We all need hobbies.

My favorite hobby?

Investing.

Whereas many hobbies cost money and are harmful, investing makes money and is helpful.

And if it’s done properly, investing can radically change your life for the better.

How is it done properly?

Well, I’d argue that long-term dividend growth investing is the most proper way to apply investing.

This is a strategy whereby you buy and hold shares in world-class businesses that pay reliable, rising dividends to shareholders.

Reliable, rising dividends act as a filtering process.

Reliable, rising dividends act as a filtering process.

Only great businesses can afford to pay reliable, rising dividends, because those payments to shareholders require the undergirding of reliable, rising profits.

You can see what I mean by perusing the Dividend Champions, Contenders, and Challengers list.

This list contains invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

You’ll notice one great business after another on this list.

And it’s hard to lose money by investing in great businesses for the long term.

This is why I’ve used the dividend growth investing strategy for myself.

I’ve used it to great effect for more than a decade now, building my FIRE Fund in the process.

This is my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

In fact, I’ve been able to live off of dividends for a number of years now.

In fact, I’ve been able to live off of dividends for a number of years now.

I even quit my job and retired in my early 30s.

How did I do that?

My Early Retirement Blueprint explains it all.

Now, it is hard to lose money by investing in great businesses.

However, if you want to ensure even more success, paying attention to valuation is very important.

Price is only what you pay, but value is what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying undervalued high-quality dividend growth stocks, and then holding them for the long term, is a great and enjoyable way to build serious wealth and passive income over time.

This does, of course, mean that you first have to understand how valuation works.

Fear not.

Fellow contributor Dave Van Knapp put together Lesson 11: Valuation in order to help you.

It’s one of his “lessons” on dividend growth investing, and it lays out a valuation template that can be used to estimate the fair value of almost any dividend growth stock you’ll run into.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Comcast Corporation (CMCSA)

Comcast Corporation (CMCSA)

Comcast Corporation (CMCSA) is a media and entertainment conglomerate with interests in cable, broadcasting, film, streaming, live entertainment, and theme parks.

Founded in 1963, Comcast is now a $175 billion (by market cap) media giant that employs nearly 190,000 people.

The company reports operations across five segments: Cable Communications, 55% of FY 2022 revenue; Media, 20%; Sky, 16%; Theme Parks, 7%; and Studios, 2%.

Cable Communications consists of the operations of Comcast Cable, which provides 17.5 million cable video connections, 30 million high-speed internet connections, and 9 million voice services.

Media consists of NBCUniversal’s television and streaming platforms, including a variety of cable networks, the NBC broadcast network, the Telemundo broadcast network, certain television stations, and Peacock.

Sky consists of the operations of Sky, a leading European entertainment company that creates content and provides video, broadband, voice, and wireless phone services.

Studios consists of NBCUniversal’s film and television studio production and distribution operations, and houses Universal Pictures – one of the five major US film production studios.

Theme Parks consists of the worldwide Universal theme parks.

Comcast also has other business interests that consists primarily of the operations of Comcast Spectacor, which owns the Philadelphia Flyers and the Wells Fargo Center arena in Philadelphia, Pennsylvania.

Comcast is an interesting case study in the difference between narrative versus reality.

The common narrative around Comcast is that it’s a dying cable company.

But the reality of the situation is that it’s a thriving conglomerate with many parts of the aggregate growing at healthy clips.

There’s nothing “dying” about broadband internet connectivity, nor are theme parks on their way out.

Yes, Comcast does have issues with the core cable TV business model.

And if that’s all Comcast had to offer, I don’t think it’d be investable.

But it’s only one part of the entire company.

And because it’s getting smaller while other parts of the company are growing, the risks around this one business and its threat to the overall company are actually shrinking.

I’ll give you a quick example of this.

Comcast is absolutely dominant when it comes to broadband internet connectivity, which is about as necessary for people these days as electricity.

Morningstar states this: “We estimate the firm has increased broadband market share in the areas it serves to about 67% from 50% a decade prior, meaning Comcast’s customer base in the typical market area is twice the size of its rivals’.”

And that’s just one area of the entirety.

Simply put, Comcast is a global media and entertainment empire.

Because of that, its growth profile across revenue, profit, and the dividend is healthy.

Dividend Growth, Growth Rate, Payout Ratio and Yield

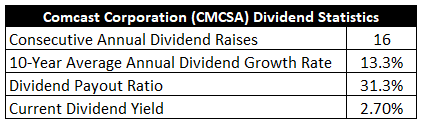

In regard to the dividend, the company has increased its dividend for 16 consecutive years.

The 10-year dividend growth rate is 13.3%, although more recent dividend raises have been in the high-single-digit range.

Still, I think that’s a pretty decent amount of growth when you get to pair it with the stock’s market-beating yield of 2.7%.

This yield, by the way, is 50 basis points higher than its own five-year average.

This yield, by the way, is 50 basis points higher than its own five-year average.

And the payout ratio is only 31.3%, based on TTM adjusted EPS.

I’m fond of dividend growth stocks in the “sweet spot” – a yield of between 2.5% and 3.5%, paired with high-single-digit (or better) dividend growth.

You get a a satisfactory amount of both income and growth, giving one the best of both worlds.

We’re clearly in the sweet spot here.

Despite the narrative, these dividend metrics show a healthy dividend growing at a pretty good clip.

Revenue and Earnings Growth

As healthy as the dividend may appear to be, most of these metrics are looking into the past.

However, investors must look into the future, as today’s capital is being risked for tomorrow’s rewards.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be very handy when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this manner should allow us to roughly gauge where the business might be going from here.

Comcast moved its revenue from $64.7 billion in FY 2013 to $121.4 billion in FY 2022.

That’s a compound annual growth rate of 7.2%.

Surprisingly impressive.

Even though I’m already aware that Comcast isn’t struggling, this is strong top-line growth from a mature company that was already doing more than $60 billion in revenue a decade ago.

Meanwhile, the company grew its earnings per share from $1.28 to $3.64 (adjusted) over this period.

That’s a CAGR of 12.3%.

Wow.

That just doesn’t look like a dying business at all to me.

This is why it’s so important to drill down into the financial reports.

It’s an exercise that can separate fact from fiction.

Now, I used adjusted EPS for FY 2022.

That’s because Comcast recorded non-cash impairment charges related to Sky during the year.

We can see that there was some excess bottom-line growth, and that was mostly driven by extensive share buybacks.

To that point, the outstanding share count has been reduced by about 17% over the last decade.

Looking forward, CFRA is forecasting that Comcast will compound its EPS at an annual rate of 7% over the next three years.

That strikes me as a fair assessment.

CFRA sums it up pretty well with this passage: “We see a continued rebound at the NBCU division, with a full reopening of the worldwide theme parks and the studio pipelines combined with growth in TV distribution and ad revenue. At the cable division, we see continued growth in broadband and wireless subscribers (versus further losses of video and voice customers).”

That’s the crux of it.

It’s a conglomerate with a lot of moving parts.

Many of the moving parts are doing quite well, and better than a lot of people give the company credit for.

But one of the moving parts – cable TV – isn’t.

Don’t get me wrong, it’d certainly be better if cable TV weren’t a melting ice cube.

But that looks like more of a blemish to me than some kind of cancerous stain that’s spreading.

As I touched on earlier, Comcast is dominant in broadband internet connectivity, and this dominance is only increasing.

Broadband is now the cash cow that cable TV once was.

Also, Comcast has been growing its Peacock streaming offering in earnest.

Peacock now has ~20 million subscribers, and the revenue generated from Peacock tripled for FY 2022.

If we take CFRA’s projection as our base case for the near term, that sets up the dividend for a similar, or better, growth track.

And that would line up nicely with what’s been playing out over the last several years.

One could do a lot worse than snagging a high-single-digit dividend growth rate that comes on top of a near-3% starting yield.

Financial Position

Moving over to the balance sheet, Comcast has a mediocre, at best, financial situation.

The long-term debt/equity ratio is 1.2, while the interest coverage ratio is just under 5.

I consider the balance sheet to be the weakest part of the business, although it has improved ever so slightly over the last few years.

Profitability, on the other hand, is robust, and it’s also been improving.

The firm’s net margin has averaged 12.1% over the last five years, while return on equity has averaged 16.1%.

These numbers would both be quite a bit higher if not for the impairment that was recorded in FY 2022.

Overall, I see Comcast as a very solid media and entertainment empire.

Sure, it’s not perfect, and cracks do exist.

But, to paraphrase Mark Twain, reports of the company’s death have been greatly exaggerated.

And with economies of scale, high barriers to entry, and the ability to operate as a local monopoly in many markets, the business does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

While the industry at large is fiercely competitive, Comcast benefits from often being the only major player in any given market.

Streaming TV has been a rising threat, but Comcast counters this with Peacock and its broadband offerings (because one cannot stream television without access to the Internet).

A talent strike across the entertainment industry could temporarily reduce content production and demand for some of the company’s offerings.

Cable TV is in secular decline, and this disproportionately harms the company: It hurts both the distribution (i.e., cable video) side of the business and the production (i.e., networks) side of the business.

Comcast also faces technological obsolescence risk, with competitors constantly trying to bring better, cheaper, and/or faster options to market (e.g., 5G wireless, LEO satellites).

The indebtedness limits the company’s future flexibility in terms of M&A and network buildouts.

Comcast also has a poor reputation for customer service.

I’d agree that these risks are fairly weighty, but offsetting them is the dominance and growth profile of the business.

Another aspect of the business that’s worth weighing is the valuation, which currently looks appealing…

Stock Price Valuation

The stock is trading hands for a P/E ratio of 11.5.

That’s based on TTM adjusted EPS.

I get it.

Comcast has some legacy issues and debt.

But that’s an awfully low earnings multiple.

It’s well off of not only the broader market but also the stock’s own five-year average P/E ratio of 18.1.

The P/CF ratio of 7 is also disconnected from its own five-year average of 7.7.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

That growth rate is on the higher end of my scale, but it’s not as high as I can go.

I’m backing it down in order to meet Comcast where it’s at.

We can see that both EPS and the dividend have grown at a double-digit pace over the last decade, which is great.

However, the last few dividend raises have been in this high-single-digit range.

And the near-term forecast for EPS growth is very close to this level.

I think a sober assessment of the go-forward dividend growth capability of Comcast, at least for the foreseeable future, is somewhere around 7% to 8% annually.

The DDM analysis gives me a fair value of $49.88.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I believe my valuation is reasonable, which still shows favorable pricing.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates CMCSA as a 5-star stock, with a fair value estimate of $60.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates CMCSA as a 4-star “BUY”, with a 12-month target price of $50.00.

I’m almost right on the button with where CFRA is at. Averaging the three numbers out gives us a final valuation of $53.29, which would indicate the stock is possibly 20% undervalued.

Bottom line: Comcast Corporation (CMCSA) is a dynamic media and entertainment conglomerate showing surprising strength and growth, despite popular sentiment around the business model. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 20% undervalued, long-term dividend growth investors looking for exposure to media ought to have their gaze in this direction.

Bottom line: Comcast Corporation (CMCSA) is a dynamic media and entertainment conglomerate showing surprising strength and growth, despite popular sentiment around the business model. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 20% undervalued, long-term dividend growth investors looking for exposure to media ought to have their gaze in this direction.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is CMCSA’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 89. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, CMCSA’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income