I love, love, love being a dividend growth investor.

I wake up. Dividends. I go to sleep. Dividends. I eat. Dividends.

No matter where I go, I’m getting paid dividends. But that’s not totally accurate. I’m actually getting paid more and more dividends.

That’s because of the growth in dividend growth investing, which refers to dividend growth. When you invest in great businesses that pay reliable, rising dividends, your totally passive dividend income is rising, like clockwork, all by itself.

Want to see what that looks like? Okay.

Today, I want to tell you about six dividend growth stocks that just increased their dividends.

Ready? Let’s dig in.

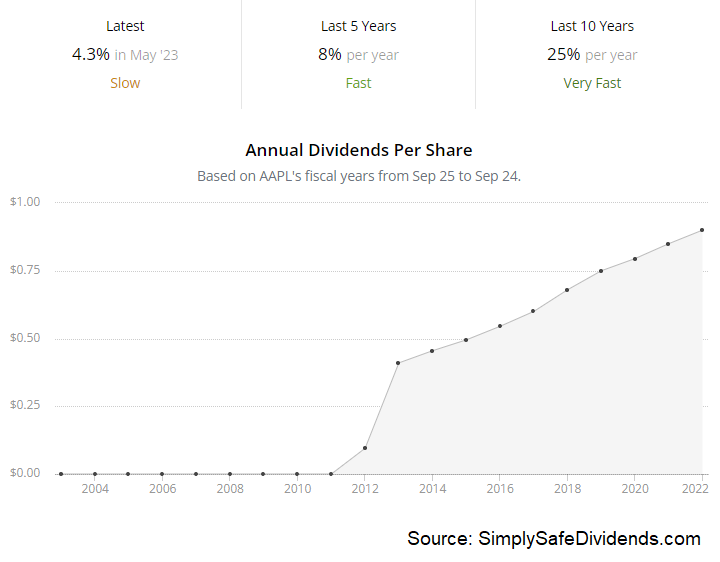

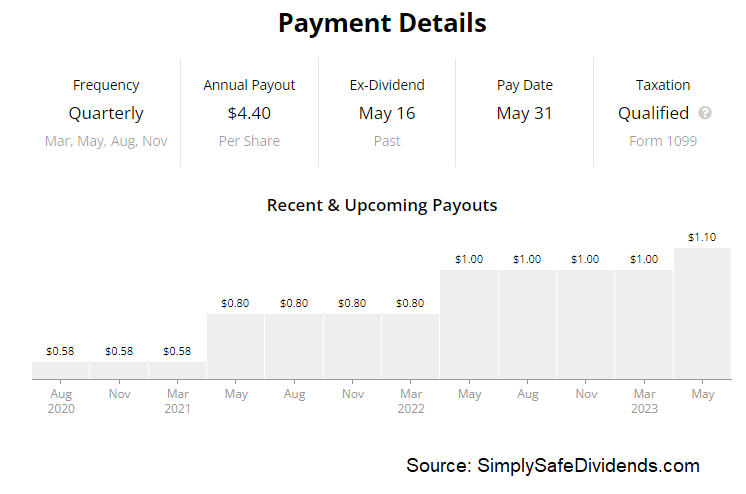

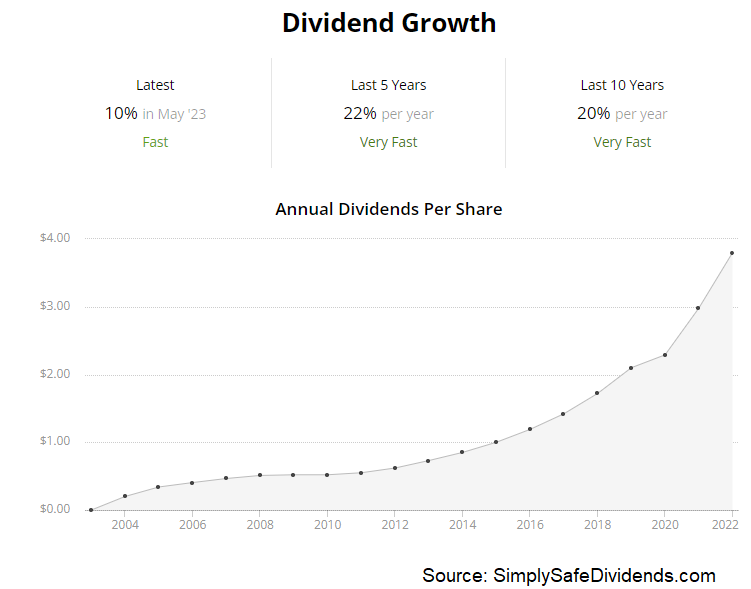

he first dividend increase I have to bring to your attention is the one that was announced by Apple (AAPL). Apple just increased its dividend by 4.3%.

I know. Not huge. Not what many Apple shareholders were expecting. But, look, dividend increases aren’t uniform. When you look at a long-term dividend growth rate, there will be some highs and lows in there – but it all averages out nicely in the end. Besides, this is 4.3% more passive income… for doing nothing. Pretty tough to complain. This is the 12th consecutive year of dividend increases for the multinational technology company.

The 10-year DGR is 17%, but Apple has kind of fallen into the mid-to-high-single-digit area in terms of annual dividend increases. Now, I wouldn’t expect 4% to be the new norm. But 17% also isn’t an accurate representation of what’s going on.

With the yield at only 0.6%, one really wants to see at least high-single-digit dividend raises here. Otherwise, it’s hard to make sense of the numbers. With a payout ratio of only 16.3%, along with billions of dollars of cash on the balance sheet, Apple can certainly afford to hand out very generous dividend increases in the years ahead.

With the yield at only 0.6%, one really wants to see at least high-single-digit dividend raises here. Otherwise, it’s hard to make sense of the numbers. With a payout ratio of only 16.3%, along with billions of dollars of cash on the balance sheet, Apple can certainly afford to hand out very generous dividend increases in the years ahead.

This might just be the best business on the entire planet. But don’t take my word for it. At this year’s Berkshire Hathaway shareholders meeting, Warren Buffett came out and said that Apple is a better business than any business Berkshire Hathaway owns outright.

Think about that for a minute. Buffett is arguably the greatest investor of all time. He’s spent his entire life assembling a collection of businesses, which he’s turned into a giant conglomerate. And, yet, he believes Apple is better than all of it. In my view, Apple’s valuation looks a bit stretched here. The P/E ratio of 29.8, for instance, is running well ahead of its own five-year average of 24.8. But if we get a sizable dip in the stock’s price, be prepared to act.

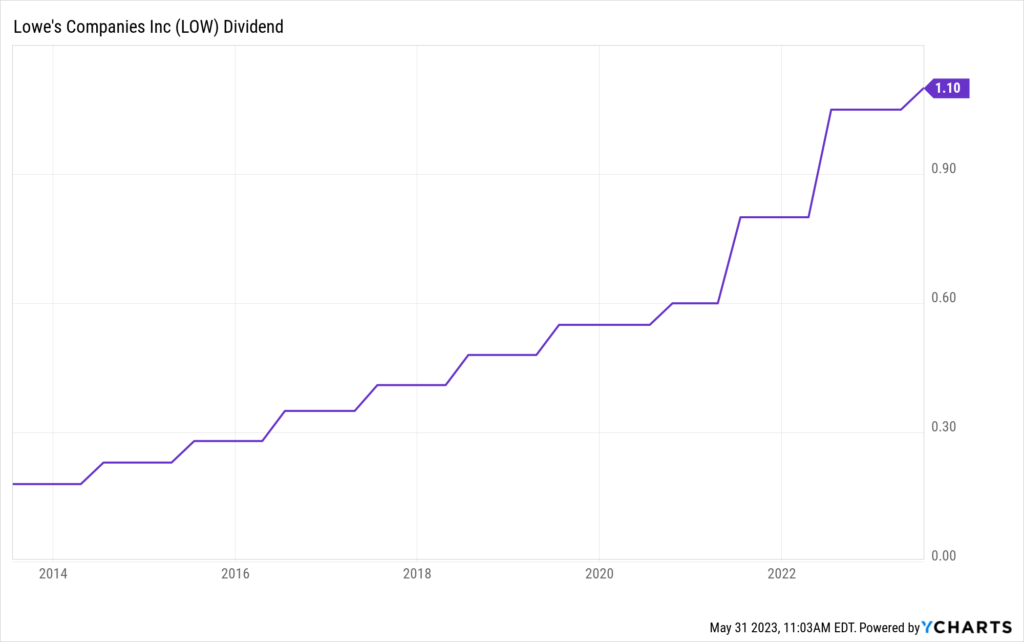

The second dividend increase I have to call out today is the one that came in from Lowe’s Companies (LOW). Lowe’s just increased its dividend by 4.8%.

Two ways to look at this. You could say it’s only a mid-single-digit increase when inflation is pretty high. Or, you could say that Lowe’s still came through, yet again, with a decent bump in its dividend, despite a really tough operating environment. I prefer the latter viewpoint, which is a case of the glass being half full.

The home improvement retailer has now increased its dividend for 61 consecutive years. Lowe’s is a Dividend Aristocrat and a Dividend King. Not many of them out there, which just goes to show how unusually reliable this company has been.

The 10-year DGR is 20%. And that’s also been something that Lowe’s has been pretty reliable with. This year’s dividend increase came in well under the mark. However, keep in mind, last year’s dividend increase was a whopping 31.3%! Like I said earlier, things tend to average out nicely. The stock’s yield is now 2%, which is above its own five-year average. And the payout ratio is 40.7%, which is still pretty moderate. Fantastic dividend metrics here.

The 10-year DGR is 20%. And that’s also been something that Lowe’s has been pretty reliable with. This year’s dividend increase came in well under the mark. However, keep in mind, last year’s dividend increase was a whopping 31.3%! Like I said earlier, things tend to average out nicely. The stock’s yield is now 2%, which is above its own five-year average. And the payout ratio is 40.7%, which is still pretty moderate. Fantastic dividend metrics here.

This Dividend Aristocrat looks undervalued to me. Not hugely undervalued. Not super cheap. But I think we’ve got a decent deal on a terrific business. We recently put together a full analysis and valuation video on Lowe’s, estimating fair value for the business at $226.60/share. And that was before this dividend boost, which only makes the equity that much more valuable. If your portfolio has room for a great retailer profiting from the American Dream, Lowe’s has to be on your radar.

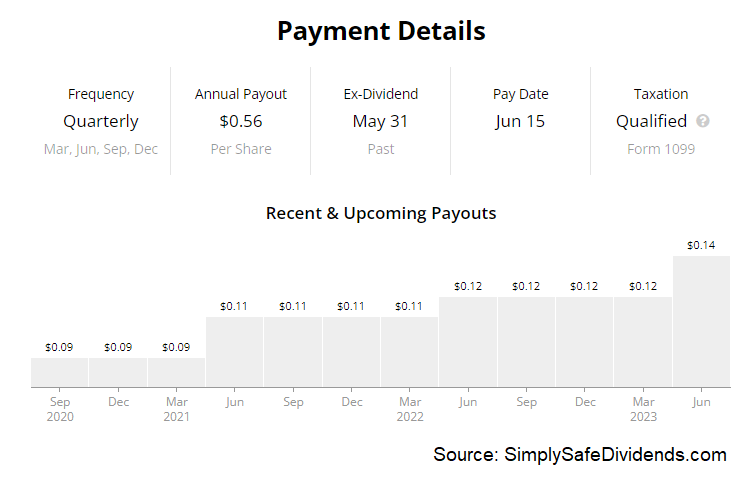

The third dividend increase I want to tell you about is the one that came courtesy of Main Street Capital (MAIN). Main Street Capital just increased its dividend by 2.2%.

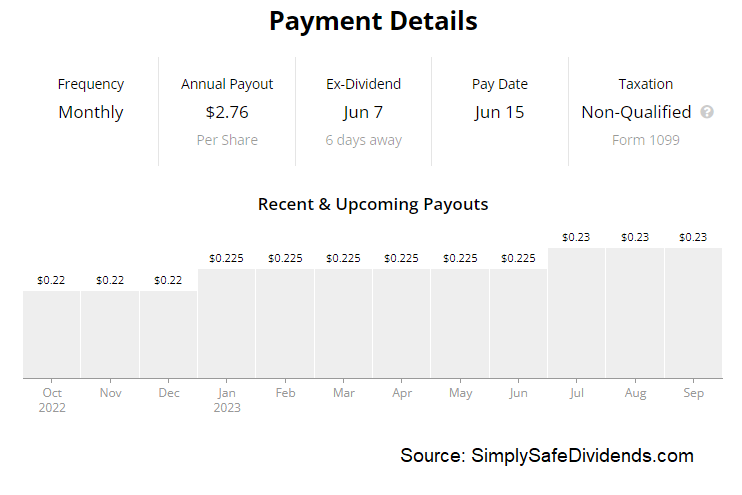

Another somewhat small dividend increase? What gives? Well, I’ll you what gives. Main Street Capital isn’t about huge dividend increases. It’s instead all about a big, juicy, monthly dividend that rises slightly every year. This marks the 14th consecutive year of dividend increases for the business development company.

So what was I just saying? Oh, yeah. Big, juicy, monthly dividend. Indeed, Main Street Capital does pay its dividend monthly. How juicy is it? Well, the stock yields 6.8% here. Not bad at all, right? Well, it’s better than it sounds. Main Street Capital tends to pay out supplemental dividends. When you factor those in, the yield can be well over 10%! And you get to pair that high yield with the 10-year DGR of 4.3%. Based on reported net investment income for the most recent quarter, the payout ratio is sitting at 67.6%.

So what was I just saying? Oh, yeah. Big, juicy, monthly dividend. Indeed, Main Street Capital does pay its dividend monthly. How juicy is it? Well, the stock yields 6.8% here. Not bad at all, right? Well, it’s better than it sounds. Main Street Capital tends to pay out supplemental dividends. When you factor those in, the yield can be well over 10%! And you get to pair that high yield with the 10-year DGR of 4.3%. Based on reported net investment income for the most recent quarter, the payout ratio is sitting at 67.6%.

This is one of the very few high-yield dividend growth stocks I like. Most of the high-yield stuff is junk that entices yield chasers. But Main Street Capital is a high-quality BDC that provides customized debt and equity financing to smaller companies that lack traditional financing options.

They have been putting up really impressive numbers for many, many years now. I’m usually leery of high yield, in general, and BDCs, in particular, but Main Street Capital has proven itself to be a winner. If we extrapolate net investment income out and do an annualized run-rate, the multiple is sitting at 9.3. I don’t think that’s unreasonable at all.

Also, that aforementioned 6.8% yield is 30 basis points higher than its own five-year average. You have to be careful with BDCs and thoughtfully right-size that exposure. But Main Street Capital is one of the very few that appears to be worth considering.

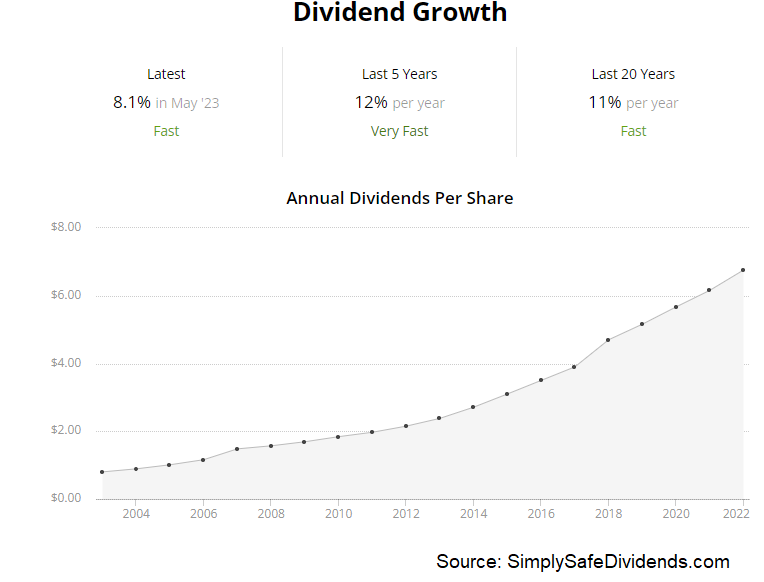

The fourth dividend increase we need to have a quick conversation about is the one that came from Northrop Grumman (NOC). Northrop Grumman just increased its dividend by 8.1%.

Now we’re talking, right? Shareholders must be grinning from ear to ear. This is 8.1% more money. And not just more money, but more passive money. And the raise itself was passive. Just blows my mind sometimes.

The multinational aerospace and defense technology company has now increased its dividend for 20 consecutive years.

Good stuff. The 10-year DGR is 12.1%. We’re a bit light this year, but it’s still a very nice dividend bump. A drawback here might be the yield, which is only 1.7%. But that’s pretty close to its own five-year average. This is a stock that typically has a pretty low yield, which reflects the growth. With a 24.2% payout ratio, you can obviously see that there’s plenty of growth ahead for this dividend.

Good stuff. The 10-year DGR is 12.1%. We’re a bit light this year, but it’s still a very nice dividend bump. A drawback here might be the yield, which is only 1.7%. But that’s pretty close to its own five-year average. This is a stock that typically has a pretty low yield, which reflects the growth. With a 24.2% payout ratio, you can obviously see that there’s plenty of growth ahead for this dividend.

If you’re looking for defense exposure, you have to be looking at Northrop Grumman. This company’s high growth rate is a result of the forward-looking programs it caters to, such as space-based security solutions. It’s new tech and new defense.

This stock is more than 20% off of its 52-week high, and this crash in pricing has created what looks like a pretty nice entry point for long-term dividend growth investors. The P/E ratio has fallen to 14.2, which is comfortably below its own five-year average of 17.3. Most multiples are showing something similar. It’s been a minute since we’ve fully covered this one, and this drop in price prompts an update. Meantime, take a good look at Northrop Grumman.

The fifth dividend increase I have to cover is the one that came through from Pool Corporation (POOL).

Pool just increased its dividend by 10%. Pool flies under the radar, but it’s been a stout dividend grower for years now. It just keeps handing out the double-digit dividend raises. Companies like Pool make it look easy, even though it’s not.

This is the 13th consecutive year in which the swimming pool products company has increased its dividend. And what a start Pool is off to. The 10-year DGR is 19.9%. While this year’s dividend increase is obviously under that mark, last year’s massive 25% dividend increase means you average out quite nicely.

This is the 13th consecutive year in which the swimming pool products company has increased its dividend. And what a start Pool is off to. The 10-year DGR is 19.9%. While this year’s dividend increase is obviously under that mark, last year’s massive 25% dividend increase means you average out quite nicely.

On the other hand, you do sacrifice some yield in order to access this high dividend growth rate. The stock’s yield is just 1.3%. But anyone focusing on that alone is totally missing the big picture, which is one of total return. This stock is up by more than 500% over the last decade, and there could be a lot more where that came from. Meantime, with a payout ratio of 26.1%, I suspect we’re looking at plenty more double-digit dividend raises to keep powering things higher.

On the other hand, you do sacrifice some yield in order to access this high dividend growth rate. The stock’s yield is just 1.3%. But anyone focusing on that alone is totally missing the big picture, which is one of total return. This stock is up by more than 500% over the last decade, and there could be a lot more where that came from. Meantime, with a payout ratio of 26.1%, I suspect we’re looking at plenty more double-digit dividend raises to keep powering things higher.

Every single multiple here is below its respective recent historical average. This is the kind of dividend growth stock that usually commands high multiples. For example, its five-year average P/E ratio is 31.5. That’s up there with tech companies.

However, the P/E ratio is currently 19.4. Indeed, this stock is more than 40% off of its all-time high, reached during the stock market mania of 2021. Recent results have been lapping really tough comps, so you must have a vision about the long-term market for pools, but this could be a base for another huge multiyear run. I think it’s definitely interesting.

The sixth dividend increase I must share with you is the one that arrived from Advanced Drainage Systems (WMS). Advanced Drainage Systems just increased its dividend by 16.7%.

Bam! How about that? Nearly 17% more passive dividend income for doing nothing other than sitting on your hands and not selling shares you already bought a while ago. That’s the life of a dividend growth investor.

The pipe and drainage company has now increased its dividend for 10 consecutive years. This year’s dividend increase may have caught shareholders by surprise. The five-year DGR is 11.7%. And most dividend raises have been right in that range, except this year’s monster.

The pipe and drainage company has now increased its dividend for 10 consecutive years. This year’s dividend increase may have caught shareholders by surprise. The five-year DGR is 11.7%. And most dividend raises have been right in that range, except this year’s monster.

That said, you would kind of expect double-digit dividend growth here, as the stock’s yield is only 0.6%. Without double-digit dividend growth, it’s hard to accept a yield that low. Again, though, this is really more of a compounder – the stock’s 250% rise over just the last five years alone oughta clue you into that. With an extremely low payout ratio of just 9.2%, which is one of the lowest I’ve ever seen, this dividend has a long compounding runway in front of it.

This is another business lapping tough comps, but there’s also been a nice valuation reset here.

Indeed, the stock is down 35% from its all-time high. It’s a lot like the aforementioned Pool. Tough comps, and recent results have reflected this. But you’ve also had a pretty big compression in multiples. We see a five-year average P/E ratio of 31.5 for the business, which is just like Pool.

And, like Pool, we’re now looking at a big discount from that level, with the stock’s current P/E ratio sitting at 16. This one is a tough call, as the last few years have shown an explosion in growth that doesn’t match up well with anything prior to the pandemic. But if this is a “new normal” for the business, it’s an awfully compelling idea. Take a close look at it.

— Jason Fieber

Source: Dividends & Income