On the Roof of the World, icebergs dot the dark Arctic Ocean. It’s a desolate place. Travelers risk the icy peril of a region where the sun never sets during the summer… and never rises in the winter. Stark emptiness surrounds ships as they crack through an icy maze across the Arctic Circle…

Yet, its geopolitical importance is increasing by the day.

As is its profit potential for savvy, globally oriented investors like us.

The Cold Is Heating Up

Six nations lay claim to the bounty of minerals lying beneath this inhospitable place. Canada, Denmark, the United States, Russia, and Norway will jockey for trillions of dollars worth of energy and minerals across 5.5 million square miles of barren land.

It is the ultimate collision point of human ambition and nature’s inclemency.

Yet one company has conquered the frozen expanse. Its ships sail forward across two routes: The Northern Sea Route, which stretches 3,000 nautical miles from the hostile Barents Sea to the Bering Strait. And the fabled Northwest Passage, which now connects the Atlantic Ocean to the Pacific through the unyielding Canadian Arctic Archipelago. This route runs even longer – 5,780 rigorous nautical miles.

The cruelty of an endless winter brings a ghostly cover over its ships as they battle with a ruthless, physical opponent: Ice. Across the Arctic, even in summer – icebergs stand like titans.

The brave crews of ice-breaking ships are masters of survival, all pushing through the cold silence of the Arctic with common goals: To help other ships pass through these trade routes. And to feed and power the world with a bounty of vital commodities.

As ice breakers charge forward into the Arctic, each strike bellows through the ship’s hull. It’s a reminder of man’s struggle against nature. But each strike moves travelers toward massive rewards: A shorter trade route, higher transport margins, arbitrage potential, and higher payment for the hassle.

The Northern Sea Route and Northwest Passage, with all their empty magnificent desolation, offer no mercy to the timid. But it stands as one of the most profitable opportunities for patient income investors. July is one of the company’s most profitable months of the year as it carves through the Roof of the World…

Your Roof of the World Stock

Pangaea Logistics Solutions (PANL) is a Rhode Island-based maritime company with 25 ships. Its daring work largely centers on ice-breaking… or carving through the Arctic’s frozen realm.

Ice-breaking is an uncommon, niche endeavor. Pangaea’s business relies on enduring customer service, a steady stream of repeat business, and long-term contracts.

It operates a fleet of Supramax-, Panamax-, and Handymax-class vessels. Its work defies the traditional humdrum of the dry bulk space. It doesn’t overly rely on coal shipments (a sector that faces renewed headwinds in the second half of the year).

Instead, it carries a diverse portfolio to sustain humanity.

Even through the extremes of the Arctic…

Pangaea Logistics Solutions carries agricultural products, cement, fertilizer, coal, iron ore, other iron products, bauxite, and aggregates.

Despite all the challenges that faced the shipping industry in 2021, Pangaea provided investors with a 33.8% return in 2022, not including dividends. It’s also been a top performer in 2023.

What Lies Ahead in the Arctic

In January, I predicted a 45% upside for PANL stock over the next two years from its then-trading price of $5.15. Today, shares trade at $6.77 – it’s up 25% to start the year. Shares rallied in February to above $7.00 before collapsing during the short-term banking crisis in March 2023.

I stick by my earlier projection.

Another pullback seems possible, given macroeconomic conditions. However, it’s important to remember a few longer-term elements of this value, income, and insider play.

PANL pays a dividend north of 5.9% today. That’s higher than its five-year average, and its low coverage ratio points to a company that’s using robust cash flow to pay down debt (reduced by ~$30 million in 2022) while expanding its fleet in 2023.

This dividend might look much lower compared to the payments of rivals like Star Bulk Carriers (SBLK) and Zim Integrated Shipping (ZIM). However, those other competitors tend to pay special, variable dividends. Pangaea’s quarterly distribution is fixed and is unlikely to fall at any time soon.

The company has a Piotroski F-score of 7. This signals that company executives have shareholder interest at heart. The score is reinforced by executives having skin in the game. Executives own roughly 23% of the company’s stock.

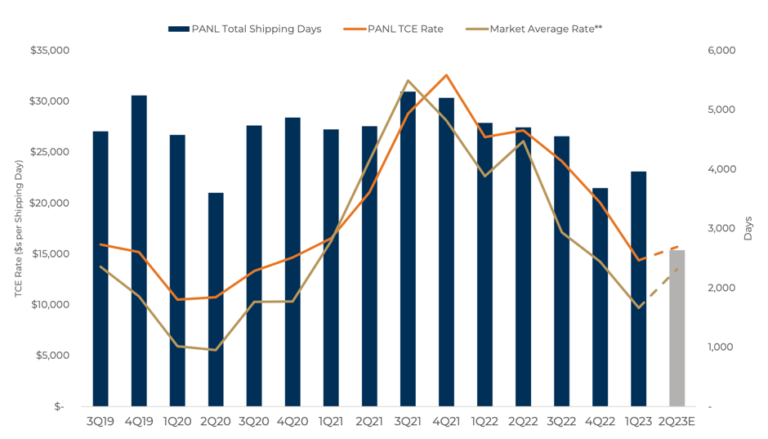

This poster child of responsible financial diligence and shareholder-friendly policies has faced new headwinds due to the falling shipping rates. But as Time Charter Equivalent rates have come down across the dry bulk shipping industry in late 2022, Pangaea projects to generate more revenue than industry peers, thanks to its niche.

Source: Company Q1 2023 Investor Presentation

Source: Company Q1 2023 Investor Presentation

In addition, the company predicts a sharp decline in new vessel manufacturing in 2023. This will constrain the global ship supply and help the dry bulk market recover. The company trades at a meager price-to-earnings ratio of 4.8X, while its price-to-Graham number trades at less than 0.45x.

As I’ve noted, 2023 will be difficult for the macro-environment.

Any short-term downside for PANL is around the March floor. I don’t anticipate a prolonged downward move for PANL, given its niche focus, income, and upside. We’ll discuss a reasonable investment strategy for this name and more all this week.

Stay golden,

Garrett Baldwin

Source: Money Morning