I live my life as a minimalist.

I own very few physical possessions.

That’s a good thing, too.

Seeing as how the apartment I live in is less than 400 square feet in size, it can’t fit much anyway.

However, when it comes to investing, I’m a maximalist.

What do I mean by that?

Well, I want maximum quality and quantity.

That is, I want to own a slice of some of the very best businesses in the world.

And since there are more than a small handful of them in existence, I’m happy to have as many as I can get my hands on.

How many of them are there?

Well, the Dividend Champions, Contenders, and Challengers list does a pretty good job of measuring that entire universe.

Every stock on that list is a dividend growth stock.

This list contains invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

As you might imagine, it’s not easy to pay out safe, growing dividends, year in and year out, like clockwork.

Only a great business that can keep racking up more and more profit by selling great products and/or services can do this.

Only a great business that can keep racking up more and more profit by selling great products and/or services can do this.

I own well over 100 of the world’s best businesses in my FIRE Fund.

That’s my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

In fact, this dividend income has been enough for me to live off of for a number of years now.

I was actually able to retire in my early 30s.

I was actually able to retire in my early 30s.

I explain exactly how I achieved such a thing in my Early Retirement Blueprint.

Suffice it to say, putting my hard-earned capital to work with wonderful businesses that pay reliable, rising dividends was key to my success.

But that’s not all.

Valuation at the time of investment is also very important.

Whereas price is what you pay, it’s value that you end up getting.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Dividend growth stocks that are undervalued often offer maximum quality at a minimum capital outlay.

Of course, finding these opportunities first requires one to be able to spot undervaluation, which in and of itself requires one to understand valuation.

Don’t worry.

My colleague Dave Van Knapp put together Lesson 11: Valuation for this purpose.

Part and parcel of a series of “lessons” that are designed to teach the A-Z of DGI, it spells out valuation and provides a simple-to-understand valuation template that can be applied toward almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Visa Inc. (V)

Visa Inc. (V)

Visa Inc. (V) is a multinational financial services corporation.

Founded in 1958, Visa is now a $485 billion (by market cap) digital payments giant that employs more than 26,000 people.

FY 2022 revenue breaks down across the following four segments: Data processing revenues, 49%; Service revenues, 46%; International transaction revenues, 33%; and Other revenues, 7%.

Client incentives, a contra-revenue item, which accounted for 35% of reported FY 2022 GAAP revenue, explains why the main four segments add up to more than 100%.

Visa runs a simple-to-understand business model, but this simplicity makes it no less powerful, beautiful, or compelling.

To the contrary, many of my best investments over the years have been with boringly simple businesses.

Essentially, Visa operates a global open-looped network that enables electronic payments for consumers, merchants, and governments.

Put simply, Visa facilities easy digital payments, collecting a small fee from every digital payment it processes.

Instead of cash, payments are able to easily and safely be handled by way of a Visa card (on Visa’s payment network).

In fact, Visa operates the largest such digital payments network in the world.

To put this in perspective, the company’s processing infrastructure, VisaNet, processes more than 600 million transactions per day.

The company is processing around $15 trillion in total volume annually.

Another mind-blowing number is 3.3 billion, which is approximately how many Visa cards are in global circulation.

It’s estimated that Visa has a 50% share of the global market, easily pinning it as the worldwide leader in digital payments.

What’s even more amazing is that, Visa might be just getting started.

Up until very recently, cash was still the dominant form of payment for global transactions.

Morningstar notes: “Digital payments, on a global basis, surpassed cash payments just a few years ago, suggesting this trend still has a lot of room to run.”

Since digital payments are superior to cash payments in almost every single way, it makes sense that cash is slowly being phased out.

That conversion from cash to cards bodes incredibly well for Visa – the company will likely continue to process the lion’s share of global payments.

Furthermore, with inflation recently running hot and causing the cost of almost everything to go up rather significantly, Visa’s fee base is rising in kind.

The annual rate of inflation in percentage terms has been slowing, but the new, higher cost base of almost everything is already firmly entrenched, which boosts Visa’s fees in absolute terms.

It’s a permanent “step up” for Visa.

All of this is why the company has such a long and wide runway for revenue, profit, and dividend growth.

Dividend Growth, Growth Rate, Payout Ratio and Yield

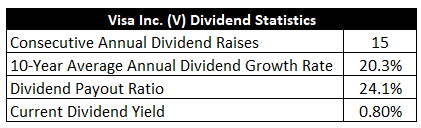

Already, Visa has increased its dividend for 15 consecutive years.

That dates back to Visa’s 2008 IPO.

The 10-year dividend growth rate is 20.3%, which is obviously exceptional.

But what’s especially exceptional about it is, there’s been no measurable slowdown.

The most recent dividend raise was 20%.

The most recent dividend raise was 20%.

Yet the payout ratio is only 24.1%.

That tells us two things.

First, we can surmise that much of this high-octane dividend growth has been fueled by similar earnings growth.

Otherwise, the payout ratio would already be very high.

Second, and related to the first point, it’s reasonable to expect this ~20% dividend growth rate to persist for a while longer.

It’s pretty clear that this is one of the safest and fastest-growing dividends out there.

Seeing as how the stock’s yield is only 0.8%, that’s good news.

Now, this yield is 20 basis points higher than its own five-year average.

Nonetheless, you really do want to see a higher dividend growth rate in order to make sense of a low yield like this.

For younger, longer-term dividend growth investors who love compounders, Visa is clearly very appealing.

Revenue and Earnings Growth

As appealing as these metrics may be, though, they are mostly looking backward.

However, investors must look forward, as today’s capital is being risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful when the time comes later to estimate its fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then uncover a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should allow us to approximate where the business could be going from here.

Visa advanced its revenue from $11.8 billion in FY 2013 to $29.3 billion in FY 2022.

That’s a compound annual growth rate of 10.6%.

Excellent top-line growth.

I usually look for a mid-single-digit top-line growth rate from a fairly mature business like this.

Visa knocked it out of the park.

Meanwhile, earnings per share grew from $1.90 to $7.00 over this period, which is a CAGR of 15.6%.

Superb.

A combination of margin expansion and share buybacks drove a lot of this excess bottom-line growth.

For perspective on the latter point, Visa reduced its outstanding share count by roughly 17% over this 10-year period.

Looking forward, CFRA is projecting an 18% CAGR for Visa’s EPS over the next three years.

I see nothing unreasonable about that.

This isn’t far off from what Visa has clearly proven to be capable of producing.

The pandemic disrupted Visa for a bit.

Of course, the pandemic was something that all businesses had to contend with, but Visa’s exposure to cross-border travel means that Visa took an outsized hit.

However, travel is on the mend and roaring back.

And all of the trends that work to Visa’s favor are firmly in place.

The cash-to-card conversion is going to be playing out for years to come.

And inflation has been a boon.

If, for example, something that would have cost $5.00 a few years ago now costs $6.00, Visa now collects a fee from a $6.00 transaction rather than a $5.00 transaction.

That’s automatically more fee revenue.

Yet Visa incurs no additional costs for the facilitation of the transaction.

The scalability is out of this world, and the business model is about as good as it gets when it comes to hedging inflation.

If we take CFRA’s forecast as the base case, that puts Visa in a great position to grow the dividend at a similar rate.

After all, the payout ratio is still quite low.

This perfectly circles back around to what I noted earlier about it being “reasonable to expect this ~20% dividend growth rate to persist for a while longer.”

Now, a while longer doesn’t mean forever.

At some point, Visa will have to start moderating the rate of dividend growth.

But I don’t think that point is on the horizon.

With the business and dividend growth at a rate of somewhere around 20% for the foreseeable future, you can easily start to picture an annualized total return somewhere in that same vicinity.

This is a stock that’s up more than 400% (before dividends) over the last 10 years alone.

Visa has been, is, and should continue to be a total return monster.

Financial Position

Moving over to the balance sheet, Visa maintains an extremely strong financial position.

The long-term debt/equity ratio is 0.6, while the interest coverage ratio is over 35.

Good numbers.

But they’re better than they look.

That’s because Visa has enough cash on the balance sheet to nearly wipe out all long-term debt.

Net debt is barely over $0.

Visa’s balance sheet, quite simply, is a fortress.

Profitability is outstanding.

Over the last five years, the firm has averaged annual net margin of 50.5% and annual return on equity of 38.9%.

Visa has some of the highest returns on capital of all businesses I’ve ever looked at.

From top to bottom, Visa is a world-class business that is operating at a very high level.

And with brand power, a huge network effect, built-out global infrastructure, global market share leadership, easy scalability on industry-leading scale, and high barriers to entry, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Regulatory headaches have been increasing for Visa.

On the other hand, seeing as how Visa operates within the favorable confines of a global oligopoly – there are only four large global payment networks – competition is limited.

Visa is exposed to broader economic trends, as its fee base is directly tied to global spending.

Any kind of recession would likely impact Visa.

Being a global payments operator, Visa naturally has exposure to geopolitics and different currencies.

The company’s large size is a risk, as the law of large numbers could start to be a drag on relative growth.

There’s technological risk present, and any major change in the way payments are handled would be a threat to Visa’s business model.

I don’t view these risks as too much to accept, especially when lined up against the immense quality of the business.

And with the valuation being modestly attractive right now, this could be a rare buying opportunity…

Stock Price Valuation

The stock’s P/E ratio is 32.4.

Is that egregious for one of the best businesses in the world?

I really don’t think so.

Keep in mind, this stock usually commands a hefty premium.

Its own five-year average P/E ratio is 35.6.

The P/S ratio of 16.5 is also below its own five-year average of 18.1.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 20% dividend growth rate for the next ten years, and a long-term dividend growth rate of 8%.

These are, admittedly, aggressive numbers.

But if there’s any business that deserves the benefit of the doubt, it’s Visa.

The demonstrated long-term dividend growth rate is approximately 20%.

The most recent dividend increase came in at 20%.

We can see a near-term forecast for underlying EPS growth at nearly 20%.

The payout ratio is very low.

And the balance sheet is stellar.

Visa may not grow the dividend at exactly 20% over the next decade, but it’s also quite possible that this elevated state of dividend growth exists for a period that extends well beyond the next decade.

Overall, Visa is one of the best businesses I’ve ever seen, and I don’t think high expectations are unreasonable.

The DDM analysis gives me a fair value of $262.00.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I see the stock as modestly undervalued, which jibes well with the disconnects in the various multiples.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates V as a 3-star stock, with a fair value estimate of $241.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates V as a 4-star “BUY”, with a 12-month target price of $272.00.

A decently tight range here. Averaging the three numbers out gives us a final valuation of $258.33, which would indicate the stock is possibly 6% undervalued.

Bottom line: Visa Inc. (V) is a world-class business with high returns on capital and a fortress-like balance sheet. And it’s benefiting from one of the strongest secular trends out there. With a competitive yield, a double-digit dividend growth rate, a very low payout ratio, 15 consecutive years of dividend increases, and the potential that shares are 6% undervalued, long-term dividend growth investors who want to own a slice of one of the best businesses on the planet ought to be taking a close look at this one.

Bottom line: Visa Inc. (V) is a world-class business with high returns on capital and a fortress-like balance sheet. And it’s benefiting from one of the strongest secular trends out there. With a competitive yield, a double-digit dividend growth rate, a very low payout ratio, 15 consecutive years of dividend increases, and the potential that shares are 6% undervalued, long-term dividend growth investors who want to own a slice of one of the best businesses on the planet ought to be taking a close look at this one.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is V’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, V’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income