Albert Einstein was one of the smartest people who ever lived.

He could visualize and explain extremely complex and abstract concepts, like spacetime and time dilation.

Einstein’s mental horsepower was up to almost any task.

But even Einstein was blown away by the power of compounding.

Here’s one of many quotes attributed to Einstein on the subject of compounding: “The most powerful force in the universe is compound interest.”

If that doesn’t tell you that you need to put compounding in your corner as soon as possible, I’m not sure what will.

But how does one go about doing that?

Well, investing in wonderful businesses that can compound profits and dividends is a pretty good method.

That leads one right to dividend growth investing.

This is a strategy whereby one invests in high-quality businesses that pay reliable, rising dividends.

And by rising, we’re talking about compounding.

How are these businesses able to pay out ever-larger dividends to their shareholders?

By producing ever-more profit, of course.

It’s a virtuous circle.

It’s a virtuous circle.

Want to find some of these stocks.

Okay.

The Dividend Champions, Contenders, and Challengers list is comprised of hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years

I have another resource for you.

It’s my real-money portfolio, which produces enough five-figure passive dividend income to live off of.

I call it the FIRE Fund, and it’s chock-full of high-quality dividend growth stocks that I’ve personally bought with my own hard-earned money.

In fact, this portfolio allowed me to retire in my early 30s.

In fact, this portfolio allowed me to retire in my early 30s.

I explain exactly how such an early retirement is possible in my Early Retirement Blueprint.

A pillar of my success has been consistently rolling my savings into high-quality dividend growth stocks.

But valuation at the time of investment has also been very important.

Price only tells you what you pay, but it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Taking advantage generally of what Einstein viewed as the most powerful force in the universe, and doing so specifically with undervalued high-quality dividend growth stocks, sets one up for tremendous wealth, passive income, and freedom over the long run.

And if you think business valuation is something impossible to understand, think again.

My colleague Dave Van Knapp made it easy to grasp with his Lesson 11: Valuation.

Part of a larger, more comprehensive series of “lessons” that are designed to teach the dividend growth investing strategy from scratch, it provides an easy-to-follow valuation template that demystifies the entire valuation process.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Qualcomm, Inc. (QCOM)

Qualcomm, Inc. (QCOM)

Qualcomm, Inc. (QCOM) is a multinational technology corporation that creates semiconductors, software, and services related to wireless technology and connectivity.

Founded in 1985, Qualcomm is now a $130 billion (by market cap) tech monster that employs 51,000 people.

The company reports results across two business segments: Qualcomm CDMA Technologies (QCT), 85% of FY 2022 revenue; and Qualcomm Technology Licensing (QTL), 14%.

The world is becoming increasingly reliant on technology right across the board.

In particular, wireless technologies based around connectivity are becoming critical to everyday life.

A digital transformation is playing out, and it’s accelerating.

This was true before the pandemic hit.

But it’s even more true today, as we now have a greater number of people working remotely.

This digital transformation started with the PC, then the Internet.

It then hit another gear with the invention of the smartphone.

Well, Qualcomm has long been a leader in the wireless space, and the company holds virtually all essential patents used in 3G, 4G, and 5G networks.

Because of this, Qualcomm collects royalty income on the majority of 3G, 4G, and 5G handsets sold worldwide.

But wait.

There’s more.

We’re now entering the age of the Internet of Things, where everything from your watch to your car are digitally interconnected.

This directly benefits Qualcomm.

The company had the foresight to parlay their early IP success into a diversified business model that offers a suite of technologies and services across an entire IoT ecosystem.

The company is now exposed to some of the biggest trends in all of technology – e.g., 5G, broadband, modern RF systems, gaming, IoT, self-driving autos, AI, and AR/VR.

Simply put, Qualcomm is positioned to reap massive rewards from the accelerating digital transformation.

What that should mean is, growth across the company’s revenue, profit, and dividend for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

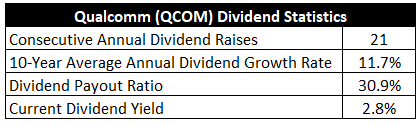

Already, Qualcomm has increased its dividend for 21 consecutive years.

Well on its way to becoming a Dividend Aristocrat.

The 10-year dividend growth rate of 11.7% is solid, although more recent dividend raises have been in the high-single-digit area.

Still, you’re able to pair that with the stock’s market-beating yield of 2.8%, which is basically right in line with its own five-year average.

And this appears to be a very safe dividend to me, as evidenced by the low payout ratio of 30.9%.

And this appears to be a very safe dividend to me, as evidenced by the low payout ratio of 30.9%.

I like dividend growth stocks in what I call the “sweet spot” – a yield of between 2.5% and 3.5%, paired with a high-single-digit (or higher) dividend growth rate.

We can see that Qualcomm is clearly right in that sweet spot, where you’re able to strike a nice balance between yield and growth.

Revenue and Earnings Growth

As sweet as these dividend metrics may be, they’re mostly looking in the rearview mirror.

However, investors must look through the windshield, as today’s capital is risked for tomorrow’s rewards.

This is why I’ll now build out a forward-looking growth trajectory for the business, which will later help when it comes time to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then uncover a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should allow us to judge where the business may be going from here.

Qualcomm advanced its revenue from $24.9 billion in FY 2013 to $44.2 billion in FY 2022.

That’s a compound annual growth rate of 6.6%.

Really good.

I usually look for a mid-single-digit top-line growth rate from a mature business like this.

Qualcomm more than delivered.

Meanwhile, earnings per share grew from $3.91 to $11.37 over this period.

That’s a CAGR of 12.6%.

Excellent bottom-line growth here.

And we can see a close relationship between EPS growth and dividend growth over the last decade, showing thoughtfulness and skill on the part of management.

Prolific buybacks account for a lot of the excess bottom-line growth.

For perspective, the outstanding share count is down by about 35% over the last 10 years.

That’s substantial.

Looking forward, CFRA believes that Qualcomm will compound its EPS at an annual rate of 1% over the next three years.

This seems awfully pessimistic to me.

Keep in mind, the last time I looked at CFRA’s three-year projection for Qualcomm’s EPS CAGR was almost exactly one year ago.

At that time, the number was 19%.

Going from 19% to 1% in one year seems a bit much to me, almost as if you’re just violently swinging from one extreme to another.

Still, I do think CFRA sums up the overall situation pretty well with this passage: “A sharp decline in smartphone demand, specifically in China and within the Android ecosystem, as well as easing of industry supply constraints, led to elevated channel inventory that will likely take until the middle of [calendar year] [2023] to normalize. We think this will also have negative implications to pricing, while the pending loss of Apple’s modem business (likely FY [2025]) will keep sentiment depressed, in our view. That said, we like increasing momentum outside of handsets, with autos growing 58% and pipeline now exceeding $30B.”

Qualcomm is still in the middle of correcting its prior overreliance on handsets.

This involves an ongoing shift toward IoT, especially via autos – the average modern car now requires well over 1,000 semiconductor chips.

And that explains the massive backlog, which CFRA touched on.

CFRA adds this on Qualcomm’s diversification strategy: “Despite challenging handset revenue (-18%), we are also impressed with [Qualcomm’s] diversification strategy, with a shift away from Apple given the expected business loss in FY [2025].”

That said, the handset space is still quite lucrative.

It’s been made to be even more lucrative over the last few years, via the adoption of 5G.

CFRA states this: “[Qualcomm] has also benefited from 5G adoption and content gains from the ongoing shift to higher-end devices, given its offerings span baseband, transceiver, RF front end, and antennas.”

Distilling it down, the 19% forecast from last year seemed to be too aggressive.

Likewise, I think this year’s 1% forecast is too cautious.

I’m somewhere in the middle.

Now, Qualcomm is navigating tough comps this year, as FY 2021 and part of FY 2022 featured above-average growth that was unsustainable.

And so this year, in particular, could be tough from a YOY growth standpoint.

But Qualcomm’s future, looking out toward FY 2024 and beyond, is about as exciting as I can remember.

If we assume pretty modest mid-single-digit EPS growth over the next year or two, that still sets up Qualcomm for continued high-single-digit dividend growth – the payout ratio gives them the room for it.

Even flat EPS growth could allow for this.

From there, the door’s open for a nice acceleration in both EPS growth and dividend growth over the following years.

And you’re starting this whole thing off with a 2.8% yield.

I think that’s a pretty nice setup.

Financial Position

Moving over to the balance sheet, Qualcomm has a rock-solid financial position.

The long-term debt/equity ratio is 0.8, while the interest coverage ratio is almost 27.

Profitability is extremely healthy.

Over the last five years, the firm has averaged annual net margin of 15.7% and annual return on equity of 77.8%.

Overall, I view Qualcomm as a fantastic tech business that is on the forefront of the digital transformation, which is something that should handsomely reward shareholders over time.

And with IP, R&D, economies of scale, pricing power, and switching costs, the business does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Litigation has been a notable issue for Qualcomm for several years.

Qualcomm has a near-monopoly on CDMA technology patents, and these valuable patents (and the lucrative royalty fees they generate) have led to contentious legal battles worldwide.

The very business model is a risk unto itself, as the ever-faster pace of change across technology means that Qualcomm will have to constantly evolve in order to keep pace and remain competitive.

Handset makers have been vertically integrating, which threatens Qualcomm’s handset chip business.

A number of Qualcomm’s end markets are still relatively new, introducing questions and uncertainty about the long-term prospects of these markets.

Being an international business, Qualcomm faces geopolitical risks and currency exchange rates.

These risks strike me as acceptable when viewed against the quality and growth of the business.

And with the stock down about 30% from its recent high, the valuation has become about as attractive as I’ve ever seen it…

Stock Price Valuation

The P/E ratio is 10.9.

This is obviously well below the broader market’s earnings multiple.

It’s also sitting at less than half of its own five-year average of 24.2.

A stunning discount here.

The P/CF ratio of 12.6 is also well off of its own five-year average of 19.3.

And the yield, as noted earlier, is in line with its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

This dividend growth rate isn’t as high as I can go, but it is near the top.

I scaled things back just slightly for Qualcomm, as the near-term picture around demand for some of its products is so cloudy.

The next year or two could be subdued in terms of the size of dividend raises.

However, once Qualcomm moves past this “air pocket”, the acceleration across the business could be rapid.

Keep in mind, the most recent dividend raise – announced less than two months ago – came in at almost 7%, despite this being a very challenging year for comps.

If that’s pretty close to the worst, I’m optimistic about the best.

With the payout ratio being as low as it is, and with Qualcomm’s dividend growth resume being as strong as it is, I would be highly surprised if the company fails to average out with a high-single-digit dividend growth rate over the next decade or so.

The DDM analysis gives me a fair value of $137.60.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I really do believe that my valuation model was realistic, yet the stock’s price looks surprisingly cheap against that valuation.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates QCOM as a 4-star stock, with a fair value estimate of $140.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates QCOM as a 3-star “HOLD”, with a 12-month target price of $140.00.

Very tight consensus here. Averaging the three numbers out gives us a final valuation of $139.20, which would indicate the stock is possibly 19% undervalued.

Bottom line: Qualcomm, Inc. (QCOM) is a terrific business that is leading the charge on the digital transformation, all while diversifying its business into exciting new growth areas of technology. It has a great balance sheet and high returns on capital. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, more than 20 consecutive years of dividend increases, and the potential that shares are 19% undervalued, long-term dividend growth investors lacking tech exposure should take a very close look at this name right now.

Bottom line: Qualcomm, Inc. (QCOM) is a terrific business that is leading the charge on the digital transformation, all while diversifying its business into exciting new growth areas of technology. It has a great balance sheet and high returns on capital. With a market-beating yield, a double-digit long-term dividend growth rate, a low payout ratio, more than 20 consecutive years of dividend increases, and the potential that shares are 19% undervalued, long-term dividend growth investors lacking tech exposure should take a very close look at this name right now.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is QCOM’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 80. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, QCOM’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income