Is there anything better than dividend growth investing? I mean, we’re talking about having some of the best businesses in the world go to work for you.

These companies are duking it out in the brutal gauntlet that is capitalism, doing all they can to get bigger and better. And what do you have to do?

Simply identify the great businesses, buy shares, and then hold. And for that “hard work”, you get rewarded with ever-higher dividends, funded by ever-higher profits. Want to see this in action? Well, that’s what today’s article is all about.

Today, I want to tell you about 6 dividend growth stocks that just increased their dividends.

Ready? Let’s dig in.

The first dividend increase I have to tell you about is the one that was announced by Bank of New York Mellon (BK). Bank of New York Mellon just increased its dividend by 13.5%.

Inflation was running hot for a bit. But it’s cooling way off. Meanwhile, Bank of New York Mellon’s dividend growth is just getting heated up. This is one of the bank’s largest dividend increases ever. So much for banking issues, right? The global financial services company has now increased its dividend for 13 consecutive years.

With a 10-year DGR of 10.6%, a yield of 3.8%, and this recent dividend boost of nearly 14%, we have some gobsmacking numbers for dividend growth investors. I know. Banks aren’t en vogue. I get it. But that might be precisely the reason why one should be taking a look at this institution right now.

With a 10-year DGR of 10.6%, a yield of 3.8%, and this recent dividend boost of nearly 14%, we have some gobsmacking numbers for dividend growth investors. I know. Banks aren’t en vogue. I get it. But that might be precisely the reason why one should be taking a look at this institution right now.

With a payout ratio of 53.2%, this new, upsized dividend is easily covered. These are surprisingly great metrics. Unlike most other banks, this name has held up really well this year. Despite that, it’s still inexpensive.

Bank of New York Mellon is not your typical commercial bank. We’re not talking about savings and loans here. This is the largest global custody bank in the world, with over $46 trillion in assets under custody and administration.

And because of that massive differentiation, the stock hasn’t been hit in the same way a lot of other bank stocks have. It’s only down 4% this year. Still, all basic valuation metrics here are undemanding, including the P/E ratio of 14.1 and the P/B ratio of 1. If you’re looking for a bank that isn’t a bank, and you want a fairly high yield at an inexpensive valuation, Bank of New York Mellon is worth a good look.

And because of that massive differentiation, the stock hasn’t been hit in the same way a lot of other bank stocks have. It’s only down 4% this year. Still, all basic valuation metrics here are undemanding, including the P/E ratio of 14.1 and the P/B ratio of 1. If you’re looking for a bank that isn’t a bank, and you want a fairly high yield at an inexpensive valuation, Bank of New York Mellon is worth a good look.

The second dividend increase I have to bring to your attention is the one that came courtesy of Caterpillar (CAT). Caterpillar just increased its dividend by 8.3%.

Big yellow coming through with some big green. As in, money. And, you know, that’s exactly what Caterpillar has been doing for years and years now. This is the 30th consecutive year of dividend increases for the manufacturer of construction and mining equipment.

That makes Caterpillar a vaunted Dividend Aristocrat. What makes this so impressive is the fact that we’re talking about a heavy machinery manufacturer, which is a business model that is prone to extreme ups and downs through the economic cycles.

That makes Caterpillar a vaunted Dividend Aristocrat. What makes this so impressive is the fact that we’re talking about a heavy machinery manufacturer, which is a business model that is prone to extreme ups and downs through the economic cycles.

I think that goes to show just how consistently great and committed to shareholders this business has been over the years. The 10-year DGR is 9%, so we’re basically right on the mark here. Again, it’s remarkable consistency. The stock yields 2.1%, which is respectable. And the payout ratio is only 38.5%. If there is any kind of downturn on the horizon, there’s a lot of cushion in place. This stock is up 40% over the last year. And that has pushed up the valuation.

Now, I don’t think that Caterpillar’s stock is egregiously overvalued. However, on the flip side, it also doesn’t look cheap, either. Most metrics are pretty close to their respective recent historical averages. The P/E ratio of 18.2, for instance, isn’t far off from its own five-year average of 19.7. The sales multiple of 2.1 is slightly ahead of its own five-year average of 1.9. I’d like to see a pullback. But this is a prime example of a wonderful business trading for a fair price.

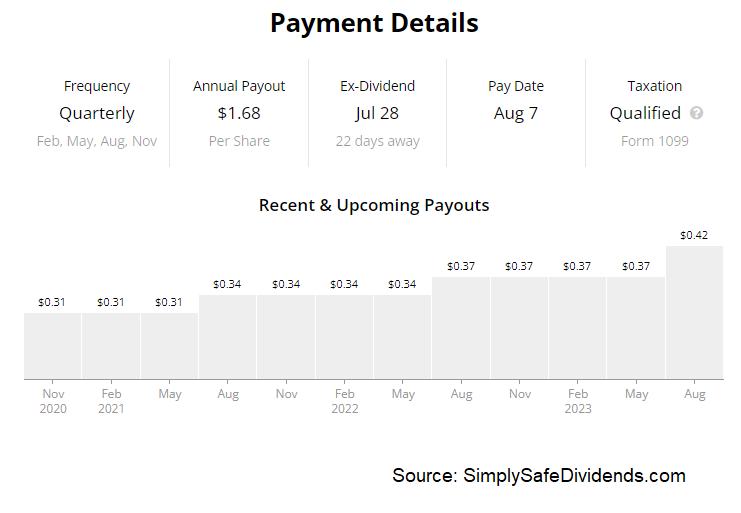

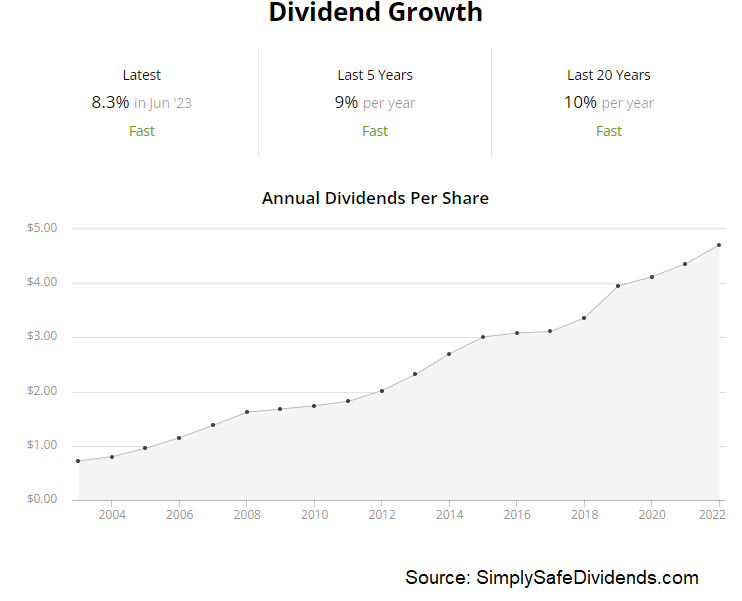

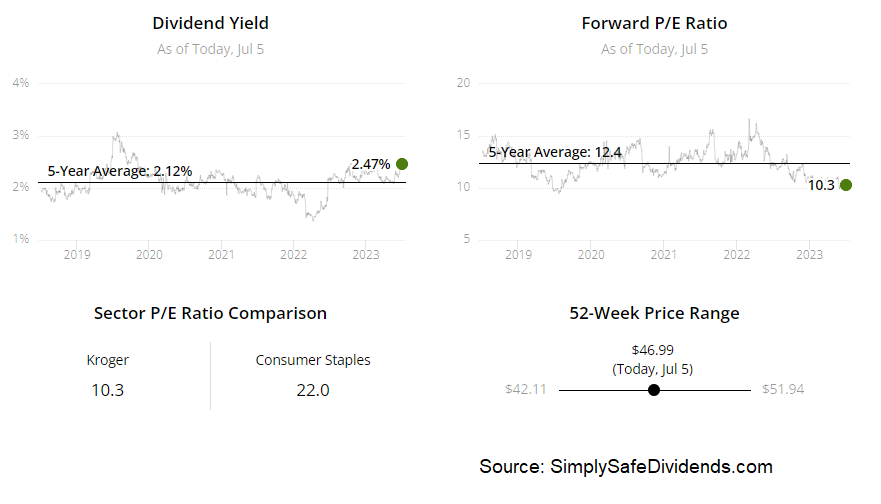

The third dividend increase we have to have a quick conversation about is the one that came in from Kroger (KR). Kroger just increased its dividend by 11.5%.

Wow. Another double-digit dividend dividend increase? What’s up with that? Well, we have great businesses doing what great businesses do. All shareholders have to do is kick back, relax, and enjoy the higher stream of passive income. This marks the 18th consecutive year of dividend increases for the supermarket chain.

The 10-year DGR is 14.3%. So we’re a bit lower than that with this year’s dividend raise. But one can forgive Kroger, considering the fact that last year’s dividend raise came in at nearly 24%. It all averages out. Meantime, the stock offers up a 2.5% yield – 50 basis points higher than its own five-year average. And a payout ratio of 33.3% shows us what a healthy dividend it is. If you like ‘em cheap, Kroger has your name on it.

This is a lowly-rated stock right across the board. Now, that’s probably deserved in many ways. This is, after all, a low-margin business operating in a mature, competitive market. It should have low multiples. And that’s what you get. The sales multiple is only 0.2. The P/E ratio of 13.5 is under its own five-year average of 14.5. Kroger isn’t exciting. And I like to see higher returns on capital. But it’s unlikely to seriously disappoint in any way. There’s just nothing demanding here. It’s hard to go wrong.

This is a lowly-rated stock right across the board. Now, that’s probably deserved in many ways. This is, after all, a low-margin business operating in a mature, competitive market. It should have low multiples. And that’s what you get. The sales multiple is only 0.2. The P/E ratio of 13.5 is under its own five-year average of 14.5. Kroger isn’t exciting. And I like to see higher returns on capital. But it’s unlikely to seriously disappoint in any way. There’s just nothing demanding here. It’s hard to go wrong.

The fourth dividend increase I want to bring up is the one that was announced by Morgan Stanley (MS). Morgan Stanley just increased its dividend by 9.7%. Nearly 10% more passive dividend income for doing nothing other than not selling shares. How can you complain? That’s so easy, even I can do it.

This is the 10th consecutive year of dividend increases for the multinational investment bank and financial services company. We have the makings of a lovely dividend growth story here. Morgan Stanley’s five-year DGR is 26.8%, which is obviously excellent, but, unsurprisingly, it has slowed down of late.

Last year’s dividend raise was in the 10% range, as is this year’s. But a 10% dividend growth rate is nothing to wag your finger at, especially since the stock also offers a stunning 3.9% yield. That yield is up there in REIT territory, and it’s 120 basis points higher than its own five-year average. It’s an incredible combination of yield and growth. And a 58.4% payout ratio supports this lovely story.

Last year’s dividend raise was in the 10% range, as is this year’s. But a 10% dividend growth rate is nothing to wag your finger at, especially since the stock also offers a stunning 3.9% yield. That yield is up there in REIT territory, and it’s 120 basis points higher than its own five-year average. It’s an incredible combination of yield and growth. And a 58.4% payout ratio supports this lovely story.

This stock has lagged the broader market this year, and it could be due for a big catch-up. There is nothing unreasonable about Morgan Stanley’s valuation. The earnings multiple is below 15. The P/B ratio is 1.6. Morgan Stanley doesn’t have to knock it out of the park. It just has to avoid driving into the ditch. We last analyzed and valued Morgan Stanley late in 2022, estimating intrinsic value for the business at almost $100/share. The stock is currently priced at right about $86. Could be some very decent upside here. And you’re collecting a near-4% yield in the meantime. Not bad at all.

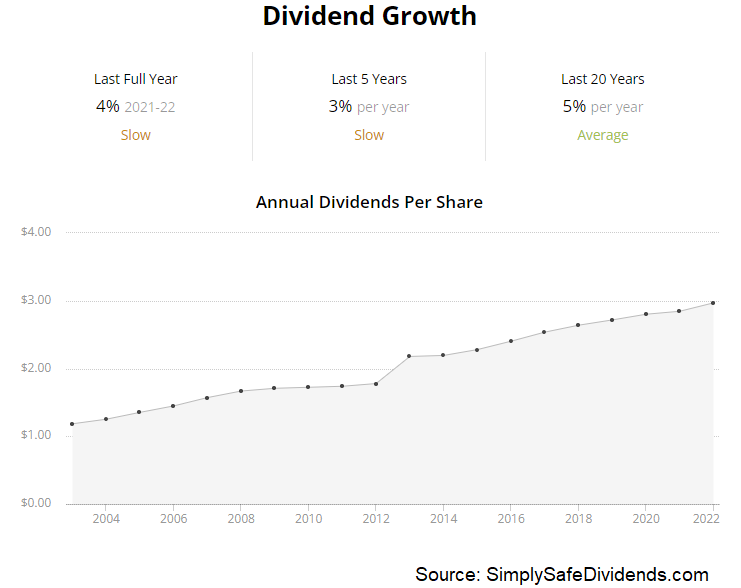

The fifth dividend increase that we have to go over is the one that occurred from Realty Income (O). Realty Income just increased its dividend by 0.2%. 0.2%? What’s up with that? Why even mention it?

Well, it’s just another feather in Realty Income’s cap, which is a cap that is about as consistent as it gets. See, this company tends to increase its dividend multiple times per year. Already, the dividend is up 2.8% YTD. And we’re only halfway through 2023.

The real estate investment trust has increased its dividend for 30 consecutive years. Realty Income is a Dividend Aristocrat. One of the very few REITs that can claim such status. Again, it’s all about consistency here. Speaking of consistent, Realty Income pays its dividend monthly.

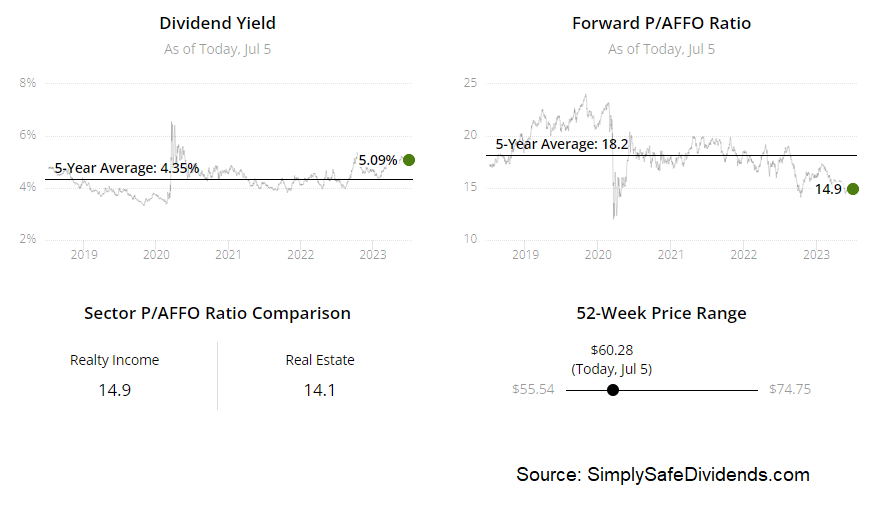

The 10-year DGR is 5.3%, and we’re on pace for something just like that in 2023. I mean, it’s just one check mark after another here. The stock yields 5.1%, which is appealing, even in this environment. And the payout ratio of 74.8%, based on this fiscal year’s FFO/share guidance, is right about where it should be and has been. You don’t get much more consistent than this. One thing that’s not consistent? The stock’s performance this year.

The 10-year DGR is 5.3%, and we’re on pace for something just like that in 2023. I mean, it’s just one check mark after another here. The stock yields 5.1%, which is appealing, even in this environment. And the payout ratio of 74.8%, based on this fiscal year’s FFO/share guidance, is right about where it should be and has been. You don’t get much more consistent than this. One thing that’s not consistent? The stock’s performance this year.

This stock consistently outperforms. But it’s down more than 5% in a year in which the broader market is up pretty substantially. Will it come back and return to its consistent glory?

Well, it wouldn’t take much for that to happen. All it would have to do is revert to the mean. Its five-year average cash flow multiple is 19.5. It’s currently commanding a multiple of 13.6. So there’s some serious ground to cover there before even factoring in any kind of advancement in the business. And shareholders get a 5%+ yield while they wait for that to play out. You could do a lot worse than that, in my view.

Well, it wouldn’t take much for that to happen. All it would have to do is revert to the mean. Its five-year average cash flow multiple is 19.5. It’s currently commanding a multiple of 13.6. So there’s some serious ground to cover there before even factoring in any kind of advancement in the business. And shareholders get a 5%+ yield while they wait for that to play out. You could do a lot worse than that, in my view.

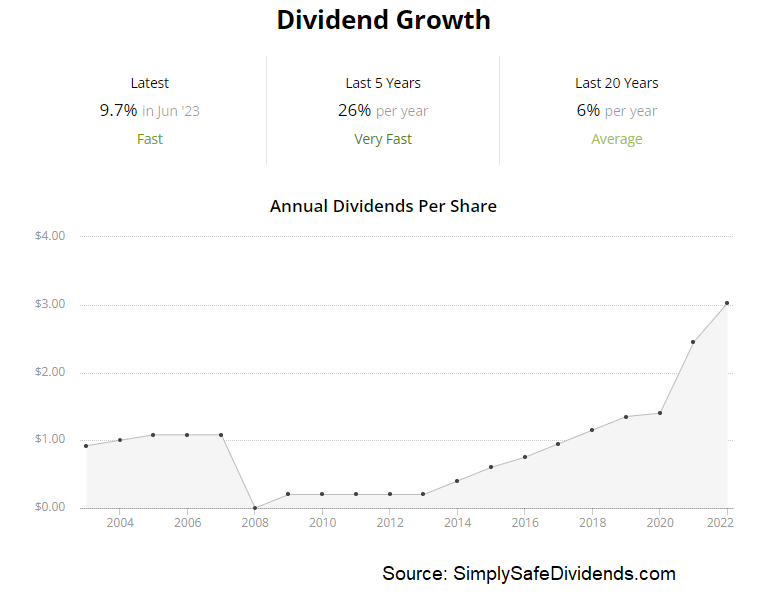

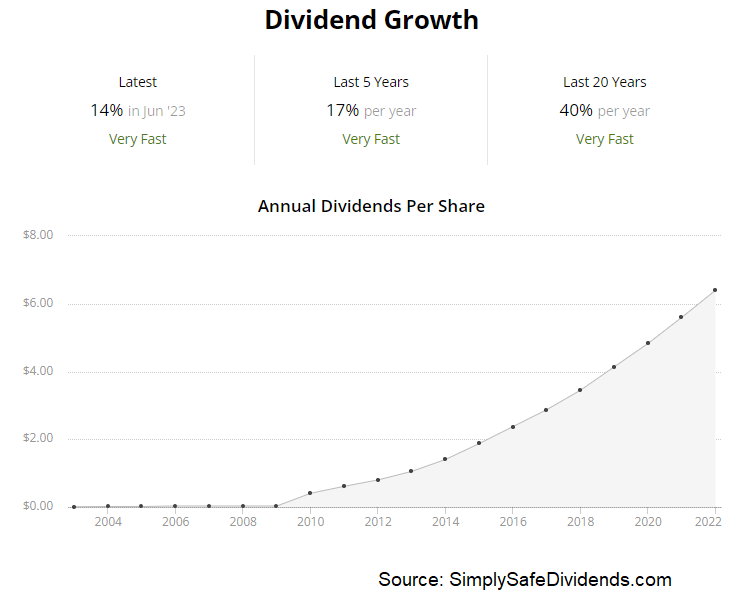

The sixth dividend increase I want to highlight is the one that was announced by UnitedHealth Group (UNH). UnitedHealth just increased its dividend by 13.9%.

14% more money for doing nothing other than sitting on your hands. How can you not love this? I’ve seen a lot of great things in life, but dividend growth investing ranks near the top. It’s just awesome. This marks 14 consecutive years of dividend increases for the healthcare conglomerate.

UnitedHealth is a dividend growth machine. Long-term dividend growth investors who don’t own this business are really missing out. A five-year DGR of 17.4%, which isn’t that far off from this year’s dividend raise, shows you just how much dividend growth has been occurring here.

Now, the stock’s yield of 1.6% isn’t much to write home about. And that’ll turn off the yield chasers out there. But when you’ve got this kind of quality and growth, you tend not to get a high yield. With the payout ratio still low, at 34.4%, UnitedHealth’s dividend growth machine is just getting warmed up.

Now, the stock’s yield of 1.6% isn’t much to write home about. And that’ll turn off the yield chasers out there. But when you’ve got this kind of quality and growth, you tend not to get a high yield. With the payout ratio still low, at 34.4%, UnitedHealth’s dividend growth machine is just getting warmed up.

This stock is going through a very rare period of underperformance. That could be a huge opportunity.

This is one of those stocks that so routinely and thoroughly outperforms, it’s tough to find that buying window. I mean, the stock has nearly doubled over the last five years alone.

It’s up more than 600% over the last 10 years. This is a monster. However, it’s down 8% YTD. Is that the buying window? Could very well be. Most basic valuation metrics are in line with, or slightly below, their respective recent historical averages. The P/E ratio of 21.9, for instance, is a tad below its own five-year average of 22.4. If you don’t yet have UnitedHealth in your portfolio, now could be the time to change that.

It’s up more than 600% over the last 10 years. This is a monster. However, it’s down 8% YTD. Is that the buying window? Could very well be. Most basic valuation metrics are in line with, or slightly below, their respective recent historical averages. The P/E ratio of 21.9, for instance, is a tad below its own five-year average of 22.4. If you don’t yet have UnitedHealth in your portfolio, now could be the time to change that.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income