It’s said that the cream always rises to the top. Well, high-quality dividend growth stocks are the crème de la crème. These stocks give you ownership in some of the greatest businesses in the world.

How do you know they’re so great? Many reasons.

How about producing the ever-growing profit necessary to pay out ever-growing dividends?

That’s a pretty good reason. Try to do something like that without running a great business. Not gonna happen. But… if you can get equity in a great business on sale, all the better.

Price and yield are inversely correlated. All else equal, lower prices result in higher yields.

This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach. I always see short-term volatility as a long-term opportunity. That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

All that said, it’s a big market, and some ideas are better than others.

Focusing on the very best long-term ideas right now is what this article is all about.

Today, I want to tell you my top 5 dividend growth stocks for June 2023.

Ready? Let’s dig in.

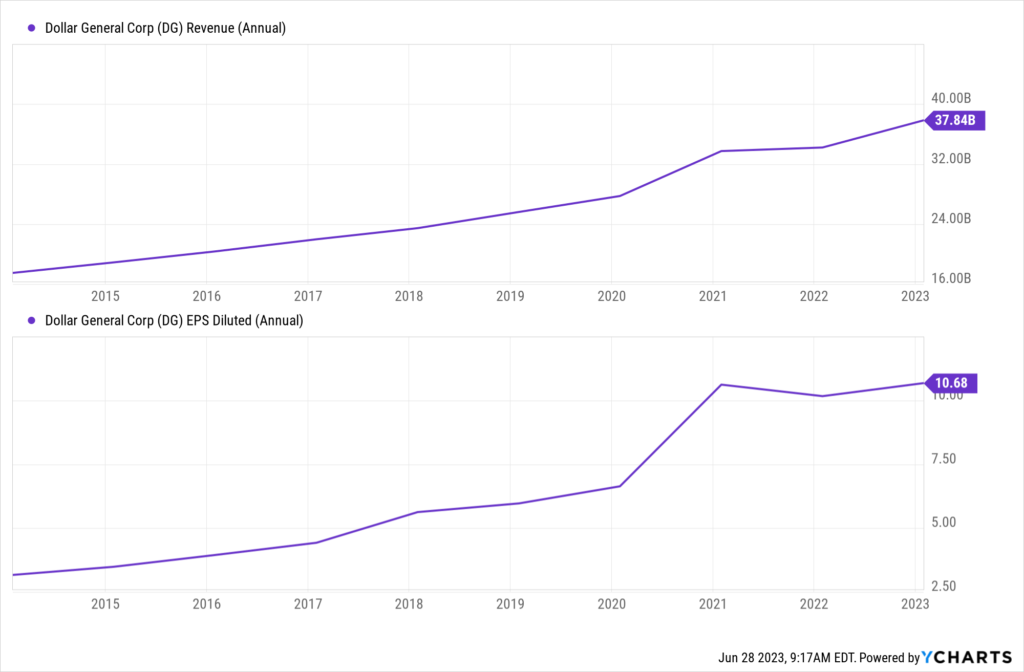

My first dividend growth stock for July 2023 is Dollar General (DG). Dollar General is an American chain of neighborhood general stores that focus on low-cost merchandise.

This is a really interesting retailer. Now, retailing is a tough gig. And that’s why it’s so important to differentiate. If you can’t operate within a niche of some kind, it’s brutal. Well, Dollar General has taken a unique path by inserting its stores in underserved, rural communities that typically lack competition.

And this local convenience is a big hit. Plus, because of the focus on affordable products, these communities, which typically feature households that earn below-average incomes, become loyal, repeat customers. This is why Dollar General has racked up an 8.9% CAGR for revenue and 14.5% CAGR for EPS over the last decade.

Huge business growth. Huge dividend growth. Indeed, Dollar General has increased its dividend for nine consecutive years, with a five-year DGR of 15% – lining up very nicely with EPS growth. And this growth uniformity has kept the payout ratio in check, which is sitting at a lowly 22.2%.

Huge business growth. Huge dividend growth. Indeed, Dollar General has increased its dividend for nine consecutive years, with a five-year DGR of 15% – lining up very nicely with EPS growth. And this growth uniformity has kept the payout ratio in check, which is sitting at a lowly 22.2%.

The one issue here, if you can call it that, is the yield. At just 1.4%, it does leave something to be desired. But Dollar General has been a compounder, not an income play, so it’s not surprising to see a low yield here.

After a serious selloff, the stock looks attractively valued for the first time in a long time.

A disappointing Q1 report sent the stock reeling. It’s now down about 30% YTD, which is pretty stunning for a stock that routinely outperforms. A bummer for existing shareholders. But an interesting opportunity for those who don’t already have shares. We’ll have a full analysis and valuation piece coming up on Dollar General shortly, so stay tuned for that. In the meantime, I’ll note that the P/E ratio of 16.1 is substantially lower than its own five-year average of 21.6. Take a look at this one.

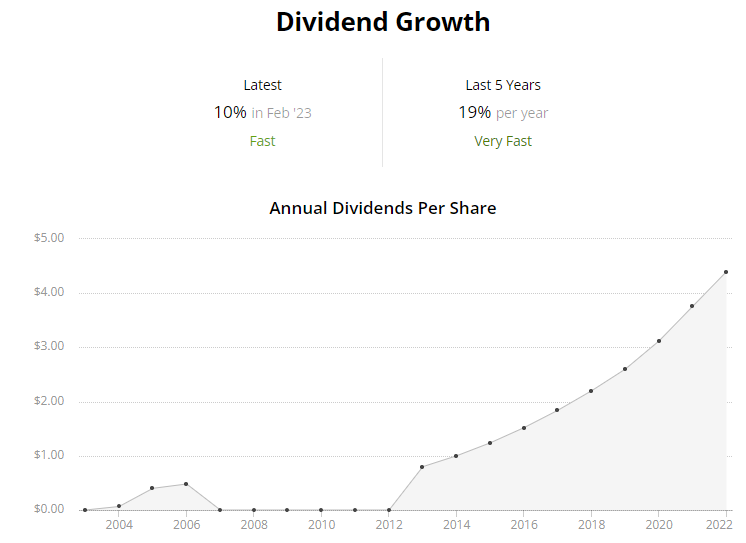

My second dividend growth stock for July 2023 is Domino’s Pizza (DPZ). Domino’s is a multinational pizza restaurant chain.

Well, I’m actually underselling it there. Domino’s is the largest pizza restaurant chain in the world. Nobody’s bigger. And one could argue that nobody’s better. Fundamentally speaking, this is a very high-quality business. It’s being run about as well as it can be.

And let’s be honest – pizza kind of sells itself, right? If you can take something that people already want to buy, and then you comport yourself at the highest level, you almost can’t help but knock it out of the park. That’s exactly what Domino’s has been doing, as evidenced by its 10.7% CAGR for revenue and 19.7% CAGR for EPS over the last decade.

What’s better? Pizza? Or a fast-growing dividend? You be the judge. I like good pizza. But I might like a fast-growing dividend even more. With Domino’s, you get both. The company has increased its dividend for 11 consecutive years, and the five-year DGR is 19%. Wow. That is a very high growth rate for a dividend.

What’s better? Pizza? Or a fast-growing dividend? You be the judge. I like good pizza. But I might like a fast-growing dividend even more. With Domino’s, you get both. The company has increased its dividend for 11 consecutive years, and the five-year DGR is 19%. Wow. That is a very high growth rate for a dividend.

Now, the stock’s yield is 1.5%, so you do sacrifice some yield in order to get that high growth rate. Can’t have it all. But with a low payout ratio of 37.3%, it’s difficult to see anything but more strong dividend growth from Domino’s over the coming years.

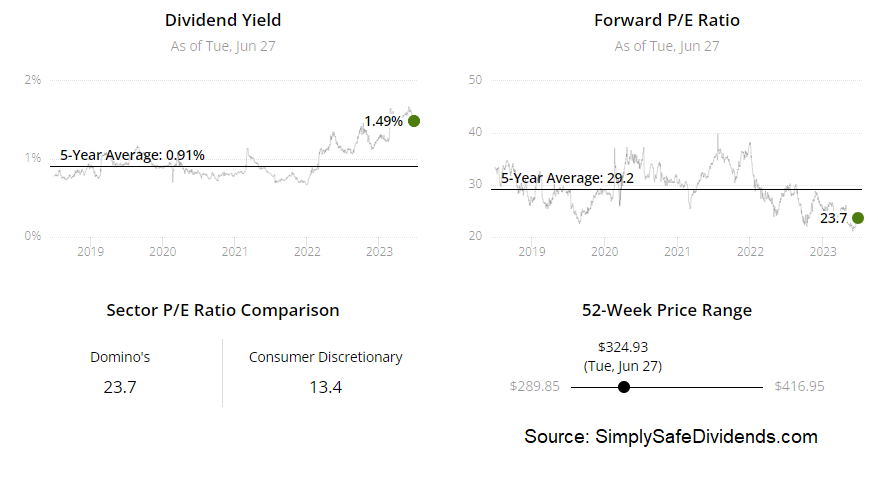

That growth should fuel a ton of total return, and the stock isn’t expensive right now.

This is another one that’s always just looked kind of expensive, but it, too, has come down to a more reasonable level. The P/E ratio of 24.4 isn’t super low, no. But I see a lot of businesses out there with almost no growth, commanding similar earnings multiples. Those are expensive. Domino’s? Not so much. Not with this growth.

Keep in mind, its five-year average P/E ratio is 32.8. We’re not even close to that. I already put together some content on Domino’s, which will fully analyze and value the business. The fair value estimate came out to $372.16/share. Just have to edit that video. Should go live soon. Until then, Domino’s should be on your radar.

Keep in mind, its five-year average P/E ratio is 32.8. We’re not even close to that. I already put together some content on Domino’s, which will fully analyze and value the business. The fair value estimate came out to $372.16/share. Just have to edit that video. Should go live soon. Until then, Domino’s should be on your radar.

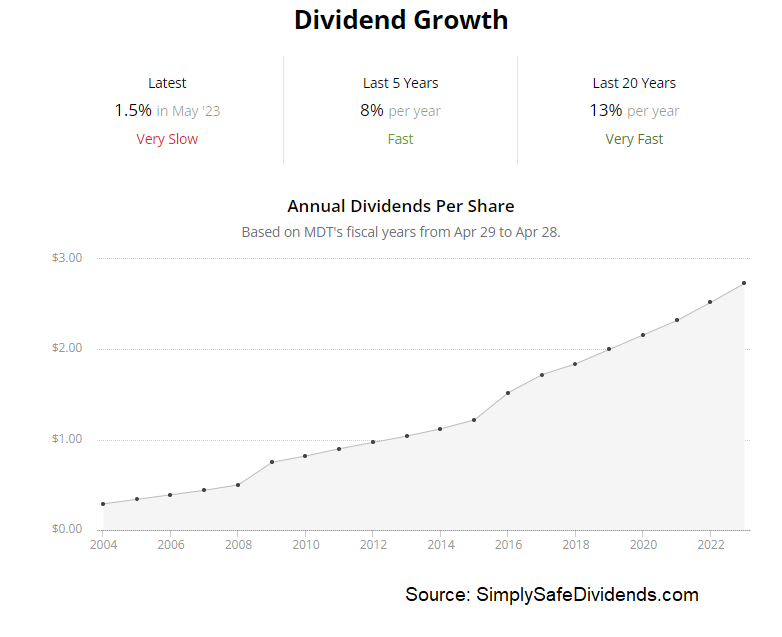

My third dividend growth stock for July 2023 is Medtronic (MDT). Medtronic is a global developer and manufacturer of medical devices for chronic diseases.

This business is in such a good spot. Healthcare is in secular growth mode, thanks to powerful demographic trends. The world is growing larger, older, and wealthier. All of that pushes up demand for quality healthcare. But Medtronic is in especially good shape, because of inelastic demand for its products.

If you’re in a life-or-death scenario, let’s just say that a higher price on a medical device is not going to reduce your demand for it. This has helped Medtronic to put up respectable growth. Revenue has compounded at 7% annually over the last decade, while EPS has compounded at 6.4% annually.

The dividend track record here is unquestionably great. This is a vaunted Dividend Aristocrat, with 46 consecutive years of dividend increases. You’ve gotta love that kind of consistency. Because guess what’s consistent? Bills. Bills are very consistent. So if your income, and the growth of it, is just as consistent, that makes life a lot easier.

The 10-year DGR of 10% is strong, although recent dividend raises have been modest. On the other hand, the stock’s 3.2% yield is well above average for this stock. And the payout ratio of 54.7% (based on midpoint guidance for FY 2024 adjusted EPS) easily supports the current dividend. Medtronic is on its way to becoming a Dividend King.

The 10-year DGR of 10% is strong, although recent dividend raises have been modest. On the other hand, the stock’s 3.2% yield is well above average for this stock. And the payout ratio of 54.7% (based on midpoint guidance for FY 2024 adjusted EPS) easily supports the current dividend. Medtronic is on its way to becoming a Dividend King.

Medtronic used to frequently command a big premium. Now? A big discount.

Medtronic used to frequently command a big premium. Now? A big discount.

That’s right. I saw this stock seemingly defy gravity for years. But it’s been in the doghouse since the pandemic hit. Why? Well, a lot of Medtronic’s products are needed in elective surgeries, and the global healthcare complex was squarely focused on the pandemic for a couple of years, much to the detriment of the likes of Medtronic. No matter.

A lot of surgeries have been deferred temporarily, not permanently canceled. And that should lead to a resurgence in the business over the coming years, which bodes well for sales, profit, and the dividend. Meanwhile, shares look worth about $102.50/each, as our upcoming analysis and valuation video will show you. With shares priced at about $87.50 each right now, this Dividend Aristocrat looks on sale.

My fourth dividend growth stock for July 2023 is Tractor Supply (TSCO).

Tractor Supply is an American retail chain of stores that sells products catering to farmers, ranchers, and customers living a rural lifestyle. Tractor Supply is easily one of the best retail outfits I’ve ever run across. Fantastic fundamentals right across the board.

This company targets consumers with above-average incomes living in areas with a below-average cost of living. And because many of the products are both heavy and consumable, Tractor Supply is largely insulated from e-commerce threats. If you want growth, you get it here. We’re talking about an 11.8% CAGR for revenue and a 17.2% CAGR for EPS over the last decade.

We can see a lot of that growth also show up with the dividend.

We can see a lot of that growth also show up with the dividend.

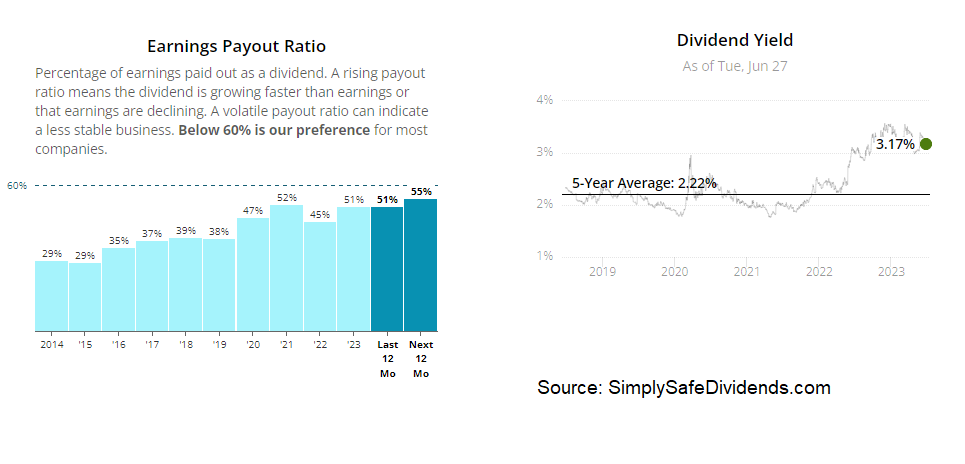

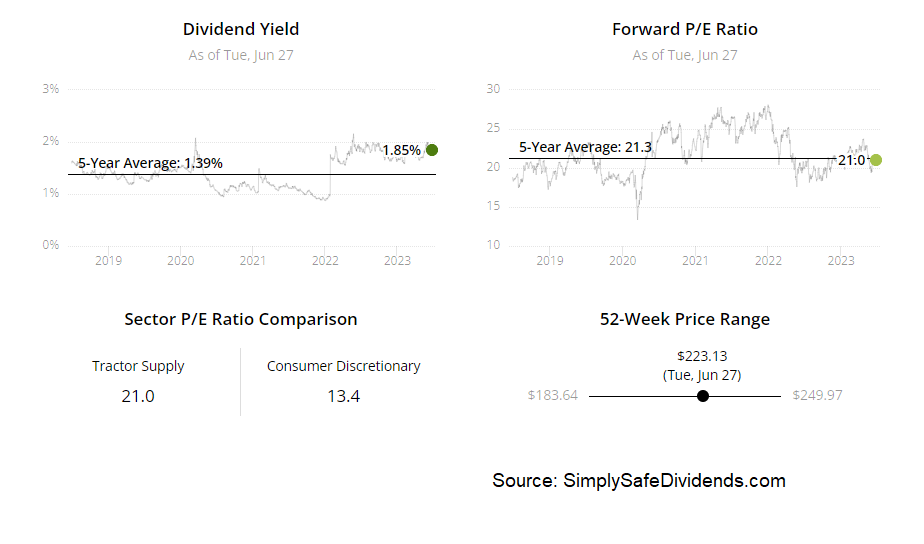

The dividend has been increased for 14 consecutive years, and I think Tractor Supply is just getting started with that. A 10-year DGR of 26.2% shows what a blazing start it’s off to. Plus, you even get a very decent yield of 1.9%. It’s rare to find a yield this high with such an outstanding growth rate. In these cases, the yield is usually around the 1% mark, or less. This is also a very safe dividend, with a payout ratio of just 42.4%.

But wait. There’s more. You also get a pretty appealing valuation here. I say that with respect to the quality and growth of the business, as well as it what it typically fetches in the market. The P/E ratio of 22.5 isn’t super low, no. But I don’t see that as aggressive at all.

For perspective, its own five-year average P/E ratio is 23.4. If it hasn’t already been published by the time this video comes out, we’ll have a full analysis and valuation video on Tractor Supply. The estimate for intrinsic value came out to about $235.50/share for the business. It’s not a steal right now. But I think it’s a wonderful business available for a better-than-fair price.

For perspective, its own five-year average P/E ratio is 23.4. If it hasn’t already been published by the time this video comes out, we’ll have a full analysis and valuation video on Tractor Supply. The estimate for intrinsic value came out to about $235.50/share for the business. It’s not a steal right now. But I think it’s a wonderful business available for a better-than-fair price.

My fifth dividend growth stock for July 2023 is Tyson Foods (TSN). Tyson Foods is one of the world’s largest processors and marketers of chicken, beef, and pork.

Now, I’ll be honest. Tyson Foods is not my favorite business. Not even close, really. But here’s the thing: People have to eat. Tyson Foods caters to this basic need. And it’s not just eating, by the way. We’re talking about proteins here.

As people become wealthier – which is a global trend – they tend to demand more proteins. That obviously bodes well for Tyson Foods. Growth has been a bit lumpy, but the business is still putting up good numbers – a 5% CAGR for revenue over the last decade, and a 17.3% CAGR for EPS over that time frame.

Dividend growth has also been a bit lumpy. Again, though, these are good numbers.

Dividend growth has also been a bit lumpy. Again, though, these are good numbers.

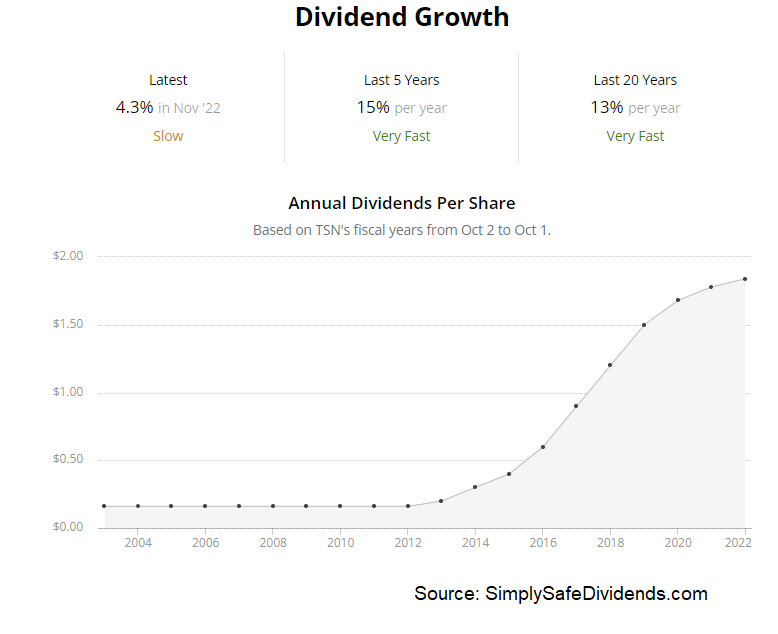

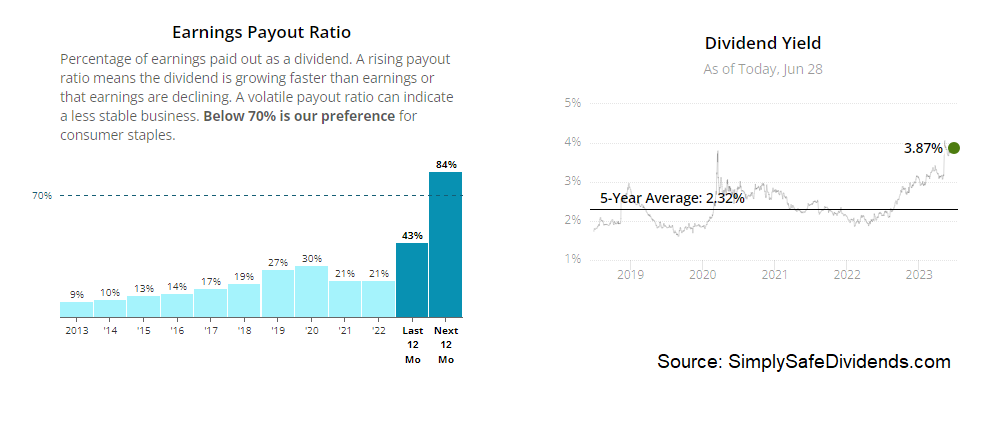

Tyson Foods has increased its dividend for 11 consecutive years. The 10-year DGR is 27%, which is fantastic. However, it’s super misleading. Recent dividend raises have been in the mid-single-digit range, and that’s the kind of expectation I’d have on a go-forward basis from Tyson Foods.

Still, you get a 3.8% yield, which is in utility and REIT territory. From a food company. That’s not bad at all. The payout ratio is 43.8%, based on TTM adjusted EPS. And that gives some cushion to the dividend’s sustainability while the business goes through a tough stretch.

Speaking of tough stretches, the stock is in one right now. And that’s exactly why I’m bringing up Tyson Foods right now. The stock is down 21% YTD and sitting at multiyear lows. Look, Tyson Foods isn’t of the same ilk as some of the other businesses I’ve talked about today. It’s not of that caliber. But it’s downright cheap.

Speaking of tough stretches, the stock is in one right now. And that’s exactly why I’m bringing up Tyson Foods right now. The stock is down 21% YTD and sitting at multiyear lows. Look, Tyson Foods isn’t of the same ilk as some of the other businesses I’ve talked about today. It’s not of that caliber. But it’s downright cheap.

For value hunters that gravitate toward cheapness, it’s pretty interesting. The P/E ratio is 12. Yes. 12. And people aren’t going to suddenly stop eating chicken, right? I recently went through the whole business in an analysis and valuation report, which should go live soon (if it hasn’t already). The estimate of fair value for Tyson Foods worked out to just over $71/share. At $50/share, Tyson Foods could be one of the cheapest dividend growth stocks out there.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income