For the vast majority of people, long-term investing is the most realistic path to wealth. Unique skills that can produce a lot of money are rare. But investing is available to all of us. And when talking about investing, I’d argue that dividend growth investing is the best long-term investment strategy of all.

High-quality dividend growth stocks represent equity in world-class businesses that pay reliable, rising dividends to shareholders.

These are some of the best stocks in the world.

That’s because they represent equity in some of the best businesses in the world. After all, the only way to fund ever-rising dividends is to produce the ever-rising profits necessary to afford that behavior. And only truly great businesses can produce ever-rising profits.

That said, your age is an important consideration. Investing at 20 isn’t necessarily like investing at 60. There are differences in aspects like time horizon, risk tolerance, income needs, etc.

If you’re in your 20s, you should be very concerned about growth of your assets. That’s because you have decades ahead of you to let that compounding process play out.

So if you’re in your 20s, it could make a lot of sense to focus on high-quality dividend growth stocks that offer high growth rates, even if the yields are low. You want to focus on extremely long-term trends that can unfold over decades. This can allow you to rack up an excellent long-term total return and a ton of aggregate dividend income.

Today, I want to tell you about 3 dividend growth stocks to consider buying if you’re in your 20s.

Ready? Let’s dig in.

The first dividend growth stock I want to highlight today is Microsoft (MSFT). Microsoft is an American multinational technology corporation.

This is one of the most successful businesses on the planet. And I mean that in every possible sense. From profitability to growth to the balance sheet, Microsoft is a stunning example of what capitalism can produce. How could you not want a company like this working for you? Technology is almost certainly going to become a bigger part of our lives in the future.

Can you imagine society using less technology in 10 or 20 years? Right. Me neither. Microsoft caters to this. It’s a pie that’s getting bigger. And Microsoft is claiming a bigger portion of it. I mentioned trends earlier. Well, Microsoft is majorly involved in cloud, software, gaming, and now even AI. If you believe in the future of any of this, you almost have to believe in the future of Microsoft.

Can you imagine society using less technology in 10 or 20 years? Right. Me neither. Microsoft caters to this. It’s a pie that’s getting bigger. And Microsoft is claiming a bigger portion of it. I mentioned trends earlier. Well, Microsoft is majorly involved in cloud, software, gaming, and now even AI. If you believe in the future of any of this, you almost have to believe in the future of Microsoft.

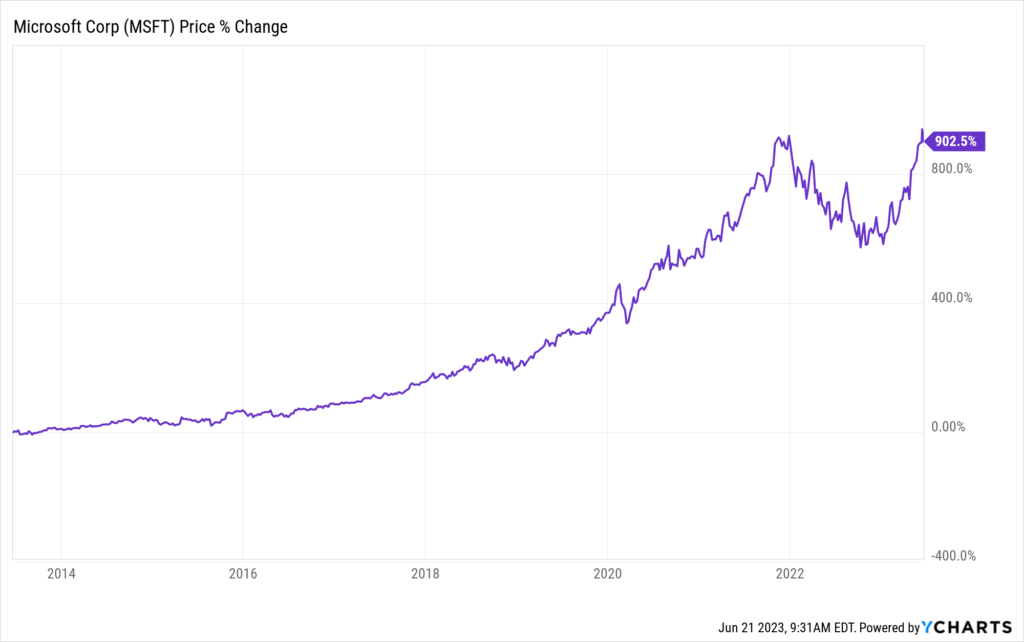

Microsoft is a compounding machine. If you’re a young investor, you should be looking for those long-term compounders. Well, Microsoft is Exhibit A. This stock has compounded at an annual rate of just under 28% over the last 10 years alone, which is incredible.

Using the Rule of 72, that kind of CAGR doubles your money every 2.5 years. Just imagine doubling your money every three years or so. You can become very wealthy like that. Now, Microsoft is big. $2.6 trillion market cap big. But it should be big.

You don’t do this much this well and not get big. That said, it continues to be a very, very strong performer, despite its large size being a possible headwind in some ways.

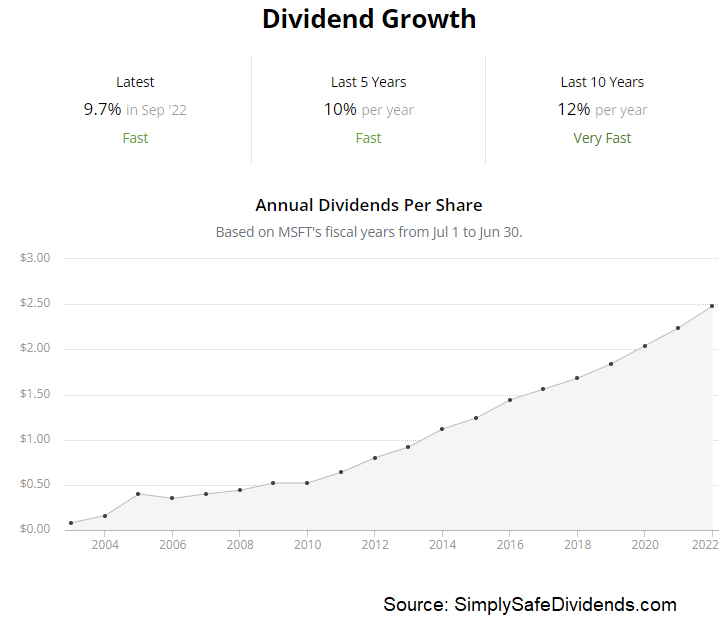

That goes for the dividend, too. Microsoft has grown its dividend for 21 consecutive years. The company is on pace to become a Dividend Aristocrat in a few years.

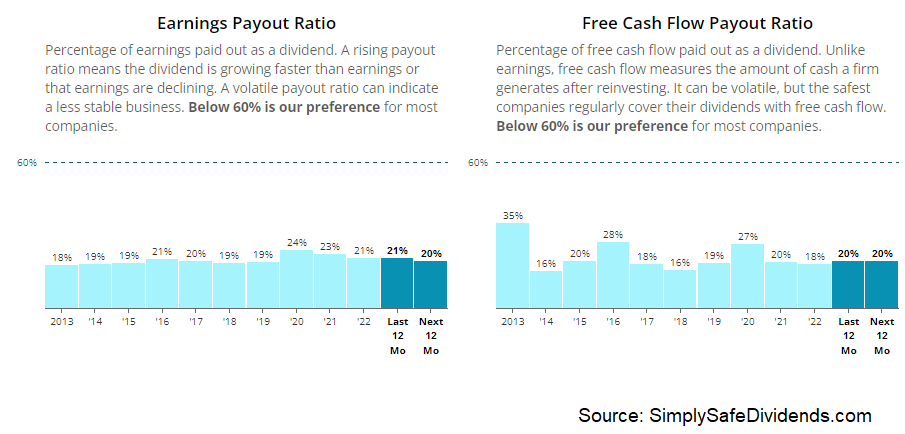

The 10-year DGR is 11.8%. No signs of a big slowdown, either. The most recent dividend raise was almost 10%. Now, the stock yields only 0.8%. But if you’re in your 20s, you’re not living off of dividends anyway. You should be thinking about where things will be in 20 or 30 years. To that point, the payout ratio here is just 29.5%.

The 10-year DGR is 11.8%. No signs of a big slowdown, either. The most recent dividend raise was almost 10%. Now, the stock yields only 0.8%. But if you’re in your 20s, you’re not living off of dividends anyway. You should be thinking about where things will be in 20 or 30 years. To that point, the payout ratio here is just 29.5%.

Plus, Microsoft has a stellar balance sheet. One of only two US companies with a AAA credit rating from S&P. This dividend is as safe as it gets. The valuation is elevated. But if you have a time horizon of 40 years, it’s all about business performance.

No business is worth unlimited money. Valuation does matter. But I’ve noticed way too many people thinking way too much about valuation and way too little about the quality of a business. Over the long run, it’s the latter, not the former, that will have the most to say about your results.

This stock’s P/E ratio of 37.6 is challenging for those who are thinking about the next year or two. But you know what? I’ve been hearing about how expensive Microsoft stock is for years and years. And yet all it’s doing is making the owners rich while the complainers keep missing out. If I’m in my 20s, I’m definitely looking at this world-class enterprise here.

The second dividend growth stock I want to bring to your attention is Visa (V). Visa is a multinational financial services corporation. Another extremely high-quality business here.

Visa essentially operates within the comfy confines of a duopoly when it comes to global digital payment networks. That means limited competition. And since there’s an ongoing shift away from cash and toward digital payments, this is yet another example of a pie that’s growing.

Huge secular trend here that you should be interested in being a part of. In many parts of the world, cash is still the dominant form of payment for transactions. But that is changing. The pandemic only accelerated this change.

This change bodes well for Visa, since the company collects a percentage of the value of every transaction that occurs over its global network. Plus, with inflation causing the cost of just about everything to rise by quite a bit over the last few years, Visa’s revenue rises in tandem.

This is an impressive business. Sky-high returns on capital. Net margin routinely coming in at over 50%. Clean balance sheet. It hits all the hallmarks of a high-quality business. The compounding prowess here is nothing less than extraordinary.

The stock is up by more than 400% over the last decade alone, before factoring in the dividend. Suffice it to say, quintupling your money inside of a decade isn’t bad. And with cash still making up the majority of payments globally, there’s a long runway for plenty more where that came from.

Visa is a dividend growth monster. Visa has increased its dividend for 15 consecutive years. The 10-year DGR is 20.3%. Huge. Now, the yield is only 0.8%. But guess what? The yield has been in that 0.8% or so range for years and years.

Visa is a dividend growth monster. Visa has increased its dividend for 15 consecutive years. The 10-year DGR is 20.3%. Huge. Now, the yield is only 0.8%. But guess what? The yield has been in that 0.8% or so range for years and years.

What’s happening is that, even though Visa keeps increasing the dividend aggressively each year, the stock price keeps rising, which puts a lid on the yield – price and yield are, after all, inversely correlated. This is exactly the kind of situation you want.

You don’t want some high-yield junk stock that keeps cutting the dividend, where the stock price keeps falling and allows the yield to keep rising. With Visa’s payout ratio being at only 24.1%, I’m highly confident of more double-digit dividend growth ahead for Visa.

The stock commands a premium valuation. But it’s done so for as long as I’ve been investing. If I listened to the naysayers, who only chase after lowly-valued, high-yield stocks – which tend to be junk investments, by the way – I never would have invested in Visa in 2014. A lot of people thought I paid too much.

The stock commands a premium valuation. But it’s done so for as long as I’ve been investing. If I listened to the naysayers, who only chase after lowly-valued, high-yield stocks – which tend to be junk investments, by the way – I never would have invested in Visa in 2014. A lot of people thought I paid too much.

Yet I’ve more than quadrupled my money. Visa’s P/E ratio right now is 30.6. And, you know, that’s pretty similar to what it was when I invested in Visa nine years ago. I suspect it’ll be a similar story nine years from now. Keep in mind, its own five-year average P/E ratio is 35.7. By its own standards, it’s actually not expensive at all. And when looking at the growth, I don’t see the current valuation as unreasonable. If you truly have a multidecade type of time horizon, fussing over a P/E ratio on a world-class business is a poor approach anyway. If you’re a younger, long-term dividend growth investor, Visa is something you have to be looking at.

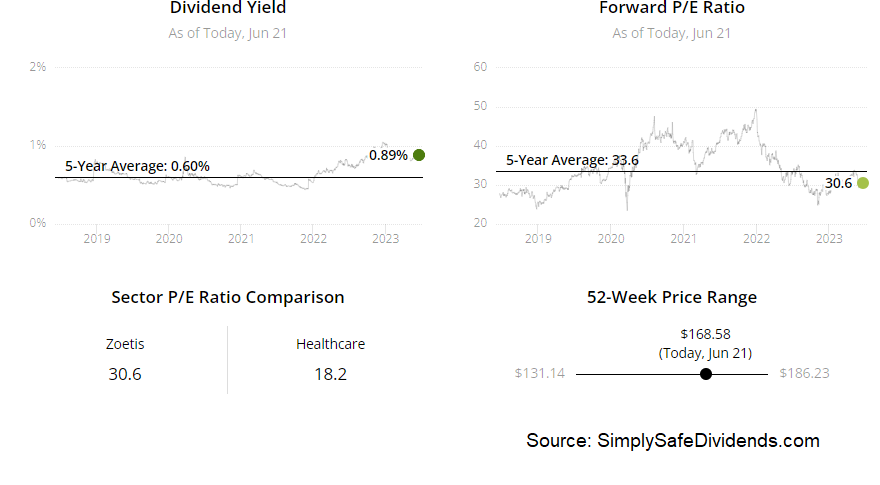

The third dividend growth stock we have to talk about today is Zoetis (ZTS). Zoetis is a producer of medicine and vaccinations for pets and livestock. Zoetis is the largest business of its kind in the world. And what a great space to be in. People care for their pets dearly. In fact, some people treat their pets better than they treat other human beings.

This is another secular trend with no end in sight. It’s also another example of something that was already occurring but was accelerated by the pandemic.

Millions of households in the US alone adopted pets during the pandemic. These people aren’t all going to suddenly relinquish these pets. And what will these pets need over the course of their lives? Care, including vaccines and medicines, which plays right into the hands of Zoetis.

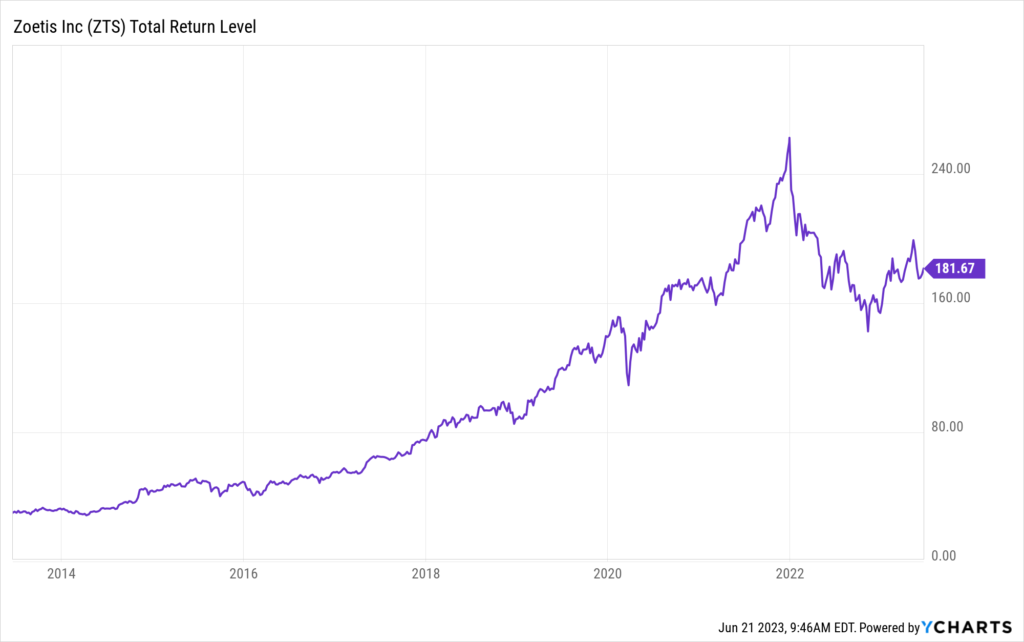

Zoetis is a terrific business that’s making its shareholders rich over time. The stock has compounded at an annual rate of slightly over 19% over the last ten years. That kind of rate of compounding would take an initial sum and nearly 6x it over that time frame.

Zoetis is a terrific business that’s making its shareholders rich over time. The stock has compounded at an annual rate of slightly over 19% over the last ten years. That kind of rate of compounding would take an initial sum and nearly 6x it over that time frame.

If every business you invest in can 6x your money every 10 years, trust me, you’re going to become very, very wealthy in time. Of course, not every business can do that. It takes a special kind of business, which is why we’re sitting here talking about three very special businesses today.

Speaking of special, this dividend growth story is special. Zoetis has increased its dividend for 11 consecutive years, dating back to its 2013 spin-off from Pfizer (PFE). The five-year DGR is 25.4%. Wow. Just wow.

The 0.9% yield is less wow-worthy, but that’s the kind of yield you tend to get with a high-quality compounder like Zoetis. Besides, if you’re young, you shouldn’t be focusing so much on yield anyway. We have yet another low payout ratio – notice a trend yet? – of 33.9%. Plenty of leeway for the dividend to head higher.

Is Zoetis cheap? No. Should it be cheap? No. This is a premium business with a premium valuation. As I’ve said many times before, you don’t get diamonds for the price of cubic zirconias. That’s not how the world works.

The P/E ratio of 38.6 looks high… until you compare it to the stock’s own five-year average P/E ratio of 42.5. And what does this tell you? Despite Zoetis frequently having a sky-high earnings multiple, it’s still compounded at a high rate and made its owners a ton of money. Zoetis is still not a huge company – its market cap is under $80 billion. And pet care isn’t going anywhere. If you’re young and have the time for compounding to do its magic, Zoetis is a very compelling long-term investment idea.

The P/E ratio of 38.6 looks high… until you compare it to the stock’s own five-year average P/E ratio of 42.5. And what does this tell you? Despite Zoetis frequently having a sky-high earnings multiple, it’s still compounded at a high rate and made its owners a ton of money. Zoetis is still not a huge company – its market cap is under $80 billion. And pet care isn’t going anywhere. If you’re young and have the time for compounding to do its magic, Zoetis is a very compelling long-term investment idea.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income