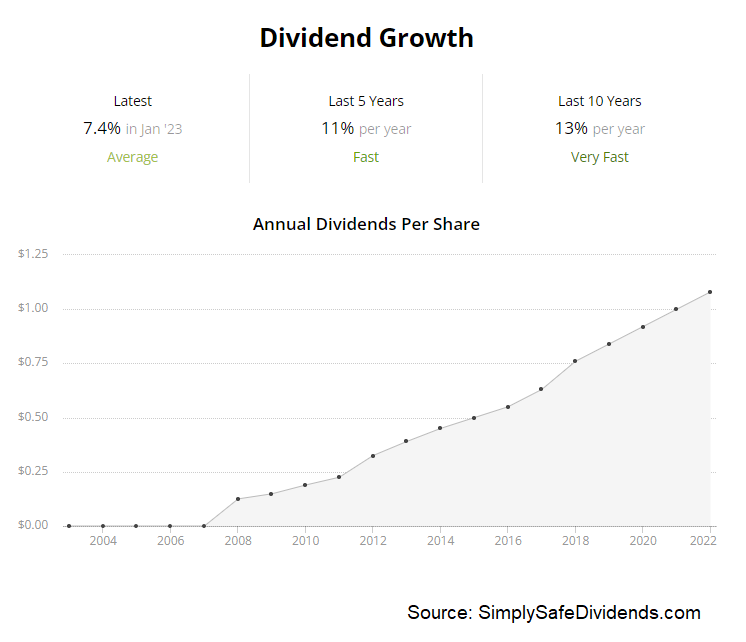

My first dividend growth stock for August 2023 is Comcast (CMCSA). Comcast is a media and entertainment conglomerate.

Yes, Comcast has cable TV. Yes, cable television is slowly dying. It’s in secular decline. But Comcast is so much more than this. It’s an empire that includes broadcast networks, streaming television, a major film studio, theme parks, and, perhaps most importantly, broadband connectivity.

Try living without high-speed access to the Internet in 2023. Not only is Comcast the largest provider of high-speed internet connections in the US but it’s often the only major player in any given market. That’s a monopoly. All of this why Comcast puts up surprisingly strong growth, translating to a 7.2% CAGR for revenue and 12.3% CAGR for EPS over the last decade.

You know what else is surprisingly strong? The dividend growth.

You know what else is surprisingly strong? The dividend growth.

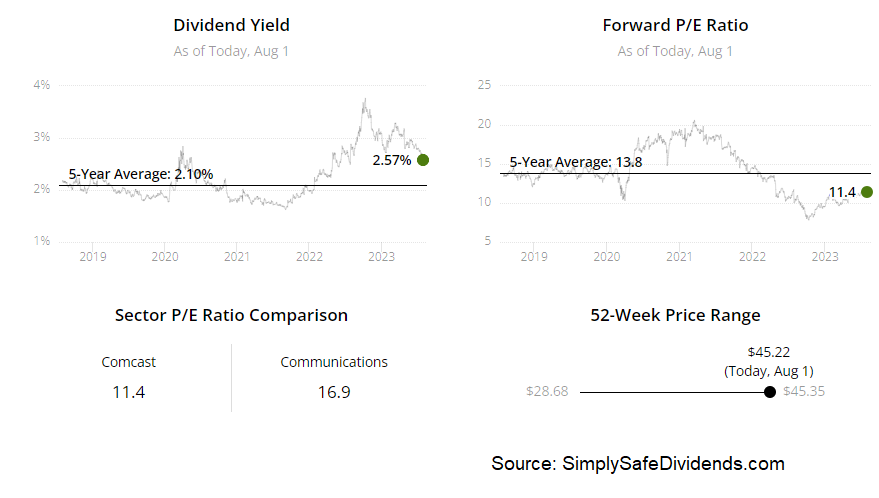

Comcast has increased its dividend for 16 consecutive years. The 10-year DGR of 13.3% just sneaks up on you. Who would expect double-digit dividend growth from Comcast? Now, more recent dividend raises have been in the 8% range. But high-single-digit dividend growth is enough to get the job done here, as evidenced by the stock’s yield of 2.7%. A payout ratio of 31.3%, based on TTM adjusted EPS, indicates to me that Comcast should be able to persist with its dividend growth.

This stock has had a nice run this year. But it still looks undervalued.

The stock is up more than 20% on the year. And shareholders have collected a nice dividend along the way. But that 20%+ pop came off of very depressed levels. It’s still about 30% off of 2021 highs. Of course, this is all pricing talk. Valuation talk is much more interesting. On that point, Comcast does look undervalued as a business.

The stock is up more than 20% on the year. And shareholders have collected a nice dividend along the way. But that 20%+ pop came off of very depressed levels. It’s still about 30% off of 2021 highs. Of course, this is all pricing talk. Valuation talk is much more interesting. On that point, Comcast does look undervalued as a business.

Based on TTM adjusted EPS, the P/E ratio is only 11.5. That is very undemanding. In our recent analysis and valuation, which should already be live, the estimate for fair value on Comcast came out to $53.29/share. Comcast remains interesting, despite the pop.

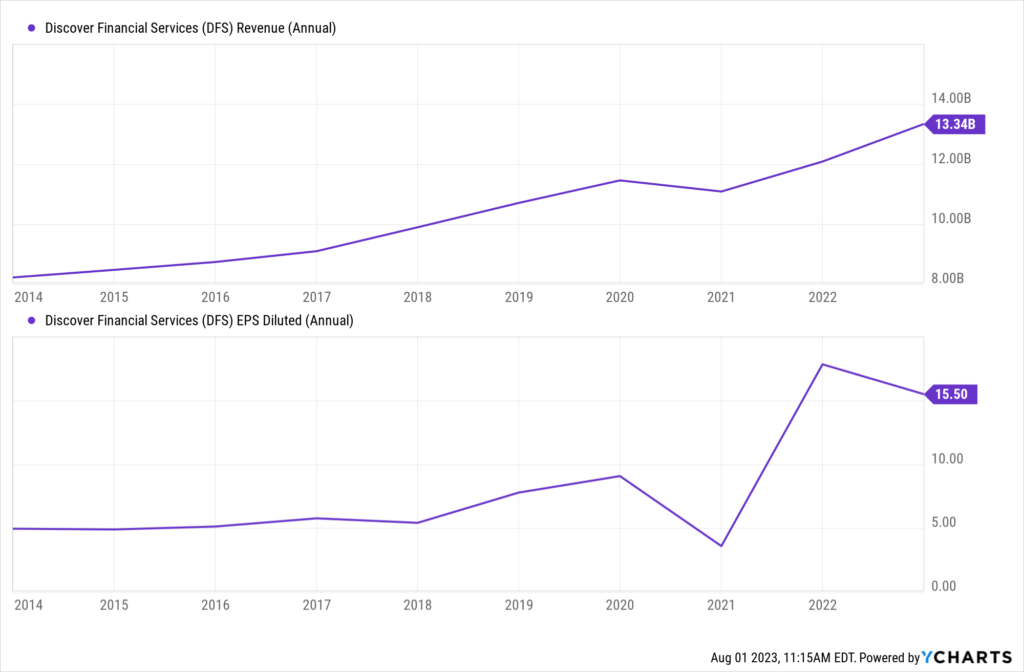

My second dividend growth stock for August 2023 is Discover Financial Services (DFS). Discover Financial is an American financial services company.

Discover Financial is very interesting. It might be best known by its payment network, whereby consumers use a Discover credit card to make purchases. But Discover Financial is mostly a digital bank, and it uses its payment network as a gateway into that bank. In my view, Discover Financial is a really good bank. And a pretty decent payment network.

Except it’s not given much credit for either one. How much credit should it get? Well, the business has compounded its revenue at an annual rate of 5.5% and its EPS at an annual rate of 13.5% over the last decade.

Double-digit business growth has fueled double-digit dividend growth.

Double-digit business growth has fueled double-digit dividend growth.

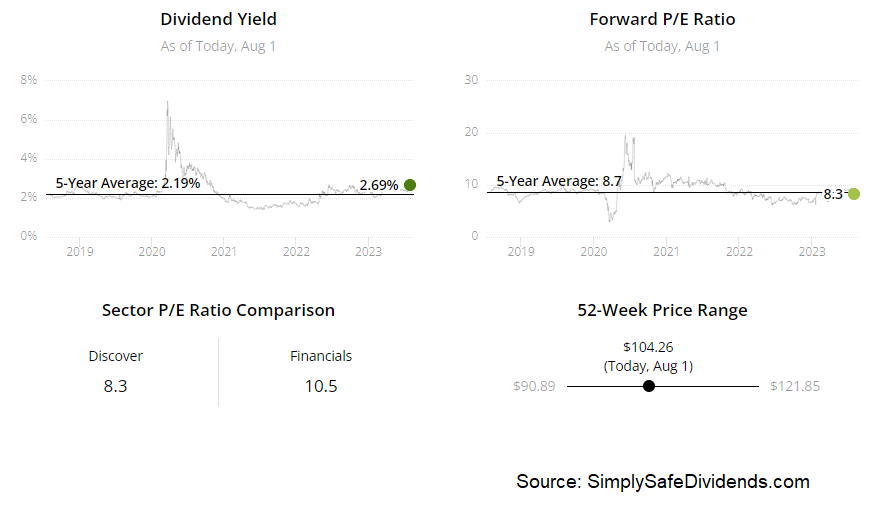

Indeed, Discover Financial, which has increased its dividend for 13 consecutive years, has a 10-year DGR of 19.1%. Even the most recent dividend raise was an astounding 16.7%. Dividend growth has outpaced EPS growth; however, the payout ratio is still sitting at just 18.8%. So the dividend growth could continue to gently outpace EPS growth for a while to come. Meantime, the stock also offers a very respectable 2.7% yield to go along with all of this.

Respectable business. Respectable dividend. Valuation? Not so respectable.

I say that because the multiples are super low across the board. Take the P/E ratio of 7.3, for instance. That’s a fraction of the broader market’s multiple. It’s also substantially lower than the stock’s own five-year average P/E ratio of 10.3.

So this is a stock that just never really commands much respect from the market, but it’s getting an unusual lack of it right now. I’m currently putting together a full analysis of the business right now, and that should go live soon. Until then, I think Discover Financial is something that value-oriented dividend growth investors should be taking a look at.

So this is a stock that just never really commands much respect from the market, but it’s getting an unusual lack of it right now. I’m currently putting together a full analysis of the business right now, and that should go live soon. Until then, I think Discover Financial is something that value-oriented dividend growth investors should be taking a look at.

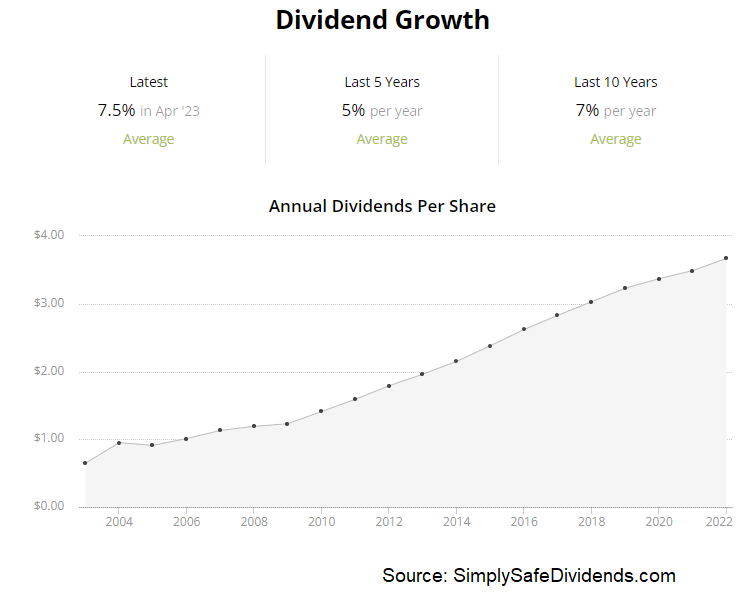

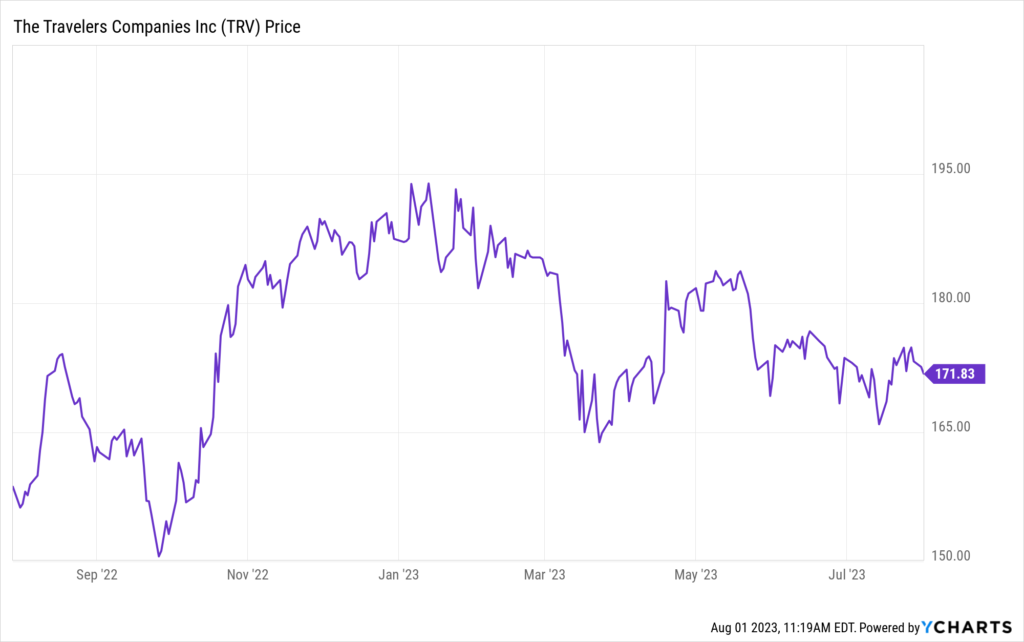

My third dividend growth stock for August 2023 is Travelers Companies (TRV). Travelers is a property and casualty insurance holding company.

Travelers is the only P&C insurance company in the Dow Jones Industrial Average. That goes to show just how much of a blue-chip company Travelers really is. Now, insurance can be a tough gig. It can be a commodity-like business in many ways. No switching costs. Customers are sensitive on price.

However, because of the float, an operator that can maintain good discipline on underwriting can make a lot of money. To that point, Travelers grew its revenue at a CAGR of 3.9% and its EPS at a CAGR of 2.1% over the last decade. Regarding that latter number, it was heavily influenced by an anomalous FY 2022.

Nothing anomalous about the dividend growth.

Travelers is super, super consistent in this department. The company has increased its dividend for 19 consecutive years. Nearly two decades straight. But what’s remarkable is the pace. The 10-year DGR is 7.4%. Not super high, no. But so consistent. It’s like clockwork. The last dividend increase was 7.5%, which is almost exactly in line with the long-term average. The stock also yields 2.3%, which isn’t bad at all. Definitely beats the market. And the payout ratio is a low 34.1%. Solid numbers right across the board.

Travelers is super, super consistent in this department. The company has increased its dividend for 19 consecutive years. Nearly two decades straight. But what’s remarkable is the pace. The 10-year DGR is 7.4%. Not super high, no. But so consistent. It’s like clockwork. The last dividend increase was 7.5%, which is almost exactly in line with the long-term average. The stock also yields 2.3%, which isn’t bad at all. Definitely beats the market. And the payout ratio is a low 34.1%. Solid numbers right across the board.

This blue-chip dividend growth stock looks decently undervalued right now.

It’s not super cheap. But why would one of the best P&C operators out there be super cheap? Instead, I think you’re getting a better-than-fair deal here. Our recent analysis and valuation on Travelers, which should be live soon, shows a great business that could be worth just over $190/share. The stock’s current pricing is sitting at about $173. Good potential upside on a great dividend growth stock.

It’s not super cheap. But why would one of the best P&C operators out there be super cheap? Instead, I think you’re getting a better-than-fair deal here. Our recent analysis and valuation on Travelers, which should be live soon, shows a great business that could be worth just over $190/share. The stock’s current pricing is sitting at about $173. Good potential upside on a great dividend growth stock.

My fourth dividend growth stock for August 2023 is Texas Instruments (TXN). Texas Instruments is a global technology company.

This is one of the best tech companies in all of America. High returns on capital. Fat margins. Exceptional management team that has long focused on free cash flow. It’s hard to run a business better. Texas Instruments specializes in analog semiconductors, which are necessary for all kinds of equipment and devices.

These semiconductors measure real-world information such as temperature, sound, and movement. There’s no future in which we need less of these products, and the company is currently building out more capacity to meet that future demand. That’s why, while Texas Instruments has compounded its revenue at an annual rate of 5.7% and its EPS at an annual rate of 19.4% over the last decade, there should be a lot more where that came from.

There’s also a lot more dividend growth to come.

Texas Instruments has increased its dividend for 19 consecutive years. The 10-year DGR is 20.8%, which lines up nicely with EPS growth over the same time frame. You also get a 2.7% yield here. Love the balance, right? Well, we can see more balance with the payout ratio, which is 55.7%. Nearly perfectly balanced between retaining profit against returning cash to shareholders. Excellent metrics.

Texas Instruments has increased its dividend for 19 consecutive years. The 10-year DGR is 20.8%, which lines up nicely with EPS growth over the same time frame. You also get a 2.7% yield here. Love the balance, right? Well, we can see more balance with the payout ratio, which is 55.7%. Nearly perfectly balanced between retaining profit against returning cash to shareholders. Excellent metrics.

This stock isn’t cheap, nor should it be. But it’s a terrific business. And I think the valuation is really quite reasonable.

Most multiples are in line with, or slightly below, their respective recent historical averages. The earnings multiple of 20.6, which trails its own five-year average of 22.8, is a prime example. The sales multiple of 8.7 is barely ahead of its own five-year average of 8.6. With the company currently building out fabs, it’s setting up for another huge run. The last 10 years saw the stock go up by nearly 400%. Will the next decade look just like that? It’s very, very possible.

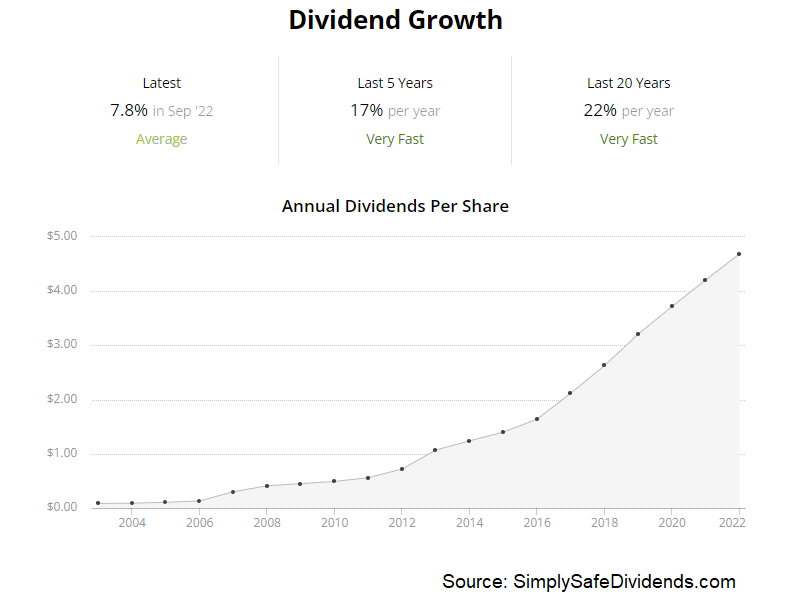

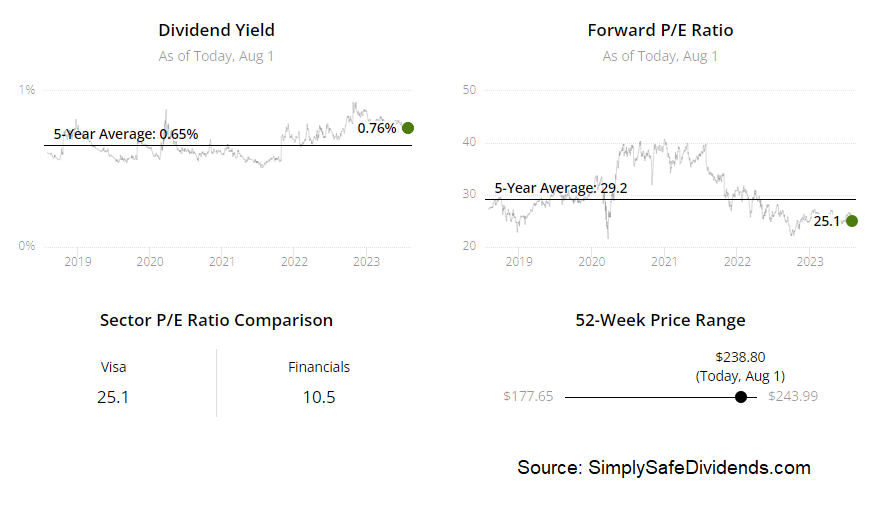

My fifth dividend growth stock for August 2023 is Visa (V).

Visa is a multinational financial services corporation.

The investment thesis for Visa is so simple. It’s thematic. We have a secular trend that’s moving society toward digital payments. The world is becoming more and more cashless. Since Visa is the world’s largest digital payments company, this obviously bodes well for the business and its shareholders. Visa is a growth monster, and I don’t see it slowing down. We’re talking about a 10.6% CAGR for revenue and 15.6% CAGR for EPS over the last decade.

Speaking of monster growth, that’s exactly what you get with the dividend.

Visa, which has increased its dividend for 15 consecutive years, has a 10-year DGR of 20.3%. Of course, with the stock yielding only 0.8%, you really do want to see strong, double-digit dividend growth in order to make sense of things. And with the payout ratio at only 24.1%, Visa has plenty of room for more double-digit dividend growth.

This is one of the best businesses in the world. In my view, the premium valuation is justified.

Having Visa will make almost any portfolio automatically better. It routinely outperforms, and I don’t see that stopping any time soon. Most multiples are high, but they’re actually not as high as they usually are. The P/E ratio of 32.2 might seem outrageous at first glance. But the stock’s own five-year average P/E ratio is 35.6.

We recently put together a full analysis and valuation on the business, and the video should go live soon, if it hasn’t already. In that video, the estimate for Visa’s fair value came out to $258.33/share. The stock’s current pricing of about $241 looks more than fair to me. If you don’t yet have this world-class business in your portfolio, you might want to question that choice right about now.

We recently put together a full analysis and valuation on the business, and the video should go live soon, if it hasn’t already. In that video, the estimate for Visa’s fair value came out to $258.33/share. The stock’s current pricing of about $241 looks more than fair to me. If you don’t yet have this world-class business in your portfolio, you might want to question that choice right about now.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income