Becoming a successful investor can be, in some ways, counterintuitive.

There’s a natural tendency to assume that complicated must be good.

People new to investing think that the big returns can be found in risky, complex areas of the market.

But that’s not necessarily true at all.

Truth be told, it’s better to keep it simple.

The legendary investor Peter Lynch looked for business models that could be boiled down into a crayon drawing by a child.

This “crayon test” is a great filter.

And if it’s good enough for one of the greatest investors of all time, it’s good enough for the rest of us.

Indeed, some of the world’s very best businesses are very easy to understand.

You can find many of these businesses on the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

We’re talking about dividend growth stocks.

A dividend growth stock represents equity in a business that pays its shareholders reliable, rising dividends.

And how do reliable, rising dividends get funded?

And how do reliable, rising dividends get funded?

By producing reliable, rising profit.

This reliable, rising profit is produced when a business is selling great products and/or services.

Generally speaking, these are the easy-to-understand, highly visible products and/or services that we all commonly use.

I’ve been keeping it simple by buying high-quality dividend growth stocks for years.

It’s how I built the FIRE Fund.

That’s my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

Dividend income has been covering my expenses for years now, which allowed me to retire in my early 30s.

My Early Retirement Blueprint explains exactly how I was able to retire so early in life.

Suffice it to say, living below my means and investing in simple-to-understand but high-quality businesses was a big part of my success.

But that’s not all.

But that’s not all.

Investing in the right businesses at the right valuations is key.

See, price only represents what you pay, but it’s value that represents what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Keeping thing simple by buying high-quality dividend growth stocks when they’re undervalued is a powerful way to build substantial wealth and passive income over the long run.

Now, this does require one to have an understanding of valuation.

But this concept is also best when kept simple.

To that end, my colleague Dave Van Knapp put together Lesson 11: Valuation.

It’s an easy-to-follow valuation guide that can be used to estimate the fair value of just about any dividend growth stock you’ll run into.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Domino’s Pizza, Inc. (DPZ)

Domino’s Pizza, Inc. (DPZ)

Domino’s Pizza, Inc. (DPZ) is a multinational pizza restaurant chain.

Founded in 1960, Domino’s is now an $11 billion (by market cap) major QSR player that employs nearly 9,000 people.

FY 2022 revenue can be broken down across three main segments: Supply chain, 61%; U.S. stores, 33%; and International Franchise, 6%.

Domino’s is the largest pizza restaurant chain in the world, with approximately 20,000 stores located across 90 different markets.

Almost all stores globally are franchised.

Some investors, especially novice investors, are under the impression that successful investing should be overly complex.

To the contrary, some of the most complex investments I’ve run across have been the worst.

And some of the very best businesses have been among the simplest.

Domino’s is a great example of the latter.

This is a company that, through local franchises, makes and sells pizza.

It doesn’t get much more simple than that.

But there’s beauty in the simplicity.

Pizza is a timeless food staple that travels well and never goes out of style.

I can tell you, as someone who’s lived abroad for a number of years, pizza is very popular worldwide.

Pizza is consumable, and it must be purchased again once it’s eaten.

The repeat business is about as good and predictable as it gets.

Moreover, with the possibility of a recession upon us, any “trading down” from consumers would play right into the hands of Domino’s – pizza is a cheap, easy meal.

I can’t imagine a future world 10 or 20 years from now in which Domino’s isn’t making more money and paying out a bigger dividend.

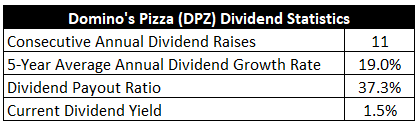

Dividend Growth, Growth Rate, Payout Ratio and Yield

Already, the company has increased its dividend for 11 consecutive years.

A young track record, sure, but what a start Domino’s is off to.

The five-year dividend growth rate of 19% speaks to this.

The five-year dividend growth rate of 19% speaks to this.

The consistent double-digit dividend growth makes up for the lowish yield of 1.5%.

As low as this yield might seem to be, it’s actually 60 basis points higher than its own five-year average.

Frankly, the market has accepted a low yield from the stock because of its high growth rate.

Based on the performance of a long-term investment in the business, this has been a good call.

Assuming a static valuation, the sum of yield and dividend growth should be pretty close to the total return.

Indeed, this stock’s CAGR over the last 10 years is roughly 20%, which is incredible, and that lines up pretty well with the dividend growth rate.

With a low payout ratio of 37.3%, I suspect we’re looking at more double-digit dividend growth from Domino’s over the next 10+ years.

That said, since some of this high dividend growth was fueled by expanding the payout ratio from 0% at the start of this epic run, I would expect things to slow down just a bit from the heady past.

Still, these are fantastic dividend metrics for those who have the time for a compounder to compound.

Revenue and Earnings Growth

As fantastic as these metrics may be, though, they’re mostly looking into the past.

However, investors must have their eyes on the future – today’s capital is being risked for tomorrow’s rewards.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be of great aid when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then uncover a professional prognostication for near-term profit growth.

Lining up the proven past against a future forecast in this manner should allow us to roughly determine where the business might be going from here.

Domino’s advanced its revenue from $1.8 billion in FY 2013 to $4.5 billion in FY 2022.

That’s a compound annual growth rate of 10.7%.

Strong top-line growth here.

I’m usually looking for a mid-single-digit top-line growth rate from a mature business.

Domino’s is fairly mature, yet it blew away my expectation.

Meanwhile, earnings per share grew from $2.48 to $12.53 over this period, which is a CAGR of 19.7%.

Wow.

We can clearly see what’s been fueling the 20% dividend growth and 20% stock CAGR.

It’s been EPS growth.

Now, it would be tough for Domino’s to follow that up with a repeat performance.

The encore will likely be less dramatic, as a massive 38% reduction in the outstanding share count over the last decade, which was assisted through leverage, is almost certainly not going to happen again over the next 10 years.

No matter, as Domino’s doesn’t need to pump out 20% growth in order for it to be a very successful long-term investment.

Even something close to half of that level would suffice for most investors.

Looking forward, CFRA believes that Domino’s will compound its EPS at an annual rate of 3% over the next three years.

When I said a slowdown in growth would be acceptable, that’s not quite what I had in mind.

CFRA expects “[Domino’s] to face headwinds until the second half of the year due to labor challenges, demand softness in delivery, and a lower mix of U.S. franchise business, which typically have higher margins.”

So what’s the story here?

It’s a similar story to that of many other businesses over the last few years – a harsh normalization of business after a strange period that was heavily influenced by a global pandemic (and the responses to it).

But here’s where Domino’s differs: You can’t “pull forward” sales of pizza.

Once you buy, say, a new deck for your house, you’re done.

On the other hand, once pizza is ordered and consumed, you have to go out and order another pizza.

The last three years were spectacular for Domino’s, no doubt about it.

But the three years prior to FY 2020 were also spectacular.

And I don’t see anything that changes the overall thesis for Domino’s or dynamics for pizza demand.

If anything, any kind of economic slowdown in the US or elsewhere, could bode well for Domino’s – pizza is a cheap, easy meal.

I’m less focused on the next year or two than I am on the next decade or two.

Regarding that latter time frame, I’m enthusiastic about what’s possible for Domino’s.

Dividend growth could be relatively modest over the very near term, but I don’t see anything that would impede Domino’s from delivering dividend raises that are in the low-double-digit range over the next 10+ years.

Furthermore, it’s not just the high growth rate that’s so appealing and valuable here but the predicability of revenue and earnings – pizza isn’t going anywhere.

Financial Position

Moving over to the balance sheet, Domino’s has a good financial position that might look worse than it really is.

The long-term debt/equity ratio is N/A (due to negative common equity), while the interest coverage ratio is approximately 4.

Domino’s has right about $5 billion in long-term debt, which isn’t bad when compared to its market cap of $11 billion.

Ordinarily, I’d be somewhat concerned about this kind of balance sheet situation.

However, because Domino’s operates within an asset-light framework built around franchises, which creates a centralized revenue collector with minimal overhead costs, I’m less concerned than I’d usually be.

Still, I’d not like to see the balance sheet deteriorate much from where it already is.

Circling back around to what I noted earlier, a lack of flexibility with the balance sheet will limit buybacks on a go-forward basis.

Profitability is robust.

Over the last five years, the firm has averaged annual ROA of 32.5% and annual net margin of 11%. Due to negative common equity, there is no ROE.

In many ways, Domino’s is a terrific business.

But what makes it especially terrific is the way in which it franchises out a timeless food staple with very predictable and repeatable sales.

And the company does benefit from durable competitive advantages that include economies of scale, brand power, and a global franchise footprint.

Of course, there are risks to consider.

Competition, regulation, and litigation are omnipresent risks in every industry.

I see regulation and litigation risks as being relatively low for Domino’s.

On the flip side, they operate in a fiercely competitive industry.

Helping to stave off competition is the company’s “fortressing” strategy – the shortening of delivery radiuses by putting in new stores in the same markets, as close to customers as possible, which means shorter delivery times and lower costs per delivery.

The stretched balance sheet is an issue.

Inflation is high right now, creating challenges around input costs and wage inflation.

The company has been facing labor shortages, especially regarding delivery drivers.

The global footprint is an advantage, but a larger absolute footprint is harder to grow in relative terms.

Risks like these are always worth considering, but the quality of the business also needs to be considered.

On top of that, the valuation, which looks attractive after the stock’s 25% drop from its 52-week high, should be strongly considered…

Stock Price Valuation

The P/E ratio is sitting at 24.9.

Compared to its own five-year average of 32.8, it’s currently remarkably low.

The sales multiple of 2.6 is also well off of its own five-year average of 3.6.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 12% dividend growth rate for the next 10 years, and a long-term dividend growth rate of 8%.

Because the growth rate is currently high, which I view as unsustainable over the very long run, I’m using a two-stage model.

The initial 12% dividend growth rate is much lower than the demonstrated dividend growth and EPS growth over the last decade.

And the payout ratio remains low.

However, recent growth has slowed, CFRA’s near-term EPS growth forecast is only in the single digits, and the last dividend raise came in at 10%.

I’m trying to balance things out here, as I do view the growth horsepower here from Domino’s not being quite as high as it used to be.

That said, to keep perspective, the company’s $11 billion market cap is actually tiny in the QSR world.

Domino’s still has plenty of runway in front of it.

Overall, I think Domino’s has the ability to grow its dividend in a low-double-digit range for years to come.

The DDM analysis gives me a fair value of $366.48.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I believe I was being judicious with my approach to the valuation, yet the stock still comes out looking decently cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates DPZ as a 4-star stock, with a fair value estimate of $385.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates DPZ as a 5-star “STRONG BUY”, with a 12-month target price of $365.00.

A pretty tight range this time. Averaging the three numbers out gives us a final valuation of $372.16, which would indicate the stock is possibly 13% undervalued.

Bottom line: Domino’s Pizza, Inc. (DPZ) is operating a simple-to-understand business model making a ton of money from selling a timeless food staple. And the company is doing so within the favorable framework of franchising. With a market-like yield, a low payout ratio, a double-digit dividend growth rate, more than 10 consecutive years of dividend increases, and the potential that shares are 13% undervalued, long-term dividend growth investors looking for a predictable compounder should have their eyes in this direction.

Bottom line: Domino’s Pizza, Inc. (DPZ) is operating a simple-to-understand business model making a ton of money from selling a timeless food staple. And the company is doing so within the favorable framework of franchising. With a market-like yield, a low payout ratio, a double-digit dividend growth rate, more than 10 consecutive years of dividend increases, and the potential that shares are 13% undervalued, long-term dividend growth investors looking for a predictable compounder should have their eyes in this direction.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is DPZ’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 55. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, DPZ’s dividend appears Borderline Safe with a moderate risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income