The US stock market is a wealth-building machine. But it’s also a machine that tests patience and rewards those who can pass.

Warren Buffett put it like this:

“The stock market is a device for transferring money from the impatient to the patient.”

Passing this test over the long run requires you to deal with volatility. Stock prices can drop dramatically in short periods of time, but this isn’t necessarily a bad thing at all.

Price and yield are inversely correlated.

All else equal, lower prices result in higher yields. This means more dividend income on the same invested dollar, making financial independence an easier and faster target to reach.

I always see short-term volatility as a long-term opportunity. That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint.

All that said, it’s a big market, and some ideas are better than others. Focusing on the very best long-term ideas right now is what this article is all about.

Today, I want to tell you my top 5 dividend growth stocks for June 2023.

Ready? Let’s dig in.

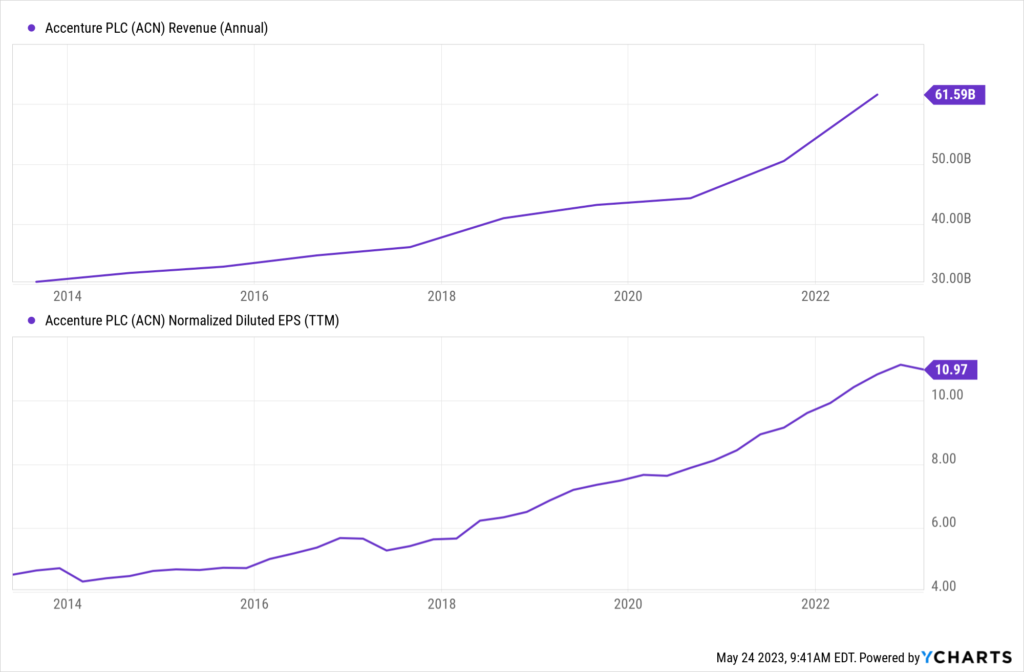

My first dividend growth stock for June 2023 is Accenture (ACN). Accenture is a professional services company specializing in IT services and consulting.

Accenture should be called “accelerate” – as in, accelerate your wealth, passive income, and financial freedom, assuming you’re a shareholder. And why is that? Because Accenture is accelerating solutions for its clients. See, enterprises have all kinds of problems. Properly navigating the digital transformation could be one example.

Formulating a strategy for entering new markets might be another example. Well, Accenture helps to solve enterprise problems just like these. The combinations of enterprises, problems, and solutions are nearly endless. And that’s exactly why Accenture has put up an 8.2% CAGR in revenue and 9% CAGR in EPS over the last decade.

Solid, consistent business growth is what’s fueled solid, consistent dividend growth.

Solid, consistent business growth is what’s fueled solid, consistent dividend growth.

Accenture has already increased its dividend for 18 consecutive years. I’m highly confident that it’ll be a Dividend Aristocrat in about seven years. The 10-year DGR is 10.5%. That’s slightly outpaced EPS growth, but the low payout ratio of 38.8% still offers some flexibility here. The only drawback to the stock might be its yield, which is only 1.6%. But this is a very high-quality compounder, not high-yield junk.

Accenture isn’t super cheap. It never really is. But I think it’s decently undervalued. And that’s enough, in my opinion. If you want single-digit P/E ratios and 10% yields, you can get that elsewhere in the market. Of course, those are also where poor total returns are usually found. This stock, on the other hand, has compounded at an annual rate of nearly 15% over the last decade. What a winner.

We recently put together a full analysis and valuation video on Accenture, and that video showed why this world-class compounder is estimated to be worth right about $310/share. The stock has already moved up since that video came out, but the pricing of $290 still offers some potential upside. Make sure you take a good look at this one.

My second dividend growth stock for June 2023 is BlackRock (BLK). BlackRock is a multinational investment management corporation.

Well, that’s not quite right. BlackRock is the world’s largest investment management corporation. No competitor is bigger. And it could be argued that no competitor does it better. This is a field in which size truly does matter, as you’re benefiting from the rising tide of capital markets lifting all boats… except BlackRock is the biggest boat, and that disproportionately benefits the firm. That explains why BlackRock has compounded its revenue at an annual rate of 6.5% and its EPS at an annual rate of 8.1% over the last decade.

BlackRock is a dividend rock. The asset manager has increased its dividend for 14 consecutive years, with a 10-year DGR of 12.5%. And the stock yields an even 3% right now. That’s a very nice combination of yield and dividend growth.

You’re beating the broader market on yield, and you’re outpacing inflation with the dividend growth. Hard to complain about that. The payout ratio of 62% is elevated, but that’s mostly a function of temporarily depressed earnings on the back of a tough stretch for markets.

You’re beating the broader market on yield, and you’re outpacing inflation with the dividend growth. Hard to complain about that. The payout ratio of 62% is elevated, but that’s mostly a function of temporarily depressed earnings on the back of a tough stretch for markets.

It’s also been a tough stretch for this stock, which has led to what I think is a pretty reasonable valuation.

Shares were trading hands for nearly $1,000/each not long ago. They’re now down to about $667/each. It might have gotten ahead of itself at the top, just like a lot of stocks did, but is it still ahead of itself? I don’t think so. The 30%+ collapse in pricing has compressed the valuation down to a much more reasonable level. The P/E ratio of 20.7 is a good example of that.

Is that not sensible for a company of this stature, quality, and positioning? I’d argue it is. And I do argue that in a full analysis and valuation video on BlackRock, which should already be live very soon. In that video, I calculate an estimate of fair value to be $825/share for the business – decently above current pricing. If you haven’t considered BlackRock before, now would be a good time to change that.

My third dividend growth stock for June 2023 is Essex Property Trust (ESS). Essex Property Trust is a multifamily property real estate investment trust.

REITs can be super hit-and-miss, just like anything else. Some REITs have definitely seen their better days, especially if their business model is catering to the real estate of yesteryear. Think poorly-located, dreary shopping malls. Think Class C office buildings. But Essex Property Trust suffers from none of this.

First, it caters to a basic need that people can’t live without – shelter. We’re talking about apartments here. Second, its portfolio of properties are high-quality, newer assets in high-quality, naturally desirable locations. That’s why it continues to put up strong numbers for a REIT. Revenue has compounded at an annual rate of 11.3% over the last decade, while FFO/share compounded at an annual rate of 6.8% over that time frame.

What more evidence of strength? This is a rare Dividend Aristocrat. It’s one of only three REITs that can claim that special status. Essex Property Trust has increased its dividend for 29 consecutive years. What’s so impressive about this is that it dates all the way back to the REIT’s original 1994 IPO.

The 10-year DGR of 7.2% lines up very nicely with FFO/share growth over the same stretch. And you’re pairing that solid dividend growth with the stock’s market-smashing 4.4% yield. With the payout ratio sitting at 62.5%, Essex Property Trust is positioned to keep its Dividend Aristocrat status for many years to come.

For years, this stock was so expensive. But not now.

I avoided Essex Property Trust for years and years out of valuation concerns. But, now, after a 40% collapse from its all-time high in price, which was reached not long ago, the valuation has become more attractive than I’ve ever seen it. Its five-year average P/CF ratio is 20.6. Pricey. It’s now 14.6, which is downright cheap.

We put together a full analysis and valuation video on Essex Property Trust, which should be live soon, and you can see why the REIT could be worth almost $271/share. The stock’s pricing of about $210 obviously compares very favorably to that. This might be a short window of opportunity in which this high-quality Dividend Aristocrat is buyable.

We put together a full analysis and valuation video on Essex Property Trust, which should be live soon, and you can see why the REIT could be worth almost $271/share. The stock’s pricing of about $210 obviously compares very favorably to that. This might be a short window of opportunity in which this high-quality Dividend Aristocrat is buyable.

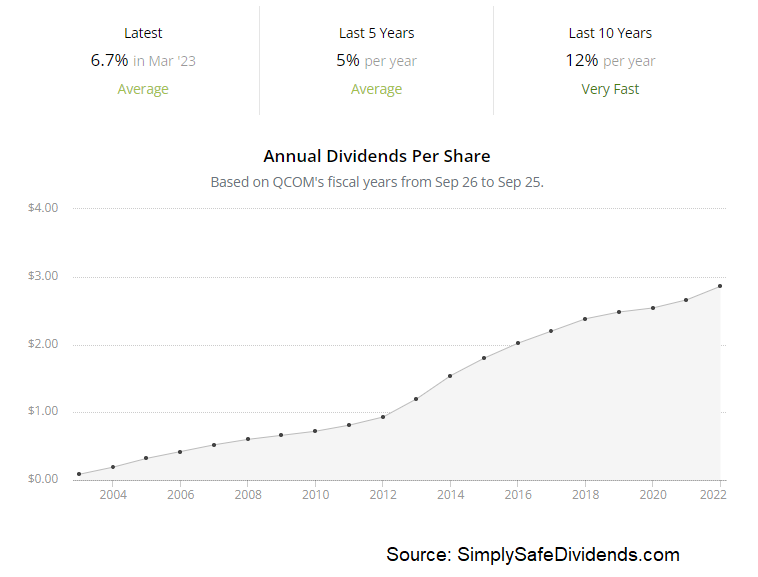

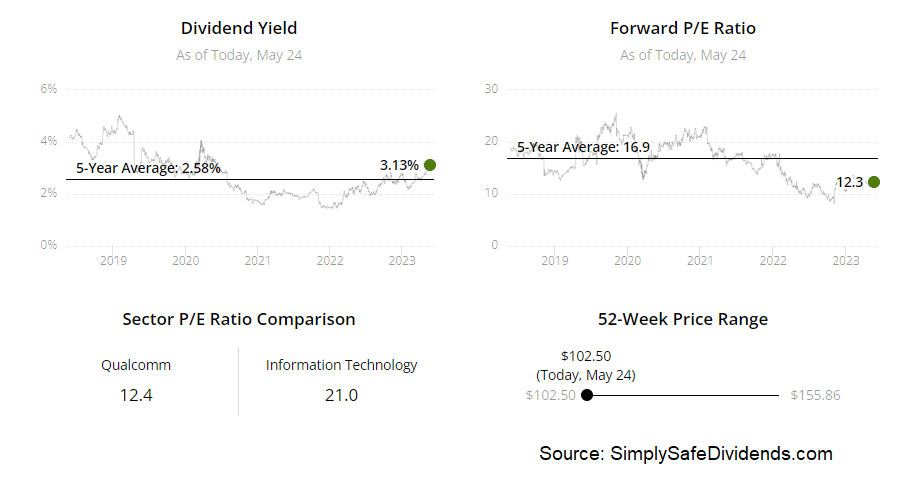

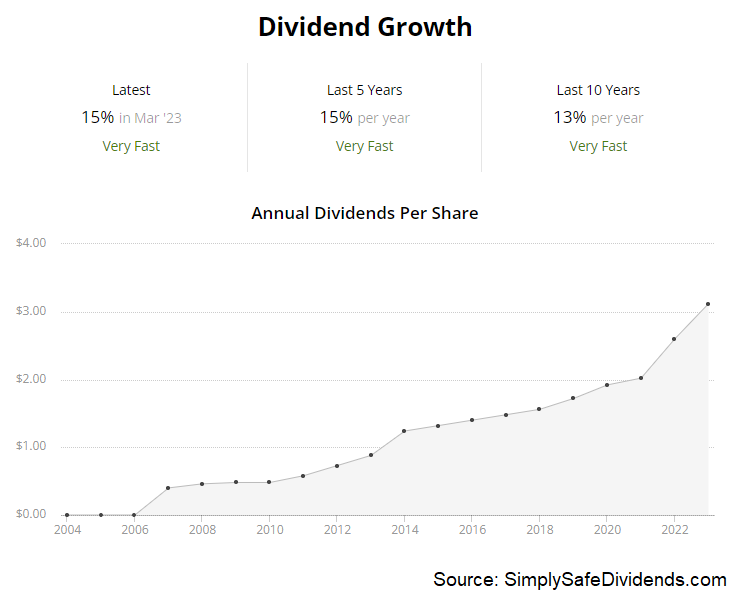

My fourth dividend growth stock for June 2023 is Qualcomm (QCOM). Qualcomm is a multinational technology corporation.

In my view, Qualcomm has transformed itself from a strong company into an even stronger company. Qualcomm took a lucrative base of handset IP and parlayed that into a diversified tech behemoth with exposure to 5G, broadband, modern RF systems, gaming, IoT, self-driving autos, AI, and AR/VR. And that’s fueled great top-line and bottom-line growth over a sustained period of time. Revenue has compounded at an annual rate of 6.6% over the last decade, while EPS compounded at an annual rate of 12.6% over that stretch.

Double-digit bottom-line growth has fueled double-digit dividend growth. The 10-year DGR is 11.7%. And you can see how well that lines up with bottom-line growth. Management has been on the ball here. This is a dividend that has been increased for 21 consecutive years. Only a few years away from vaunted Dividend Aristocrat status.

The stock yields 3%, which easily beats what the broader market gives you. And the low payout ratio of only 30.9% gives Qualcomm plenty of headroom on the dividend. I see many years of dividend raises ahead.

The stock yields 3%, which easily beats what the broader market gives you. And the low payout ratio of only 30.9% gives Qualcomm plenty of headroom on the dividend. I see many years of dividend raises ahead.

This might be one of the best long-term investment opportunities in all of tech right now.

This stock was running close to $200 just over a year ago. It’s now treading the $100 area. So the stock got cut nearly in half, yet I don’t see anything in the business, in terms of its long-term potential, to warrant it.

We recently analyzed and valued Qualcomm, and the video on that should be going live soon, if it hasn’t already. The valuation came out to $139.20/share. So it looks about 20% undervalued right now. This is a great business. And unlike almost everything else in tech, the valuation is very undemanding. Take a look.

We recently analyzed and valued Qualcomm, and the video on that should be going live soon, if it hasn’t already. The valuation came out to $139.20/share. So it looks about 20% undervalued right now. This is a great business. And unlike almost everything else in tech, the valuation is very undemanding. Take a look.

My fifth dividend growth stock for June 2023 is Williams-Sonoma (WSM). Williams-Sonoma is a multi-channel retailer of high-quality home products and furnishings.

The issues that plague many retailers out there do not plague Williams-Sonoma, and that’s because the company saw the curve coming and prepared for change. A prime example of this is e-commerce, the bane of many B&M retailers.

Williams-Sonoma made e-commerce a pillar of the company’s selling strategy years ago. The e-commerce channel now makes up 2/3rds of the company’s sales. This forward-thinking retailer dazzles across the board, including growth – a 7.9% CAGR for revenue and 21.5% CAGR for EPS over the last decade.

The dividend also dazzles. Williams-Sonoma has increased its dividend for 18 consecutive years. And this is not like some of those other retailers out there handing out tiny annual dividend increases in order to keep a streak alive.

No, the 10-year DGR for Williams-Sonoma is 13.2%. And you get to pair that double-digit dividend growth with the stock’s starting yield of 3.2%. Not dazzled enough yet? Okay. The payout ratio is just 22.1%, even after all of those big dividend raises. Incredible stuff here.

No, the 10-year DGR for Williams-Sonoma is 13.2%. And you get to pair that double-digit dividend growth with the stock’s starting yield of 3.2%. Not dazzled enough yet? Okay. The payout ratio is just 22.1%, even after all of those big dividend raises. Incredible stuff here.

I think this high-quality dividend growth stock is severely undervalued. I’m not sure why Williams-Sonoma doesn’t get the love it ought to. Other than a brief time during the market’s 2021 manic episode, this is a stock that consistently flies under the radar and commands low multiples.

I mean, the P/E ratio, right now, is below 7. We just combed through this business, and the video going over that should be live soon. The valuation estimate on the business worked out to just over $165/share. The stock is currently priced at about $112. We’re talking about the potential for more than 30% undervaluation. Want a terrific business at a low valuation? Williams-Sonoma could perfectly fit the bill.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income