Building serious wealth and passive income is simple but hard.

The necessary steps one has to follow are pretty simple to understand.

But consistently executing these steps over the course of many years is hard.

This is why investors should try to make things easier on themselves.

One of the most obvious ways to do this?

Use the right strategy.

In my experience, the best strategy to make investing easier (and, quite possibly, far more successful) over the long run is dividend growth investing.

This is a strategy whereby you buy and hold shares in wonderful businesses that are paying safe, growing dividends to shareholders.

These growing dividends are funded by growing profit.

And growing profit is a natural outcome for wonderful businesses selling great products and/or services.

It really can be that easy.

To see what I mean, take a look at the Dividend Champions, Contenders, and Challengers list.

This list contains invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

You’ll notice many household names on the list.

That’s not by accident, nor is a lengthy track record of growing dividends accidental.

I’ve been personally employing this strategy for more than a decade now.

I’ve used it to build the FIRE Fund.

I’ve used it to build the FIRE Fund.

That’s my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

Indeed, dividends started to eclipse my expenses many years ago.

I actually retired in my early 30s.

How?

My Early Retirement Blueprint explains.

Much of my success can be attributed to the dividend growth investing strategy, which filtered me into wonderful businesses.

However, there’s another important aspect to cover.

However, there’s another important aspect to cover.

It’s valuation.

Price only tells you what you pay, but value tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying high-quality dividend growth stocks when they’re undervalued is an obvious way to make long-term investing easier and, likely, far more successful.

That said, valuation is another thing that might seem simple but hard.

Fear not.

My colleague Dave Van Knapp made it a lot more simple with Lesson 11: Valuation.

Part of an overarching series of “lessons” on dividend growth investing, it shares a valuation template that can be used to estimate fair value on just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Medtronic PLC (MDT)

Medtronic PLC (MDT)

Medtronic PLC (MDT) is a global developer and manufacturer of medical devices for chronic diseases.

Founded in 1949, Medtronic is now a $111 billion (by market cap) healthcare giant that employs 95,000 people.

The company reports results across four segments: Cardiovascular, 37% of FY 2023 revenue; Neuroscience, 29%; Medical Surgical, 27%; and Diabetes, 7%.

Medtronic’s product portfolio is comprised of a variety of life-saving and life-improving medical devices that include implantable defibrillators, heart valves, insulin pumps, glucose monitoring systems, pacemakers, stents, and surgical tools.

Healthcare is fertile ground for long-term investors.

See, demand for healthcare does not correlate with economic cycles.

If one has a serious health issue, rectifying the issue is all that matters to that person at that point in time.

The GDP, or some other economic consideration, is inconsequential.

Well, to this point, health issues are a common feature of the human condition – human bodies slowly deteriorate as they age.

This means there’s a constant base level of demand for healthcare through existence alone.

Building on this, three demographic trends are combining to create secular growth across global healthcare.

First, our global population is growing.

Second, people are, on average, living longer than ever before.

Third, the wealth of the average person continues to rise.

A greater number of older and wealthier human beings walking around almost guarantees increased demand for quality healthcare.

That’s global healthcare, in general.

But Medtronic, in particular, is beneficially situated within the global healthcare complex.

It comes down to the inelastic demand for its products.

The spending on these products is usually non-discretionary in nature, especially if it’s a life-or-death circumstance that does not lend itself to price sensitivity or negotiation.

Let’s say, for example, you need emergency surgery – one is much more concerned with survival than the exact pricing of the medical devices needed to save one’s life.

If all of this weren’t alluring enough, Medtronic also has market leadership in the areas in which it competes.

Morningstar puts it like this: “Medtronic has historically held roughly 50% share in its core heart devices. It’s also the market leader in spinal products, insulin pumps, and neuromodulators for chronic pain.”

It’s hard to imagine Medtronic not doing very well over the long run, which should translate to growth across its revenue, profit, and dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

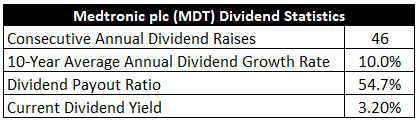

To date, the company has increased its dividend for 46 consecutive years.

That’s not only one of the longest dividend growth track records in healthcare but in all of Corporate America.

It easily qualifies Medtronic for its status as an esteemed Dividend Aristocrat.

The 10-year dividend growth rate of 10% is strong, although more recent dividend raises have been modest.

Medtronic has been challenged over the last few years by the pandemic, as elective procedures were delayed.

This headwind has been dissipating, however, which sets up Medtronic for a big bounce in sales.

And the stock is offering a nice 3.2% yield while you wait for that to play out.

And the stock is offering a nice 3.2% yield while you wait for that to play out.

Notably, that market-beating yield is 90 basis points higher than its own five-year average.

Despite that yield being so much higher than it usually is, the payout ratio is a reasonable 54.7% (based on midpoint guidance for FY 2024 adjusted EPS).

I like dividend growth stocks in what I call the “sweet spot” – a yield of between 2.5% and 3.5%, paired with a high-single-digit (or higher) dividend growth rate.

We’re right in the sweet spot here.

Revenue and Earnings Growth

Be that as it may, these metrics are mostly looking backward.

However, investors must look forward – today’s capital is being risked for tomorrow’s rewards.

Therefore, I’ll now build out a forward-looking growth trajectory for the business, which will be instrumental when the time comes later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then unveil a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should allow us to roughly gauge where the business could be going from here.

Medtronic moved its revenue from $17 billion in FY 2014 to $31.3 billion in FY 2023.

That’s a compound annual growth rate of 7%.

I’m usually looking for a mid-single-digit top-line growth rate from a mature business like this.

Medtronic more than delivered.

However, a major chunk of this revenue growth resulted from the acquisition of Covidien PLC in 2015 for almost $50 billion.

This complementary addition to the company (with Covidien focusing on endomechanical instruments, adding to Medtronic’s cardiovascular and orthopedic offerings) gave a large boost to the business in absolute terms.

Relative profit growth, on a per-share basis, should better inform us.

Earnings per share grew from $3.02 to $5.29 (adjusted) over this period, which is a CAGR of 6.4%.

Even during a really tough period, which unfairly and inaccurately skews recent results downward, Medtronic still put up respectable numbers.

This business could have done better, if not for two serious headwinds (one of which is not the company’s fault).

First, Medtronic’s outstanding share count has been increased significantly as a result of the company using equity to help finance the Covidien acquisition.

This has made growth on a per-share basis more onerous.

Second, the pandemic has acutely affected Medtronic.

The overwhelming focus on the pandemic by the global healthcare complex led to the delaying of anything that could be delayed (such as elective surgeries).

Worse yet, key product launches coincided with the onset of the pandemic and the lessened demand.

In addition, the pandemic made it difficult to bring new supply to market.

Put simply, Medtronic has been facing both supply and demand challenges over the last three years.

But this coin has a flip side.

Surgeries that could not be performed previously are almost certainly demand deferral, not demand destruction.

These delays could be causing pent-up demand, which would be a strong driver of accelerated growth for the business over the next few years.

Furthermore, the arrival of new products to the market precisely at the same time as rising demand could be a potent mix for the business, turning a former headwind into a new tailwind.

Looking forward, CFRA believes that Medtronic will grow its EPS at a CAGR of 4% over the next three years.

It appears to me that CFRA is forecasting a lingering hangover from the pandemic.

Indeed, CFRA states: “We see growth picking up to 5% in FY 25 with pandemic disruptions to supply and demand finally ending, in our view.”

I think residual effects are still present, but will they last into FY 2025?

Hard to say.

Either way, Medtronic is positioned really well for a full recovery.

To that point, CFRA states: “We expect strong results from [Medtronic] as its health care provider customers serve pent-up demand for procedures that had to be postponed due to the pandemic and then subsequent staffing shortages at medical facilities. [Medtronic] also stands out from medical device peers because of its product innovation and new launches, which drove market share gain during the pandemic and should continue to do so over the longterm. One product line that has particularly immense potential is [Medtronic’s] robotic assisted surgery platform, which we see ultimately being adopted worldwide, up from around 13 countries using the technology in FY 23.”

The company’s new robotic-assisted surgery offering, Hugo, which CFRA is referring to, is promising.

If we move past the shaky near term, the long-term picture looks bright.

Dividend raises over the next year or two are likely to be small, sure.

But I see a good chance of Medtronic returning to its glory years after marching through this temporary setback.

If the business can produce high-single-digit dividend growth, which it seems fully capable of, that’s a compelling offer on top of the 3%+ starting yield.

Moving over to the balance sheet, Medtronic has a solid financial position that should improve as the business rebounds.

Financial Position

The long-term debt/equity ratio is 0.5, while the interest coverage ratio is nearly 10.

Profitability is good now, but I think this is another area of the business that can, and likely will, improve as the entire operating environment normalizes.

Over the last five years, the firm has averaged annual net margin of 13.8% and annual return on equity of 8.2%.

Medtronic was producing net margin closer to 16% before the pandemic hit, so there’s a lot of room for margin expansion here.

Medtronic has lost some luster, but it’s in a great position to return to its former glory as supply and demand shocks fade.

And with IP, R&D, switching costs, economies of scale, a global distribution network, high barriers to entry, and a diversified portfolio of entrenched products, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

All three of these risks are elevated for this business model in comparison to many other business models, in my view.

Any changes in the way healthcare spending is managed, especially in the United States, would almost certainly impact the company.

Medtronic occasionally recalls products, which involves cost and reputation risks.

Demand for medical devices is fairly disconnected from economic cycles, but a recession could cause people to delay or cancel elective surgeries.

Any major technological changes in medical devices can alter the competitive landscape, which pressures Medtronic to constantly innovate and stay ahead of the tech curve.

Every business has risks – Medtronic is no different – but I think the long-term reward picture here is compelling.

Making that picture look even more compelling is the valuation, which appears to be quite attractive after the stock’s 35% fall from its 2021 high…

Stock Price Valuation

The P/E ratio is 16.6, using adjusted EPS.

That’s measurably lower than the broader market’s earnings multiple.

It’s also favorable in comparison to the stock’s five-year average P/E ratio of 34.4, but frequent adjustments make it impossible to accurately compare.

A better comparison would be to look at the sales multiple, which doesn’t suffer from the same adjustments.

The current P/S ratio of 3.8 is quite a bit lower than its own five-year average of 4.5.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

This dividend growth rate looks conservative against the demonstrated dividend growth over the last decade.

And it’s also lower than the rate I’ve used in the past for Medtronic.

I’ve become slightly less sanguine about the prospects due to the possibility of lasting scars on the business.

Moreover, the EPS CAGR over the last decade is lower than this mark, and some of the prior dividend raises, which were sizable, came at the expense of expanding the payout ratio.

Keep in mind, the most recent dividend raise was only 1.5%.

Also, the near-term forecast for EPS growth is lackluster.

Honestly, it’s difficult to get a real handle on Medtronic.

There are a lot of moving parts, and unprecedented hits to both supply and demand aren’t helping.

The last few years have been so tough, but I don’t see why the business can’t mount a serious comeback – even if it takes a few years to fully flesh it out.

It’s probably unreasonable to expect too much from Medtronic over the next 12-24 months, but I believe dividend growth could return in a big way when looking out past FY 2025.

I’m averaging things out here, with a lot of the growth weighted out past the next year or two.

The DDM analysis gives me a fair value of $98.44.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think my valuation model was justifiable, yet the stock looks cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates MDT as a 4-star stock, with a fair value estimate of $112.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates MDT as a 4-star “BUY”, with a 12-month target price of $97.00.

I came out very close to where CFRA is at, although we’re all in a pretty close range. Averaging the three numbers out gives us a final valuation of $102.48, which would indicate the stock is possibly 14% undervalued.

Bottom line: Medtronic PLC (MDT) has been directly impacted by the pandemic, both in terms of supply and demand, but it’s positioned well for an explosive rebound. With a market-beating yield, a double-digit long-term dividend growth rate, a reasonable payout ratio, almost 50 consecutive years of dividend increases, and the potential that shares are 14% undervalued, long-term dividend growth investors would be wise to take a good look at this Dividend Aristocrat right here, right now.

Bottom line: Medtronic PLC (MDT) has been directly impacted by the pandemic, both in terms of supply and demand, but it’s positioned well for an explosive rebound. With a market-beating yield, a double-digit long-term dividend growth rate, a reasonable payout ratio, almost 50 consecutive years of dividend increases, and the potential that shares are 14% undervalued, long-term dividend growth investors would be wise to take a good look at this Dividend Aristocrat right here, right now.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is MDT’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, MDT’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income