Charlie Munger is one of the greatest investors of all time.

Serving as Warren Buffett’s right-hand man for decades, Munger has dropped countless nuggets of wisdom over the years.

One of his best insights?

Munger has noted how Berkshire Hathaway Inc. (BRK.B) spawned from a doomed department store, a doomed New England textile company, and a doomed trading stamp company.

What does this tell us?

It tells us that we’ll all have losers.

Even the greats have plenty.

Even the greats have plenty.

The key is to foster and protect the winners.

How do we do this?

Well, as Munger would also say, we go and fish where the fish are.

In the spirit of this, I’m a huge advocate of high-quality dividend growth stocks.

These stocks represent equity in world-class businesses that pay reliable, rising dividends to their shareholders.

Reliable, rising dividends are able to be funded when reliable, rising profits are generated.

And reliable, rising profits are generated when businesses are run extremely well and sell the great products and/or services the world demands.

You can find hundreds of these stocks on the Dividend Champions, Contenders, and Challengers list.

This list has compiled valuable metrics on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

I put my money where my mouth is, as I’ve been personally buying high-quality dividend growth stocks for more than a decade now.

Doing so has allowed me to build the FIRE Fund.

That’s my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

Indeed, I’ve been fortunate enough to live off of dividends since I quit my job and retired in my early 30s.

I was able to retire so early in life mostly by consistently living below my means and intelligently investing my capital, as I describe in my Early Retirement Blueprint.

Of course, there’s more to it than just buying the right stocks.

Of course, there’s more to it than just buying the right stocks.

There’s also the very important matter of valuation.

Price only tells you what you pay, but it’s value that tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying high-quality dividend growth stocks when they’re undervalued and then holding them for the long run is a great way to heed Munger’s advice.

Now, this does mean that one has to be somewhat familiar with valuation as a concept.

Fear not.

My colleague Dave Van Knapp put together Lesson 11: Valuation for those that need initiation.

Part and parcel of a series of “lessons” on dividend growth investing, it lays out a valuation template that can be easily understood and applied in order to estimate the fair value of just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Travelers Companies Inc. (TRV)

Travelers Companies Inc. (TRV)

Travelers Companies Inc. (TRV) is a holding company that, through its subsidiaries, provides commercial and personal property and casualty insurance products to individuals, businesses, government units, and associations.

Founded in 1853, Travelers is now a $40 billion (by market cap) insurance major that employs more than 32,000 people.

Net written premiums for FY 2022 break down across the following segments: Business Insurance, 50%; Personal Insurance, 40%; and Bond & Specialty Insurance, 10%.

Travelers is the only P&C insurance company in the Dow Jones Industrial Average.

This is truly a blue-chip company.

I really like this business model.

See, most business models make money by selling products and/or services.

The insurance business model takes this a step further – making money from its core service many times over.

This is due to the “float”.

The float is the capital that builds up as a natural course of doing business.

An insurance company charges premiums up front for coverage.

Claims against policies come in later, at which time an insurance company has to pay out.

The lag between collecting premiums and paying claims often leads to an insurance company sitting on a lot of cash – which is a low-cost and low-risk source of capital that earns returns all by itself.

That’s the float.

For perspective on just how powerful this can be, Travelers manages an investment portfolio with a carrying value of $86.7 billion (as of the end of FY 2022).

The investment portfolio is more than twice as large as the company’s entire market cap.

As you might imagine, this kind of capital base can produce a lot of income for a company.

Indeed, Travelers reported just over $2.8 billion in net income last fiscal year.

Well, the investment portfolio was responsible for almost all of that, with net investment income (after-tax) coming in at slightly under $2.2 billion for FY 2022.

The float is what makes the insurance business model so lucrative.

It’s easy to assume that an insurance company makes money by selling insurance.

The truth is that most of the money is made by properly utilizing the float.

Just imagine if every company could collect money for its products and/or services long before customers actually get what they paid for!

Travelers almost can’t help but continue to churn out money, even if premiums aren’t strong.

This is why the company should be able to continue growing its revenue, profit, and dividend for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

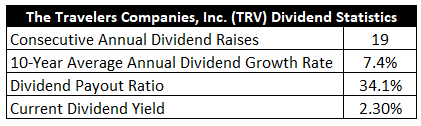

Already, Travelers has increased its dividend for 19 consecutive years.

Well on its way to Dividend Aristocrat status.

The 10-year dividend growth rate is 7.4%.

Travelers has been a model of consistency in this department, as the dividend raises have been extremely uniform over the years.

In fact, the most recent dividend raise of 7.5% was basically right on the nose.

Along with that high-single-digit dividend growth, the stock offers a market-beating 2.3% yield.

This yield, by the way, is right in line with its own five-year average.

This yield, by the way, is right in line with its own five-year average.

And the dividend is protected by a low payout ratio of only 34.1%.

I see clear sailing ahead for Travelers and its ability to continue raising the dividend at a high-single-digit rate.

Great dividend metrics here, especially for conservative dividend growth investors.

Revenue and Earnings Growth

As great as these metrics may be, though, they’re mostly looking into the past.

However, investors must look into the future, as today’s capital is being risked for tomorrow’s rewards.

That’s precisely why I’ll now build out a forward-looking growth trajectory for the business, which will be instrumental when the time comes to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then unveil a professional prognostication for near-term profit growth.

Deftly fusing the proven past with a future forecast in this manner should allow us to roughly judge where the business might be going from here.

Travelers moved its revenue from $26.1 billion in FY 2013 to $36.9 billion in FY 2022.

That’s a compound annual growth rate of 3.9%.

Pretty much right where I’d expect it to be for a fairly mature P&C insurance business.

Meanwhile, Travelers grew its earnings per share from $9.74 to $11.77 over this period, which is a CAGR of 2.1%.

On the face of it, that’s a disappointing number.

However, with an insurance business, much depends on the starting point and ending point.

And that’s because of events that may happen, or may not happen, that can radically alter claims, the combined ratio, and profit.

In this case, FY 2013 was an unusually strong year for Travelers, with EPS up 55% from FY 2012.

At the same time, FY 2022 was a somewhat weak year for the business.

If we back up the 10-year comparison by just one year at the starting point and ending point, the EPS CAGR is over 9%.

Thus, I’d take the 2.1% number with a big grain of salt.

It’s worth quickly noting that Travelers has been an extraordinary repurchaser of shares, with the outstanding share count down by about 32% over the last decade.

Looking forward, CFRA believes that Travelers will compound its EPS at an annual rate of 8% over the next three years.

This would be more in line with what Travelers has historically generated.

I think this is a pretty accurate reflection of reality for the business.

CFRA states that its “forecast assumes that underwriting results remain profitable, and that [Travelers]’s prior year loss development trends remain positive. Results in 2022 reflected a 2% rise in an already elevated level of after-tax catastrophe losses, offset by a significant improvement in prior-year loss development trends.”

Building on that point, Travelers ended FY 2022 with a combined ratio of 95.6%.

The combined ratio is a measurement of an insurance company’s underwriting profit.

In order to ascertain it, you divide the total sum of incurred losses and expenses by the earned premium.

The lower the combined ratio, the better.

Travelers ended FY 2021 with a combined ratio of 94.5%, so you can see some erosion here in underwriting efficiency, and that speaks on what I noted earlier about FY 2022 being a somewhat poor year for the business.

With P&C insurance, you have to accept some uncertainty and lumpiness as a natural course of doing business.

After all, catastrophes are unpredictable.

It’s really the long-term trends that matter most.

As long as you don’t become irrational with underwriting, and as long as the float is managed properly, the business model can do very well over the long run.

I don’t see anything unrealistic about where CFRA is at with Travelers here.

And if that’s the base case, it sets up the dividend for like dividend growth.

That is, an expectation for a continuation of the status quo – high-single-digit dividend growth – is a reasonable one.

When one is already starting off with a 2%+ yield, that puts shareholders in a pretty good position for a ~10% annualized total return, assuming no major changes with valuation.

Getting that kind of total return with a conservative, blue-chip dividend growth stock is compelling, in my view.

Moving over to the balance sheet, Travelers has a solid financial position.

The long-term debt/equity ratio is 0.3, while the interest coverage ratio is approximately 10.

The credit ratings are well into investment-grade territory.

Financial Position

The company’s senior debt has the following ratings: A, Standard & Poor’s; A2, Moody’s; A, Fitch.

Profitability is good.

Over the last five years, the firm has averaged annual net margin of 8.6% and annual return on equity of 11.1%.

Travelers is running a tight ship and earns its blue-chip status.

And with brand recognition, scale and diversification that spread out risk, underwriting expertise, and the established float, Travelers does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Competition, in particular, is a risk in insurance, as it can pressure insurers on the underwriting side.

Natural disasters, which are impossible to predict with 100% accuracy, are a constant threat.

The company’s investment portfolio is mostly in fixed-income instruments that have exposure to interest rates and government solvencies.

The very business model in and of itself is a risk, and an uncertain one at that, as it’s only in the future that shareholders may find out that underwriting policies of the past weren’t appropriately priced.

Recent slippages in the combined ratio will have to be rectified.

Overall, I see these risks as pretty standard for a P&C insurer, but the company’s standing is definitely far and above standard.

And with the stock down about 8% this year, the valuation has moved beyond standard and looks appealing…

Stock Price Valuation

The stock is trading hands for a P/E ratio of 14.7.

That’s significantly below the broader market’s earnings multiple.

And while it’s pretty close to the stock’s own five-year average P/E ratio, this stock had its pricing depressed for a considerable period of time during the pandemic, which skews the averages.

The P/B ratio of 1.7 is quite reasonable for a world-class insurance operation.

And the yield, as noted earlier, is basically right in line with its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

This growth rate is at the higher end of what I allow for, but the consistent nature of this business gives me confidence.

In spite of the lumpiness of underlying profits, Travelers raises its dividend in a machine-like way.

The dividend relentlessly rises by about 7.5% or so, year after year.

It’s a beautiful thing to behold.

And with CFRA seeing Travelers producing an 8% CAGR in its EPS over the next few years, that should open the door for Travelers to keep doing what Travelers has been doing.

Everything just fits into place really nicely here.

You can easily imagine the glide path in place.

It’s not an exciting business, but Travelers really does get the job done.

The DDM analysis gives me a fair value of $172.00.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I basically see Travelers as reasonably valued, albeit not optically cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates TRV as a 4-star stock, with a fair value estimate of $194.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates TRV as a 4-star “BUY”, with a 12-month target price of $205.00.

I came out pretty low this time around, which surprises me. Perhaps I was too cautious. Averaging the three numbers out gives us a final valuation of $190.33, which would indicate the stock is possibly 9% undervalued.

Bottom line: Travelers Companies Inc. (TRV) is a business that has shown a remarkable amount of consistency over the years. It’s a blue-chip stock. With a market-beating yield, a high-single-digit dividend growth rate, a low payout ratio, nearly 20 consecutive years of dividend increases, and the potential that shares are 9% undervalued, conservative dividend growth investors looking for a great business at a reasonable valuation should have this name on their list.

Bottom line: Travelers Companies Inc. (TRV) is a business that has shown a remarkable amount of consistency over the years. It’s a blue-chip stock. With a market-beating yield, a high-single-digit dividend growth rate, a low payout ratio, nearly 20 consecutive years of dividend increases, and the potential that shares are 9% undervalued, conservative dividend growth investors looking for a great business at a reasonable valuation should have this name on their list.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is TRV’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 78. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, TRV’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income